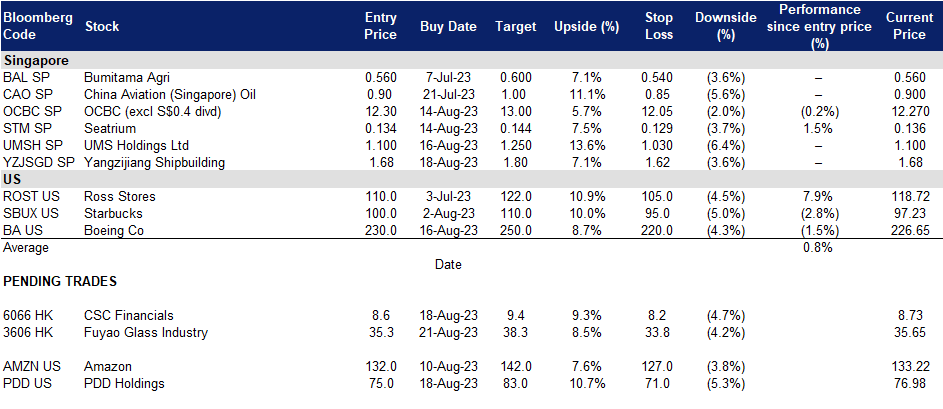

21 August 2023: Yangzijiang Shipbuilding (YZJSGD SP), Fuyao Glass Industry Group Co. Ltd. (3606 HK), Uber Technologies Inc. (UBER US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

