Technical Analysis – 7 March 2024

United States | Singapore | Hong Kong | Earnings

Prudential Financial, Inc. (PRU US)

- Shares closed at a 52-week high with constructive volume.

- MACD just turned positive, RSI is constructive.

- Long – Entry 109, Target 115, Stop 106

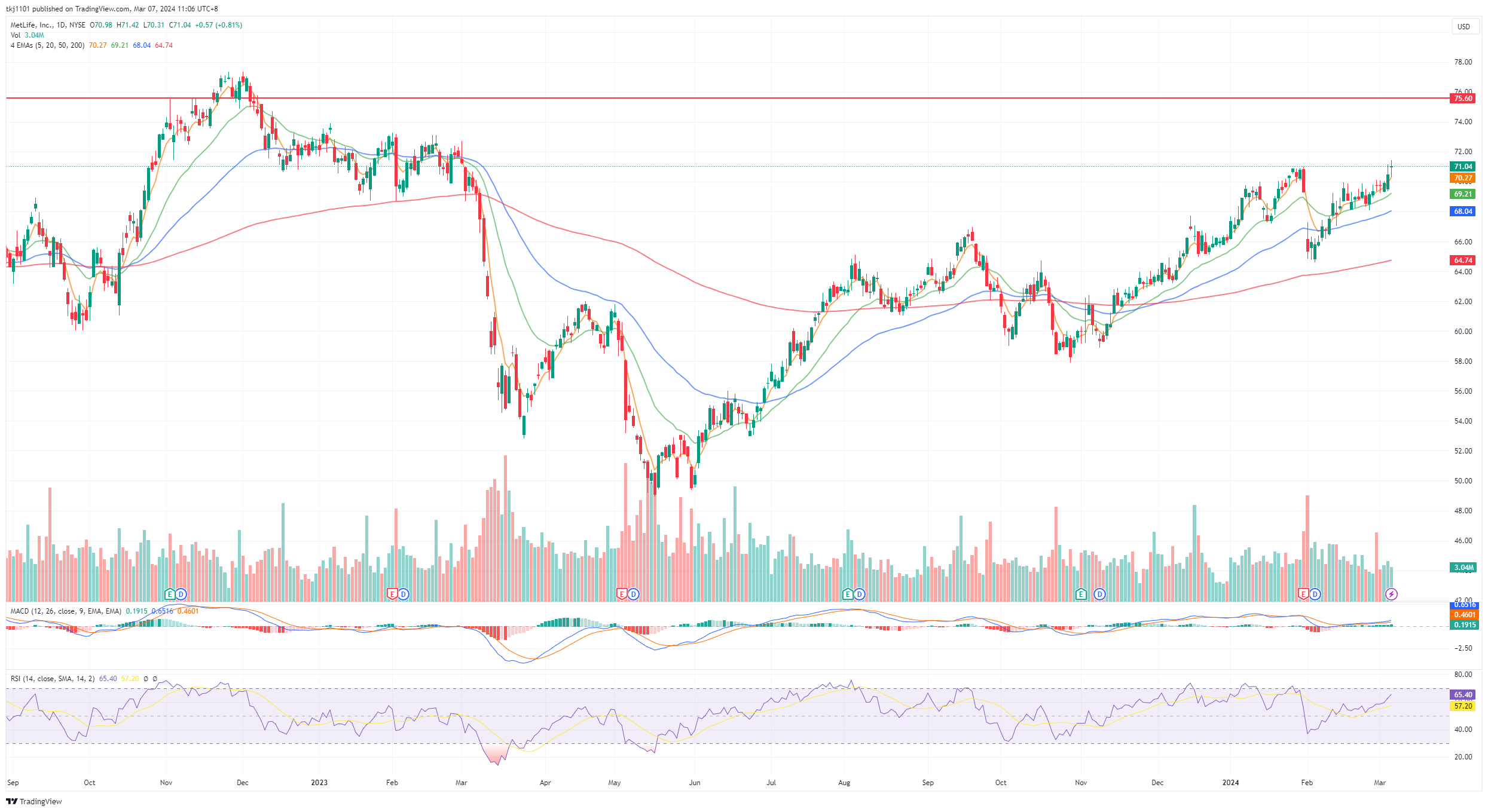

Metlife, Inc. (MET US)

- Shares closed at a 52-week high.

