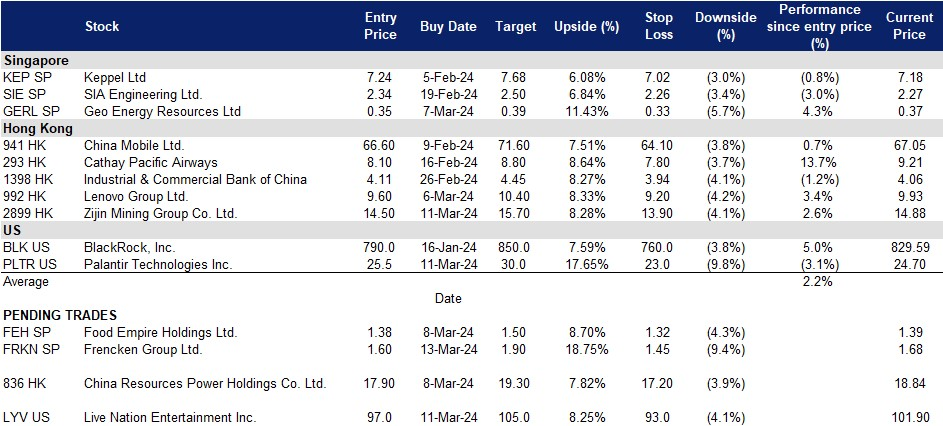

13 March 2024: Frencken Group Ltd. (FRKN SP), CZijin Mining Group Co. Ltd. (2899 HK), Live Nation Entertainment Inc (LYV US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

Frencken Group Ltd. (FRKN SP): Following the semiconductor recovery

- Entry – 1.60 Target– 1.90 Stop Loss – 1.45

- Frencken Group Limited (“Frencken”) is a Global Integrated Technology Solutions Company that is listed on the Main Board of the Singapore Exchange. They provide comprehensive Original Design, Original Equipment and Diversified Integrated Manufacturing solutions for world-class multinational companies in the analytical & life sciences, automotive, healthcare, industrial and semiconductor industries.

- Strong AI chip demand signal from the world’s largest semiconductor producer. Taiwan Semiconductor Manufacturing’s strong demand for high-end chips used in artificial intelligence (AI) has propelled the semiconductor index up, contributing to broader market gains. The positive outlook for AI demand in 2024 has driven optimism, with experts foreseeing substantial revenue growth for semiconductor companies, indicating the early stages of a technological revolution. Nvidia, a key player in AI computing, also experienced share gains, reaching a fresh record peak. We anticipate that this positive momentum will translate into revenue generated by Frencken’s semiconductor segment, which accounted for about 40% of its Q3 revenue.

- Continued demand for AI Chips. Applied Materials, Frencken’s main customer, announced an earnings beat for FY23 and expects continued outperformance as customers ramp up next-generation chip technologies critical to AI and the Internet of Things. Their key customer, Taiwan Semiconductor Manufacturing Co., also highlighted that revenue rose 9.4% in 2024’s first two months, riding a wave of global AI development. These strong demands for AI chips would translate to more revenue growth for Frencken.

- Anticipated decline in interest rates. Fed Chair Jerome Powell recently mentioned that inflation is “not far” from where it needs to be for the central bank to start cutting interest rates, but did not provide a specific timeline. The market expects a rate cut to occur in June’s FOMC meeting, with a market’s implied probability of 25bps in June at 56.7%. The expected rate decline throughout the year could contribute to increased valuations in the semiconductor sector.

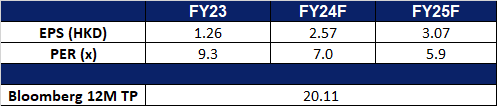

- FY23 results review. FY23 revenue declined by 5.5% to $742.9mn, compared to $786.1mn in FY22. Net profit plunged 38.1% YoY to $32.0mn due to challenging business conditions for the technology sector, compared to $51.6mn in FY22. Gross profit margin contracted to 13.2% in FY23 from 15.1% in FY22, attributing it to lower revenue, inflationary cost pressures as well as increased depreciation expenses.

