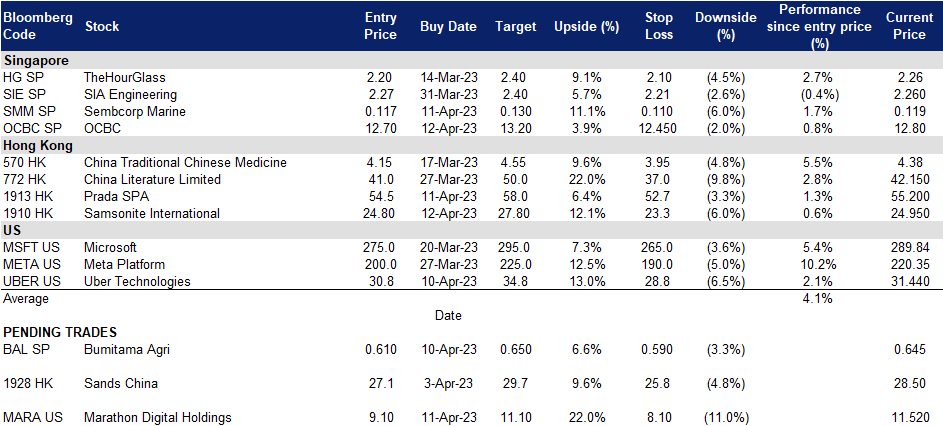

14 April 2023: Oversea-Chinese Banking Corp Ltd (OCBC SP), Samsonite International S.A. (1910 HK), Marathon Digital Holdings, Inc. (MARA US)

Singapore Trading Ideas | Hong Kong Trading Ideas |United States Trading Ideas | Sector Performance | Trading Dashboard

