United States | Singapore | Hong Kong | Earnings

Boeing, Inc. (BA US)

- Shares closed higher above the 20dEMA with constructive volume. 5dEMA is about to cross the 20dEMA.

- MACD is positive, RSI is constructive.

- Long – Entry 177, Target 193, Stop 169

Ambarella, Inc. (AMBA US)

- Shares closed higher above the 20dEMA with constructive volume. 5dEMA is about to cross the 20dEMA

- MACD is positive, RSI is constructive.

- Long – Entry 46.3, Target 50.3, Stop 44.3

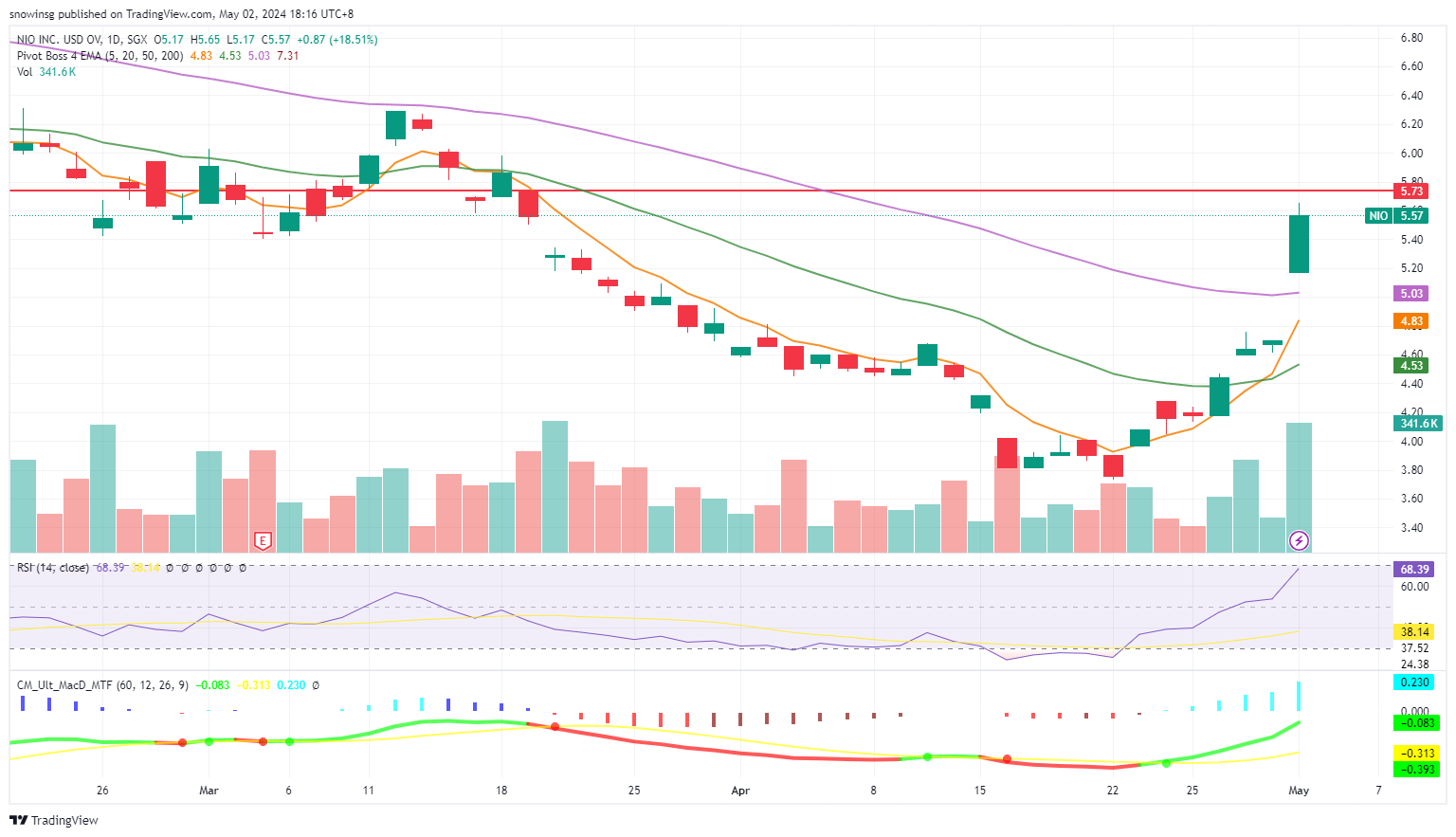

NIO Inc (NIO SP)

- Shares closed above the 50dEMA with a jump in volume.