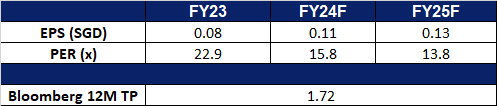

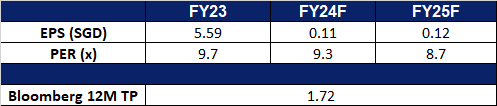

- Market Consensus

(Source: Bloomberg)

Food Empire Holdings Ltd. (FEH SP): Soaring to new heights

Food Empire Holdings Ltd. (FEH SP): Soaring to new heights

- RE-ITERATE Entry – 1.38 Target– 1.50 Stop Loss – 1.32

- Food Empire Holdings (Food Empire) is a multinational food and beverage manufacturing and distribution group headquartered in Singapore. Food Empire’s products are sold in over 60 countries, spanning North Asia, Eastern Europe, South-East Asia, Central Asia, the Middle East, and North America. The Group has 23 offices worldwide and operates 8 manufacturing facilities located in 5 countries.

- Strong consumer demand. Consumer demand stays resilient across Food Empire Holdings’ key markets despite ongoing geopolitical tensions worldwide, alongside a high-interest rate environment. Demand for coffee and tea remained strong across company’s all key markets, seeing volume growth YoY, as well as an increase in sales YoY in local currencies. The expectation that interest rates have peaked and potential rate cuts on the horizon due to cooling inflation will likely enhance consumer sentiment, fuelling the demand for consumer goods. We expect to see further growth in FY24.

- Optimising product mix. The company still remains focused on optimising its product mix and reducing costs in 4Q23. For the full year, the company’s gross profit margin (GPM) rose to 33.2% in FY23, compared to 29.8% in FY22.

- Malaysia’s NDC plant to commence operation soon. The group has finalized its non-dairy creamer expansion in Malaysia, anticipating the commencement of commercial production in the next few months, pending final approval from the Malaysian government. This expansion aims to boost non-dairy creamer sales to external parties in the region. Marketing efforts have already commenced to identify potential customers, and the group foresees the plant reaching 30% to 40% capacity by year-end.

- FY23 financial results. The company reported a record revenue of US$425.7mn for FY23, up 6.9% YoY, due mainly to higher volume and higher pricing from all the group’s core markets. The company saw a significant increase in revenue in Ukraine, Kazakhstan, and CIS, and South Asia, attributed to higher contributions from the group’s coffee manufacturing plants in these markets. Gross profit also rose by 19.0% to US$141.5mn YoY, compared to US$118.8 in FY22. Net profit increased 25.3% YoY to US$56.5mn in FY23 compared to US$45.1mn in FY22, excluding a one-off gain of US$15.0 million from the disposal of non-core assets in FY22.

- Special dividend. The company declares a final FY23 dividend of 5 Scents per share and a surprise special dividend of 5 Scents per share, indicating a forward yield of 7.14%.

- We have fundamental coverage with a BUY recommendation and a TP of S$1.65. Please read the full report here.

(Source: Bloomberg)

Zijin Mining Group Co. Ltd. (2899 HK): Gold hits an all-time high

- BUY Entry – 14.50 Target – 15.70 Stop Loss – 13.90

- Zijin Mining Group Company Limited is a China-based company in mineral business. The Company operates nine segments. The Gold Bullion segment mainly produces gold ingots for the production links of other divisions. The Processed, Refined and Trading Gold segment is engaged in the processing of purchased gold ingots and trading gold ingots. The Gold concentrate section processes gold bearing ores and generates gold concentrates. The Electrolytic Copper segment is produced by electrolytic copper and electrowinning copper. The Refined Copper segment is engaged in the processing of self-produced copper and purchased copper. The Copper concentrates segment processes copper ore and produce copper concentrate. The Other Concentrate segment is responsible for producing zinc concentrate, tungsten concentrate and lead concentrate. The Zinc Bullion segment produces zinc ingots. Others segment is mainly engaged in the sales of sulfuric acid, copper strip, silver and iron.

