Technical Analysis – 17 August 2023

United States | Singapore | Hong Kong | Earnings

Suncor Energy, Inc. (SU US)

- Shares closed higher above the 5dEMA with constructive volume. 20dEMA is about to cross the 200dEMA.

- MACD is positive, RSI is constructive.

- Long – Entry 31.5, Target 33.5, Stop 30.5

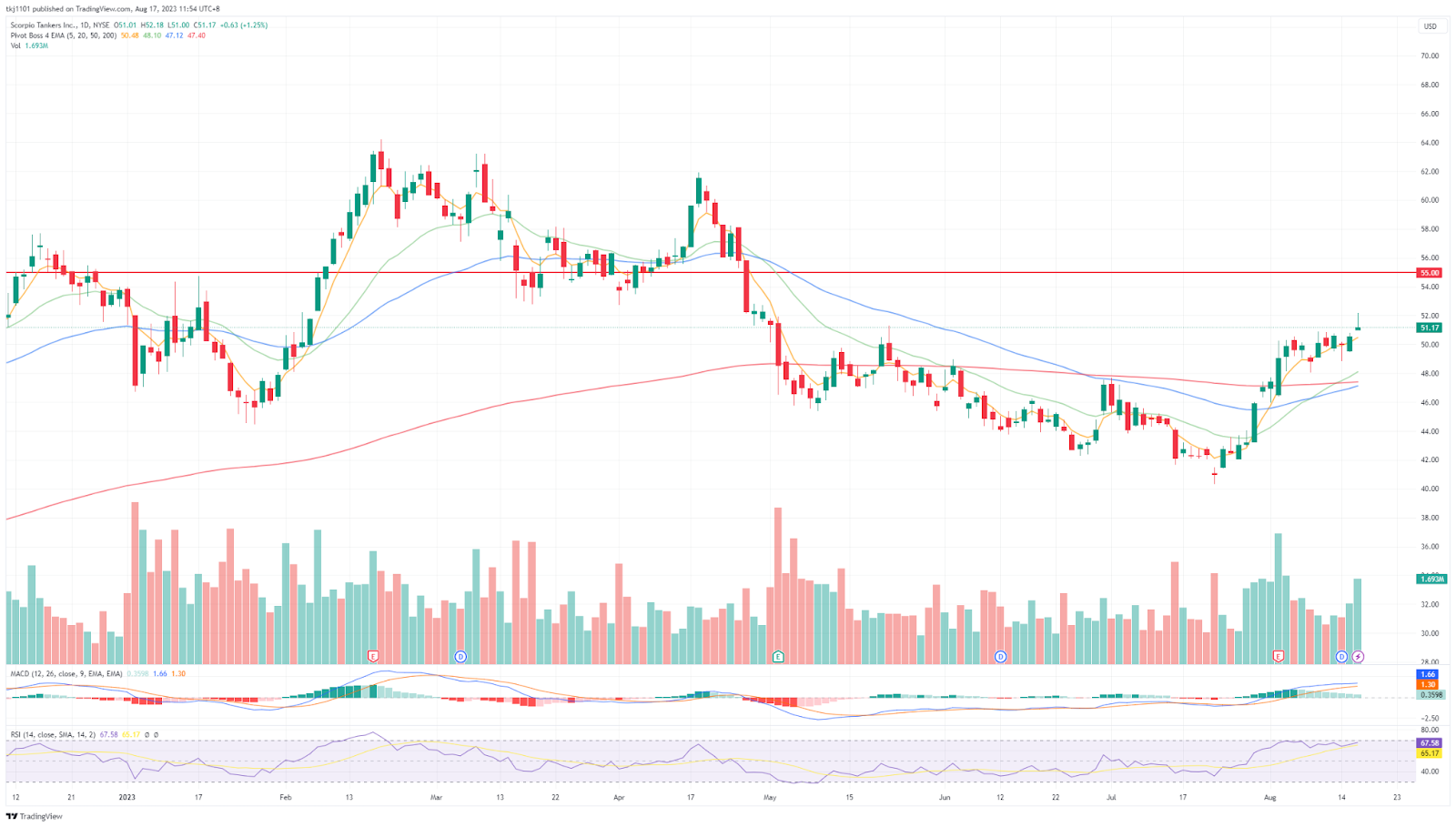

Scorpio Tankers, Inc. (STNG US)

- Shares closed higher above the 5dEMA with a surge in volume. 50dEMA is about to cross the 200dEMA.

- MACD is positive, RSI is constructive.