- Both RSI and MACD are constructive.

- Long – Entry 5.37, Target 5.73, Stop 5.19

SIA Engineering Co Ltd (SIE SP)

- Shares closed above the 50dEMA with rising volume. The 5dEMA touched the 50dEMA.

- Both RSI and MACD are constructive.

- Long – Entry 2.26, Target 2.38, Stop 2.20

Standard Chartered PLC (2888 HK)

- Shares closed at a 6-month high above the 5dEMA with a surge in volume.

- MACD is constructive, while RSI is at an overbought level.

- Long – Entry 69.6, Target 74.8, Stop 67.0

ASMPT Ltd (522 HK)

- Shares closed above the 20dEMA with an increase in volume. The 5dEMA is about to cross the 20dEMA.

- RSI is constructive, while MACD is about to turn positive.

- Long – Entry 100.0, Target 108.8, Stop 95.6

Novo Nordisk A/S (NVO)

- 1Q24 Revenue: DKK65.35B, +22.4% YoY

- 1Q24 GAAP EPADR: DKK5.68

- FY24 Guidance: Expect sales growth to be to be 19%-27% at CER, and operating profit growth is now expected to be 22%-30% at CER. Growth reported in Danish Kroner is now expected to be in line with CER growth for both sales and operating profit. The effective tax rate for 2024 is still expected to be in the range of 19%-21%. Capital expenditure is still expected to be around DKK 45B in 2024. The free cash flow is now expected to be DKK 57B-67B. Depreciation, amortisation and impairment losses are still expected to be around DKK 10B.

- Comment: Novo Nordisk reported better-than-expected Q1 profits, with strong demand for Wegovy but lower-than-expected sales. The company revised its 2024 outlook upwards, driven by efforts to increase production of its weight-loss treatment Wegovy, though price cuts due to competition from Eli Lilly impacted its shares. Despite ongoing supply challenges, Novo anticipates significant sales and profit growth this year, fuelled by expanding market reach and enhanced production capacity. Eli Lilly, Novo’s competitor, is also expanding its manufacturing capacity for its obesity treatment, which will impact net pricing of Wegovy and Ozempic in the US. However, with Novo gradually increasing its supply of lower strengthen Wegovy doses in the US, to meet the high demands, more patients are able to start on their weekly injection treatment. 2Q24 recommended trading range: $115 to $140. Positive Outlook.

诺和诺德(NVO)

- 24财年第一季营收:653.5亿丹麦克朗,同比增幅22.4%

- 24财年第一季GAAP每股盈利:5.68丹麦克朗

- 24财年指引:预计销售额增长率为19%至27%,营业利润增长率为22%至30%。以丹麦克朗计算的增长预计将与按不变利率销售和营业利润的增长保持一致。预计2024年的有效税率仍将在19%至21%之间。2024年的资本支出预计仍将在450亿丹麦克朗左右。自由现金流目前预计为570亿至670亿丹麦克朗。折旧、摊销和减值损失预计仍在100亿丹麦克朗左右。

- 短评:诺和诺德公布的第一季度利润好于预期,Wegovy需求强劲,但销售额低于预期。由于努力增加其减肥药物Wegovy的产量,该公司上调了2024年的预期,尽管由于来自礼来的竞争而导致的价格下调影响了其股价。尽管持续的供应挑战,Novo预计今年的销售额和利润将显著增长,主要得益于扩大市场覆盖范围和提高产能。诺和的竞争对手礼来也在扩大其肥胖治疗药物的生产能力,这将影响Wegovy和Ozempic在美国的净定价。然而,随着公司逐渐增加其在美国低强度Wegovy剂量的供应,以满足高需求,更多的患者能够开始每周注射治疗。24财年第二季度建议交易区间:115美至140美元。积极前景。

Apple Inc (AAPL)

- 2Q24 Revenue: $90.8B, -4.3% YoY, beat estimates by $190M

- 2Q24 GAAP EPS: $1.53, beat estimates by $0.03

- FY24 Guidance: No guidance provided.