- MACD is positive, RSI is constructive.

- Long – Entry 70.6, Target 75.6, Stop 68.1

Samudera Shipping Line Ltd. (SAMU SP)

- Shares closed higher above the 5dEMA with a surge in volume volume.

- MACD is positive, RSI is constructive.

- Long – Entry 0.740, Target 0.840, Stop 0.690

Aztech Global Ltd. (AZTECH SP)

- Shares closed at a 52-week high with constructive volume.

- MACD is positive, RSI is at an “overbought” level.

- Long – Entry 1.01, Target 1.09, Stop 0.97

China Mobile Ltd (941 HK)

- Shares closed above the 5dEMA.

- RSI is constructive and MACD is negative.

- Long – Entry 67.2, Target 70.0, Stop 65.8

China Unicom Hong Kong Ltd (762 HK)

- Shares closed above the 5dEMA.

- RSI is constructive, while MACD is about to turn positive.

- Long – Entry 5.66, Target 5.96, Stop 5.51

NIO Inc (NIO)

- 4Q23 Revenue: $2.41B, +6.5% YoY, beat estimates by $70M

- 4Q23 Non-GAAP EPADS: –$0.39, miss estimates by $0.07

- 1Q24 Guidance: Deliveries of vehicles to be between 31,000 and 33,000 vehicles, representing a decrease of approximately 0.1% to an increase of approximately 6.3% from the same quarter of 2023; Total revenue to be between RMB10,499mn (US$1,479mn) and RMB11,087mn (US$1,562mn) vs consensus of $2.28bn, representing a decrease of approximately 1.7% to an increase of approximately 3.8% from the same quarter of 2023.

- Comment: NIO Inc’s reported a mixed set of results. While the company saw a YoY growth in vehicle deliveries, QoQ deliveries fell, highlighting a lackluster demand for EVs. The company also provided weak guidance for vehicle deliveries in 1Q24, representing a decrease of 34% to 38% from the previous quarter. A price war between EV companies has also continued pushing the price of EVs down across the market, amidst slowing growth and rising competition. The company also sees a further 1% decline in ASP compared to 4Q23. The company delivered a total of 18,187 vehicles in January and February, which means that the company expects at least 12,800 vehicle deliveries in March, which may indicate a recovery in EV demand. The company also mentioned they will begin deliveries of 2024 NIO products equipped with the highest computing power among production vehicles and constantly enhance users’ driving and digital experience. 1Q24 recommended trading range: $3.50 to $6.50. Neutral Outlook.

蔚来(NIO)

- 23财年第四季营收:24.1亿美元,同比增加6.5%,超预期7,000万美元

- 23财年第四季Non-GAAP每股亏损:0.39美元,超预期0.07美元

- 24财年第一季指引:汽车交付量介于31,000辆至33,000辆之间,与2023年同期相比减少约0.1%至增长约6.3%;总收入介于104.99亿元人民币(14.79亿美元)至1108.7亿元人民币(15.62亿美元)之间,而市场预期为22.8亿美元,较2023年同期下降约1.7%至增长约3.8%。

- 短评:蔚来汽车公布的业绩喜忧参半。虽然该公司的汽车交付量同比增长,但季度交付量下降,突显出电动汽车需求低迷。该公司还对第一季度的汽车交付量给出了疲弱的指引,较上一季度下降了34%至38%。在增长放缓、竞争加剧的情况下,电动汽车公司之间的价格战也在继续压低整个市场的电动汽车价格。该公司还预计,与去年第四季度相比,平均售价将进一步下降1%。该公司在1月和2月共交付了18187辆汽车,这意味着该公司预计3月份至少交付了12800辆汽车,这可能预示着电动汽车需求的复苏。蔚来还表示,将从2024年开始交付在量产车型中配备最高计算能力的蔚来产品,并不断提升用户的驾驶和数字体验。24财年第一季度建议交易区间:3.5美至6.5美元。中性前景。