- Long – Entry 51, Target 55, Stop 49

Hongkong Land Holdings Ltd (HKL SP)

- Shares closed above the 20dEMA with an incline in volume. The 5dEMA is about to cross the 20dEMA.

- Both RSI and MACD are constructive.

- Long – Entry 3.65, Target 3.90 Stop 3.52

ComfortDelGro Corp Ltd (CD SP)

- Shares closed at a 9-month high, above the 5dEMA with a jump in volume.

- RSI is at an overbought level and MACD is about to turn positive.

- Long – Entry 1.27 Target 1.38, Stop 1.21

Sinopharm Group Co Ltd (1099 HK)

- Shares closed above the 5dEMA with rising volume.

- RSI is constructive, while MACD is negative.

- Long – Entry 21.3, Target 23.1, Stop 20.4

CGN Power Co Ltd (1816 HK)

- Shares closed above the 5dEMA. The 20dEMA recently crossed the 50dEMA.

- Both RSI and MACD are constructive.

- Long – Entry 2.00, Target 2.18, Stop 1.91

Target Corp (TGT)

- 2Q23 Revenue: $24.77B, -4.9% YoY, miss estimates by $460M.

- 2Q23 Non-GAAP EPS: $1.80, beat estimates by $0.38.

- FY23 Guidance: lowered its full year sales and profit expectations. The company now expects comparable sales in a wide range around a mid-single digit decline for the remainder of the year, and now expects full-year GAAP and Adjusted EPS of $7.00 to $8.00.

- Comment: The company reported better profits mainly attributed to fewer discounts and better stocked store shelves, but sales performed poorly as a result of Pride backlash. Going forward, the company expects a gloomier outlook as they think that consumers will not spend more than necessary. With mixed signals towards interest rates hike, the economy still has an uncertain outlook. However, consumer confidence appears to remain high for July and August, which might bring some positives for the company. 3Q23 recommended trading range: $120 to $140. Neutral Outlook.

塔吉特百货 (TGT)

- 23财年第二季营收:247.7亿美元, 同比跌幅4.9%,逊预期4.6亿美元

- 23财年第二季Non-GAAP每股盈利:1.80美元,超预期0.38美元

- 23财年指引:下调了全年销售和利润预期。该公司目前预计,在今年剩余时间内,可比销售额将在中等个位数左右的范围内下降,目前预计全年GAAP和调整后每股收益为7.00美元至8.00美元。

- 短评:该公司报告称,更好的利润主要归功于折扣减少和库存增加,但由于“骄傲月”的反弹,销售表现不佳。展望未来,该公司预计前景将更加黯淡,因为他们认为消费者不会超出必要的支出。由于加息的信号不一,经济前景仍不明朗。然而,7月和8月的消费者信心似乎仍然很高,这可能会给公司带来一些积极因素。23财年第三季度建议交易区间:120美元至140美元。中性前景。

JD.Com Inc (JD)

- 2Q23 Revenue: $39.7B, +7.6% YoY, beat estimates by $1.21B.

- 2Q23 Non-GAAP EPADS: $0.74, beat estimates by $0.06.

- 3Q23 Guidance: No guidance provided.

- Comment: The company posted a set of solid results, with the company seeing the number of their marketplace merchants more than doubled and reached a new record during the quarter, reflecting their efforts to build a superior marketplace ecosystem. However, the China market remains gloomy as the economy slights into deflation. Several economic data also re-emphasize the weak China market. Going forward, consumption is still expected to be low and this would still remain as a headwind for JD.com. 3Q23 recommended trading range: $28 to $38. Negative Outlook.

京东 (JD)

- 23财年第二季营收:397.0亿美元, 同比增幅7.6%,超预期12.1亿美元

- 23财年第二季GAAP每股盈利:0.74美元,超预期0.06美元

- 23财年第三季指引:不提供指引。

- 短评:该公司公布了一系列稳健的业绩,该公司看到其市场商家的数量增加了一倍多,并在本季度达到了新的记录,这反映了他们为建立一个卓越的市场生态系统所做的努力。然而,随着中国经济步入通货紧缩,中国股市依然低迷。一些经济数据也再次强调了中国市场的疲软。展望未来,预计消费仍将很低,这仍将是京东的逆风。23财年第三季度建议交易区间:28美元至38美元。负面前景。

TJX Companies Inc (TJX)

- 2Q24 Revenue: $12.76B, +7.8% YoY, beat estimates by $310M.

- 2Q24 GAAP EPS: $0.85, beat estimates by $0.07.

