KGI DAILY TRADING IDEAS – 5 November 2021

Singapore Trading Ideas | Hong Kong Trading Ideas | Market Movers | Trading Dashboard

SINGAPORE

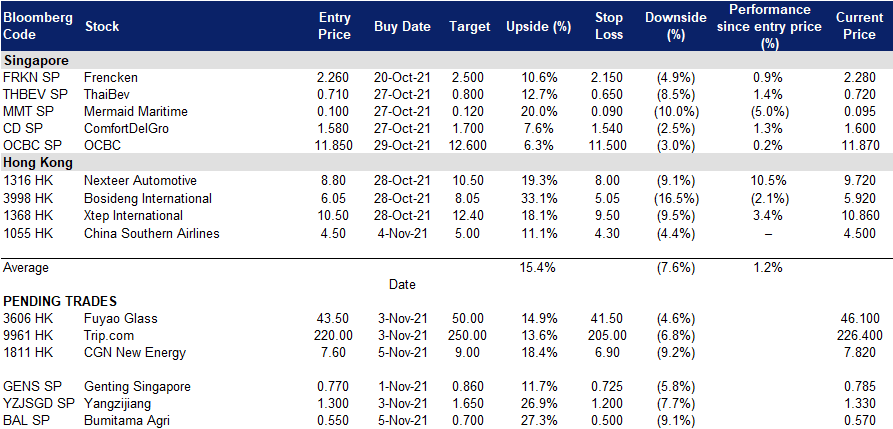

Bumitama Agri (BAL SP): Palm oil prices to the moon

- BUY Entry – 0.55 Target – 0.70 Stop Loss – 0.50

- A palm oil play. Bumitama Resources is a leading producer of palm oil and palm kernel in Indonesia. The group has a total planted area of 187,917 hectares and operates 14 CPO mills with a combined processing capacity of 6mn tonnes of fresh fruits bunches annually.

- To the moon. Palm oil, the most consumed edible oil, has been leading this year’s rally in global vegetable oil markets. Palm oil futures recently traded above RM5,000 per tonne, the highest on record, and an increase of more than 60% from the start of the year. The key reason has been lower supplies in Malaysia, lower crop yields of alternatives such as canola, and stronger-than-expected demand as economies reopen.The Malaysian Palm Oil Association warned that output in the world’s second largest producer may drop to 18mn tonnes in 2021, which will be more than 1mn lower than in 2020.

- Potential to exceed estimates. Consensus estimates are mixed, with 2 Buys and 2 Holds, and a 12m TP of S$0.65 (+14% potential upside). The low expectations may provide upside, given that Bumitama’s valuations are relatively cheap at 8.5x FY2021 P/E, a 30% discount to Wilmar’s 12.6x FY2021 P/E.

Bursa Malaysia Ringgit Denominated Crude Palm oil Futures

Bumitama Agri Share Price

Yangzijiang Shipbuilding (YZJSGD SP): Danger or opportunity

- REITERATE BUY Entry – 1.30 Target – 1.65 Stop Loss – 1.20

- China’s largest private shipbuilder. Yangzijiang is China’s largest private shipbuilder. The company builds a broad range of commercial vessels including containerships, bulk carriers and LNG vessels. Yangzijiang has been at the forefront of shipbuilding in China, receiving its first ever 24,000 TEU containership order in December 2020, the largest containership currently operating in the world.

- Poor 3Q earnings. Shares of Yangzijiang fell 5% yesterday after its 3Q2021 numbers failed to impress. While 3Q revenue surged 45% YoY to RMB3.7bn, gross profit dropped 30% YoY to RMB0.5bn, mainly as gross profit margin fell to 13% (from 27% in the prior year) due to higher raw material costs.

- Potentially better 4Q. Due to the power crunch in China, there were some constraints to the company in September and October. However, management has said that since the start of November, restrictions and constraints on electricity usage have eased and the shipyards are back to normal operations. Furthermore, we note that raw material prices have also come down in 4Q2021.

- Upside catalyst from potential spin-off of investment portfolio. Yangzijiang is currently conducting a preliminary strategic review of its debt investment portfolio to focus on shipbuilding. The potential listing of Yangzijiang’s debt securities portfolio, which makes up 50% of gross profit, could provide a rerating to its share price.

- Positive consensus estimates. Valuations are still attractive at 8x/7x/6x FY21/22/23 PE, while trading at a 25% discount to historical book value. Cash & cash equivalents make up almost 80% of its current market cap. Consensus currently has 7 BUYS, 1 HOLD and 1 SELL, and a 12m TP of S$1.77.

HONG KONG

CGN New Energy Holdings Co Ltd (1811 HK): Bullish trend intact

- Buy Entry – 7.6 Target – 9.0 Stop Loss – 6.9

- CGN New Energy Holdings Co., Ltd. is an investment holding company mainly engaged in the operation of power plants. Along with subsidiaries, the Company operates its business through three segments. The Power Plants in Korea segment is engaged in the generation and supply of electricity. It is involved in the projects, including Daesan I Power Project, among others. The Power Plants in the PRC segment is engaged in the generation and supply of electricity. It mainly engages in wind power and solar power projects. The Management Companies segment is engaged in the provision of management services to power plants operated by CGN and its subsidiaries. The Company is involved in the wind, solar, gas-fired, coal-fired, oil-fired, hydro, cogen and fuel cell and steam projects.

