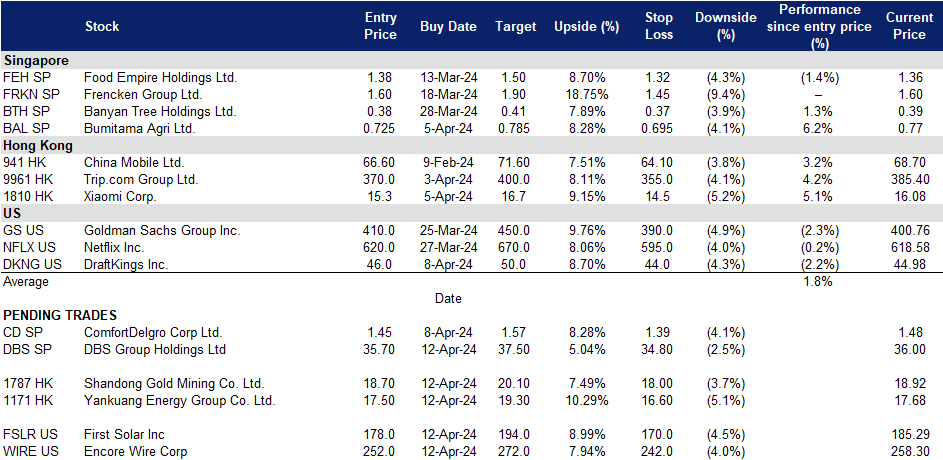

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

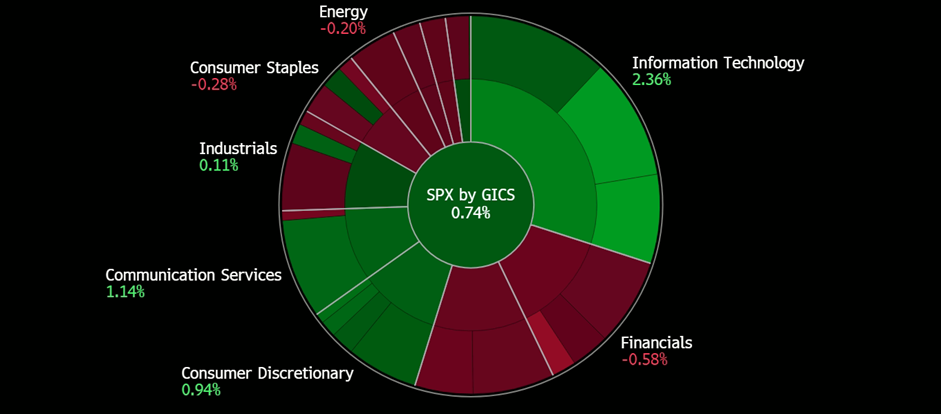

United States

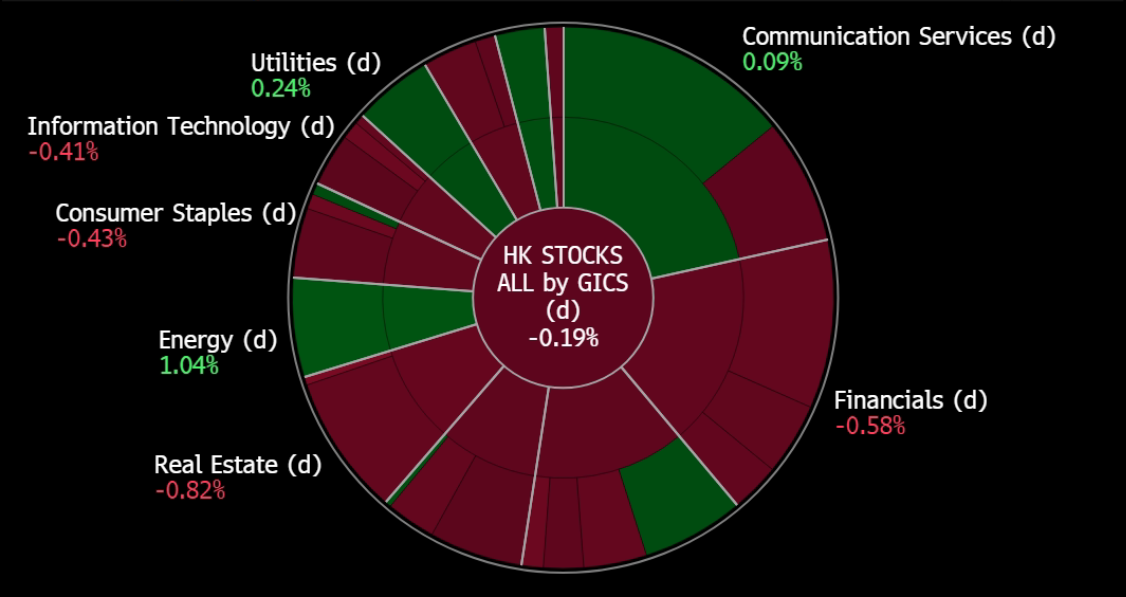

Hong Kong

DBS Group Holdings Ltd (DBS SP): Increase shareholders returns

- Entry – 35.7 Target– 37.5 Stop Loss – 34.8

- DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

- Bonus share issuance. On 19 April, DBS will pay out its Q4 final dividend amounting to 54 Singapore cents per share. On 30 April, DBS is expected to issue one bonus share for every 10 shares held and these shares will qualify for dividends from 1Q24. The increase in dividend payout and issuance of bonus shares is to increase capital returns to its shareholders.

- Expectations of monetary policy to remain unchanged. The Monetary Authority of Singapore (MAS) is expected to maintain its current monetary policy in the upcoming review. Despite inflation showing some volatility, core inflation remains above the central bank’s target. MAS may consider easing monetary settings in the second half of the year if inflation stabilizes. While inflation in Singapore remains elevated, forecasts suggest moderation throughout the year. Global central banks are cautiously adjusting interest rates, and MAS is likely to follow suit gradually, balancing growth and inflation concerns. Analysts suggest MAS may not rush to relax policy, considering Singapore’s role as a bellwether for global growth and the ongoing export-driven economic recovery. Policy easing, if any, is anticipated in October at the earliest, with MAS managing monetary policy through adjustments to the Singapore dollar’s exchange rate against its main trading partners. With the monetary policy expected to remain unchanged, DBS will continue to benefit from the high net interest margins for the coming quarters, allowing it to maintain its FY23 net interest income levels.