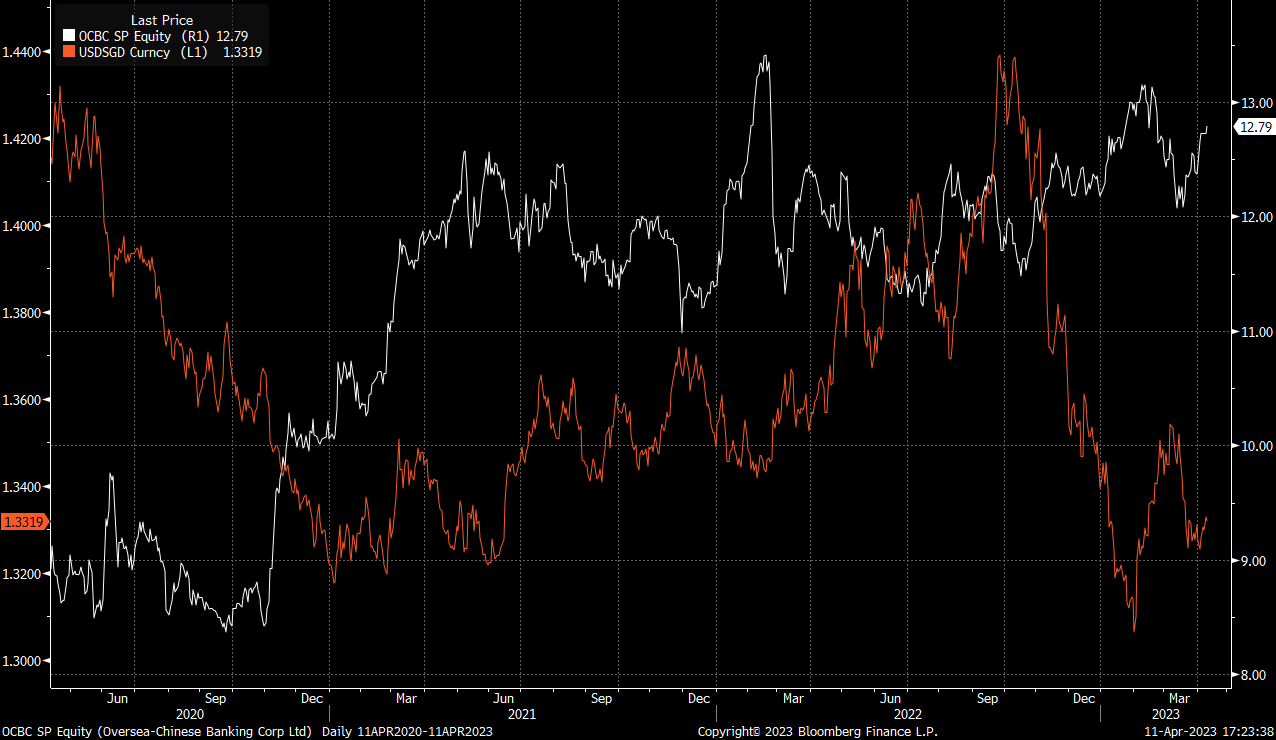

Oversea-Chinese Banking Corp Ltd (OCBC SP): Benefiting from weakening USD

- RE-ITEREATE BUY Entry 12.70 – Target – 13.20 Stop Loss – 12.45

- Oversea-Chinese Banking Corporation Limited offers a comprehensive range of financial services. The Company’s services include deposit-taking, corporate, enterprise and personal lending, international trade financing, investment banking, private banking, treasury, stockbroking, insurance, credit cards, cash management, asset management and other financial and related services.

- Stepping into a new dimension. OCBC is the first Singaporean bank to introduce a virtual banking experience for customers in the metaverse. Customers can access OCBC’s virtual branch in the blockchain-based decentraland platform, where they can open virtual savings accounts and interact with other customers in a virtual world. The virtual banking experience is part of OCBC’s efforts to reach out to the younger generation of customers and explore new channels for customer engagement.

- US CPI data release. With the US Core Consumer Price Index (CPI) data to be released on Wednesday and CPI expected to decline MoM, showing reduced inflation. This will further support the market expectations of rate cuts in the future, which will result in weakening US Dollars and provide support for Singapore bank stocks as both have an inverse correlation.

OCBC stock price vs USD/SGD price trend

(Source: Bloomberg)

- Benefit from rate cut expectations. Even though it is uncertain when rates will start to decline, Singapore banks will continue to thrive in this volatile environment as our local banking system is heavily regulated and conditioned under various stresses by the Monetary Authority of Singapore (MAS). MAS has also expressed its readiness to provide liquidity to maintain financial stability and orderly market functions. The overall market believes that the Feds will also attempt to decrease systemic risk in the financial sector by reducing interest-rate hikes and start to cut rates by 3Q23, with interest rates expected to peak at 4.75% to 5.00%. The expected decrease in interest rates could result in borrowers refinancing their loans, which were granted at higher rates.

- Growing wealth segment. Singapore is seeing an influx of wealthy individuals and family offices, which has led to a rise in assets under management at the country’s banks. The Monetary Authority of Singapore estimated there were about 700 family offices in 2021, but the current estimate is around 1,400, with mainland Chinese being the biggest drivers of growth. Although the family offices generate jobs indirectly through external finance, tax, and legal professionals, little of the money is being invested in funds or private equity firms. Despite this, the influx of wealth will still benefit banks in Singapore, particularly with the tax exemption programs for family offices, which have led to higher assets under management at banks in the country. Furthermore, with fear brewing due to the deteriorating US-China ties, the ultra-rich in Taiwan are considering setting up family offices in Singapore to protect their wealth. BDO Tax Advisory has reported an increase in inquiries from the ultra-rich in Taiwan. OCBC’s wealth management income contributed 33% to the Group’s total income in FY22. The group wealth management AUM was higher at S$258bn compared to S$257bn in FY21, driven by continued growth in net new money inflows which offset negative market valuation. As Singapore continues to attract a growing number of wealthy individuals, the country’s banks are expected to receive a boost in assets and deposits.