- Dividend: Apple’s board of directors has declared a cash dividend of $0.25 per share of the Company’s common stock, an increase of 4%. The dividend is payable on 16 May 2024 to shareholders of record.

- Share repurchase: The board of directors authorized an additional program to repurchase up to $110bn of the Company’s common stock.

- Comment: Apple’s quarterly results surpassed expectations, boasting a profit of US$23.6bn. The company also announced a record share buyback program of an additional US$110bn and increased its cash dividend by 4%. While quarterly revenue saw a slight decline, Apple’s CEO remains confident in revenue growth for the current quarter. Despite challenges in the smartphone market, particularly from China, iPhone sales reached US$45.7bn, reflecting a 10.5% YoY decline, slightly below analysts’ expectations of US$46bn. Excluding a one-time US$5bn surge in sales in 2Q23 due to supply chain issues, iPhone sales only experienced a marginal decline YoY. Apple anticipates growth in services and iPad revenue for the current quarter, with services segment sales exceeding analyst forecasts at US$23.87bn and Mac sales reaching US$7.5bn, surpassing estimates of US$6.86bn. Despite competition and regulatory pressures, Apple’s massive share buyback aims to garner investor trust and buy time for future developments, including investments in generative AI. 3Q24 recommended trading range: $175 to $195. Positive Outlook.

苹果(AAPL)

- 24财年第二季营收:908亿美元,同比跌幅4.3%,超预期1.9亿美元

- 24财年第二季GAAP每股盈利:1.53美元,超预期0.03美元

- 24财年指引:不提供指引。

- 股息:苹果董事会宣布向股东派发每股普通股0.25美元的现金股息,增幅为4%。股息于2024年5月16日支付给记录在案的股东。

- 股票回购:董事会授权了一项额外的计划,以回购公司高达1,100亿美元的普通股。

- 短评:苹果公司的季度业绩超出预期,利润达到236亿美元。该公司还宣布了一项额外1,100亿美元的创纪录股票回购计划,并将现金股息提高了4%。虽然季度收入略有下降,但苹果首席执行官对当前季度的收入增长仍充满信心。尽管智能手机市场面临挑战,尤其是来自中国的挑战,但iPhone的销售额达到457亿美元,同比下降10.5%,略低于分析师460亿美元的预期。除去供应链问题导致的23年第二季度50亿美元的一次性销售额激增,iPhone的销售额同比仅略有下降。苹果预计,本季度服务和iPad的收入将出现增长,服务部门的销售额将超过分析师的预测,达到238.7亿美元,Mac的销售额将达到75亿美元,超过68.6亿美元的预期。尽管面临竞争和监管压力,苹果大规模回购股票的目的是赢得投资者的信任,为未来的发展争取时间,包括对生成式人工智能的投资。24财年第三季度建议交易区间:175美至195美元。积极前景。

Coinbase Global Inc (COIN)

- 1Q24 Revenue: $1.64B, +112.3%YoY, beat estimates by $300M

- 1Q24 GAAP EPS: $4.40, beat estimates by $3.33

- FY24 Guidance: No guidance provided.

- Comment: Coinbase Global reported a significant turnaround in its first-quarter earnings, swinging from a loss of US$79mn a year ago to a profit of US$1.2bn, or US$4.84 per share. This surge in profitability was driven by increased cryptocurrency trading, spurred by the launch of the first US listed exchange traded funds (ETFs) tracking bitcoin in January. Despite the strong report, analysts and investors are concerned about potential decreases in trading volumes amid downward movements in bitcoin prices. The company benefited from its role as custodian for several spot bitcoin ETFs, including BlackRock’s iShares Bitcoin Trust, which contributed to renewed investor enthusiasm in digital assets. Coinbase’s trading volumes in the first quarter reached US$312bn, up from US$145bn a year earlier. The company’s interest income also saw a significant boost, reaching US$66.7mn in the first quarter compared to US$43.3mn the year prior, driven by higher interest rates and increased interest from reserves in USD Coin (USDC). Coinbase’s CEO credited Coinbase’s low cost structure and continued innovation for its success. Looking ahead Coinbase will continue to benefit from the high interest rates to boost its interest income as it is expected to remain higher for longer, with no signs of a rate cut in the coming month. 2Q24 recommended trading range: $200 to $270. Positive Outlook.