- New sustainability initiative. On 3 April, DBS Bank and Enterprise Singapore launched a programme to support local companies in becoming more sustainable. The initiative offers training, guidance, and financing options to SMEs and mid-cap companies, with around 100 expected to join the first cohort. Companies will receive support from sustainability specialists and can choose basic or intermediate training levels. By the end of the programme, participating firms should have a clear sustainability action plan. Enterprise Singapore will finance 70% of eligible activities per company until March 2026. The initiative aims to help businesses future-proof themselves, cut costs, and meet growing demand for sustainability.

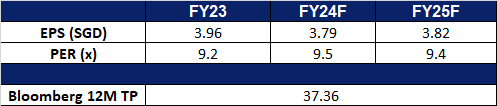

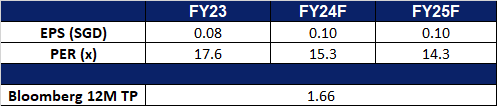

- FY23 results review. FY23 revenue rose by 22.2% YoY to S$20.1bn, compared to S$16.5bn in FY22. Net profit increased 25.5% YoY to S$10.3bn, compared to S$8.19bn in FY22. Basic EPS rose to S$3.87 in FY23 compared to S$3.15 in FY22. FY23 total dividend amounted to S$1.92 per share.

- Market Consensus

(Source: Bloomberg)

ComfortDelGro Corp Ltd (CD SP): Upbeat overseas expansion

- RE-ITERATE Entry – 1.45 Target– 1.57 Stop Loss – 1.39

- ComfortDelGro Corporation Limited provides land transportation services. The Company offers bus, taxi, rail, car rental and leasing, automotive engineering services, inspection and testing services, driving center, insurance broking services, and outdoor advertising.