Target Corp (TGT)

- 4Q23 Revenue: $31.47B, +1.6% YoY, miss estimates by $400M

- 4Q23 Non-GAAP EPS: $2.98, beat estimates by $0.56

- 1Q24 Guidance: Expect a comparable sales decline of 3% to 5%; GAAP and adjusted EPS are both expected to range from $1.70 to $2.10 vs $2.10 consensus. FY24 Guidance: Expect a modest increase in comparable sales in a range from flat to 2%. GAAP EPS and Adjusted EPS are both expected to range from $8.60 to $9.60 vs $9.14 consensus.

- Comment: Target posted a mixed set of results but provided better-than-expected guidance. The company’s revenue, while missing expectations, was helped by robust Black Friday and Cyber Monday spending. Looking ahead, the company will be focused on rolling out new products and services to reignite sales, traffic, and market share gains in 2024. The company announced that it will be relaunching the Target Circle loyalty program, including a new paid version that will launch next month, called Target Circle 360, which would offer shoppers unlimited same-day delivery. This new membership feature aims to lure back shoppers who have turned to other retailers, helping the company gain back market share. The company also plans to open new stores and grow its private-label brands. Improving consumer sentiment in 2024 is likely to bolster sales recovery for the company as well. 1Q25 recommended trading range: $160 to $185. Positive Outlook.

目标百货 (TGT)

- 23财年第四季营收:314.7亿美元,同比增加1.6%,逊预期4.0亿美元

- 23财年第四季Non-GAAP每股盈利:0.15美元,超预期0.07美元

- 24财年第一季指引:预计可比销售额将下降3%至5%; GAAP和调整后每股收益预期均在1.70美元至2.10美元之间,而市场预期为2.10美元。24财年指引:预计可比销售额将在持平至2%的范围内小幅增长。预计GAAP每股收益和调整后每股收益均在8.60美元至9.60美元之间,而市场预期为9.14美元。

- 短评:目标百货公布了喜忧参半的业绩,但提供了好于预期的指引。该公司的营收虽然不及预期,但得益于“黑色星期五”和“网络星期一”的强劲消费。展望未来,该公司将专注于推出新产品和服务,以在2024年重振销售、流量和市场份额。该公司宣布将重新推出Target Circle忠诚度计划,其中一个新的付费版本将于下个月推出,名为Target Circle 360,它将为购物者提供无限制的当日送达服务。这个新的会员功能旨在吸引那些转向其他零售商的顾客,帮助公司重新获得市场份额。该公司还计划开设新店,发展自有品牌。2024年消费者信心的改善可能也会提振该公司的销售复苏。25财年第一季度建议交易区间160美至185美元。积极前景。

CrowdStrike Holdings Inc (CRWD)

- 4Q24 Revenue: $845.3M, +32.6% YoY, beat estimates by $5.34M

- 4Q24 Non-GAAP EPS: $0.95, beat estimates by $0.13

- 1Q25 Guidance: Q1 total revenue of $902.2 – $905.8mn vs. consensus of $901.12mn, Non-GAAP EPS of $0.89 – $0.90 vs $0.82 consensus. FY25 Guidance: FY25 Total revenue of $3924.9mn – $3989mn, vs. consensus of $3.94bn, Non-GAAP EPS of $3.77 – $3.97 vs $3.76 consensus.

- Comment: CrowdStrike holdings posted a strong set of results, and provided a better than expected guidance. The company forecasts stronger demand for its cybersecurity platform and emphasizes on its single-platform, Falcon platform which is data-centric, AI native, and scalable, delivering immediate times, favored by customers. The company expects 1Q25 net new ARR YoY growth to be at least double digits up to the low teens. The company plans to increase hiring in FY25, riding on its current strong momentum continue to invest in its innovation engine and go-to-market functions to scale the business further. The company also announced that it would be acquiring Flow Security, the industry’s first and only cloud data runtime security solution, for an undisclosed price in a cash-and-stock deal, slated to close in the company’s fiscal first quarter. 1Q25 recommended trading range: $350 to $420. Positive Outlook.

