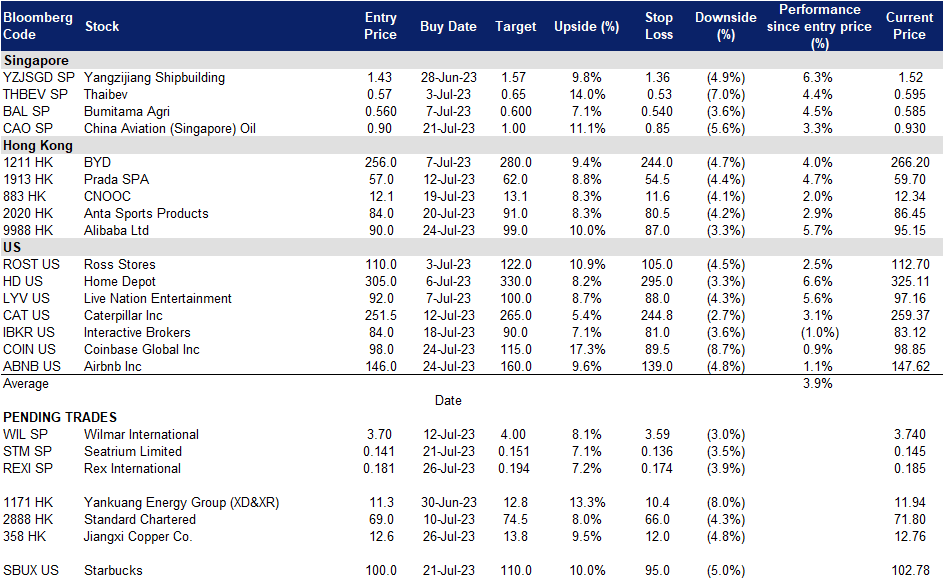

26 July 2023: Rex International Holding Ltd (REXI SP), Jiangxi Copper Co. (358 HK), Airbnb Inc (ABNB US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