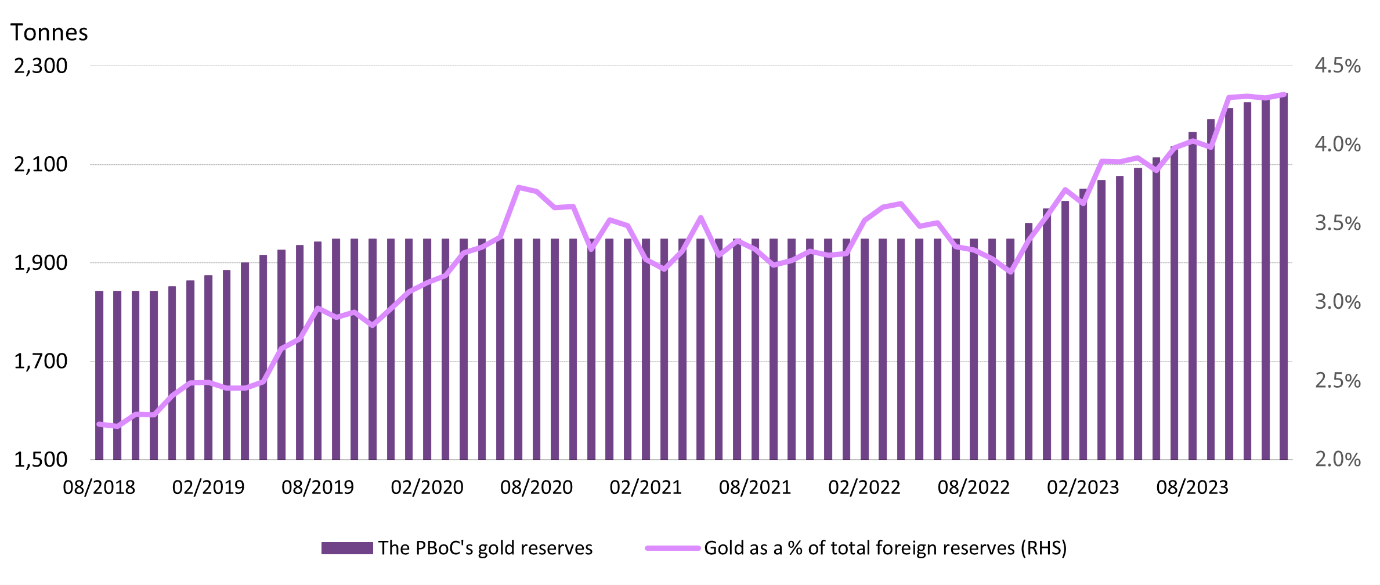

- China increasing its gold reserves. China recently extended its continuous gold purchase record after the central bank bought another 12 tonnes of precious metal in February. This brings China’s gold reserves now a total of 2,257 tonnes, according to the World Gold Council. These purchases increase the country’s already sizable holdings as part of a strategy to reduce its reliance on the US dollar. Gold now makes up 4.33% of China’s foreign exchange reserves in US dollars, the highest level ever recorded. The central bank’s gold buying spree, combined with weak performances of Chinese assets such as equities and properties, has sparked retail investors’ interest in gold. It also contributed to a surge in local gold investment demand during 2023 and could continue to support the sector’s growth.

PBOC Gold Reserves

(Source: PBoC, World Gold Council)