CrowdStrike (CRWD)

- 24财年第四季营收:8.453亿美元,同比增加32.6%,超预期534万美元

- 24财年第四季Non-GAAP每股盈利:0.95美元,超预期0.13美元

- 25财年第一季指引:第一季度总收入为9.022亿至9.058亿美元,市场预期为9.0112亿美元;Non-GAAP每股收益为0.89至0.90美元,市场预期为0.82美元。25财年指引:25财年总收入为3.9249亿至3.989亿美元,市场预期为39.4亿美元,Non-GAAP每股收益为3.77至3.97美元,市场预期为3.76美元。

- 短评:CrowdStrike公布了一系列强劲的业绩,并提供了好于预期的指导。该公司预测其网络安全平台的需求将会更强劲,并强调其单一平台Falcon平台,该平台以数据为中心,人工智能原生,可扩展,可即时交付,受到客户的青睐。该公司预计,第一季度新年华经常性收入(ARR)同比净增长率将至少达到两位数,达到10%左右。该公司计划在25财年增加招聘,利用目前的强劲势头继续投资于其创新引擎和上市功能,以进一步扩大业务规模。该公司还宣布,将以现金加股票的方式收购业界首个也是唯一一个云数据运行时安全解决方案Flow Security,交易价格未公开,预计将在公司第一财季完成。25财年第一季度建议交易区间350美至420美元。积极前景。

Ross Stores Inc (ROST)

- 4Q23 Revenue: $6.02B, +15.5% YoY, beat estimates by $210M

- 4Q23 GAAP EPS: $1.82, beat estimates by $0.17

- 4Q23 Dividend: Ross Stores declares $0.3675/share quarterly dividend, 9.7% increase from prior dividend of $0.3350. Payable March 29; for shareholders of record March 15; ex- div March 14. The company’s BOD also approved a new 2 year $2.1bn stock repurchase authorization for FY24 and FY25.

- 1Q24 Guidance: Comparable store sales expect to be up 2% to 3% with earnings per share projected to be $1.29 to $1.35, up from $1.09 in 1Q23. FY24 Guidance: Expects same-store sales to grow 2% to 3% on top of a solid 5% gain in 2023; Expects EPS to be $5.64 to $5.89 compared to $5.56 in FY23, which included an estimated per share benefit of $0.20 from the 53rd week.

- Comment: Ross Stores posted a solid set of results. Operating margin rose to 12.4% from 10.7% YoY, thanks to “strong gains” in same-store sales and lower freight costs. However, management remains conservative in forecasting their business for FY24. While inflation has moderated, ongoing macroeconomic and geopolitical uncertainty remains, and management highlights that consumers are still facing the pressure of elevated prices, especially those in low to middle-income levels. The company still expects these lower-income customers to continue to limit their purchases to necessities such as groceries in the near term. The company remains focused on delivering a wide assortment of quality branded bargains for customers, which they think would be the key drive to gain market share. On the other hand, competitors, such as Target, are launching new products and services to attract more customers and gain customer loyalty to increase their market shares. 1Q24 recommended trading range: $135 to $155. Neutral Outlook.

罗斯百货 (ROST)

- 24财年第四季营收:1.638亿美元,同比增加33.3%,超预期554万美元

- 24财年第四季GAAP每股盈利:1.82美元,超预期0.17美元

- 23财年第四季股息:罗斯百货宣布每股0.3675美元的季度股息,比之前的0.3350美元股息增加9.7%。3月29日付款;3月15日股东登记;3月14日除息。公司董事会还批准了24财年和25财年为期2年的21亿美元股票回购授权。

- 24财年第一季指引:可比门店销售额预计增长2%至3%,每股收益预计为1.29至1.35美元,高于23年第一季度的1.09美元。24财年指引:24财年指引:预计同店销售额在2023年稳步增长5%的基础上增长2%至3%;预计每股收益为5.64美元至5.89美元,而23财年为5.56美元,其中包括从第53周开始的每股收益0.20美元。