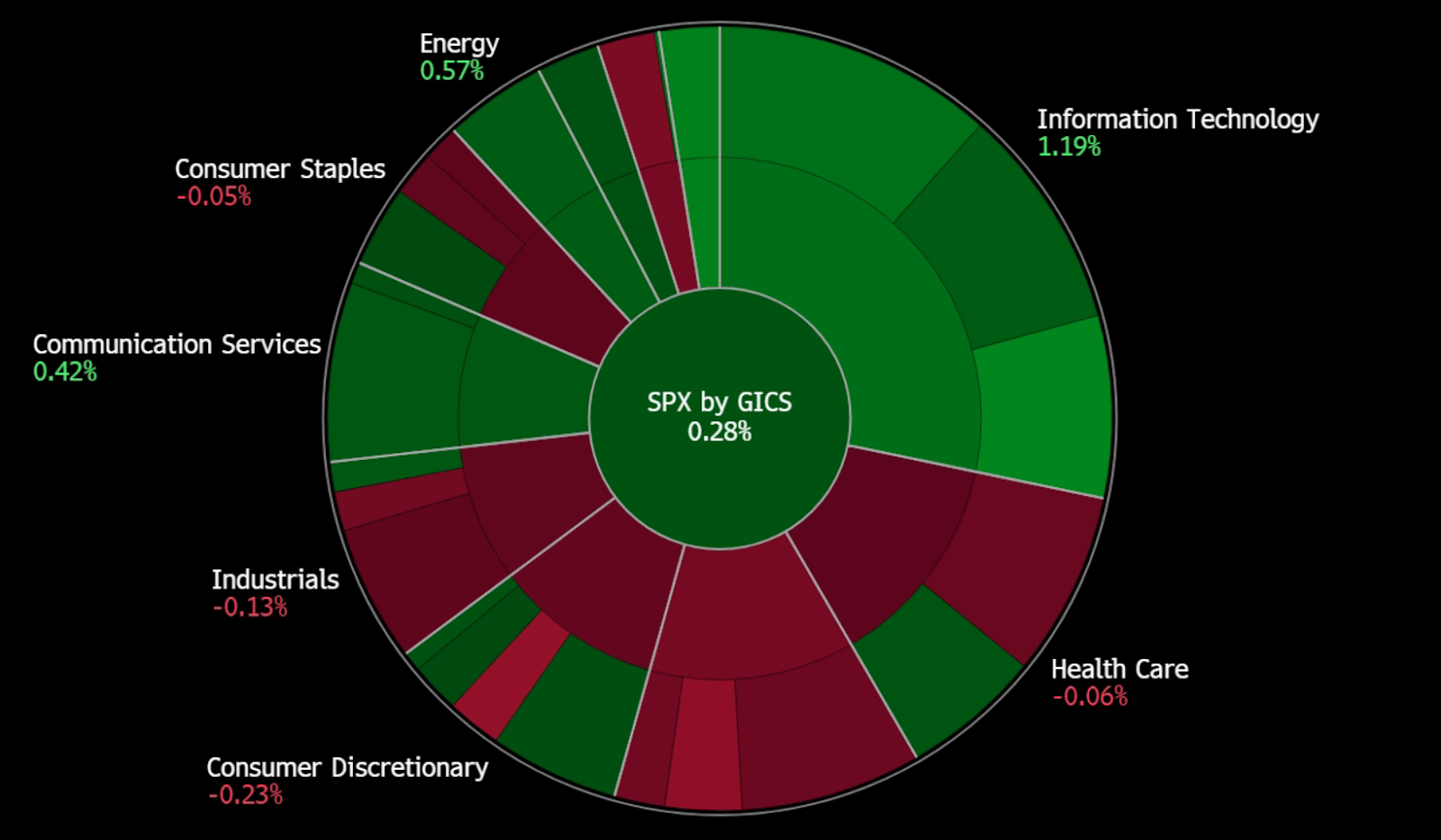

United States

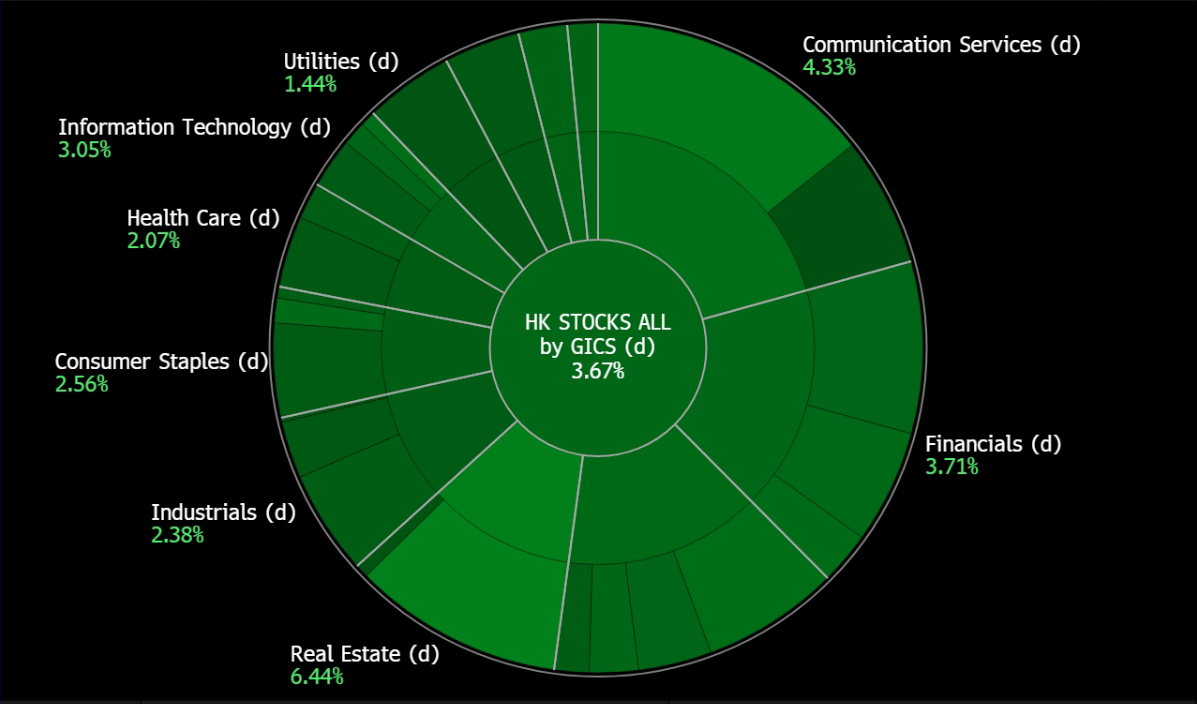

Hong Kong

Rex International Holding Ltd (REXI SP): Oil bottoming out

- BUY Entry 0.181 – Target – 0.194 Stop Loss – 0.174

- Rex International Holding Limited operates as an independent oil exploration and production company. It operates through Oil and Gas, and Non-Oil and Gas segments. The company offers Rex Virtual Drilling, a liquid hydrocarbon indicator, which uses seismic data to search for oil. The company is involved in the oil and gas exploration and production activities with a focus in Oman and Norway.

- OPEC+ cuts. Saudi Arabia and Russia, the world’s top oil exporters, have announced deeper oil cuts to support oil prices despite concerns over a global economic slowdown and potential interest rate increases from the U.S. Federal Reserve. Saudi Arabia will extend its voluntary oil output cut of one million barrels per day (bpd) for another month until August, and Russia will cut its oil exports by 500,000 bpd in August. These cuts amount to 1.5% of global supply and bring the total pledged by OPEC+ to 5.16mn bpd. Algeria will also make an extra 20,000-barrel cut in August to support market balance efforts. OPEC+ already has in place cuts of 3.66mn bpd. Oil prices have shown signs of increase as supplies tighten due to the oil cuts.

- China stimulus expectations. China’s leaders have pledged to step up policy support for the economy, focusing on boosting domestic demand, amid a post-COVID recovery. This includes expanding domestic demand, increasing residents’ incomes to drive consumption-led economic growth, and promoting investment in various sectors, including autos, electronics, household products, and tourism. The government will also adjust property policies to address changes in the property market and resolve local government debt risks. Chinese authority’s actions and focus on domestic demand could have an impact on oil demand as it is the world’s second-largest oil consumer. With the Chinese government planning to ramp up economic activity, oil demand is expected to rise, potentially leading to higher oil prices as demand outpaces supply.