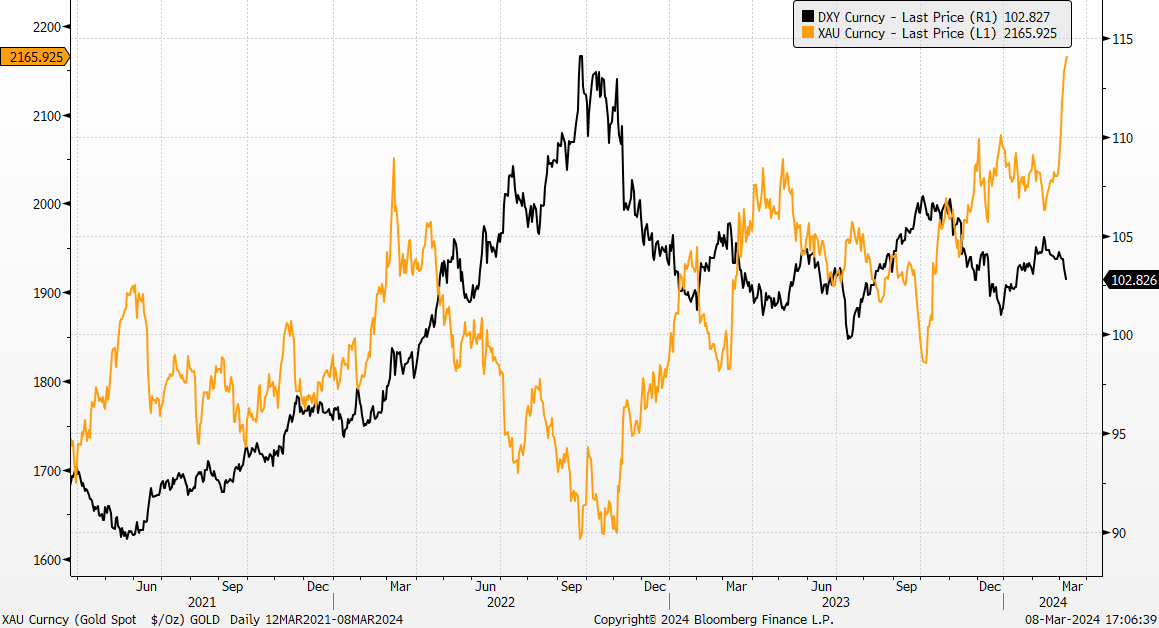

- Interest rate cuts in sight. Fed Chair Jerome Powell mentioned recently that inflation is “not far” from where it needs to be for the central bank to start cutting interest rates. The market currently expects a rate cut to happen in June’s FOMC meeting. With interest rate cuts in sight, the price of gold may see more positives, given that inflation continues to show signs of slowing down towards moving sustainably at 2%.

Gold Price and Dollar Index Trend

(Source: Bloomberg)

- Expansion of copper mine. Zijin Mining Group recently received the green light to proceed with the second-phase expansion of the Julong copper project situated in Tibet. This adds a new production scale of 200,000 tonnes/day through upgrade and expansion, thus forming a total production scale of 350,000 tonnes/day. Annual output will exceed 100 million tons, making it the largest single copper mine in China. The expansion will require an investment of around 17.5 billion yuan ($2.43 billion) and enter operation in 2025.

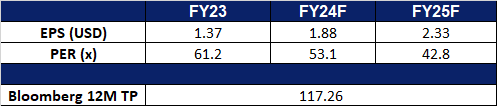

- 3Q23 earnings. Operating income rose 10.19% YoY to RMB225.0bn in 3Q23, compared with RMB204.2bn in 3Q22. Net profit fell 2.98% to RMB20.1bn in 3Q23, compared to RMB20.7bn in 3Q22. Basic earnings per share was RMB0.615 in 3Q23, compared to RMB0.635 in 3Q22.

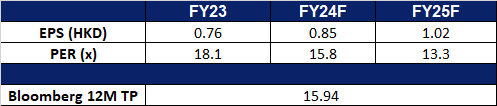

- Market consensus.

(Source: Bloomberg)

China Resources Power Holdings Co. Ltd. (836 HK): Increase coal use

- RE-ITERATE BUY Entry – 17.90 Target – 19.30 Stop Loss – 17.20

- China Resources Power Holdings Company Limited is a Hong Kong-based investment holding company principally engaged in the investment, development and operation of power plants. The Company operates through three segments. Thermal Power segment is engaged in the investment, development, operation and management of coal-fired power plants and gas-fired power plants, as well as the sales of heat and electricity. Renewable Energy segment is engaged in wind power generation, hydroelectric power generation and photovoltaic power generation, as well as the sales of electricity. Coal Mining segment is engaged in the mining of coal mines, as well as the sales of coal. The Company mainly operates businesses in China.

- Cold wave. China’s national observatory recently renewed an orange alert, the second-highest in the country’s four-tier weather warning system, for cold waves in various areas, forecasting plunging temperatures. The cold wave is set to bring a significant temperature decline to central and eastern China, progressing towards the east and south. In late February, northern China witnessed strong winds, widespread sandstorms, dramatic temperature drops, and rainy and snowy conditions. Temperatures in the north plummeted, with certain areas experiencing declines exceeding 20 degrees Celsius. Over the period, central and eastern China saw more widespread rainy, snowy, and freezing weather, coupled with noticeable temperature fluctuations. The cold wave is expected to drive increased electricity consumption as individuals opt to stay home, seeking warmth amid the freezing conditions across the period.