- Key financial highlights:

| (USD mn) | 1H21 | 1H20 | YoY change |

| Revenue | 797 | 593 | 34.4% |

| Gross profit | 454 | 323 | 40.6% |

| GPM (%) | 57.0 | 54.5 | 2.5 ppt |

| Net profit | 162 | 104 | 55.8% |

| NPM (%) | 20.3 | 17.5 | 2.8 ppt |

- September operation updates. The power generation of the company and its subsidiaries on a consolidated basis grew by 11.4% YoY to 1,368.9 GWh. Power generation of PRC wind and solar projects grew by 67.8% and 8.6% YoY respectively. Power generation of PRC cogen and gas-fired and hydro projects dropped by 64.3% and 30.7% YoY respectively. Power generation of Korea projects dipped by 2.9% YoY.

- Opportunities from the energy crisis in China. The skyrocketing coal prices this year caused China power shortage from 2Q21 to 3Q21 as coal-fired power is the dominant source of electricity supply. Authorities have increasingly realized the importance of balancing the energy consumption structure. Meanwhile, China has set the carbon-neutrality goal last year, complying with the global climate advocations. Hence, China has a long way to go for the clean energy deployment. Wind and solar are the two main alternative energy supplies that China is aggressively promoting to develop.

- Consensus estimates per the 12-month target price is at HK$4.32. EPS is forecasted to grow at 35.5%/11.7%/25% for FY2021/22/23F, which would bring forward P/Es down to 19.7x/17.6x/14.0x FY2021/22/23F.

TRIP.COM (9961 HK): Contrarian trade, buy the dip when lockdown comes

- REITERATE Buy Entry – 220 Target – 250 Stop Loss – 205

- Trip.com Group Limited, formerly Ctrip.com International, Ltd., is a travel service provider in China that provides accommodation booking, transportation ticketing, package tours and corporate travel management. The company aggregates hotel and transportation information to help leisure and business travellers make reservations. The company helps leisure travellers book travel packages and guided tours and helps corporate clients manage their travel needs. The company also offers a range of travel-related services to meet the different booking and travel needs of leisure and business travellers, including visitor reviews, attraction tickets, travel-related financial services, car services, travel insurance services and passport services. The company also offers package tours for independent leisure travellers, including tour groups, semi-tour groups and private groups, as well as package tours that require different transportation arrangements (such as cruise, buses or self-driving).

- Speed bump again. Tourism and recreation sector is on a tortuous path of recovery. Countries who have 60% to 70% of vaccination rates gradually open the borders. However, China still strictly adopts the zero-infection policy domestically. Recently, there were rising infection cases in China, and related cities and districts were locked down again. This led to the sell-down of the stock, breaking the recovery of price. However, it is a buying opportunity now as the past performance showed a resiliency to such kind of news.

- Promising recovery against COVID-19. Previously, the company announced 1H21 results. Total net revenue increased by 86% YoY and 43% QoQ to RMB10bn, driven by the strong recovery momentum of the China domestic market. Both domestic hotel and air-ticket GMV increased by about 150% YoY. Compared with the same pre-COVID period in 2019, both domestic hotel and air ticketing reservations achieved double-digit growth in 2Q21. Staycation travel continues to serve as a major driver of domestic recovery with local hotel reservations growing nearly 80% versus pre-COVID period in 2019. Revenues from corporate travel management grew 141% year over year and 26% compared with the pre-COVID period in 2019. In 1H21, the company reported a net profit of RMB 1bn compared to a net loss of RMB 5.8bn during the same period last year.

- Best performance among all the e-commerce large-cap Chinese companies. The crackdown of multiple sectors hammered share prices of technology stocks. Currently, there is no obvious sign of turnaround. However, tourism is one of the few sectors that are relatively immune to policy risks. The price performance of the company showed positive signs of turnaround amidst the recent bearish market sentiment.

- The updated market consensus of the estimated net profit growth in FY22 and FY23 is 383.1% and 51.6% respectively, which translates to 27.4x and 18.1x forward PE. Bloomberg consensus average 12-month target price is HK$286.36.

Market Movers

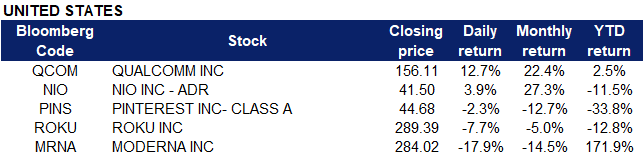

United States

- Moderna (MRNA US) shares plummeted 12.1% in premarket trading on Thursday, after the biotech company announced third quarter financial results that missed analyst expectations. Revenue was at $5 billion, and earnings per share at $7.70, compared to consensus estimates of $6.2 billion and $9.05 respectively. Moderna also cut its fiscal 2021 full-year product sales forecast to between $15-18 billion, down from its previous projection of $20 billion. The stock closed 17.9% lower at $284.02

- Qualcomm (QCOM US) shares jumped 8.3% in premarket trading, before closing 12.73% higher at $156.11. The company posted stronger than expected profits of $2.55 per share with record high revenues of $9.32 billion for the three months ending in September. Qualcomm also forecasts strong growth, driven by demands for 5G smartphone technology.