- Regulatory changes in Singapore. The Land Transport Authority (LTA) is introducing new standards for taxi and ride-hailing operators to enhance service reliability and reduce operational costs. Operators must notify LTA, passengers, and drivers within an hour of any incidents affecting service provision. Taxi operators will see lower operating costs through changes like extending the lifespan of non-electric cabs and reducing inspection frequency for newer taxis. Regulatory tweaks aim to balance the regulatory burden between taxis and private-hire cars. While concerns over driver earnings persist, the proposed changes aim to stabilize the transport sector and maintain a balance between taxis and private-hire cars. These new standards will bolster ComfortDelGro’s efforts to enhance its Taxi & Private Hire segment in Singapore, aligning with the increasing demand for personal transportation services.

- Secured contracts in Manchester. Metroline Limited, a subsidiary of ComfortDelGro, has secured contracts valued at £422mn to operate four public-bus franchises in the UK for five years. Awarded by the Greater Manchester Combined Authority, the contracts include options for two one-year extensions. Metroline will operate 232 services with 420 buses and over 1,350 employees, doubling its services and representing a 30% increase over its London portfolio. ComfortDelGro’s track record positions it well to fulfill these contracts, according to its managing director Cheng Siak Kian. This move aligns with ComfortDelGro’s strategy to strengthen its core public transportation businesses and solidify its reputation as a leading multi-modal transport operator.

- Acquisition of A2B. Shareholders of Australian taxi network operator A2B voted overwhelmingly in favour of ComfortDelGro’s acquisition, with 97.7% of votes cast supporting the deal. ComfortDelGro proposed to acquire all shares in A2B Australia for A$1.45 per share, totaling A$165.1 million. The transaction is expected to be finalized in April 2024 pending court approval. Upon completion, A2B’s 8,000-vehicle network will complement ComfortDelGro’s global taxi fleet of 21,300 vehicles. ComfortDelGro’s managing director sees A2B as a strategic fit to expand the company’s point-to-point offerings and strengthen its presence in the Australian market. This acquisition aligns with ComfortDelGro’s strategy to grow and defend its core transport businesses, which contributed to a 4.2% revenue increase and a 76.5% net profit growth in H2 FY2023. Additionally, ComfortDelGro has been expanding its global presence through acquisitions and joint ventures, such as the recent acquisition of CMAC Group and securing contracts for metro lines in Paris and Stockholm.

- FY23 results review. FY23 revenue rose by 2.6% YoY to S$3,880.3mn, compared to S$3,780.8mn in FY22. Net profit inclined 4.3% YoY to S$180.5mn, compared to S$173.1mn in FY22. FY23 earnings would have risen 26.6% YoY, excluding the one-off gain of S$30.5mn from its sale of its Alperton property in London in FY22. The taxi and private hire business had a 59.5% YoY jump in operating profit to S$106.7mn in FY23. Basic EPS rose to S$8.33 in FY23 compared to S$7.99 in FY22. FY23 total dividend amounted to 6.66 sing cents per share.

- Market Consensus

(Source: Bloomberg)

Yankuang Energy Group Co. Ltd. (1171 HK): Demand for coal surging

- BUY Entry – 17.50 Target – 19.30 Stop Loss – 16.60

- Yankuang Energy Group Co Ltd is a China-based international comprehensive energy company engaged in coal and coal chemical industry. The Company operates in five segments. The Coal Mining segment is engaged in underground and open-cut mining, preparation and sale of coal and potash mineral exploration. The Smart Logistics segment provides railway transportation services. The Electricity and Heating Supply segment provides electricity and related heat supply services. The Equipment Manufacturing segment is engaged in the manufacture of comprehensive coal mining and excavating equipment. The Chemical Products segment is engaged in the production and sale of chemical products. The coal products mainly include thermal coal, pulverized coal injection (PCI), and coking coal. The coal chemical products mainly include methanol, ethylene glycol, acetic acid, ethyl acetate and crude liquid wax, among others. The Company distributes products in the domestic market and to overseas markets.