Coinbase 全球(COIN)

- 24财年第一季营收:16.4亿美元,同比增幅112.3%,超预期3亿美元

- 24财年第一季GAAP每股盈利:4.40美元,超预期3.33美元

- 24财年指引:不提供指引。

- 短评:Coinbase 全球报告称,其第一季度收益出现了重大转变,从一年前的亏损7,900万美元转变为盈利12亿美元,合每股4.84美元。今年1月,首批追踪比特币的美国上市ETF的推出,刺激了加密货币交易的增加,推动了盈利能力的飙升。尽管报告表现强劲,但分析师和投资者担心,随着比特币价格下跌,交易量可能会减少。该公司受益于其作为几只现货比特币ETF(包括贝莱德的iShares比特币信托基金)托管人的角色,这有助于重振投资者对数字资产的热情。Coinbase第一季度的交易量达到3,120亿美元,高于去年同期的1,450亿美元。该公司的利息收入也出现了显著增长,第一季度达到6,670万美元,而去年同期为4,330万美元,这主要得益于利率上升和美元币储备利息的增加。Coinbase的首席执行官将其成功归功于低成本结构和持续创新。展望未来,Coinbase将继续受益于高利率,以提高其利息收入,因为预计它将在更长时间内保持较高水平,而未来一个月没有降息的迹象。24财年第二季度建议交易区间:200美至270美元。积极前景。

Block Inc (SQ)

- 1Q24 Revenue: $5.96B, +19.4% YoY, beat estimates by $140M.

- 1Q24 Non-GAAP EPS: $0.85, beat estimates by $0.12

- FY24 Guidance: No guidance provided.

- Comment: Block exceeded analysts’ expectations in its first-quarter earnings report. The company reported adjusted earnings per share of US$0.85, surpassing the estimated US$0.72, and revenue of US$5.96bn, higher than the expected US$5.82bn. Gross profit reached US$2.09bn, up 22% YoY. Net income quadrupled to US$472mn, compared to US$98.3mn a year earlier. The Cash App business saw significant growth, with gross profit reaching US$1.26bn, and monthly active users for the Cash App Card rising to 24mn in March. Despite ongoing scrutiny and a federal probe into compliance practices, Block remains optimistic about its performance and future prospects. Its CEO addressed concerns about the company’s focus on Bitcoin, stating that less than 3% of resources are dedicated to Bitcoin-related projects. Block plans to invest 10% of gross profit from bitcoin products into purchasing bitcoin for investment. Despite recent challenges, including layoffs and regulatory investigations, Block is raising its outlook for the year to reflect its strong performance in the first quarter and aims to integrate its Afterpay company into its operations. 2Q24 recommended trading range: $70 to $90. Positive Outlook.

Block (SQ)

- 24财年第一季营收:59.6亿美元,同比增幅19.4%,超预期1.4亿美元

- 24财年第一季Non-GAAP每股盈利:0.85美元,超预期0.12美元

- 24财年指引:不提供指引。

- 短评:Block在第一季度的收益报告中超出了分析师的预期。该公司报告调整后每股收益为0.85美元,超过预期的0.72美元,收入为59.6亿美元,高于预期的58.2亿美元。毛利润达到20.9亿美元,同比增长22%。净利润翻了两番,达到4.72亿美元,而去年同期为9,830万美元。现金应用业务大幅增长,毛利润达到12.6亿美元,现金应用卡的月活跃用户在3月份上升至2400万。尽管正在进行审查,联邦政府也在调查合规行为,但布洛克对其业绩和未来前景仍持乐观态度。该公司首席执行官对公司对比特币的关注表示担忧,称只有不到3%的资源专门用于比特币相关项目。Block计划将比特币产品毛利润的10%用于购买比特币进行投资。尽管最近面临裁员和监管调查等挑战,Block仍提高了今年的预期,以反映其第一季度的强劲表现,并计划将旗下的Afterpay公司整合到其运营中。24财年第二季度建议交易区间:70美至90美元。积极前景。