- Pinterest (PINS US) gained 6% in after hours trading after closing at its lowest in a year during the regular trading session. The company reported better than expected earnings and revenue for the third quarter. Adjusted earnings per share was at $0.28 vs estimates of $0.23, revenue was at $633 million vs expectations of $630.9 million, monthly active users came in at 444 million vs 460 million. This was the second quarter in a row that Pinterest saw a drop in monthly active users. Pinterest did not comment on the rumors of a potential takeover by Paypal.

- Roku (ROKU US) shares slid 7.7% after the company reported worse than expected third quarter results. Quarterly adjusted EBITDA was at $130.1 million, up from $56.2 million YOY. Quarterly revenue was $680 million, which came in below the estimate of $683.67 million. Roku expects fourth-quarter net sales of $893 million versus the estimate of $944.43 million.

- Nio (NIO US) shares jumped nearly 4% after Deutsche Bank analysts boosted their target price on the stock by $10 to $70 per share. The Chinese electric vehicle maker previously reported October deliveries of only 3,667 vehicles, citing supply chain issues and downtime to upgrade assembly lines for additional capacity. However, Nio co-founder Qin Lihong said that the company has maintained an order book above 10,000 vehicles for several months in a row, which was what prompted Deutsche Bank analyst Edison Yu to raise his delivery expectations for 2022 by 10,000 vehicles to 160,000 and up to 285,000 for 2023.

Singapore

The Singapore market was closed yesterday in observance of a public holiday (Deepavali). Trading resumes today, 5 November.

Hong Kong

Top Sector Gainers

| Sector | Gain | Related News |

| Electric Equipment | +4.50% | China’s Wind Giants Hatch Plans to Muscle In on U.S., Europe |

| Environmental Energy Material | +2.98% | Founder Of China’s Top Solar Panel Maker Rides Global Demand For Renewable Energy |

| Industrial Goods | +2.00% | Top Solar Firm Longi Says U.S Customs Detained Products |

Top Sector Losers

| Sector | Loss | Related News |

| Petroleum & Gases | -2.28% | Oil prices tumble as U.S. intensifies pressure on OPEC for more crude |

| Property Management & Agency | -1.44% | Chinese developer Kaisa unit misses payment, debt worries mount |

| Precious Metal | -0.97% | Fed Will Start Tapering in December 2021 |

- Xinjiang Goldwind Science & Tech Co Ltd (2208 HK), Dongfang Electric Corp Ltd (1072 HK), CGN New Energy Holdings Co Ltd (1811 HK). Clean energy power generation stocks rose collectively yesterday. Shares rose 11.6%, 8.6% and 7.3% respectively. Yesterday, it was announced that China is targeting a 1.8% reduction in average coal use for electricity generation at power plants over the next 5 years, in a bid to lower greenhouse gas emissions. In addition, Citic Securities maintained its BUY rating on Dongfang Electric with a TP of HK$17. The report stated that wind power was the main revenue contributor in the first three quarters of about 84%, with 26,772,800 kilowatts production, a YoY increase of 49.21%. The bank also stated that the company would benefit from China’s 14th Five-Year Plan, with expected increase in capacity of nuclear power, pumped storage and wind power.

- GCL-Poly Energy Holdings Ltd (3800 HK). Shares rose 8.8% yesterday as Credit Suisse issued a report with a BUY rating on GCL-Poly with a TP of HK$4. The company’s revenue in the first half of the year was RMB 8.779bn, a YOY increase of 22.3%. The increase in revenue was mainly due to a YOY increase in the average price of silicon materials by approximately double. In the first half of the year, the company generated a net profit attributable to shareholders of RMB 2.41bn, compared to losses of RMB 1.996bn in the same period last year. The bank believes that the company’s share price adjustment of 24% in the past two days may be due to profit-taking and believes that this pullback has created an attractive buying point for the GCL-Poly.

- BYD Co Ltd (1211 HK). Shares rose 7.8% yesterday as Daiwa Securities issued a report reiterating its BUY rating on BYD, with a TP of HK$382. The report stated that the company is expected to benefit from the strong prospects of electric vehicle sales and the demand for lithium iron phosphate batteries. The company’s sales reached nearly 90,000 passenger vehicles and commercial vehicles in October this year, representing an increase of 88% YoY and 12% MoM. BYD pointed out that the sales of pure electric vehicles were driven by the “Han” and “DM-i” models, whereas the sales of gasoline vehicles fell 64% YoY.

- Trading Dashboard: Hua Hong semiconductor (1347 HK) took profit at HK$44.2, Hainan Meilan Airport (357 HK) cut loss at HK$29; Add China Southern Airlines (1055 HK) at HK$4.5.

Trading Dashboard

Related Posts: