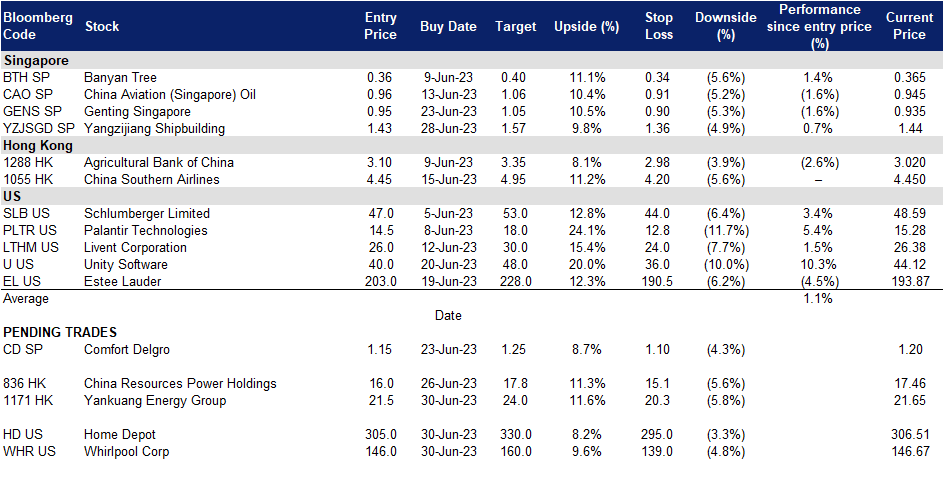

30 June 2023: Yangzijiang Shipbuilding (YZJSGD SP), Yankuang Energy Group Co. Ltd. (1171 HK), Whirlpool Corp (WHR US)

Singapore Trading Ideas | Hong Kong Trading Ideas |United States Trading Ideas | Sector Performance | Trading Dashboard

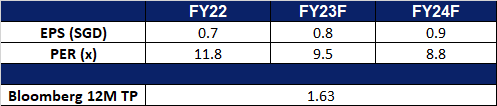

Yangzijiang Shipbuilding (YZJSGD SP): Double bonanzas-record order book and weak RMB

- RE-ITERATE BUY Entry 1.43 – Target – 1.57 Stop Loss – 1.36

- Yangzijiang Shipbuilding Holdings Limited builds a wide range of ships. The Company produces a wide range of commercial vessels, mini bulk carriers, multi-purpose cargo vessels, container ships, chemical tankers, offshore supply vessels, rescue and salvage vessels, and lifting vessels.

- Secures contract to build six mid-size container vessels. YZJ Shipbuilding just secured a contract with A.P. Moller-Maersk to construct six 9,000TEU methanol dual-fuel containerships in-house which are due for delivery between 2026 and 2027. They are designed to operate on green methanol and feature dual-fuel engines that can run on both fuel oil and methanol. With a capacity to carry over 9,000 containers, the new ships will replace existing vessels in Maersk’s fleet as part of their commitment to transitioning to greener options. Green methanol is reported to be able to significantly reduce nitrogen oxide (NOx) and sulphur oxide (SOx) emissions compared to conventional fuels. Moreover, considering the International Maritime Organization’s regulations that are pushing the shipping industry towards decarbonisation, it is highly likely that this contract is just the beginning of a series of future methanol dual-fuel fleet orders for YZJ Shipbuilding.

- Repeat customer. On June 25 it was announced that YZJ Shipbuilding had secured a contract from Klaveness Combination Carriers to construct three 83,300DWT third-generation CABU vessels, scheduled for delivery in 2026. The contract price for each vessel is US$56.4 million, with an estimated delivered cost of approximately US$60.5 million per vessel, including zero-emission readiness and shipyard supervision costs. These combination carriers can transport both wet and dry cargo, offering increased operational efficiency compared to single-purpose vessels. The new vessels will feature fuel-efficient solutions such as wind-assisted propulsion, reducing overall carbon dioxide (CO2) emissions by approximately 35%. This contract marks a repeat order from Klaveness Combination Carriers, highlighting the trust placed in YZJ’s delivery capabilities.

- YTD orderbook hits the full-year target. As of 26 June, YZJ Shipbuilding has secured orders for a total of 37 vessels. YTD, the company has obtained orders for 69 vessels, amounting to a value of US$5.6 billion, surpassing its target of US$3 billion for 2023. This has resulted in the highest-ever outstanding orderbook value for Yangzijiang, standing at US$14.6 billion for 180 vessels, as reported in an SGX filing. Among the newly ordered vessels, 16 are containerships, 11 are oil tankers, and 10 are bulk carriers.

- FY22 results review. Revenue for FY22 increased 24% YoY to RMB20.7bn. Net profit (ex-investment) grew 33% YoY to RMB2.6bn.

- Market consensus.

Share price and RMB price trend comparison

(Source: Bloomberg)

(Source: Bloomberg)

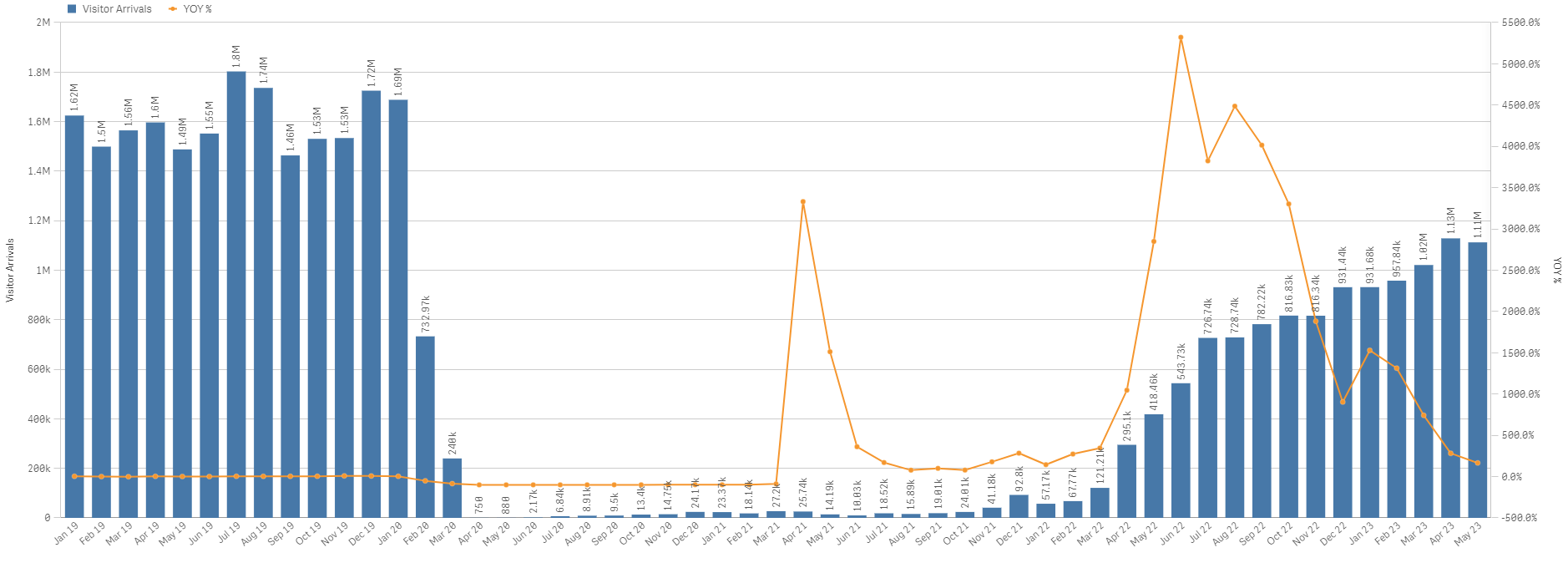

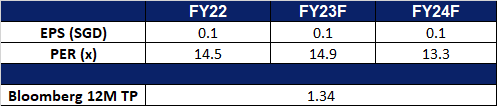

ComfortDelgro (CD SP): Peak Travel Season

- RE-ITERATE BUY Entry 1.15 – Target – 1.25 Stop Loss – 1.10

- ComfortDelGro Corporation Limited provides land transportation services. The Company offers bus, taxi, rail, car rental and leasing, automotive engineering services, inspection and testing services, driving center, insurance broking services, and outdoor advertising.

- Peak travel season drives demand for transportation. Longer waiting time were seen for taxis over peak travel season over the summer holidays. This boosted the demand for private transportation within Singapore, which was already recovering from the pandemic, as more employees return to the office. Supply of drivers has not been keeping up with the increase in demand for private transportation, as the supply of private drivers are only at around 80% of pre-pandemic levels, attributing to the long waiting time for ride-hailing passengers.

Comfort Delgro Seasonality Trend

(Source: Bloomberg)

Singapore Visitor Arrival Trend

(Source: Singapore Tourism Analytics Network)

(Source: Singapore Tourism Analytics Network)

- Platform fee to drive sales amidst higher demand. Comfort Delgro has recently made an announcement regarding their plans to implement a surcharge of 70 cents for taxi and private-hire car rides booked through their CDG Zig app starting from July 1, 2023. This platform fee has been introduced with the intention of further enhancing the quality of their point-to-point transport services. By implementing this additional fee, Comfort Delgro aims to leverage the increased demand for taxis during the peak travel period, ultimately boosting their sales.

- FY22 results review. Revenue rose by 7.94% YoY to S$3.708bn, compared to S$3.502bn in FY2021. Net profit rose by 40.7% YoY to S$173.1mn, compared to S$123.0mn in FY2021. EPS rose to 7.99 SG cents (+40.7% YoY) compared to 5.68 SG cents in FY2021.

- Market consensus.

(Source: Bloomberg)

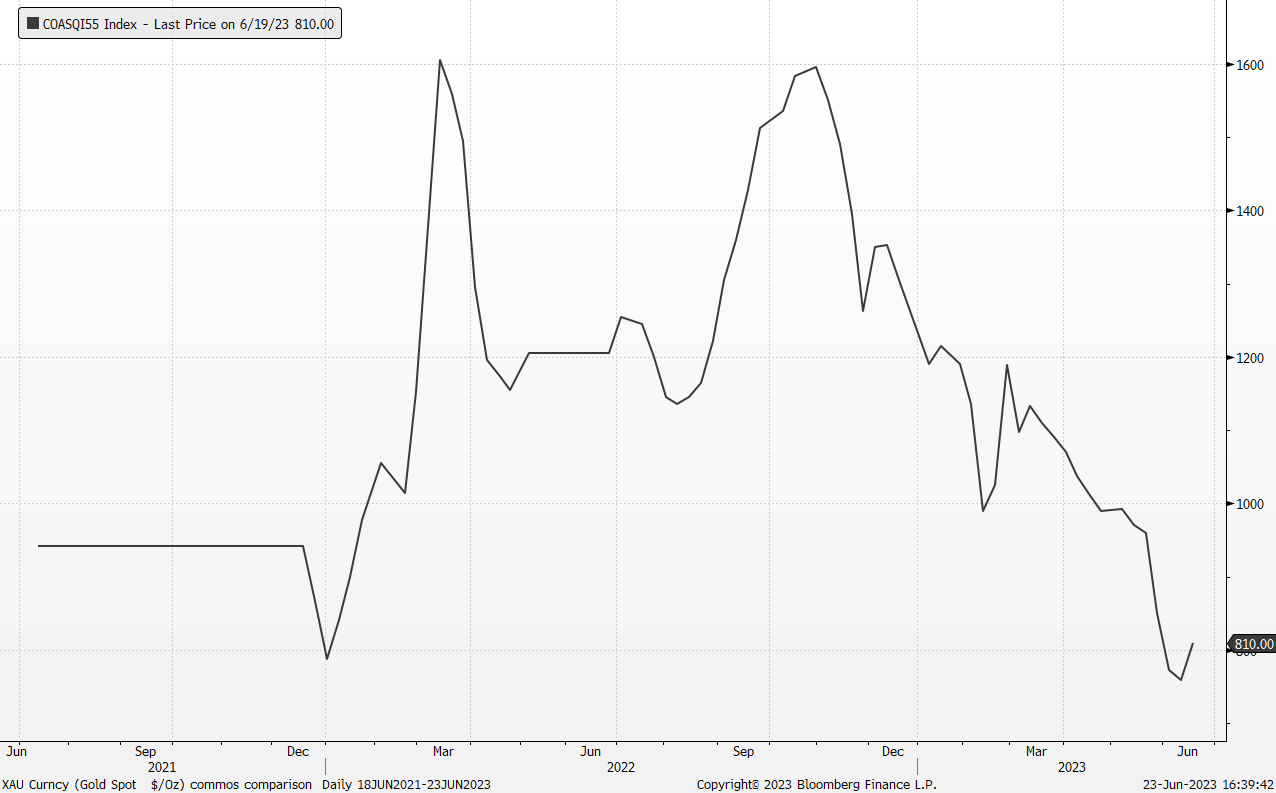

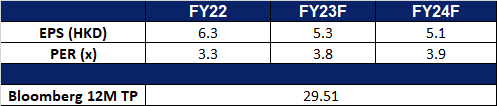

Yankuang Energy Group Co. Ltd. (1171 HK): Peak seasonal demand for coal

- BUY Entry – 21.50 Target – 24.00 Stop Loss – 20.25

- Yankuang Energy Group Co Ltd is a China-based international comprehensive energy company engaged in coal and coal chemical industry. The Company operates in five segments. The Coal Mining segment is engaged in underground and open-cut mining, preparation and sale of coal and potash mineral exploration. The Smart Logistics segment provides railway transportation services. The Electricity and Heating Supply segment provides electricity and related heat supply services. The Equipment Manufacturing segment is engaged in the manufacture of comprehensive coal mining and excavating equipment. The Chemical Products segment is engaged in the production and sale of chemical products. The coal products mainly include thermal coal, pulverized coal injection (PCI), and coking coal. The coal chemical products mainly include methanol, ethylene glycol, acetic acid, ethyl acetate and crude liquid wax, among others. The Company distributes products in the domestic market and to overseas markets..

- Scorching weather drives demand for coal. Recently, the China Meteorological Administration took action in response to the prediction of scorching heat and heavy rains expected to affect large areas of the country in the upcoming days. Beijing, the capital, elevated its hot weather warning to the highest level, designated as red, marking the first instance of such an alert being issued since the adoption of the new classification system in June 2015. This is expected to drive up the demand for coal as electricity consumption surge as consumers seek refuge away from the hot weather in China.

Thermal Coal Price

(Source: Bloomberg)

- Upcoming AGM. Yankuang Energy Group will be hosting its AGM on 30th June 2023, where its shareholders will be voting on the acquisition of 51% equity of Luxi Mining and 51% equity of Xinjiang Neng Hua.The company mentioned that the intended acquisition of high-quality assets and the control of mature mines in production is to realize the inflow of income into the consolidated financial statements.The successful acquisition of these assets would boost Yankuang Energy Group’s production capabilities, with Luxi Mining and Xinjiang Nenghua achieving a total coal output of 31.81mn tons in 2022, and is expected to reach a production capacity of 39.89mn tons in 2025.

- 1Q23 earnings. Operating Income rose to RMB44.4bn, a 7.82% increase YoY, compared to RMB41.2bn in 1Q22. Net Income fell to RMB5.6bn in 1Q23 compared to RMB6.7bn in 1Q22. Reported EPS of RMB1.16 fell YoY.

- High dividend yields. FY23F/24F dividend yield is 15.5%/14.5% respectively.

- Market Consensus.

(Source: Bloomberg)

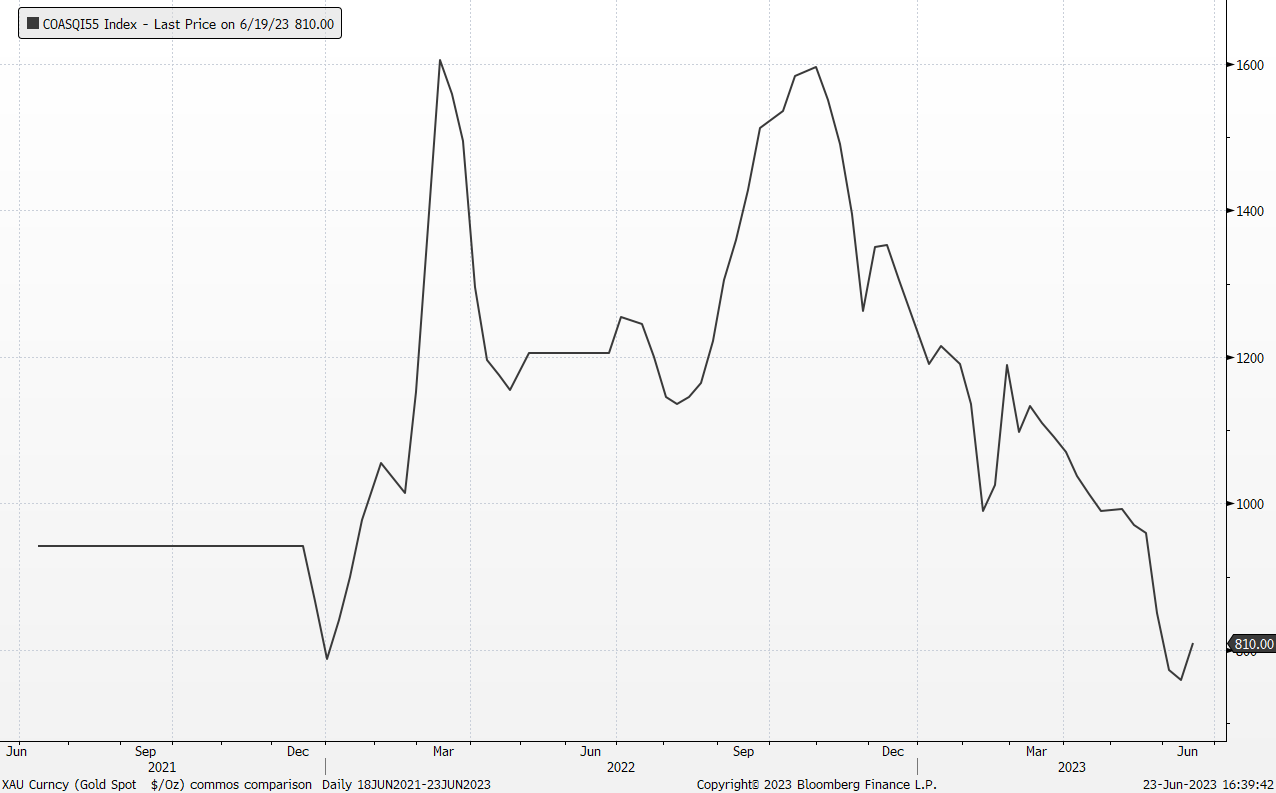

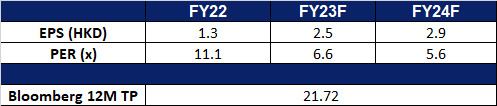

China Resources Power Holdings Co. Ltd. (836 HK): Heat wave strikes

China Resources Power Holdings Co. Ltd. (836 HK): Heat wave strikes

- RE-ITERATE BUY Entry – 16.0 Target – 17.8 Stop Loss – 15.1

- China Resources Power Holdings Company Limited is a Hong Kong-based investment holding company principally engaged in the investment, development and operation of power plants. The Company operates through three segments. Thermal Power segment is engaged in the investment, development, operation and management of coal-fired power plants and gas-fired power plants, as well as the sales of heat and electricity. Renewable Energy segment is engaged in wind power generation, hydroelectric power generation and photovoltaic power generation, as well as the sales of electricity. Coal Mining segment is engaged in the mining of coal mines, as well as the sales of coal. The Company mainly operates businesses in China.

- Higher temperatures expected. Last Friday, the China Meteorological Administration took action in response to the prediction of scorching heat and heavy rains expected to affect large areas of the country in the upcoming days. Beijing, the capital, elevated its hot weather warning to the highest level, designated as red, marking the first instance of such an alert being issued since the adoption of the new classification system in June 2015. Additionally, notable weather stations in Tianjin, as well as Hebei and Shandong provinces, experienced unprecedented high temperatures on the preceding Thursday. According to the administration’s forecast, heatwaves are anticipated to persist for a duration of 10 days in Beijing, Tianjin, other parts of North China, and select regions in Henan and Anhui provinces.

- Lower Coal Prices. The decline in global coal prices is expected to have significant benefits for the company’s coal-fired power plants and gas-fired power plants. With prices at a 2-year low around $130 per tonne, lower fuel costs for coal-fired power plants translate into improved profitability and a competitive advantage in the market. While China Resources Powers does have its own coal production plants, energy consumption during summer typically skyrockets for China, this means that the company will be required to buy coal from other suppliers to further supplement its energy production and will therefore benefit from the lower prices. Additionally, the predictability of prices enables better operational planning and mitigates risks associated with volatility. The declining prices also create opportunities for the company’s gas-fired power plants, as natural gas becomes a more cost-effective alternative. This diversification and cost advantage contribute to improved financial performance, market competitiveness, and the ability to offer competitive electricity prices to consumers. Overall, the decline in coal prices presents favourable conditions for the company’s power generation operations, enhancing profitability and sustainability.

Thermal Coal Price

(Source: Bloomberg)

- Expansion of renewable projects. The city’s stock exchange has granted approval to China Resources Power (CRP) for the independent listing of its renewable energy division in Shenzhen. This decision enables CRP to generate additional funds that will be used to support the company’s ambitious growth plans in wind and solar power initiatives. Furthermore, the separate listing is expected to enhance the valuation of CRP’s assets, benefiting its shareholders.

- FY22 earnings. Revenue rose to HK$103.3bn, a 15.0% increase YoY. Net Income of HK$7.04bn was up 342% compared to FY2021.Net profit Margin rose to 6.8%, compared to 1.8% in FY2021

- Market Consensus.

(Source: Bloomberg)

Whirlpool Corp (WHR US): Home appliance sales recover

- BUY Entry – 146.0 Target – 160.0 Stop Loss – 139

- Whirlpool Corporation manufactures and markets major home appliances. The Company provides principal products include laundry appliances, refrigeration, room air conditioning equipment, cooking appliances, dishwashers, and mixers and other small household appliances. Whirlpool serves customers worldwide.

- US home sales jump as prices fall. Sales of new single-family homes in the US reached their highest level in almost 1-1/2 years in May due to a shortage of previously owned homes. The Commerce Department reported a 12.2% surge to a rate of 763,000 units, the highest since February 2022. Real construction spending on new manufacturing facilities has also doubled this year, driven by infrastructure and clean energy subsidies. Although mortgage rates rose, new home sales increased in the Northeast, South, and West. The median new house price dropped 7.6% from last year, and the supply of homes on the market slightly decreased. It is likely that signs of revival in the housing market will contribute to an increase in the purchase of household appliances. As the housing market improves and new homes are being sold at a higher rate, new homeowners typically need to furnish their homes with essential appliances such as refrigerators, stoves, washers, dryers, and more.

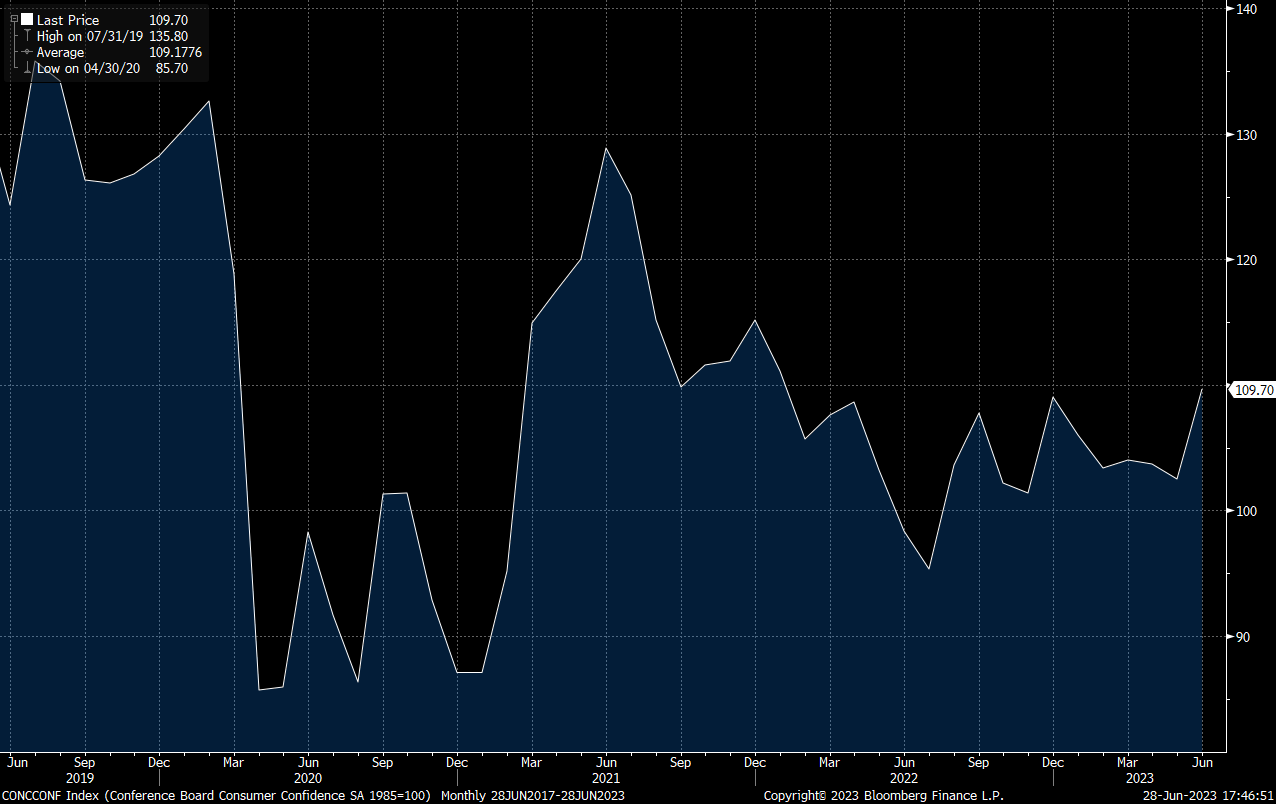

- Rise in consumer confidence. Consumer confidence in the United States soared to its highest level in nearly 1-1/2 years in June, surpassing expectations and marking the strongest reading since January 2022. The increase was especially prominent among consumers under 35 and those with incomes over $35,000. Strong economic indicators, such as increased consumer confidence, unexpected growth in new home sales, and robust demand for big-ticket manufactured items, reassured investors about the overall economic outlook. The positive trend in the housing market, coupled with increased consumer confidence, may encourage existing homeowners to invest in new appliances, bolstering sales of the appliance industry.

US Conference Board’s Consumer Confidence Index

(Source: Bloomberg)

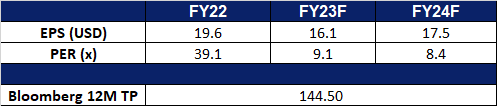

- 1Q23 earnings review. Revenue fell 6.8% YoY to US$4.65bn, beating estimates by US$150mn. Non-GAAP earning per share was US$2.66, $0.49 above expectations. The company’s strong performance was bolstered by robust demand for its refrigerators and washing machines in North America, which is its largest market. It is anticipating FY23 sales to reach approximately US$19.4B.

- Market consensus.

(Source: Bloomberg)

Home Depot Inc (HD US): Improving US housing market

Home Depot Inc (HD US): Improving US housing market

- RE-ITERATE BUY Entry – 305 Target – 330 Stop Loss – 295

- The Home Depot, Inc. is a home improvement retailer. The Company offers wide range of building materials, home improvement, lawn, and garden products, as well as provides DYI ideas, installation, repair, and other services. Home Depot serves customers worldwide.

- Housing shortage. The tightening supply of available homes is exacerbated by the current high-interest rate environment. Although there was a slight increase in existing home sales in May, overall market activity remained subdued. The rate-sensitive nature of the housing market has been negatively affected by the central bank’s decision to raise the benchmark lending rate as a response to inflation concerns. Furthermore, the inventory of homes for sale is significantly lower compared to pre-pandemic levels, amplifying the scarcity of housing options. This limited supply, combined with a decline in mortgage applications following the rise in interest rates, indicates that sales are likely to remain subdued in the near future. These factors indicate a housing shortage, as the demand for homes surpasses the available supply, making it challenging for potential buyers to find suitable and affordable housing options.

- US housing market is showing signs of a potential turnaround. Housing starts in May rose to a seasonally adjusted annual rate of 1.631mn units, the highest since April 2022, indicating strong demand. This marked a significant increase from April’s rate of 1.34mn units. Permits for future construction also saw a positive growth of 5.2% to the highest level since October. The National Association of Home Builders/Wells Fargo Housing Market Index in June rose above the midpoint mark of 50 for the first time since July 2022, further reflecting an improved outlook. Moreover, the average rate on the popular 30-year fixed mortgage has come down from its high above 7% in November. These figures indicate positive momentum in the housing market, which is expected to contribute to US economic growth in the second half of the year. While these trends suggest a potential recovery, it’s important to acknowledge the volatility of the housing market, with no guarantees of sustained improvement. Nevertheless, these developments could positively impact Home Depot’s sales as it operates in the home improvement sector.

- Housing shortage. In May, sales of existing homes in the United States increased slightly despite limited demand caused by a shortage of supply and high-interest rates. The housing market, which is sensitive to interest rate changes, has been impacted by the central bank’s decision to raise lending rates in order to address persistent inflation. Additionally, the availability of homes for sale is significantly lower than it was before the pandemic. Analysts have observed a decline in mortgage applications following an increase in interest rates, suggesting that sales may remain subdued in the near future. The National Association of Realtors reported a 0.2% rise in existing home sales from April, reaching a seasonally adjusted rate of 4.3 million, but compared to the previous year, sales were down by 20.4%.

- Look to improve. The shortage in the housing market has led to skyrocketing prices, further exacerbated by high mortgage rates. As a result, many homeowners may opt to improve their existing homes rather than purchase new ones. This shift in consumer behaviour can be attributed to the limited availability and increased cost of housing options. Homeowners, faced with inflated prices and limited choices, may invest in renovations, remodelling, and home improvement projects to enhance their living spaces. This trend is expected to drive increased sales of products and services offered by companies like Home Depot, as homeowners seek to upgrade their properties rather than enter the competitive and expensive housing market. With limited supply and soaring prices in the housing market, the focus on home improvements presents an alternative for homeowners to create their desired living spaces and contribute to the growth of businesses specialising in home improvement products and services.

30Y U.S. Home Mortgage Rates

(Source: Bloomberg)

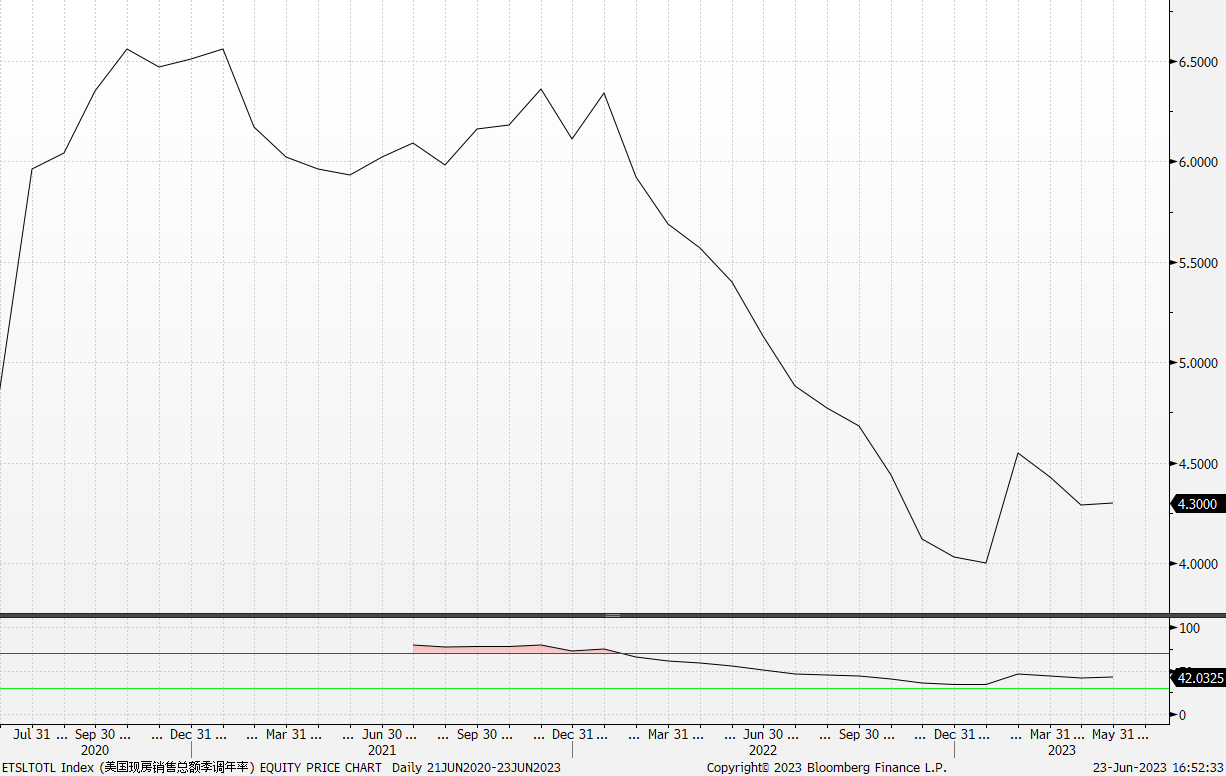

US National Association Realtors Total Existing Home Sales

(Source: Bloomberg)

(Source: Bloomberg)

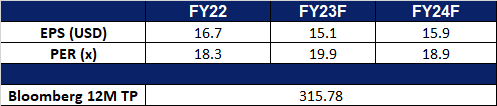

- 1Q23 earnings review. Revenue fell 4.2% YoY to US$37.3bn, missing estimates by US$1.04bn. GAAP earning per share was US$3.82, $0.03 above expectations.

- Market consensus.

(Source: Bloomberg)

United States

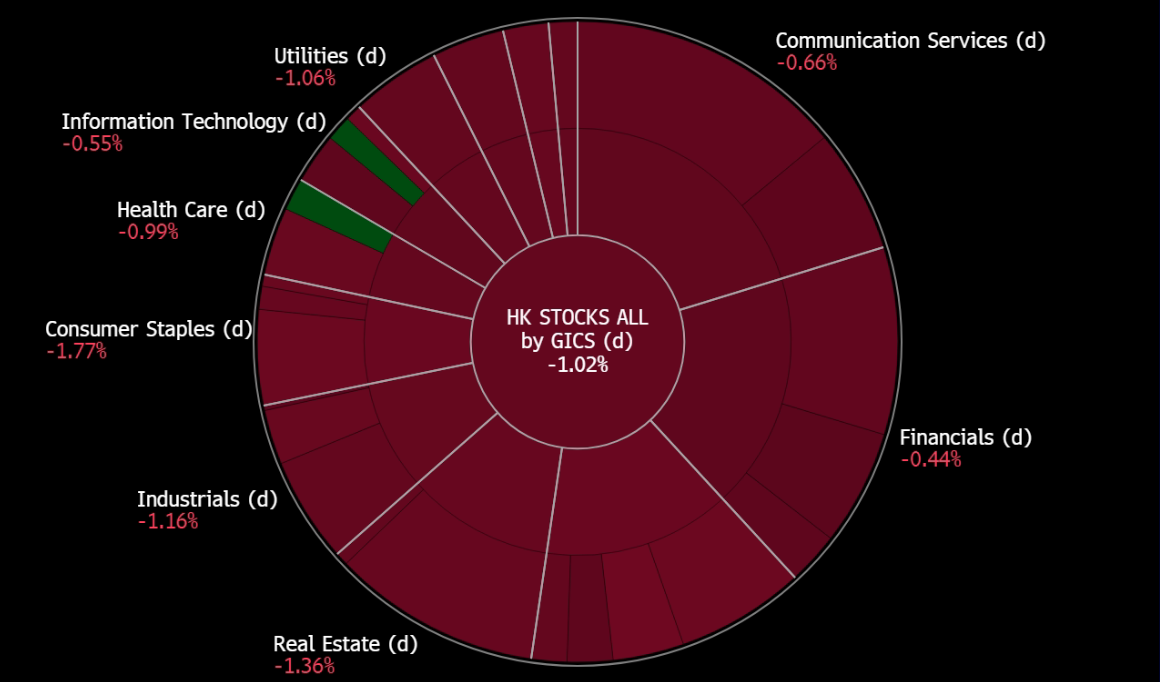

Hong Kong

Trading Dashboard Update: Cut loss on Alphabet (GOOG US) at US$118. Add Yangzijiang Shipbuilding (YZJSGD SP) at S$1.43.