- Power demand is driving record-high thermal coal imports. In March, China significantly increased its imports of seaborne thermal coal to levels not seen in three months, capitalizing on lower international prices to meet surging domestic power needs. With power consumption soaring by 11% in January and February compared to the same period in 2023, and power generation growing by 6.9% in 2023—outpacing the overall economic growth of 5.2%—the demand for thermal coal surged. As the world’s largest coal producer and importer, China witnessed arrivals of seaborne thermal coal reaching 29.7mn metric tons in March, marking a notable increase from 23.03mn tons in February and surpassing the 28.62mn tons recorded in March 2023.

- Increased coal-fired power capacity. Despite its pledge to “strictly control” the use of coal, China spearheaded a worldwide surge in new coal-fired power plants last year, surpassing levels not seen in nearly a decade. According to the annual survey from Global Energy Monitor (GEM), China alone contributed two-thirds of the newly added coal-fired power capacity, installing 47.4 gigawatts (GW) out of the global total of 69.5GW. Furthermore, China initiated the construction of an additional 70.2GW of coal-power capacity in 2023, accounting for 95% of global construction starts and marking the country’s swiftest pace of groundbreaking since 2015. This uptick in coal-fired power capacity is expected to sustain heightened demand for coal in the foreseeable future.

- China reinstates coal tariffs. At the start of 2024, China has reinstated tariffs on coal imports. The reinstated tariffs include a 6% levy on coal for electricity and heating and a 3% tariff on coking coal used in steelmaking. Russia, South Africa, Mongolia, and the United States will be impacted by these tariffs, while Indonesia and Australia remain exempt due to free trade agreements with China. The implementation of these tariffs is likely to drive up domestic coal production and demand as there is less competition from foreign coal companies. This allows domestic producers like Yankuang Energy to extend their competitive edge in the Chinese market.

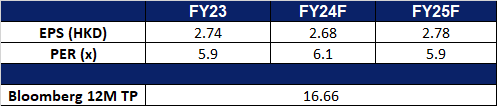

- FY23 earnings. Revenue fell by 23.4% YoY to RMB118.4bn in FY23, compared to RMB154.6bn in FY22. Net profit fell 41.3% YoY to RMB23.0bn in FY23, compared to RMB39.1bn in FY22. Basic EPS fell to RMB2.39 in FY23, compared to RMB4.10 in FY22.

- Market Consensus.

(Source: Bloomberg)

Shandong Gold Mining Co. Ltd. (1787 HK): Record Gold Prices

- RE-ITERATE BUY Entry – 18.70 Target – 20.10 Stop Loss – 18.00

- Shandong Gold Mining Co., Ltd. is a China-based company principally engaged in the mining, processing and sales of gold. The Company operates two segments. The Gold Mining segment is engaged in the mining of gold ore. The Gold Refining segment is engaged in the production and sales of gold. The Company is also engaged in the distribution of other metals extracted during the gold ore smelting process, such as silver, copper, iron, lead and zinc. The Company conducts its businesses in domestic and overseas markets.

- Gold prices all time high. Gold prices rose past $2,320 an ounce last Friday, touching a new record high and building on the gains for the third straight week. The precious metal has been supported by US interest rate cut bets, speculative buying and central bank purchases, amid strong US job growth in March. The country’s economy added the most jobs in 10 months, while jobless rate dropped below forecasts, indicating the continued tightness in the labor market and supporting the case for the interest rates to remain restrictive longer.

- Continued global geopolitical tension and economic uncertainties. The ongoing Israle-Hamas conflict is likely to continue escalate regional tensions. Recently, suspected Israeli warplanes bombed Iran’s embassy in Syria on Monday in a strike that Iran said killed seven of its military advisers, including three senior commanders, marking a major escalation in Israel’s war with its regional adversaries. Red sea attacks by the Houthis, as well as the recent Baltimore bridge incident, has caused more uncertainty in the global economy. Rising global geopolitical tensions and economic uncertainties lead to the pursuit of safe haven assets such as gold.