- Long-Term green power purchase agreement with Merck. China Resources Power has revealed its intention to engage in a long-term power purchase agreement with Merck. Under this agreement, Merck China will substantially enhance its utilization of green electricity in production and operations, aiming to achieve a 60% usage and reduce Scope 2 carbon emissions by 185,000 tonnes. This initiative aligns with Merck’s broader objective of raising its global procurement of electricity from renewable sources to 80% by 2030 and achieving climate neutrality by 2040. The ten-year power purchase agreement with Merck guarantees the life-cycle traceability of a total of 300 GWh of green power.

- Coal Prices. The decline in global coal prices is expected to have significant benefits for the company’s coal-fired power plants and gas-fired power plants. With prices at a 2-year low around of $130 per tonne, lower fuel costs for coal-fired power plants translate into improved profitability and a competitive advantage in the market. While China Resources Powers does have its own coal production plants, energy consumption during the current winter period typically skyrockets for China, this means that the company will be required to buy coal from other suppliers to further supplement its energy production and will therefore benefit from the lower prices. The declining prices also create opportunities for the company’s gas-fired power plants, as natural gas becomes a more cost-effective alternative. This diversification and cost advantage contribute to improved financial performance, market competitiveness, and the ability to offer competitive electricity prices to consumers. Overall, the decline in coal prices presents favourable conditions for the company’s power generation operations, enhancing profitability and sustainability.

Thermal Coal Price

(Source: Bloomberg)

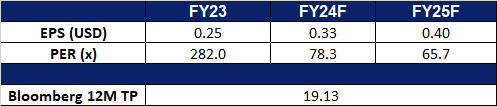

- 1H23 earnings. Revenue rose 2.13% YoY to HK$51.5bn in 1H23, compared with HK$50.4bn in 1H22. Net profit rose 61.8% to HK$7,08bn in 1H23, compared to HK$4.37bn in 1H22. Basic earnings per share was HK$1.40 in 1H23, compared to HK$0.91 in 1H22.

- Market consensus.

(Source: Bloomberg)

Live Nation Entertainment Inc (LYV US): Benefit from concert economics

- BUY Entry – 97 Target – 105 Stop Loss –93

- Live Nation Entertainment, Inc. produces live concerts and sells tickets to those events over the Internet. The Company offers ticketing services for leading arenas, stadiums, professional sports franchises and leagues, college sports teams, performing arts venues, museums and theaters. Live Nation Entertainment serves customers worldwide.

- 2023 biggest year for concerts. Live Nation had a remarkable year in 2023, surpassing previous records with revenue reaching US$22.7bn, a 36% YoY increase, driven by record attendance, ticket sales, and sponsorships. Concert attendance rose by 20.3% to 145.8mn, with significant gains in both North America and internationally. The company’s acquisition of Mexican promoter OCESA and the rise of K-pop and Latin music contributed to the international expansion of its concert business, with 50% more international acts featured in its top 50 tours compared to five years ago. Revenue from Live Nation’s owned and operated venues, Ticketmaster, and sponsorship and advertising divisions all saw substantial growth, reflecting the robustness of its business model. Looking ahead, Live Nation expects continued growth and profitability across its businesses, with strong ticket sales and sponsorship commitments already secured for 2024.

- Continued momentum through 2024. In 2023, Taylor Swift’s eras tour, promoted and organised by Live Nation, smashed records, grossing over US$1bn. This unprecedented success has fuelled a surge in concert attendance, with artists like LANY and Conan Grey following suit under Live Nation’s banner. This trend extends to established superstars as well, with Live Nation promoting tours for FY24 from Bad Bunny (Latin Trap, Reggaeton), Billie Eilish (Pop), Drake (Hip Hop), Harry Styles (Pop), and The Weeknd (Pop, R&B). Further solidifying the live music industry’s strength, JYP Entertainment, home to popular K-Pop groups like TWICE, Stray Kids, and ITZY, announced a multi-year strategic partnership with Live Nation. This collaboration aims to expand the global reach of these K-Pop acts by leveraging Live Nation’s extensive network and experience in promoting large-scale tours worldwide. This strong showing across genres indicates that the momentum for continued ticketed concerts and festivals has continued through to FY24, showing that consumers are willing to spend on such activities.