- 3Q24 Guidance: the company is planning overall comparable store sales to be up 3% to 4%, pretax profit margin to be in the range of 11.3% to 11.5%, and diluted EPS to be in the range of $0.95 to $0.98. FY24, the company is now planning overall comparable store sales to be up 3% to 4%; increasing its expectations for pretax profit margin to a range of 10.7% to 10.8% and diluted earnings per share to be in the range of $3.66 to $3.72; adjusted pretax profit margin to be in the range of 10.6% to 10.7% and adjusted diluted earnings per share to be in the range of $3.56 to $3.62.

- Comment: The company reported a strong sets of results, showcasing the strength of its off-price business model amidst a consumer slowing backdrop in 2Q24. The company benefitted from a surge in inventory that plagued full-price retails for the first half of 2022. While the macroeconomic environment remains uncertain, consumers are also more likely to only purchase goods that provide more value to them, which TJX is able to provide them with. Consumer confidence appears to remain high for July and August, bringing more positives for the company. 3Q24 recommended trading range: $84 to $100. Positive Outlook.

TJX 公司 (TJX)

- 24财年第二季营收:127.6亿美元, 同比增幅7.8%,超预期3.1亿美元

- 24财年第二季GAAP每股盈利:0.85美元,超预期0.07美元

- 24财年第三季指引:该公司计划整体可比门店销售额增长3%至4%,税前利润率在11.3%至11.5%之间,摊薄后每股收益在0.95美元到0.98美元左右。该公司目前计划在24财年将整体可比门店销售额提高3%至4%;将税前利润率预期提高至10.7%至10.8%区间,全年摊薄后每股收益预期提高至3.66美元至3.72美元区间;调整后的税前利润率在10.6%至10.7%之间,调整后的摊薄每股收益在3.56美元至3.62美元之间。

- 短评:该公司公布了一系列强劲的业绩,显示出在24财年第二季度消费放缓的背景下,其低价业务模式的实力。该公司受益于2022年上半年困扰全价零售的库存激增。虽然宏观经济环境仍然不确定,但消费者也更有可能只购买能为他们提供更多价值的商品,而TJX能够为他们提供这些商品。7月和8月消费者信心似乎保持在高位,为公司带来更多积极因素。23财年第三季度建议交易区间:84.0美元至100.0美元。积极前景。

Tencent Holdings Ltd (TCEHY)

- 2Q23 Revenue: $20.45B, +3.45% YoY, miss estimates by $372.58M.

- 2Q23 GAAP EPS: $0.53, miss estimates by $0.08.

- FY23 Guidance: No guidance provided. The company highlighted that its domestic games revenue should resume YoY growth in the third quarter of 2023.

- Comment: Tencent’s revenue growth slowed in 2Q23, as a sputtering economy weighed on its recovery from last year’s record downturn. The company’s core gaming business experienced weaker-than-expected growth, but revenue from online advertisements and fintech and business services grew. Tencent said that the government had become supportive of platform companies like Tencent and it expects “no material impact” from Beijing’s newly proposed rules to ban children from using smartphones for more than two hours a day. We anticipate that its growth will remain stagnant in the coming quarter as it faces intense competition and a lack of stimulus support from the Chinese government. 3Q23 recommended trading range: $35 to $42. Neutral Outlook.

腾讯 (TCEHY)

- 23财年第二季营收:204.5亿美元, 同比增幅3.45%,逊预期3.7258亿美元

- 23财年第二季GAAP每股盈利:0.53美元,逊预期0.08美元

- 23财年第三季指引:不提供指引。该公司强调,其国内游戏收入将在2023年第三季度恢复同比增长。

- 短评:腾讯的营收增长在23年第二季度放缓,原因是经济低迷拖累了该公司从去年创纪录的低迷中复苏。该公司核心游戏业务的增长低于预期,但在线广告、金融科技和商业服务的收入有所增长。腾讯表示,政府已经开始支持腾讯这样的平台公司,它预计北京新提出的禁止儿童每天使用智能手机超过两小时的规定“不会产生实质性影响”。我们预计,由于面临激烈竞争和中国政府缺乏刺激支持,下一季度中国的增长仍将停滞不前。23财年第三季度建议交易区间:35美元至42美元。中性前景。

Cisco Systems Inc (CSCO)

- 4Q23 Revenue: $15.2B, +16.0% YoY, beat estimates by $150M.

- 4Q23 Non-GAAP EPS: $1.14, beat estimates by $0.08.