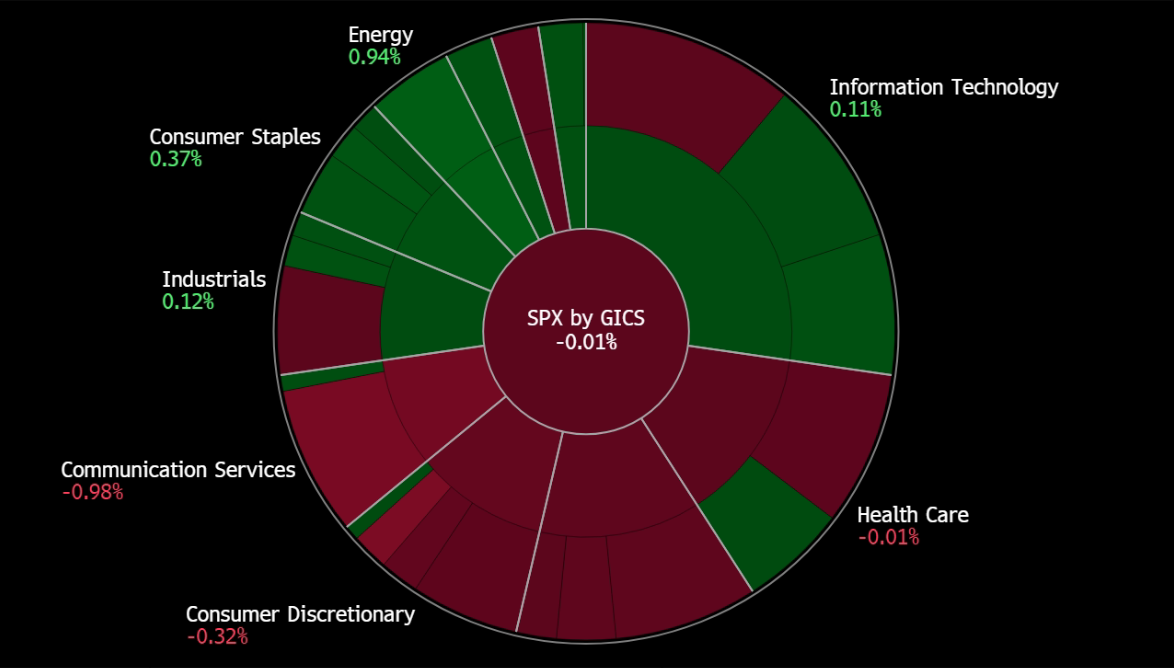

United States

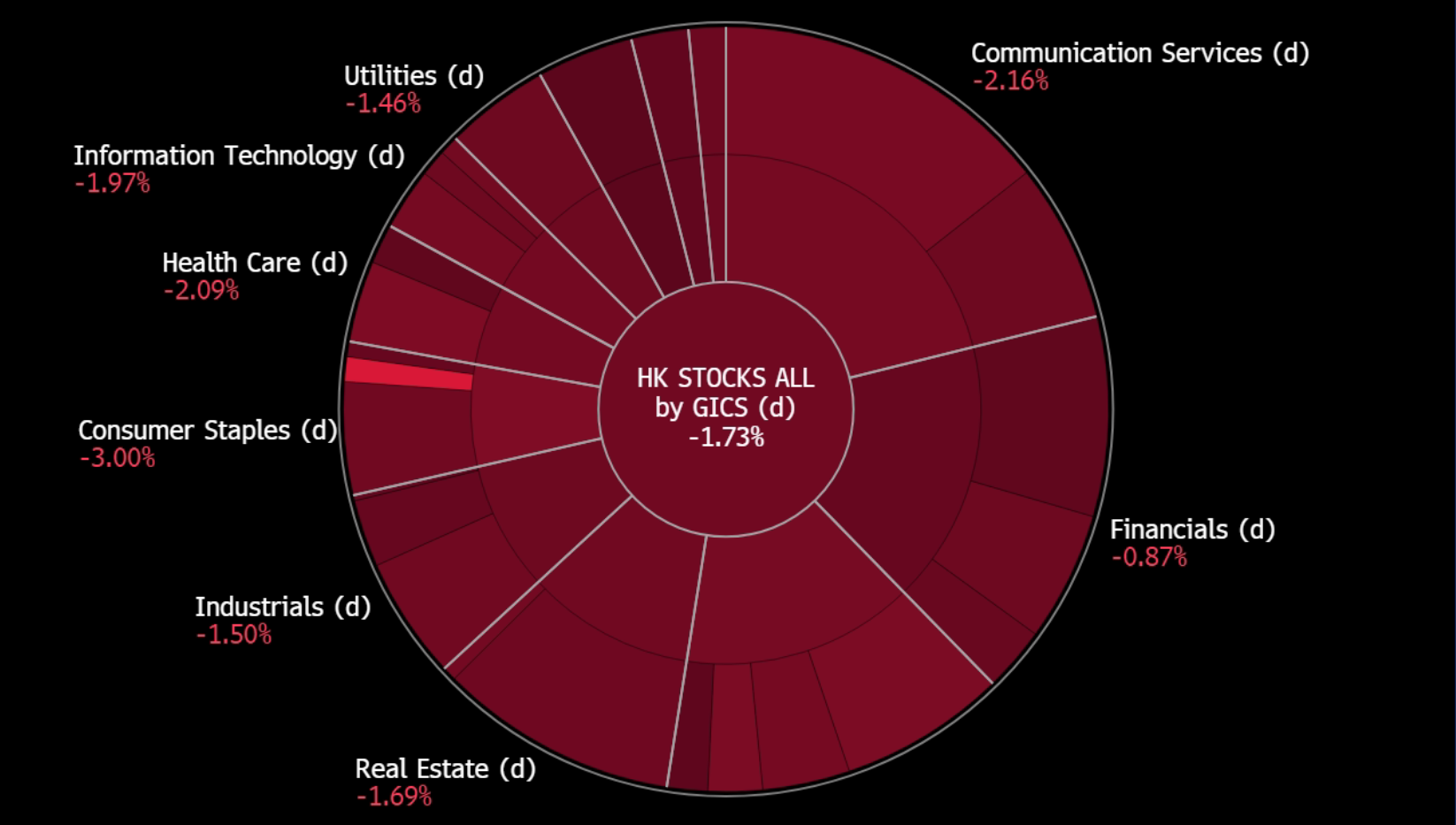

Hong Kong

Yangzijiang Shipbuilding (YZJSGD SP): Double bonanzas-record order book and weak RMB

- RE-ITERATE BUY Entry 1.68 – Target 1.80– Stop Loss – 1.62

- Yangzijiang Shipbuilding Holdings Limited builds a wide range of ships. The Company produces a wide range of commercial vessels, mini bulk carriers, multi-purpose cargo vessels, container ships, chemical tankers, offshore supply vessels, rescue and salvage vessels, and lifting vessels.

- Hedging against weakening RMB. Recent macro figures released from China showed a gloomy outlook as soft domestic, exports and property crisis continues to weaken confidence. USD/RMB recently broke 7.3, a low since November 2022. The authority has released multiple stimuli, but all are ineffective. The US Fed remains hawkish towards fighting against inflation, and hence, the US will keep rates high for the rest of 2023. There is downside room for RMB if China’s economy further slows down in 3Q23.

Share price and USD/RMB price trend comparison

(Source: Bloomberg)

- Shipbuilding outshines other sectors. According to the China Association of the National Shipbuilding Industry, new contracts secured by Chinese shipyards surged by 67.7% YoY in 1H23 with 123.77m dwt orders on hand as of June. Containerships and LNG carriers dominate the new orders. The newly-received orders and orders on hand in deadweight tonnage accounted for 49.6%, 72.6% and 53.2% of the global market share; the amount in gross tonnage accounted for 47.3%, 67.2% and 46.8% of the world volume, both ranking as number one in the global market.

- YTD orderbook exceeded the full-year target. As of June, the company has obtained orders for 72 vessels, amounting to a value of US$5.76 billion, surpassing its target of US$3 billion for 2023. This has resulted in the highest-ever outstanding orderbook value for Yangzijiang, standing at US$14.7 billion for 181 vessels. Among all ordered vessels, 91 are containerships, 29 are oil tankers, 53 are bulk carriers, and 8 are LNG/LPG/LEG.

- 1H23 results review. Revenue for 1H23 increased by 16% YoY to RMB11.3bn. Gross profit increased by 48% YoY to RMB2.1bn. GPM increased by 4ppts to 19%. PATMI increased by 26% YoY to RMB1.7bn.

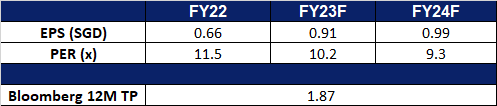

- Market consensus.

(Source: Bloomberg)

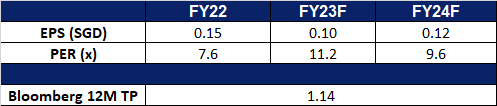

UMS Holdings (UMSH SP): Better outlook moving forward

- RE-ITEREATE BUY Entry 1.10 – Target – 1.25 Stop Loss –1.03

- UMS Holdings Limited provides equipment manufacturing and engineering services to Original Equipment Manufacturers (OEMs) of semiconductors and related products. The Company manufactures high precision components and complex electromechanical assembly and final testing services. UMS supports the electronic, machine tools and oil and gas industries.