- Russia lower export discount. Russia’s finance ministry intends to reduce the discount used to calculate taxes on crude oil exports from $25 to $20 per barrel. This decision comes in response to Western sanctions, including a $60 per barrel price cap on Russian crude exports and the EU’s import ban, affecting Russia’s oil sales. The discount is based on Russia’s dominant Urals blend of crude oil. The ministry is also exploring further measures to improve tax calculations on oil exports. As a result of the reduced discount, purchasers of Russian crude oil exports will face higher costs per barrel.

- Oman and Norway oil production. In June, Rex International Holding’s unit, Masirah Oil, reported an average oil production of 3,364 stock tank barrels per day from the Yumna Field in offshore Block 50 Oman. Rex International holds a 91.81% stake in Masirah Oil. Additionally, Rex International’s subsidiary, Lime Petroleum, recorded oil production of 4,370 barrels of oil equivalent per day from the Brage Field in Norway and 1,907 barrels of oil equivalent per day from the Yme Field in the same month. Lime Petroleum holds a 33.8% interest in the Brage Field and a 10% interest in the Yme Field.

- FY22 results review. Rex International posted a loss of US$1mn versus a net profit of US$67.2mn in 2021. Revenue for the financial year from crude oil sales was up 7% to US$170.3mn.

- Market Consensus.

(Source: Bloomberg)

Seatrium Limited (STM SP): More bullets to fire

Seatrium Limited (STM SP): More bullets to fire

- RE-ITERATE BUY Entry 0.141 – Target – 0.151 Stop Loss – 0.136

- Seatrium Limited provides offshore and marine engineering solutions. It operates through two segments: Rigs & Floaters, Repairs & Upgrades, Offshore Platforms, and Specialised Shipbuilding; and Ship Chartering.

- Green trade finance facility. The company secured a green trade finance facility from OCBC bank with a total amount of EUR720mn (S$1.04bn). The facility will be particularly utilized for the company’s offshore renewable projects and decarbonisation. The latest renewables and green solutions projects account for about 39% of the total net order book which increased to S$20bn in 1Q23.

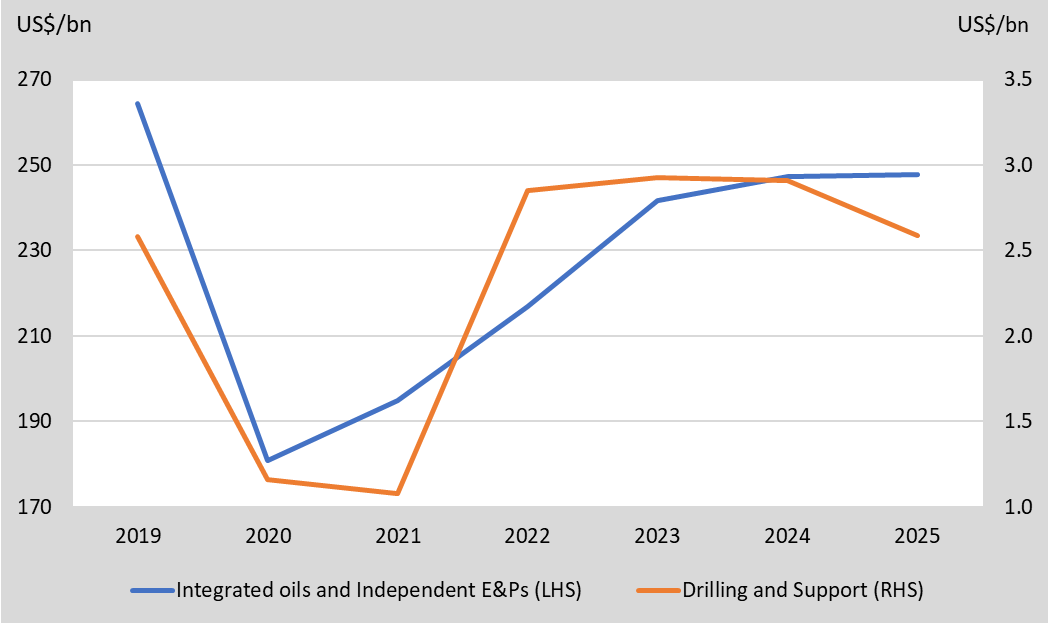

- Expecting mild growth in the upstream oil and gas capex. Though oil prices have topped out since July 2022 as global economic growth slows down, especially China’s recovery tumbles, the oil and gas upstream spending continues. Oil majors accelerated to explore and develop oil resources outside Russia after the sanction. Hence, there still be mild growth in the upstream capex during 2023/2024.

Global upstream oil and gas capex

(Source: Bloomberg)

(Source: Bloomberg)

- FY22 results review. Revenue rose 4.6% YoY to S$1,947mn from S$1,862mn the prior year. Net loss declined by 78.0% YoY to -S$261mn from -S$1,171mn in FY21. With positive EBITDA for 2H22, the FY22 EBITDA was -S$7mn a 99% decrease YoY from the previous -S$1,028mn. The company will release 1H23 results on July 28th.

- Market consensus.

(Source: Bloomberg)

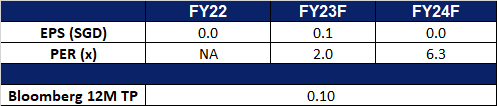

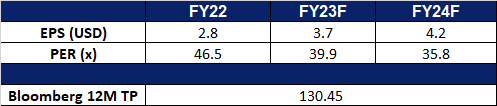

Jiangxi Copper Co. (358 HK): Further easing property regulations

- BUY Entry – 12.6 Target – 13.8 Stop Loss – 12.0

- Jiangxi Copper Company Limited is a China-based company, principally engaged in the mining, smelting and processing of copper. The Company is also engaged in the extraction and processing of precious metals and dissipated metals, sulfur chemical industry business, and financial and trading businesses. The company’s products include cathode copper, gold, silver, sulfuric acid, copper rods, copper foils, selenium, tellurium, rhenium, bismuth and others. The Company mainly conducts its businesses within Mainland China and Hongkong.

- Support for the property sector. The latest Politburo meeting in China indicated increased backing for the struggling real estate sector while also committing to bolster consumption and address local government debt. President Xi Jinping is embracing a more supportive approach, emphasizing the idea that “housing is for living, not for speculation.” He also recognized a “significant” shift in the supply and demand dynamics of the property market. During the meeting, it was underscored that China could reconsider its stringent measures that had previously been implemented in first- and second-tier cities, with the aim of timely adjustments and optimizations of policies. An extension of the 16-item guideline which was implemented last year until December 31, 2024, will provide financial institutions with a boost to negotiate outstanding loans with real estate enterprises, promoting a market-friendly approach and protecting creditors’ rights. These policy support for the real estate economy in China is likely to drive the demand for construction materials including copper.

- Copper futures rebounded. Due to China’s favourable economic stimulus plan released on Monday, copper futures rebounded more than 1.8% on Tuesday.

Copper futures price trend

(Source: Bloomberg)

- 1Q23 earnings. Revenue rose to RMB127.7bn, up 4.57% YoY. Gross profit dropped by 7.5% to RMB3.3bn. Net profit was RMB 1.76bn, up 19.1% YoY.

- Market Consensus.

(Source: Bloomberg)

Alibaba Ltd. (9988 HK): More stimulus released from the Politburo meeting

Alibaba Ltd. (9988 HK): More stimulus released from the Politburo meeting

- RE-ITERATE BUY Entry – 90.0 Target – 99.0 Stop Loss – 87.0

- Alibaba Group Holding Ltd provides technology infrastructure and marketing platforms. The Company operates through seven segments. China Commerce segment includes China retail commerce businesses such as Taobao, Tmall and Freshippo, among others, and wholesale business. International Commerce segment includes international retail and wholesale commerce businesses such as Lazada and AliExpress. Local Consumer Services segment includes location-based businesses such as Ele.me, Amap, Fliggy and others. Cainiao segment includes domestic and international one-stop-shop logistics services and supply chain management solutions. Cloud segment provides public and hybrid cloud services like Alibaba Cloud and DingTalk for domestic and foreign enterprises. Digital Media and Entertainment segment includes Youku, Quark and Alibaba Pictures, other content and distribution platforms and online games business. Innovation Initiatives and Others segment include Damo Academy, Tmall Genie and others.

- Economic stimulus to boost domestic consumption. China’s ongoing economic recovery is encountering challenges due to inadequate demand, sluggish momentum, and low confidence. During the July Politburo meeting, China’s top leaders pledged to increase policy support for the economy to address slow economic growth in Q2 due to weakened domestic and international demand. The government plans to implement precise and forceful macro adjustments while maintaining a prudent monetary policy and proactive fiscal policy. To bolster the recovery, China will actively expand domestic demand, promoting consumption-led economic growth, and boost demand in sectors like autos, electronics, household products, and tourism. To support the economy, the government will adjust property policies, address local government debt risks, and create a more favourable environment for private firms. Measures are also being taken to stabilise trade, foreign investment, and improve the private sector’s growth prospects. Additionally, the Commerce Ministry of China recently unveiled an 11-point plan aimed at bolstering domestic consumption of household consumer goods and services.

- Supply Chain Establishment. Cainiao Group, Alibaba’s logistics arm, is set to speed up global logistics network development and expand its presence in Europe, North America, and Southeast Asia with more local warehousing and distribution centers. In the coming decade, Cainiao aims to establish a leading global smart logistics network, covering domestic, cross-border, and overseas logistics, including last-mile deliveries and logistics technology. To achieve this, they are collaborating with AliExpress to offer a global delivery service that guarantees cross-border parcel delivery within five working days, 30% faster than the industry standard. The company has already expanded its global logistics infrastructure with 18 overseas distribution centers, warehouses, and self-operated distribution and pickup facilities.

- Driving growth in Asia. Alibaba has made a recent announcement about investing an extra $845.44 million in Lazada, the Southeast Asian e-commerce unit. This move is part of Alibaba’s strategy to strengthen its presence in the fiercely competitive region. Lazada aims to increase its current user base of 160 million in countries like Singapore, Indonesia, Thailand, and Malaysia to an impressive 300 million by the year 2030. This expansion plan will enable Lazada to gain a competitive edge against rivals like Shopee and Tiktok Shop in the Southeast Asian market.