- 短评:罗斯百货公司公布了一系列稳定的业绩。营业利润率从上年同期的10.7%上升至12.4%,这得益于同店销售额的“强劲增长”和运费成本的降低。然而,管理层在预测其24财年业务方面仍持保守态度。虽然通货膨胀有所缓和,但宏观经济和地缘政治的不确定性仍然存在,管理层强调消费者仍然面临价格上涨的压力,特别是中低收入人群。该公司仍预计,这些低收入消费者短期内将继续限制购买杂货等必需品。该公司仍然专注于为客户提供各种各样的优质品牌便宜货,他们认为这将是获得市场份额的关键动力。另一方面,竞争对手,如目标百货,正在推出新的产品和服务,以吸引更多的客户,获得客户的忠诚度,以增加他们的市场份额。24财年第一季度建议交易区间135美至155美元。中性前景。

Nordstrom Inc (JWN)

- 4Q23 Revenue: $4.42B, +2.3% YoY, beat estimates by $40M

- 4Q23 Non-GAAP EPS: $0.96, beat estimates by $0.07

- 1Q24 Guidance: Expect results to be near break-even to a slight loss. FY24 Guidance: Expect revenue to be between down 2% and up 1% vs estimates of a 0.04% rise and annual profit per share in a range of $1.65 to $2.05, vs analysts consensus of $1.98.

- Comment: Despite reporting better-than-expected fourth-quarter revenue and earnings, Nordstrom’s forecast for annual results falls short of Wall Street expectations, indicating a sluggish recovery in consumer demand amid lingering inflation concerns. In Q4 the company banner net sales decreased by 3% and GMV decreased by 3.4%YoY, whereas net sales for Nordstrom Rack increased 14.6%. The company expects revenue for 2024 to range from a slight decrease of 2% to a slight increase of 1% and projected earnings per share below analysts’ estimates. Nordstrom expects to continue to face challenges, especially in its full-line stores, prompting a focus on its discount Rack stores and plans to open new locations to attract lower-income shoppers. In contrast, its competitor, Macy’s plans to concentrate on its luxury brands, Bloomingdale’s and Bluemercury, to target higher-earning customers. However, with plans to open 26 new Rack stores only this year and next spring, the turnaround for Nordstrom is likely to be seen in the longer term. 1Q24 recommended trading range: $18 to $21. Neutral Outlook.

诺德斯特龙 (JWN)

- 23财年第四季营收:44.2亿美元,同比增加2.3%,超预期4,000万美元

- 23财年第四季Non-GAAP每股盈利:0.96美元,超预期0.07美元

- 24财年第一季指引:预计结果将接近盈亏平衡或略有亏损。24财年指引:预计营收将在下降2%至增长1%之间,而分析师预期为增长0.04%;年度每股利润在1.65美元至2.05美元之间,而分析师预期为1.98美元。

- 短评:尽管诺德斯特龙公布的第四季营收和获利好于预期,但其年度业绩预估却不及华尔街的预期,表明在通胀担忧挥之不去的情况下,消费者需求复苏乏力。第四季度,该公司净销售额同比下降3%,GMV同比下降3.4%,而Nordstrom Rack的净销售额同比增长14.6%。该公司预计2024年收入将小幅下降2%至1%,每股收益低于分析师预期。诺德斯特龙预计将继续面临挑战,尤其是在其全线商店方面,这促使其将重点放在折扣店Rack上,并计划开设新店以吸引低收入购物者。相比之下,它的竞争对手梅西百货(Macy’s)计划专注于旗下的奢侈品牌布鲁明戴尔(Bloomingdale’s)和Bluemercury,以瞄准收入较高的客户。然而,诺德斯特龙计划仅在今年和明年春季就新开26家Rack门店,从长远来看,它的好转可能还需要一段时间。24财年第一季度建议交易区间18美至21美元。中性前景。