Draftkings Inc (DKNG)

- 1Q24 Revenue: $1.18B, +53.2% YoY, beat estimates by $60M

- 1Q24 Non-GAAP EPS: $0.03, beat estimates by $0.14

- FY24 Guidance: Raise the midpoint of its FY24 revenue guidance to $4.9B from $4.775B vs $4.82B consensus and the midpoint of our Adjusted EBITDA guidance to $500M from $460M as a result of excellent first quarter results and improved outlook on customer acquisition and engagement for the rest of 2024.

- Comment: DraftKings surpassed analysts’ estimates in its Q1 earnings report and raised its revenue guidance. Revenue surged by 53% YoY to US$1.18bn, driven by robust customer engagement, efficient acquisition of new customers, and expansion into new jurisdictions for its sportsbook product. The company’s monthly unique paying customers increased to 3.4mn, with average revenue per MUP up by 25% YoY. DraftKings reported adjusted EBITDA of US$22.4mn and adjusted EPS of US$0.03. Looking ahead, DraftKings raised its 2024 revenue guidance to a midpoint of US$4.9bn, reflecting the introduction of legislation in nine jurisdictions for mobile sports betting legalization, representing around 11% of the US population. 2Q24 recommended trading range: $40 to $50. Positive Outlook.

Draftkings (DKNG)

- 24财年第一季营收:11.8亿美元,同比增幅53.2%,超预期6,000万美元

- 24财年第一季Non-GAAP每股盈利:0.03美元,超预期0.14美元

- 24财年指引:将其24财年收入指导的中点从47.75亿美元提高到49亿美元,而市场预期为48.2亿美元,调整后EBITDA指导的中点从4.6亿美元提高到5亿美元,这是由于第一季度业绩出色,以及2024年剩余时间客户获取和参与前景改善。

- 短评:DraftKings在其第一季度收益报告中超过了分析师的预期,并提高了收入预期。营收同比增长53%,至11.8亿美元,这主要得益于强劲的客户参与度、高效的新客户获取以及其体育博彩产品向新司法管辖区的扩张。该公司的每月独立付费用户(MUP)增加到340万,每个MUP的平均收入同比增长25%。DraftKings报告调整后的EBITDA为2240万美元,调整后的每股收益为0.03美元。展望未来,DraftKings将其2024年的收入指导上调至49亿美元的中间值,这反映了代表美国约11%人口的9个司法管辖区对移动体育博彩合法化的立法。24财年第二季度建议交易区间:40美至50美元。积极前景。

Cloudflare Inc (NET)

- 1Q24 Revenue: $378.6M, +30.5% YoY, beat estimates by $5.32M

- 1Q24 Non-GAAP EPS: $0.16, beat estimates by $0.03

- 2Q24 Guidance: Expect total revenue of $393.5 to $394.5M, Non-GAAP income from operations of $35.0 to $36.0M and Non-GAAP net income per share of $0.14, utilizing weighted average common shares outstanding of approximately 360M.

- FY24 Guidance: Expect total revenue of $1,648.0 to $1,652.0M, Non-GAAP income from operations of $160.0 to $164.0M and Non-GAAP net income per share of $0.60 to $0.61, utilizing weighted average common shares outstanding of approximately 361M.

- Comment: Cloudflare reported strong revenue growth of 30.5% YoY in the first quarter, reaching US$378.6mn, alongside adjusted profit rising to US$0.16 per share, surpassing estimates. However, the company faced a wider quarterly operating loss of US$54.6mn due to increased expenses, particularly in sales and marketing, which surged about 42% YoY to US$194.1mn. Despite this, Cloudflare added 122 new large customers in the quarter, totalling 2,878, a 33% YoY increase. Revenue from large customers rose to 67% YoY, indicating the company’s success in moving upmarket. Cloudflare delivered a gross margin of 79.5% and an operating profit of US$42.4mn. For the second quarter, the company expects revenue between US$393.5mn and US$394.5mn, in line with analysts’ estimates. Cloudflare remains optimistic about its long-term prospects despite short-term uncertainties in the geopolitical landscape. For the FY24, the company anticipates revenue in the range of US$1.648bn to US$1.652bn and operating income between US$160mn to US$164mn. Looking ahead, the persisting high interest rate environment will likely affect enterprise budgets, as businesses prioritize protecting their bottom line amidst ongoing economic uncertainty. This could potentially impact Cloudflare’s top and bottom lines. 2Q24 recommended trading range: $70 to $85. Negative Outlook.