- FY22 results review. Group net profit for FY22 increased 18% to S$5.75bn, from S$4.86bn a year ago. Net interest income grew 31% to a record S$7.69bn from S$5.86bn in FY21.

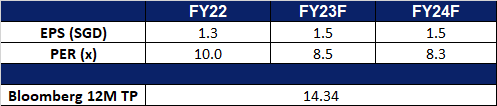

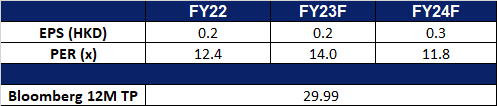

- Market consensus

(Source: Bloomberg)

Bumitama Agri Ltd (OCBC SP): Palm oil rebounding

- RE-ITEREATE BUY Entry 0.61 – Target – 0.65 Stop Loss – 0.59

- Bumitama Agri Ltd. produces CPO and PK, with its oil palm plantations located in Indonesia. The Company’s primary business activities are cultivating and harvesting our oil palm trees, processing FFB from its oil palm plantations, its plasma plantations and third parties into CPO and PK, and selling CPO and PK in Indonesia.

- Palm oil prices. Malaysian palm oil futures were trading below the MYR 3,900 per tonne mark, easing from an almost three-week peak of around MYR 4,000 as a stronger ringgit prompted investors to unwind some long positions. Palm oil prices remained supported by prospects of lower production and shrinking inventories. Heavy rains, floods, and older trees will likely constrain Malaysia’s output growth to less than 3% in 2023. Furthermore, inventories in Malaysia probably plunged the most in over two years in March, sinking below the two million-tonne level, as exports soared and production remained sluggish. With reported increased Malaysian shipments to India, China, European Union, and Africa. Malaysia has also been benefiting from Indonesia’s move to support domestic demand by curbing exports until the end of Ramadan and the Eid celebration.

Palm oil price trend

(Source: Bloomberg)

- Stabilization of palm oil. On 1 April, the Malaysian Palm Oil Board (MPOB) signed an MOU with the China Chamber of Commerce of Import and Export of Foodstuffs, Native Produce, and Animal By-products (CFNA) in Beijing to enhance trade and cooperation in the palm oil sector between both countries. The MOU includes promoting the supply chain stability of palm oil, promoting the exploration and implementation of new technologies, and facilitating China’s participation in oil palm mechanisation in Malaysia. China is Malaysia’s second-largest trading partner for palm oil and palm products, with exports valued at RM14.86 billion in 2022. The MOU aims to increase China’s confidence in Malaysian palm oil and secure its position in the Chinese market.

- FY22 results review. Revenue rose 29% YoY to IDR15,829bn from IDR12,249bn the prior year. Despite a decline in net profit for 2H22, FY22 net profit increased by 67% YoY to IDR3,003bn from IDR1,802bn in FY21. FY22 EBITDA was IDR5,686bn a 63% increase YoY from the previous IDR3,498bn.

- Market consensus

(Source: Bloomberg)

Samsonite International S.A. (1910 HK): Holiday season coming

- RE-ITEREATE BUY Entry – 24.8 Target – 27.8 Stop Loss – 23.3

- Samsonite International S.A. is a Hong Kong-based company principally engaged in the design, manufacture, sourcing and distribution of luggages, business and computer bags, outdoor and casual bags, travel accessories and slim protective cases for personal electronic devices. The Company operates its business through three segments. The Travel Bag segment is engaged in travel products with suitcases and carry-ons of three main categories, including hard-side, soft-side and hybrid luggages. The Casual Bags segment is engaged in daily use, including different types of backpacks, female and male shoulder bags and wheeled duffel bags. The Business Bags segment is engaged in business use, including rolling mobile office bags, briefcases and computer bags.