- FY22 earnings. Revenue rose to RMB208.2bn, up 2.03% YoY. Net profit was RMB 23.5bn, compared to a net loss of RMB13.3 during the same period. Non-GAAP diluted earnings per share was RMB1.34, an increase of 35% YoY.

- Market Consensus.

(Source: Bloomberg)

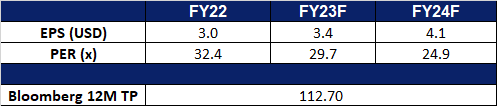

Airbnb Inc (ABNB US): Travel still in demand

- RE-ITERATE BUY Entry – 146 Target – 160 Stop Loss – 139

- Airbnb, Inc. operates an online marketplace for travel information and booking services. The Company offers lodging, home-stay, and tourism services via websites and mobile applications. Airbnb serves clients worldwide.

- Air travel demand. The travel industry is experiencing a sustained high demand as people eagerly resume travel after the pandemic, with major airlines anticipating demand to surpass pre-pandemic levels and remain robust throughout FY23. While Airbnb is just one of many accommodation options available to travellers, it stands to benefit from the rising travel demand. The increasing popularity of travel and Airbnb’s unique marketplace can lead to its growth in the short term. However, the company’s long-term success will depend on its ability to compete with other accommodation options and manage factors like rental costs and economic conditions. Nonetheless, the ongoing high travel demand is likely to positively impact Airbnb’s revenue and profit in the near future.

- 1Q23 earnings review. Revenue grew by 20.5% YoY to US$1.82bn, beating estimates by US$30mn. 1Q23 GAAP EPS was US$0.18, beating estimates by US$0.08. Gross booking value grew by 19% YoY to US$20.4bn. Nights and experiences booked grew by 19% YOY to 121.1mn. Average daily rates remained flat YoY at US$168. 2Q23 revenue is expected to between US$2.35bn to US$2.45bn. The consensus revenue estimate is US$2.42bn.

- Market consensus.

(Source: Bloomberg)