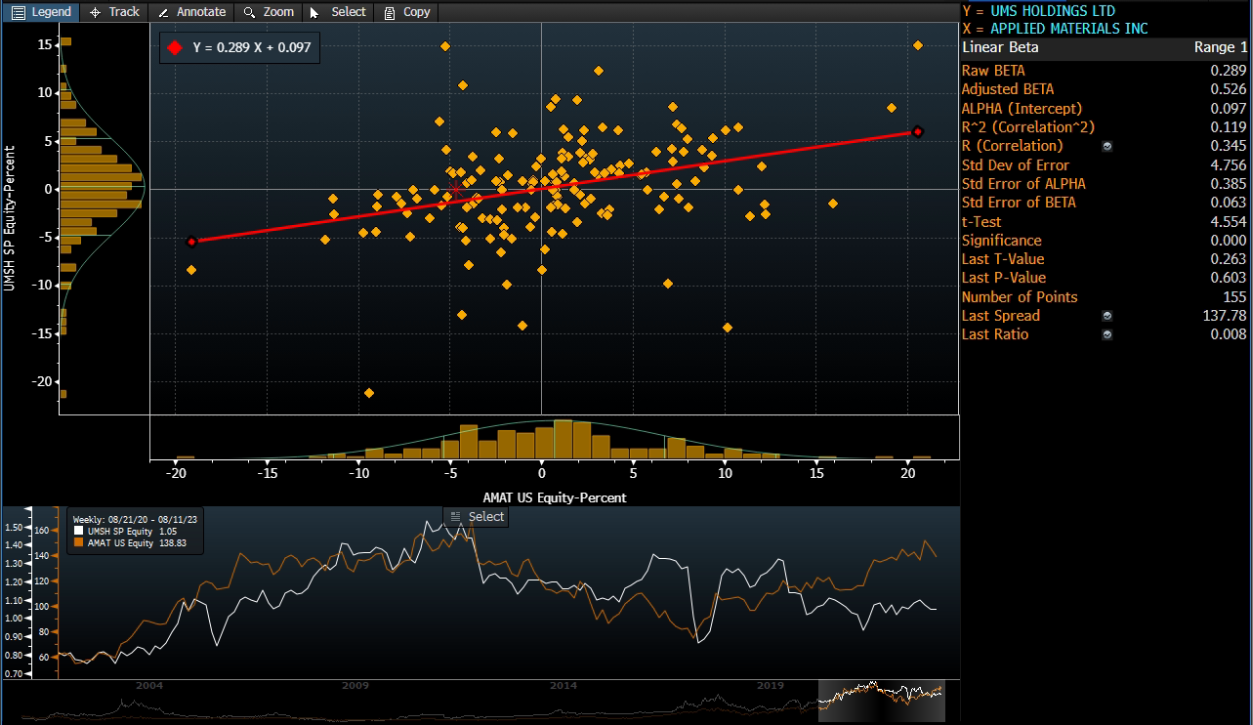

- Semiconductor sector is bottoming out. The milestone development of artificial intelligence (AI) in 1H23 not only buffers the downcycle of the semiconductor sector but also kickstarts a new growth engine. The AI hype shadows the fall in demand for mobile/PC chips due to the normalisation of life and the drop in capex due to geopolitical factors. However, several market leaders projected that the sector will bottom out in 2H23 or 1H24 as both orders and capex will gradually recover. In the UMS’s 2Q23 press release, according to SEMI, global 300mm fab equipment spending for front-end facilities next year is expected to begin a growth streak to hit a US$119 billion record high in 2026 following a decline in 2023.

- Applied Materials 3Q23 earnings preview. Applied Materials (AMAT US) is a key customer to UMS, and it will release its 3Q23 results on 17th August. Previously, AMAT guided its 3Q23 net sales to be US$6.15bn (plus or minus US$400mn), compared to a consensus of US$6.05bn. Non-GAAP adjusted diluted EPS was guided to be between US$1.56 and US$1.92, compared to a consensus of US$1.64.

Weekly return correlation between UMS and AMAT

(Source: Bloomberg)

(Source: Bloomberg)

- 2Q23 results review. Revenue fell 14% YoY to S$74.4mn. Gross material margin decreased to 46.3% from 51.7%. PATMI plugged 42% YoY to S$11.6mn. Net margin fell to 15.4% from 23.2%. The new plant in Penang is expected to contribute at least US$30mn for FY24. The company declared an interim dividend of 1.2 SG cents.

- Market consensus.

(Source: Bloomberg)

(Source: Bloomberg)

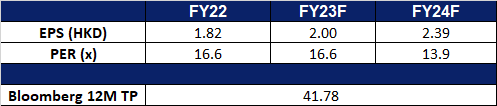

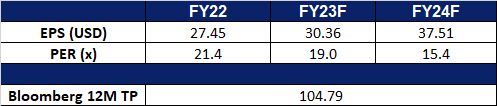

Fuyao Glass Industry Group Co. Ltd. (3606 HK): Beneficial sectoral conditions

- BUY Entry – 35.3 Target – 38.3 Stop Loss – 33.8

- FUYAO GLASS INDUSTRY GROUP CO., LTD. is a China-based company, principally engaged in the manufacture and distribution of float glasses and automobile glasses. The Company’s products portfolio consist of automobile glasses, such as coating glasses and others, which are applied in passenger cars, buses, limousines and others, and float glasses. The Company distributes its products within domestic markets and to overseas markets.