Cloudflare (NET)

- 24财年第一季营收:3.786亿美元,同比增幅30.5%,超预期532万美元

- 24财年第一季每股盈利:0.16美元,超预期0.03美元

- 24财年第二季指引:预计总收入为3.935亿至3.945亿美元,Non-GAAP运营收入为3,500万至3,600万美元,Non-GAAP每股净收入为0.14美元,基于约3.6亿股加权平均普通股流通股。

- 短评:Cloudflare报告称,第一季度收入同比增长30.5%,达到3.786亿美元,调整后每股利润上升至0.16美元,超出预期。然而,由于费用增加,特别是销售和营销费用增加,公司面临5,460万美元的季度经营亏损,同比增长约42%,达到1.941亿美元。尽管如此,Cloudflare在本季度增加了122个新的大客户,总计2,878个,同比增长33%。来自大客户的收入同比增长67%,表明该公司在向高端市场进军方面取得了成功。Cloudflare的毛利率为79.5%,营业利润为4240万美元。该公司预计第二季度营收在3.935亿美元至3.945亿美元之间,与分析师的预期相符。尽管短期内地缘政治环境存在不确定性,但Cloudflare仍对其长期前景持乐观态度。对于本财年,公司预计收入在16.48亿至16.52亿美元之间,营业收入在1.6亿至1.64亿美元之间。展望未来,持续的高利率环境可能会影响企业预算,因为企业在持续的经济不确定性中优先考虑保护自己的底线。这可能会影响Cloudflare的收入和利润。24财年第二季度建议交易区间:70美至85美元。负面前景。

Fortinet Inc (FTNT)

- 1Q24 Revenue: $1.35B, +7.1% YoY, beat estimates by $10M

- 1Q24 Non-GAAP EPS: $0.43, beat estimates by $0.05

- 2Q24 Guidance: Expect revenue in the range of $1.375B to $1.435B, billings in the range of $1.490B to $1.550B, Non-GAAP gross margin in the range of 76.50% to 77.50%, Non-GAAP operating margin in the range of 25.75% to 26.75% and diluted non-GAAP net income per share in the range of $0.39 to $0.41, assuming a non-GAAP effective tax rate of 17%. This assumes a diluted share count of 775 million to 785 million.

- FY24 Guidance: Expect revenue in the range of $5.745B to $5.845B, service revenue in the range of $3.940B to $3.990B, billings in the range of $6.400B to $6.600B, Non-GAAP gross margin in the range of 76.50% to 78.00%, Non-GAAP operating margin in the range of 26.50% to 28.00% and diluted non-GAAP net income per share in the range of $1.73 to $1.79, assuming a non-GAAP effective tax rate of 17%.

- Comment: Fortinet reported strong performance in the first quarter, achieving a record operating margin of 28.5% and generating $830mn in cash flow from operations. It delivered US$1.35bn in revenue and earnings of US$0.43 per share surpassing analysts’ estimates. The growth in revenue was primarily due to a 24% increase in service revenue reaching US$944mn, however product revenue decreased 18.3% to US$408.9mn. Despite unified SASE and SecOps delivering strong billings growth, total billings saw a 6% YoY decline, due to the backlog contribution to billings in the year before. The company remains focused on investing in the unified SASE and secure operations market, which accounted for one-third of Q1 billings. The company also highlighted the success of its unified SASE solution and its differentiated features, such as deployment flexibility and comprehensive functionality. Its advanced platform approach, leveraging FortiOS and FortiASIC technologies, has been recognized with third-party awards. Additionally, Fortinet announced new AI-related offerings, including an IoT security generative AI assistant. Additionally, Fortinet expects Q2 revenue to be in the range of US$1.375bn to US$1.435bn and FY24 revenue to range between US$5.745bn and US$5.845bn, anticipating continued growth and profitability in the coming quarters. 2Q24 recommended trading range: $55 to $65. Neutral Outlook.