- 1Q24 Guidance: Revenue $14.5 billion – $14.7 billion vs. consensus of $14.6B; Non-GAAP gross margin rate 65% – 66%; Non-GAAP operating margin rate 34% – 35%; Non-GAAP EPS $1.02 – $1.04 vs. consensus of $0.99. FY24 Revenue $57.0 billion – $58.2 billion vs. consensus of $58.37B; Non-GAAP EPS: $4.01 – $4.08 vs. consensus of $4.04.

- Comment: Cisco Systems mentioned that it is able to fill more orders now that the chip supply shortages have eased. However, the company’s revenue growth is expected to decelerate in fiscal 2024 due to concerns about the declining spending on tech infrastructure, but it remains confident that it can weather the economic headwinds. Cisco is focused on expanding its software and services segments, which are more profitable than its hardware segment. The company is also investing in new technologies, such as artificial intelligence and cloud computing, which it believes will drive future growth. With the varied outlook ahead, the company may show decelerated growth in the near term till it is able to fully capitalise on the higher demand for more profitable segments of its business. 1Q24 recommended trading range: $54 to $57. Neutral Outlook.

思科系统 (CSCO)

- 23财年第四季营收:152.0亿美元, 同比增幅16.0%,超预期1.5亿美元

- 23财年第四季Non-GAAP每股盈利:1.14美元,超预期0.08美元

- 24财年第一季指引:营收145至147亿美元,市场预期为146亿美元;Non-GAAP毛利率65%至66%;Non-GAAP营业利润率34%至35%;Non-GAAP每股收益为1.02美元至1.04美元,市场预期为0.99美元。24财年预期营收为570亿至582亿美元,市场预期为583.7亿美元;Non-GAAP每股收益预期为4.01美元至4.08美元,市场预期为4.04美元。

- 短评:思科系统公司提到,由于芯片供应短缺已经缓解,它能够完成更多的订单。然而,由于对技术基础设施支出下降的担忧,该公司的收入增长预计将在2024财年放缓,但它仍然有信心能够抵御经济逆风。思科正专注于扩大其软件和服务部门,这两个部门比硬件部门更有利可图。该公司还投资于人工智能和云计算等新技术,它认为这些技术将推动未来的增长。由于未来前景多变,该公司可能会在短期内放缓增长,直到它能够充分利用其业务中需求更高、利润更高的部分。24财年第一季度建议交易区间:52美元至57美元。中性前景。

Wolfspeed Inc (WOLF)

- 4Q23 Revenue: $235.8M, +3.2% YoY, beat estimates by $13.11M.

- 4Q23 Non-GAAP EPS: -$0.42, miss estimates by $0.22.

- 1Q24 Guidance: Target revenue in a range of $220mn to $240mn, vs. consensus of $234.30M. GAAP net loss is targeted at $145mn to $169mn, or $1.16 to $1.35 per diluted share. Non-GAAP net loss is targeted to be in the range of $75mn to $94mn, or $0.60 to $0.75 per diluted share, vs. consensus of -$0.28.

- Comment: Wolfspeed, a chipmaker whose products are used in sectors ranging from electric vehicles to renewable energy, is facing some challenges. The company expects a larger-than-expected quarterly loss due to significant factory start-up costs. Revenue is also expected to be below expectations. However, the company remains optimistic about its long-term prospects and expects to reach 20% utilisation out of its Mohawk Valley fabrication plant by the end of fiscal 2024. In the near term, the company is expected to remain unprofitable. 1Q24 recommended trading range: $42 to $47. Negative Outlook.

Wolfspeed Inc (WOLF)

- 23财年第四季营收:2.358亿美元, 同比增幅3.2%,超预期1,311万美元

- 23财年第四季Non-GAAP每股亏损:0.42美元,逊预期0.22美元

- 24财年第一季指引:目标营收在2.2亿美元至2.4亿美元之间,而市场预期为2.343亿美元。GAAP净亏损目标为1.45亿美元至1.69亿美元,摊薄后每股亏损1.16美元至1.35美元。Non-GAAP净亏损目标在7,500万美元至9,400万美元之间,即每股摊薄后亏损0.60美元至0.75美元,而市场预期为-0.28美元。

- 短评:芯片制造商Wolfspeed的产品应用于从电动汽车到可再生能源等多个领域,该公司正面临一些挑战。由于大量的工厂启动成本,该公司预计季度亏损将超过预期。预计收入也将低于预期。然而,该公司对其长期前景仍持乐观态度,预计到2024财年末,其莫霍克山谷制造工厂的利用率将达到20%。在短期内,该公司预计仍将无利可图。24财年第一季度建议交易区间:42美元至47美元。负面前景。