- Strong EV productions. With several EVs manufacturing companies in China hitting record sales in 1H2023, demand for EV is still expected to be strong for the rest of 2023. These companies have plans to increase their production capacity to capture the higher demand for EVs. China’s largest automaker, recently announced that it reached a total production of 5 million NEVs, just 9 months after it announced a production of 3 million NEVs. The increased level of production of EVs by these auto companies in China is expected to drive the demand for automobile glass produced by Fuyao Glass Industry Glass.

- Lower cost of production. China’s economy has slipped into deflation as consumer prices declined in July for the first time in more than two years. The official consumer price index, fell by 0.3% YoY in July. While this brings concerns to the performance of the China economy, it also lowers the cost of production for Fuyao Glass Industry as input materials become cheaper to purchase. The company would still be able to reap the benefits of a lower cost of production despite a faltering economy as EV production is still expected to remain strong.

- 1H23 results. Revenue improved to RMB15.0bn, +16.5% YoY, compared to RMB12.9bn in 1H22. Net profit rose to RMB2.8bn in HQ23, +19.08% YoY, compared to RMB2.4bn in 1H22. Basic and diluted EPS rose to RMB1.09 +19.8% YoY, compared to RMB0.91 in 1H22.

- Market Consensus.

(Source: Bloomberg)

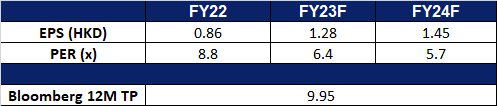

CSC Financials Co. Ltd. (6066 HK): More support expected

- RE-ITERATE BUY Entry – 8.6 Target – 9.4 Stop Loss – 8.2

- China Securities Co., Ltd. is mainly engaged in securities brokerage, securities investment consulting, financial advisers related to securities trading and securities investment activities, securities underwriting and sponsor, securities self-management, securities asset management, securities investment fund agent distribution, providing futures companies with medium introduction services, margin financing, financial products agent distribution, insurances facultative agent, stock options market making, securities investment fund trusteeship and precious metal products sales businesses.

- Expectations of lower stamp duties. China is currently considering reducing its stamp duty on stock trades to support its stock market. This aims at encouraging trading activity and volume and provides a boost to the market’s overall performance.The potential reduction of the stamp duty on stock trades is a significant development for investors and market participants, as it is expected to lower transaction costs and, in turn, increase the attractiveness of trading stocks for all investors. This move is in line with China’s ongoing efforts to deepen its capital markets and attract more local and foreign investments.

- Loan Prime Rate (LPR) cut. China’s central bank cut key interest rates unexpectedly last Tuesday. This is the second time in three months that the bank has cut rates, a sign that the government is taking steps to boost the economy. The People’s Bank of China (PBOC) lowered the rate on one-year medium-term lending facilities (MLFs) by 15 basis points, from 2.65% to 2.5%. The PBOC also injected 400 billion yuan (US$55 billion) into the financial system through these facilities. The market expects a cut in the loan prime rate (LPR) by 15 basis points in August, to 3.4%, aimed at improving the profitability of businesses and banks, and encouraging them to lend more money. This will help to boost economic activity and growth.

- 1Q23 results. Revenue improved to RMB6.7bn, up 5.81% YoY. Net profit rose to RMB2.4bn in 1Q23, up 57.8% YoY. Basic and diluted EPS were RMB0.28.

- Market Consensus.

(Source: Bloomberg)

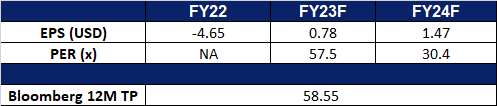

Uber Technologies Inc. (UBER US): Improving operations

- BUY Entry – 44 Target – 48 Stop Loss – 42

- Uber Technologies, Inc. develops and operates proprietary technology applications in the United States, Canada, Latin America, Europe, the Middle East, Africa, and Asia excluding China and Southeast Asia. It operates through three segments: Mobility, Delivery, and Freight.