飞塔信息(FTNT)

- 24财年第一季营收:13.5亿美元,同比增幅7.1%,超预期1,000万美元

- 24财年第一季Non-GAAP每股盈利:0.43美元,超预期0.05美元

- 24财年第二季指引:预计营收在13.75亿美元至14.35亿美元之间,收入在14.9亿美元至15.5亿美元之间,Non-GAAP毛利率在76.50%至77.50%之间,Non-GAAP营业利润率在25.75%至26.75%之间,摊薄后Non-GAAP每股净收入在0.39美元至0.41美元之间,假设Non-GAAP有效税率为17%。假设摊薄后的股票数量为7.75亿至7.85亿股。

- 24财年指引:预计收入在57.45亿美元至58.45亿美元之间,服务收入在39.4亿美元至39.9亿美元之间,账单收入在64亿美元至66亿美元之间,Non-GAAP毛利率在76.50%至78.00%之间,Non-GAAP营业利润率在26.50%至28.00%之间,摊薄后Non-GAAP每股净收入在1.73美元至1.79美元之间,假设Non-GAAP有效税率为17%。

- 短评:飞塔在第一季度表现强劲,实现了创纪录的28.5%的营业利润率,并从运营中产生了8.3亿美元的现金流。营收13.5亿美元,每股收益0.43美元,超出分析师预期。收入的增长主要是由于服务收入增长24%,达到9.44亿美元,然而,产品收入下降18.3%,至4.089亿美元。尽管统一的SASE和SecOps带来了强劲的账单增长,但由于前一年的积压账单贡献,总账单同比下降了6%。该公司仍然专注于投资统一的SASE和安全运营市场,这占第一季度收入的三分之一。该公司还强调了其统一SASE解决方案的成功及其差异化特点,如部署灵活性和全面的功能。其先进的平台方法,利用FortiOS和FortiASIC技术,已获得第三方奖项的认可。此外,飞塔还宣布了新的人工智能相关产品,包括物联网安全生成人工智能助手。此外,飞塔预计第二季度收入将在13.75亿美元至14.35亿美元之间,24财年收入将在57.45亿美元至58.45亿美元之间,预计未来几个季度将继续增长和盈利。24财年第二季度建议交易区间:55美至65美元。中性前景。

Booking Holdings Inc (BKNG)

- 1Q24 Revenue: $4.42B, +16.9% YoY, beat estimates by $160M

- 1Q24 Non-GAAP EPS: $20.39, beat estimates by $6.25

- 2Q24 Guidance: Expect growth of 4% to 6% in room-night bookings, less than the 7.4% increase analysts were expecting. Gross travel bookings which include taxes and fees, should rise 3% to 5%, missing Wall Street’s estimates for 7.9% growth.

- Dividend: Board declared a cash dividend of US$8.75 per share payable on 28 June.

- Comment: Booking Holdings had a strong first quarter with revenue and earnings exceeding expectations. The majority of its total revenue, approximately 89% is from non-US travel with the Middle East, including Turkey and Egypt, making up about 7% of global room nights. However, the company cautioned that growth is likely to slow in the second quarter due to geopolitical tensions in the Middle East. Despite this, Booking Holdings reported healthy demand in Europe and better-than-expected room night bookings for the first quarter, growing 8.5% YoY to 297mn room nights sold surpassing expectations of a 6.2% YoY growth and 290.9mn room nights sold. Booking expects its second quarter to benefit from the shift in Easter timing, but it will be offset by less expansion of the booking window and an increased impact from the geopolitical situation in the Middle east, which would result int the deceleration in room night growth. For Q2, the company expects growth of 4% to 6% in room nigh bookings and 3% to 5% growth in gross travel bookings less than analysts’ expectations of 7.4% and 7.9% respectively. The company’s outlook is more cautious than analysts anticipated, but its overall performance remains positive. 2Q24 recommended trading range: $3,400 to $3,600. Neutral Outlook.