- Global tourism to continue to recover in 2023. According to the Economist Intelligence Unit Tourism in 2023 report, global tourism arrivals will increase by 30% YoY in 2023, following growth of 60% YoY in 2022, but will remain below pre-COVID levels. Based on UNWTO’s forward-looking scenarios for 2023, international tourist arrivals could reach 80% to 95% of pre-pandemic levels this year. UNWTO foresees the recovery to continue throughout 2023 even as the sector faces up to economic, health and geopolitical challenges. The recent lifting of COVID-19 related travel restrictions in China, the world’s largest outbound market in 2019, is a significant step for the recovery of the tourism sector in Asia and the Pacific and worldwide. In the short term, the resumption of travel from China is likely to benefit Asian destinations in particular.

- Campaign with New Balance. Recently, Samsonite introduced an all new “Live United” campaign with New Balance. This campaign seek to address the travel and lifestyle needs of today’s consumers. This collection features four bags that come in different sizes, in 2 colours, catering to the needs to different travel purposes.

- FY22 results review. FY22 sales improved to US$2,880 million (+57.4% YoY), driven by increased travel demand across most of the world. 2H22 sales growth of -0.8% YoY (+3.5% YoY excluding China) was largely recovered to 2019 levels. FY22 gross margins improved by 130 basis points to 55.8% from 2021, in-line with historical levels. The re-opening of borders in China would help further drive the travel and business recovery in 2023. Management highlighted that January and February 2023 are off to a very strong start with strong growth over 2019 levels across all regions.

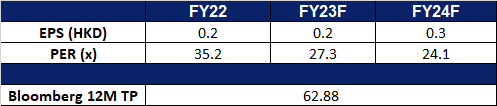

- Market consensus.

(Source: Bloomberg)

Prada SPA (1913 HK): Luxury never goes out of style

- RE-ITERATE BUY Entry – 54.5 Target – 58.0 Stop Loss – 52.7

- Prada SpA is an Italy-based company engaged in fashion industry. The Company is a parent of the Prada Group. The Company, along with its subsidiaries, is engaged in the design, production and distribution of leather goods, handbags, clothing, eyewear, fragrances, footwear and accessories. Prada SpA manufactures jackets, trousers, skirts, dresses, sweaters, blouses, as well as perfumes and watches, among others. The Company trades its products through several brands, such as Prada, Miu Miu, The Church and The Car Shoe. Prada SpA operates in approximately 70 countries through directly operated stores, franchise operated stores, a network of selected multi-brand stores and department stores. Prada Spa operates through a numerous subsidiaries, including Artisans Shoes Srl, Angelo Marchesi Srl, Prada Far East BV, Tannerie Megisserie Hervy SAS and Prada SA, among others.

- Strengthening Production. Prada Group recently announced that the company will recruit 400 people by the end of 2023 to strengthen its production capability and craftsmanship expertise in Italy. The strengthening of the company’s production would allow for greater agility and a reduction of time-to-market, bolstering its internal logistics process, which already includes quality checks on raw materials and finished goods.This builds on the Prada Group’s ongoing investment into its supply chain, a strategy that it first announced during its Capital Markets Day at the end of 2021.

- An enhanced marketing partnership. Prada Group announced recently that the company would be engaged in a partnership with Adobe to elevate customer experiences across all digital and physical retail properties. The partnership spans Prada Group’s range of brands, including Prada, Miu Miu, Church’s, Car Shoe, Pasticceria Marchesi, and Luna Rossa. The company will be able to combine vast amounts of existing data, create unified customer profiles, and deliver personalized experiences across any channel to its customers in real-time. Clients who have opted in will enable sales assistants to know when they visit a store and their preferences, with the goal of a richer personalized experience.

- Lyst index. Lyst, a reporting index that uses shopper data to rank popular fashion brands quarterly, has released its latest report for October to December 2022, marking its fifth year of customer insights. This unique index ranks fashion’s top brands and products by gathering shopping data from two hundred million customers globally. The determination of brand heat on the Lyst index chart goes beyond sales and views. It also includes social media mentions, activity, and engagement stats from around the world to determine which brands top the rankings. In Lyst’s latest report, Prada ranked at the top followed by Gucci and Moncler.