- Increasing controlling stake of Gold Mine in Inner Mongolia. Shandong Gold Mining, recently announced that it plans to buy a controlling stake in the operator of a gold mine in China’s northeastern Inner Mongolia Autonomous Region. The company will be acquiring a 70% stake in Baotou Changtai Mining for RMB471mn (US$66mn). The acquisition will bring Shandong Gold over 16 tons of new proven gold resource holdings, which may grow to more than 20 tons as the exploration progresses this year. This also marks the third gold mine acquisition that Shandong Gold and its controlled companies announced this year.

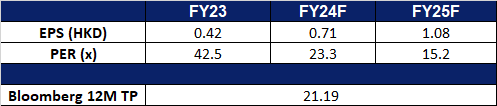

- FY23 results. Total revenue increased by 17.8% YoY to RMB59.3bn in FY23, compared to RMB50.3bn in FY22. Gross profit increased by 39.9% to RMB6.63bn in FY23, compared to RMB6.17bn in FY22. Net profit increased by 108.5% YoY to RMB2.82bn in FY23, compared to RMB1.35bn in FY22.

- Market Consensus.

(Source: Bloomberg)

Encore Wire Corp (WIRE US): Continued growth of electrical demand

- BUY Entry – 252 Target – 272 Stop Loss – 242

- Encore Wire is a low-cost manufacturer of building copper wire and cable, producing NM-B cable (a sheathed cable used for wiring homes, apartments, and manufactured homes) and UF-B. Its stock units include THWN-2 cable, insulated feeders, circuits and branch wiring for commercial and industrial buildings, and other wires including SEU, SER, PV, URD, tray cable, metal clad and armoured cable. The company’s primary customers are electrical wholesale distributors who sell its products to electrical contractors.

- North America faces power shortages. According to a March report by the North American Electric Reliability Corporation (NERC), 300mn people in the United States and Canada will face power shortages in 2024. Current electricity demand is greater than at any time in the past 5 years. The North American economy is continuing to grow, and electricity demand is also growing. Driven by the wave of artificial intelligence, data centres will be built in large numbers in the next few years, so power consumption will expand rapidly. The popularity of new energy vehicles is also driving up electricity demand. The report warns that extreme weather events, such as heat waves and droughts, could further exacerbate power shortages. These events can damage power infrastructure and make it more difficult to generate electricity.

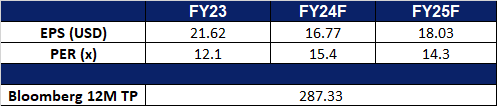

- 4Q23 earnings review. Revenue was US$634mn, falling 8.7% YoY, beating expectations by US$32.3mn. GAAP earnings per share were US$4.10, beating expectations by US$0.08. As of December 23, the company had no debt and US$560mn in cash and cash equivalents, representing approximately 14.3% of its market capitalisation.

- Market consensus.

(Source: Bloomberg)

First Solar Inc (FSLR US): Next sector to benefit from the AI wave

- RE-ITERATE BUY Entry – 178 Target – 194 Stop Loss – 170

- First Solar, Inc. designs and manufactures solar modules. The Company uses a thin film semiconductor technology to manufacture electricity-producing solar modules.