缤客 (BKNG)

- 24财年第一季营收:44.2亿美元,同比增幅16.9%,超预期1.6亿美元

- 24财年第一季Non-GAAP每股盈利:20.39美元,超预期6.25美元

- 24财年第二季指引:预计客房夜预订量将增长4%至6%,低于分析师预期的7.4%。包括税费在内的旅游预订量预计将增长3%至5%,低于华尔街7.9%的预期。

- 股息:董事会宣布于6月28日派发每股8.75美元的现金股息。

- 短评:缤客第一季度收入和收益都超出预期,表现强劲。其总收入的大部分(约89%)来自中东地区的非美国旅游,包括土耳其和埃及,占全球客房夜数的7%左右。然而,该公司警告说,由于中东的地缘政治紧张局势,第二季度的增长可能会放缓。尽管如此,缤客报告称,欧洲市场需求强劲,第一季度客房夜预订量好于预期,同比增长8.5%至2.97亿间房夜,超过了同比增长6.2%和2.990亿间房夜的预期。缤客预计其第二季度将受益于复活节时间的转变,但这将被预订窗口扩张的减少和中东地缘政治局势的影响所抵消,这将导致客房夜增长的减速。对于第二季度,该公司预计夜间客房预订量将增长4%至6%,总旅行预订量将增长3%至5%,低于分析师预期的7.4%和7.9%。该公司的前景比分析师预期的更为谨慎,但其整体表现仍然乐观。24财年第二季度建议交易区间:3,400美至3,600美元。中性前景。

Expedia Group Inc (EXPE)

- 1Q24 Revenue: $2.89B, +8.2% YoY, beat estimates by $80M

- 1Q24 Non-GAAP EPS: $0.26, not comparable to estimates of -$0.16

- FY24 Guidance: Lower full-year guidance to a range of mid- to high single-digit top-line growth, with margins relatively in line with FY23.

- Comment: Expedia beat analyst expectations for both profit and revenue in the first quarter, with strong hotel growth partially offset by the ongoing softness in its Vrbo business which is taking longer to recover. Its total gross bookings of US$30.2bn rose 3% YoY, less than expected, was driven primarily by total lodging gross bookings growth of 4% YoY and led by its hotel business growing 12% YoY. The company lowered its full-year guidance to a range of mid- to high single-digit top-line growth due to a slower-than-expected Vrbo recovery. While Expedia itself thrived from recent investments, technical migrations hurt Vrbo and Hotels.com. The new CEO will focus on boosting consumer business growth, improving conversion rates, and leveraging the new platform for better travel experiences. Despite the lowered guidance, Expedia feels optimistic about its long-term future under Ariane’s leadership. We anticipate that Expedia’s top and bottom lines will continue to be impacted by the Vrbo’s slow recovery and the rate of acceleration in B2C in the current quarter. 2Q24 recommended trading range: $110 to $135. Negative Outlook.

亿客行(EXPE)

- 24财年第一季营收:28.9亿美元,同比增幅8.2%,超预期8,000万美元

- 24财年第一季Non-GAAP每股盈利:0.26美元,去年同期每股亏损为0.16美元

- 24财年指引:将全年盈利预期下调至个位数中高增长区间,利润率与23财年相对持平。

- 短评:亿客行第一季度的利润和收入都超出了分析师的预期,酒店业务的强劲增长部分抵消了其Vrbo业务持续疲软的影响,该业务需要更长的时间才能恢复。其总预订量为302亿美元,同比增长3%,低于预期,主要受住宿总预订量同比增长4%和酒店业务同比增长12%的推动。由于Vrbo复苏速度慢于预期,该公司将全年收入增长预期下调至中位数至高个位数。虽然亿客行本身因最近的投资而蓬勃发展,但技术迁移却对Vrbo和Hotels.com造成了伤害。新任首席执行官将专注于促进消费者业务增长,提高转化率,并利用新平台提供更好的旅行体验。尽管下调了预期,但亿客行对其在Ariane领导下的长期前景感到乐观。我们预计,亿客行的营收和营收将继续受到Vrbo缓慢复苏和B2C业务加速增长的影响。24财年第二季度建议交易区间:110美至135美元。负面前景。