- Recent controversy. Live Nation has pushed back against accusations that its dominance in the live music industry, along with its Ticketmaster division, contributes to high ticket prices. In a blog post, Live Nation’s EVP Corporate and Regulatory Affairs, Dan Wall, argues that promoters and ticketing companies do not determine ticket prices; instead, artists and venues play a more significant role. Wall contends that service charges added to ticket prices cover costs for venues and ticketing companies and are not “junk fees.” He emphasizes that artists ultimately decide ticket prices, and venues determine service fees. Wall also suggests that economic factors, such as concerts becoming premier “experience goods” and artists’ increasing dependence on touring income due to declining recorded music sales, contribute to rising ticket prices. Despite Live Nation’s ownership of Ticketmaster, Wall asserts that secondary ticketing platforms, not Live Nation’s core business, are responsible for inflated resale prices. Overall, Live Nation aims to steer the political debate around ticketing toward issues that have minimal impact on its operations.

- 4Q23 earnings review. Revenue rose by 36.1% YoY to US$5.84bn, beating estimates by US$1.06bn. EPS was US$1.37, not comparable with estimates of -US$0.94. In FY24 growth is expected to be more weighted toward 2Q and 3Q compared to previous years, and capital expenditure is estimated to be US$540mn, in line with previous years as a percentage of revenue.

- Market consensus.

(Source: Bloomberg)

Palantir Technologies Inc (PLTR US): Backed by private and public sectors

- RE-ITERATE BUY Entry – 25.5 Target – 30.0 Stop Loss – 23.0

- Palantir Technologies Inc. develops software to analyze information. The Company offers solutions support many kinds of data including structured, unstructured, relational, temporal, and geospatial. Palantir Technologies serves customers worldwide.

- Unveiled new customers at AIPCon. On 7 March, Palantir Technologies Inc. held AIPCon, which was accessible via livestreamed on YouTube, with over 60 customers who presented their work on Palantir’s Artificial Intelligence Platform (AIP) and introduced over 20 new customers and partners. Since the launch of AIP in mid-2023, nearly 850 AIP Bootcamps have been conducted globally, helping customers implement use cases swiftly. Its new customers and partners such as Lennar, General Mills, Lowe’s, Cone Health, CSX, OpenAI and many others led the AIP Bootcamps and shared their experiences at the event.

- Secured new contracts with US Army. On 6 March, Palantir Technologies Inc. announced that it had been awarded a US$178.4mn prime agreement by the Army Contracting Command – Aberdeen Proving Ground (ACC-APG) to develop and deliver the Tactical Intelligence Targeting Access Node (TITAN) ground station system. TITAN, the Army’s next-generation deep-sensing capability enabled by artificial intelligence and machine learning, aims to provide actionable targeting information for mission command and long-range precision fires. The system, designed to enhance the automation of target recognition and geolocation, will integrate systems and technologies from various partners including Northrop Grumman, Anduril Industries, and L3Harris Technologies. Palantir, as the prime contractor, will deliver both software and hardware components, leveraging innovative solutions to meet the Army’s modernization priorities. The award, facilitated through an Other Transaction Authority (OTA) agreement, underscores the changes AI is bringing about across various industries including the military.

- 4Q23 earnings review. Revenue rose by 19.6% YoY to US$608.35mn, beating estimates by US$5.55mn. Non-GAAP EPS was US$0.08, in-line with estimates. In 1Q24 it expects revenue to be between US$612mn- US$616mn and FY24 revenue to be between US$2.652bn- US$2.668bn.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Take profit on BYD Co. Ltd. (1211 HK) at HK$208. Add Zijin Mining Group Co. Ltd. (2899 HK) at HK$14.5 and Palantir Technologies Inc (PLTR US) at US$25.5. Cut loss on Frencken Group Ltd (FRKN SP) at S$1.66 and PVH Corp (PVH US) at US$130.5.