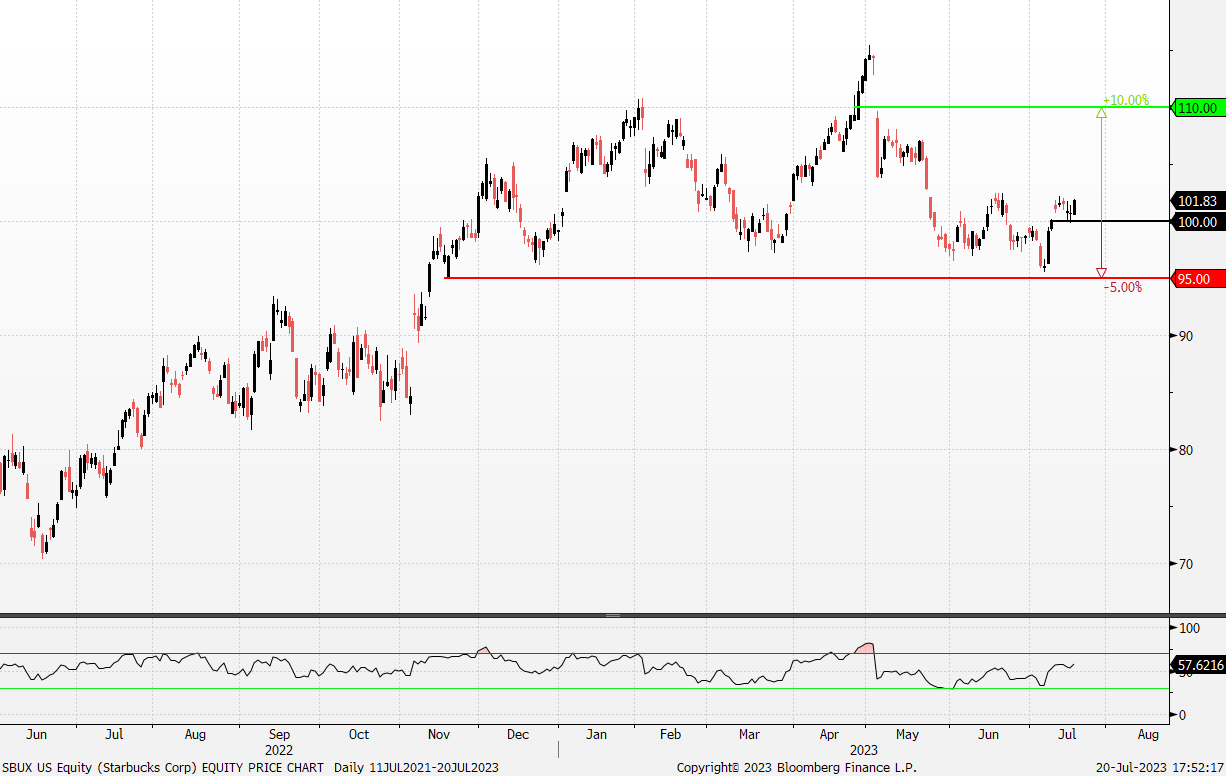

Starbucks Corp (SBUX US): BLACKPINK in your drink

Starbucks Corp (SBUX US): BLACKPINK in your drink

- RE-ITERATE BUY Entry – 100 Target – 110 Stop Loss – 95

- Starbucks Corporation is the premier roaster, marketer, and retailer of specialty coffee. The Company offers packaged and single-serve coffees and teas, beverage-related ingredients, and ready-to-drink beverages, as well as produces and sells bottled coffee drinks and a line of ice creams. Starbucks serves customers worldwide.

- Partnership with BLACKPINK. Starbucks recently unveiled an exclusive fan experience, exclusive to the Asia Pacific region, commencing on 25 July, featuring a BLACKPINK-themed Frappuccino and limited-edition merch collection. This collaboration with one of today’s biggest icons resonates with Starbucks’ dedication to uplifting customers and fans through meaningful connections, creating an unforgettable Starbucks Experience. The accompanying limited-edition merch collection boasts 11 drinkware styles and six lifestyle accessories in a striking pink and black color palette. The partnership, available at select Starbucks locations across Hong Kong, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan, Thailand, and Vietnam, aims to attract BLACKPINK fans, affectionately known as “Blinks,” capitalizing on the K-pop frenzy to potentially boost sales. Notably, this collaboration marks the first regional-scale partnership and menu item development for Starbucks, signifying their confidence in this collaboration with global icons.

- Expansion opportunity. Intense competition among global coffee chains like Starbucks and Costa, and local players such as Luckin Coffee and Manner Coffee, has driven a proliferation of coffee shops across countries, leading to a significant surge in coffee consumption. This trend is further fuelled by the growing demand for coffee makers and beans sourced internationally. Capitalising on immense growth prospects, Starbucks identifies substantial opportunities for expansion in China, where coffee consumption is on the rise due to increasing affluence and population. With rising coffee consumption in cities and a sizable middle-income consumer group, China remains a pivotal market for the coffee industry. Both global and domestic coffee chains are prioritising human connections, optimising performance, and investing in digital capabilities and innovation. In this pursuit, they are allocating more resources and manpower to penetrate smaller cities in China, aiming to tap into a larger consumer base while benefiting from lower costs in terms of management, labor, and rent compared to major cities. This strategic move enables large on-premise coffee brands to thrive and consolidate their presence in China’s rapidly evolving coffee landscape.

- Strength in its branding. Starbucks is poised to leverage the ongoing growth of the coffee industry and favorable customer preferences, ensuring continued success. Moreover, the company’s strong position is evident in its capacity to navigate potential economic downturns effectively. This resilience is attributed to its loyal membership program and a customer base that boasts relative affluence. These factors collectively fortify Starbucks’ market standing and reinforce its ability to thrive even in challenging economic conditions.

- 2Q23 earnings review. Revenue rose 14.5% YoY to $8.7bn, beating estimates by $270mn. Non-GAAP earnings per share was $0.74, $0.09 above expectations.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Take profit on China Southern Airlines (1055 HK) at HK$4.84. Add Alibaba Ltd (9988 HK) at HK$90, Coinbase Global Inc (COIN US) at US$98 and Airbnb Inc (ABNB US) at US$146. Cut loss on Genting Singapore (GENS SP) at S$0.935 and Livent Corporation (LTHM US) at US$24.95.