- FY22 earnings. Revenue in FY22 was €4.2 bn, up 21% YoY. Retail Sales rose 24% YoY to €3.7 bn.

- Market consensus.

(Source: Bloomberg)

Marathon Digital Holdings, Inc. (MARA US): BTC recovered above US$30,000

- RE-ITEREATE BUY Entry – 9.1 Target – 11.1 Stop Loss –8.1

- Marathon Digital Holdings, Inc. operates as a digital asset technology company that mines digital assets with a focus on the blockchain ecosystem and the generation of digital assets in United States.

- Bitcoin break-out. Bitcoin broke out of the US$30,000 level, a 10-month high, marking a gain of nearly 82% YTD. The jump was before the release of March inflation data which will be out on Wednesday, implying that investors are expecting a further decline in inflation in the US. And the expectation of the end of the rate hike cycle is reinforced.

Bitcoin and Ethererum

- Record Bitcoins were mined. The company announced that it mined 825 Bitcoins in March, up from 683 in February. Meanwhile, the company sold 750 Bitcoins in March, and it held 11,466 Bitcoins at the end of March.

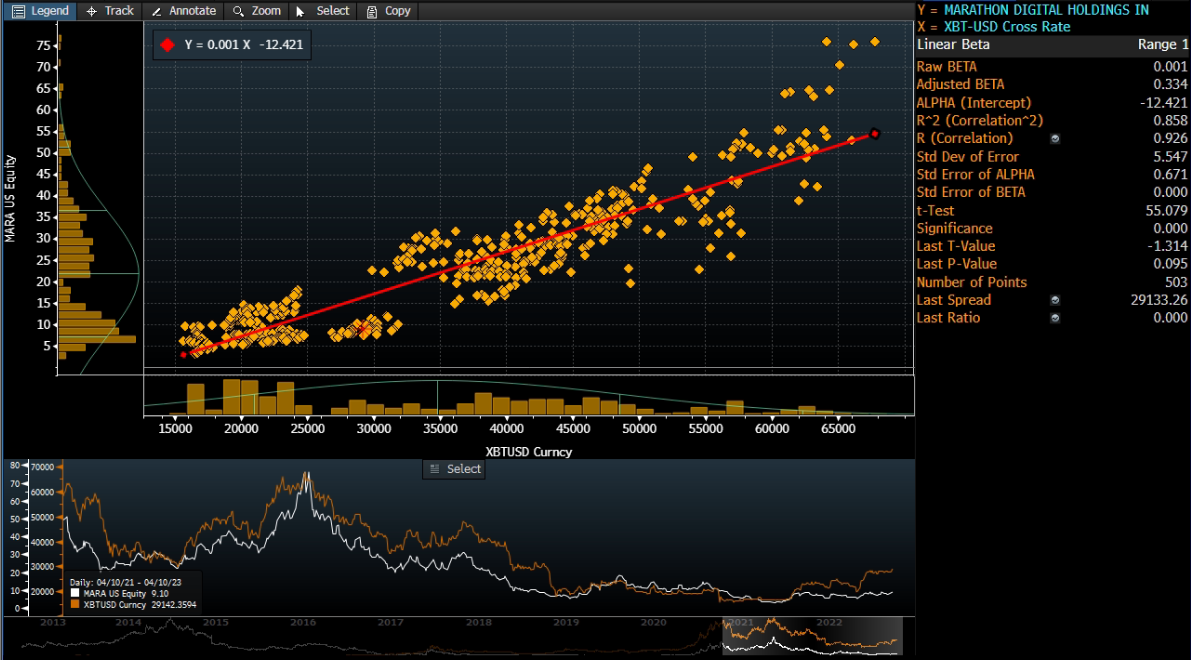

MARA and BTC price correlations

- 4Q22 earnings missed. 4Q22 revenue plunged by 58.4% YoY to US$28.42, missing estimates by US$6.2mn. 4Q22 GAAP losses per share was US$3.14, missing estimates by US$2.95.