- Finally profitable. Uber has achieved its first-ever operating profit in 2Q23, after facing years of losses due to aggressive growth strategies. Despite accumulating $31.5bn in operating losses since 2014, this turnaround came as a result of improved cost management and increased demand for ride-hailing and food delivery services following the pandemic. The CEO attributed this success to disciplined execution, record audience engagement, and strong growth. Uber’s financial turnaround was driven by its expansion into food deliveries, price adjustments, and cost-cutting measures. Despite competition from rivals like Lyft and DoorDash impacting growth, the company issued a stronger forecast for 3Q23, projecting higher earnings and bookings than analysts’ expectations.

- AI Integration. Uber is in the process of developing an AI-powered chatbot similar to ChatGPT to integrate into its app, following the footsteps of rivals DoorDash and Instacart who are also utilising language AI for customer service and automation. Uber CEO revealed that the company has been using machine learning and AI systems for years, particularly in tasks like matching users with cars or couriers. While he didn’t provide specific details about the capabilities of the chatbot, he highlighted Uber’s extensive experience with AI-driven algorithms. The chatbot will help to enhance Uber’s customer experience and streamline services.

- 2Q23 earnings review. Revenue rose 14% year-over-year to US$9.2bn, missing estimates by US$140mn. GAAP EPS of $0.18 beat expectations by $0.19.

- Market consensus.

(Source: Bloomberg)

PDD Holdings Inc (PDD US): Goods for cheap

PDD Holdings Inc (PDD US): Goods for cheap

- RE-ITERATE BUY Entry – 75 Target – 83 Stop Loss –71

- PDD Holdings Inc. is a multinational commerce group that owns and operates a portfolio of businesses. The Company focuses on the digital economy so that local communities and small businesses can benefit from the increased productivity and new opportunities. PDD Holdings has built a network of sourcing, logistics, and fulfilment capabilities for its underlying businesses.

- Defensive in the weak economic outlook. The economic outlook in China is looking bleak, with the country’s GDP growth forecast to slow down in 2023. Consumers will look towards purchasing cheaper substitutes. Chinese consumers, who have become more discerning, seek value for money and prioritise quality at reasonable prices. With attractive discounts and vouchers offered by domestic e-commerce platforms and brands, increased sales are expected, driven by pent-up demand and the preference for high-quality and new-generation products. The reported success of major Chinese e-commerce platforms during the last quarter further affirms the recovery in online consumer spending in China. PDD platform’s focus on fast-moving consumer goods (FMCG) and its unique approach of encouraging customers to join together in purchasing groups to maximise savings through bulk purchases will further contribute to its anticipated success ahead.

- Expanding its reach. Temu, PDD’s e-commerce platform, made its entry into the US market in September 2022. This Chinese-owned marketplace has expanded into around 27 countries, connecting predominantly Chinese merchants with customers in the US, Canada, Europe, and Australia; with recent expansions into Japan and South Korea. Temu distinguishes itself with its focus on ultra-low prices, achieved by reducing supply chain inefficiencies by sourcing products directly from manufacturers and cutting out middlemen; passing the savings to consumers. Its website and app heavily emphasise deals and discounts, allowing users to “shop like a billionaire”. This approach has led the platform to gain significant traction, surpassing popular platforms like Amazon, TikTok, and Instagram in download charts. Temu’s success is due to factors, including its appeal to budget-conscious customers, its focus on high-quality products, and its ability to offer competitive prices.

- Entrance to other Asian countries. Temu recently launched in South Korea. The app is offering coupons and discounts to attract new customers and is cooperating with third parties to provide logistics and delivery services. Temu is currently the No. 1 shopping app on Japan’s iOS store, and has not disclosed its next destination in Asia, but has sent out a survey to sellers asking about platforms in Japan, South Korea, and Southeast Asia. In South Korea, Temu will need to contend with other China-originated shopping apps such as Shein and AliExpress.

- 1Q23 earnings review. Revenue rose 58% year-over-year to US$5.48bn, beating estimates by US$920mn. Non-GAAP EPADS of $1.01 beat expectations by $0.38.

- Market consensus.

(Source: Bloomberg)

(Source: Bloomberg)

Trading Dashboard Update: Add Yangzijiang Shipbuilding (YZJSGD SP) at S$1.68.