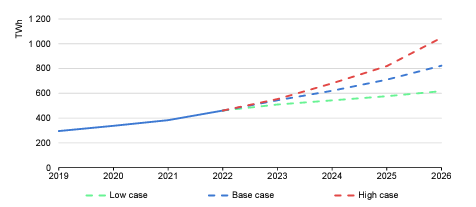

- Doubled electricity demand from data centres towards 2026. The 2024 IEA electricity report shows that global electricity demand from data centres, cryptocurrencies, and artificial intelligence (AI) is projected to nearly double by 2026, reaching between 620 and 1,050 terawatt-hours (TWh), with a base case of just over 800 TWh, up from 460 TWh in 2022. This surge in demand, driven by the expansion of digitalization, poses challenges and opportunities for various regions. In the United States, data centre electricity consumption is forecasted to rise rapidly, with Virginia’s data centre sector becoming a significant economic driver. China anticipates doubling its data centre electricity demand by 2030, while the European Union aims to bolster sustainable practices in data centres to align with decarbonization goals. In Ireland, data centres are expected to consume almost one-third of the country’s electricity by 2026. Efforts to enhance energy efficiency and regulatory measures are underway globally to mitigate the environmental impact of escalating electricity consumption in data centres. First Solar stands to benefit from the projected surge in electricity demand as solar energy can help these data centres to mitigate the environmental impact of escalating electricity consumption by providing renewable and sustainable power sources, thus contributing to the reduction of carbon emissions and promoting greener operations.

Global electricity demand from data centres, AI and cryptocurrencies

(Source: IEA electricity 2024 report)

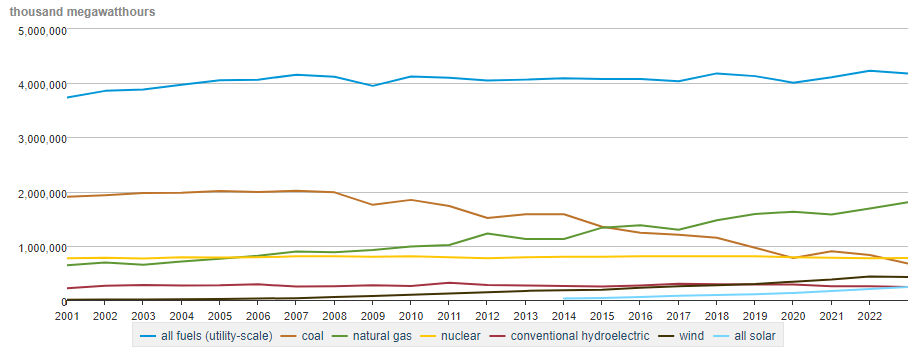

- Solar demand to grow. In the coming years, solar panel installations are predicted to substantially increase in the United States to meet the soaring electricity demand, driven particularly by data centres, electric vehicles, and heating/cooling systems. This surge comes as legacy power plants retire, and solar emerges as a cost-effective and rapid solution. Solar energy, being one of the fastest-growing energy sources in the US, is expected to expand significantly despite challenges like permitting delays and increased capital costs. In response to the growing demand, solar companies plan to boost their manufacturing capacity, buoyed by tax incentives under President Biden’s Inflation Reduction Act.

Net electricity generation in the United States

(Source: US Energy Information Administration)

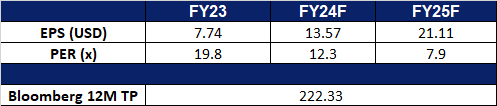

- 4Q23 earnings review. Revenue was US$1.16bn, rising 16.0% YoY, missing expectations by US$160mn. GAAP earnings per share were US$3.25, beating expectations by US$0.13. The company issued FY24 guidance for revenue of US$4.4B to US$4.6B and EPS US$13 to US$14, compared to analyst consensus estimates of US$4.56B of revenue and EPS of US$13.26. FSLR also forecast full-year sales volumes of 15.6 to 16.3 GW, gross margin of US$2bn to US$2.1bn, and operating income of US$1.5bn to US$1.6bn on sales volume of 15.6 to 16.3 GW, which includes anticipated Section 45X tax credits of US$1bn to US$1.05bn and US$85mn to US$95mn of production start-up expense; year-end net cash balance is projected at US$900mn to US$1.2bn.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Take profit on China Resources Power Holdings Co. Ltd. (836 HK) at HK$19.3. Cut loss on Yangzijiang Shipbuilding (YZJSGD SP) at S$1.82, Keppel Ltd (KEP SP) at S$7.23, NVIDIA Corp (NVDA US) at US$850 and BlackRock Inc (BLK US) at US$783.7.