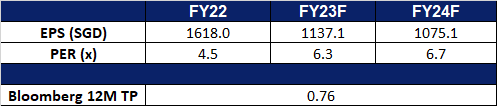

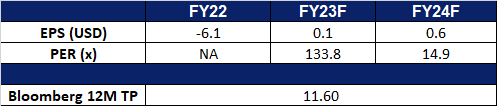

- Market Consensus

(Source: Bloomberg)

Uber Technologies, Inc. (UBER US): Year of turnaround

- RE-ITERATE BUY Entry – 30.8 Target – 34.8 Stop Loss –28.8

- Uber Technologies, Inc. develops and operates proprietary technology applications in the United States, Canada, Latin America, Europe, the Middle East, Africa, and Asia excluding China and Southeast Asia. It operates through three segments: Mobility, Delivery, and Freight.

- Mobility business expansion. The company recently announced that it would make electric and common bicycles on its app in Latin America together with the Brazilian bike-sharing company Tembici. By the end of 2023, Uber expects 30,000 bicycles to run in Latin America, one-third out of which is electric.

- Ongoing restructuring. Previously, Uber was reported to consider a spin-off of its Freight logistics arm. Listing the freight business is more likely instead of selling to peers. On the other hand, the company also planned to remove 5,000 virtual brands from its Uber Eats delivery. According to the main press, these virtual brands are delivery businesses that do not have physical locations, make up more than 8% of Uber Eats’ storefront in the US and Canada, but less than 2% of bookings.

- Ready for recession. The abovementioned actions show that the company is preparing for the upcoming recession. Both bicycle-sharing development and the potential spin-off can be viewed as a way to reserve capital, and the removal of virtual brands is to optimise operating costs.

- 4Q22 earnings beat estimates. 4Q22 revenue jumped by 48.8% YoY to US$8.6bn, beating estimates by US$90mn. 4Q22 GAAP EPS was US$0.45, beating estimates by US$0.29. Gross Bookings grew by 19%YoY and 26% YoY (constant currency basis). The company guided 1Q23 Gross Bookings to grow by 20%-24% YoY on a constant currency basis.

- Market Consensus

(Source: Bloomberg)

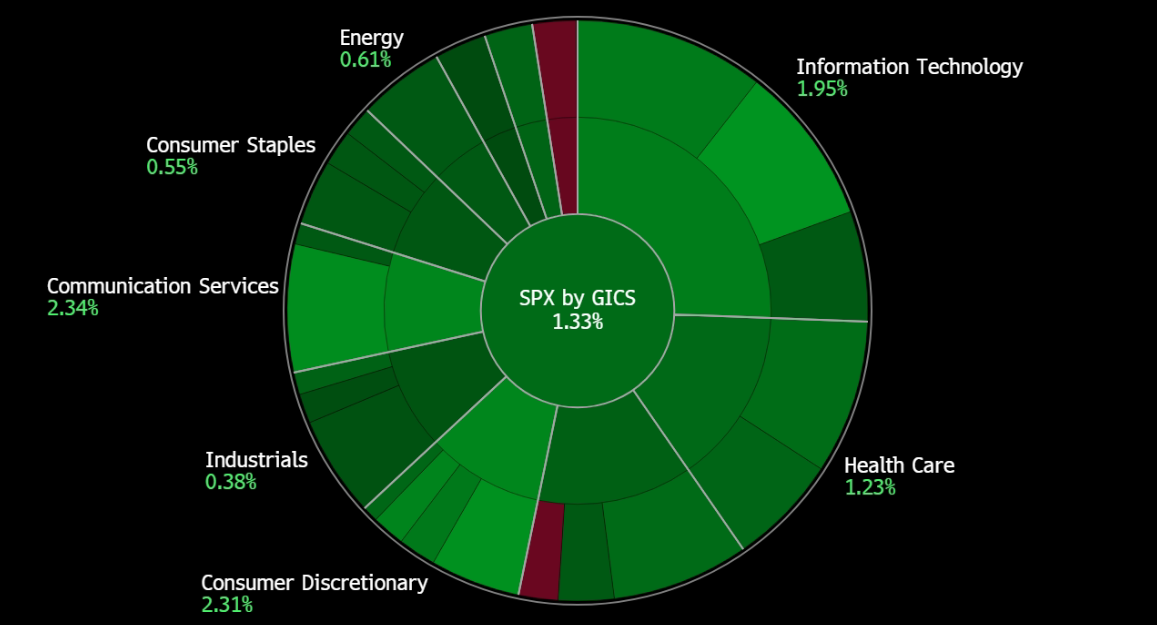

United States

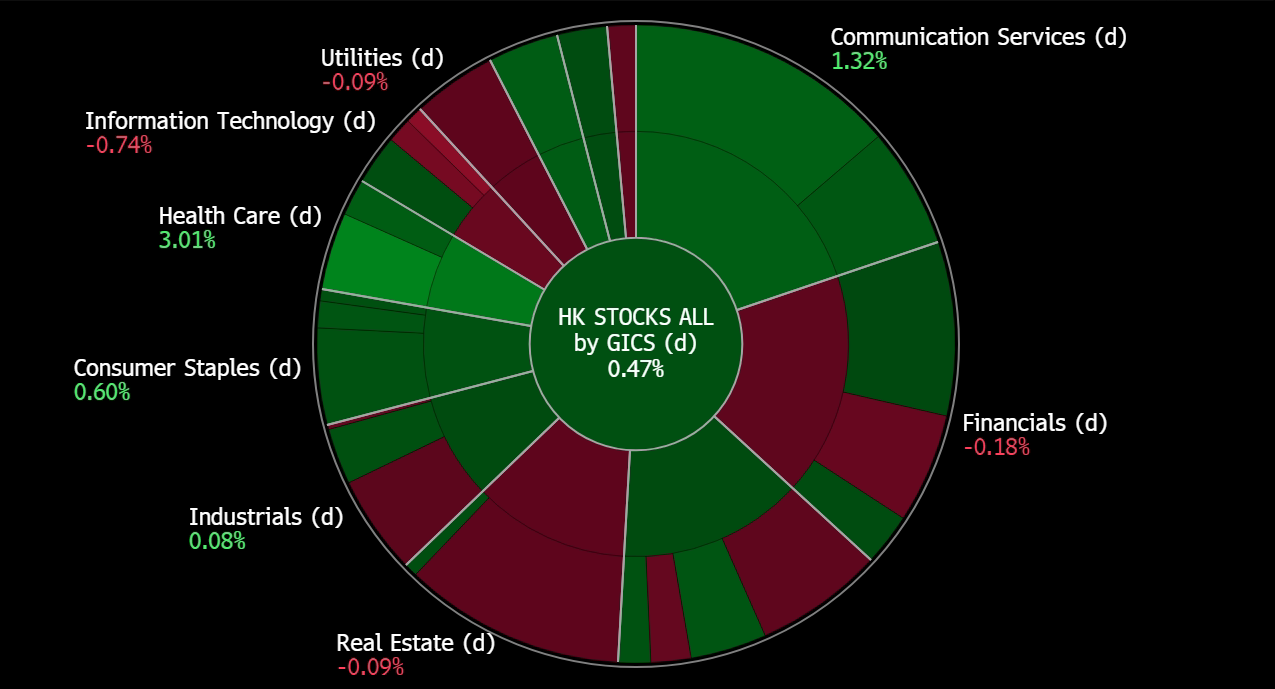

Hong Kong

Trading Dashboard Update: Add OCBC (OCBC SP) at S$12.70, Samsonite International (1910 HK) at HK$24.80. Take profit on Jiangxi Copper (358 HK) at HK$14.30, Agnico Eagle Mines (AEM US) at US$59.0.