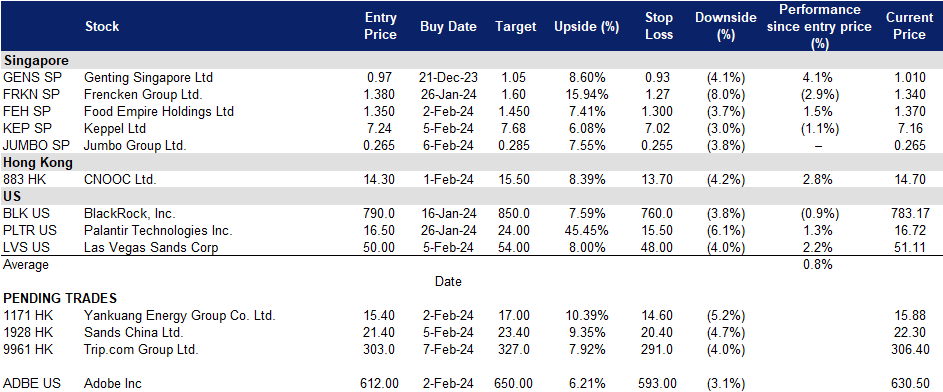

7 February 2024: Keppel Ltd (KEP SP), Trip.com Group Ltd. (9961 HK), Palantir Technologies Inc (PLTR US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

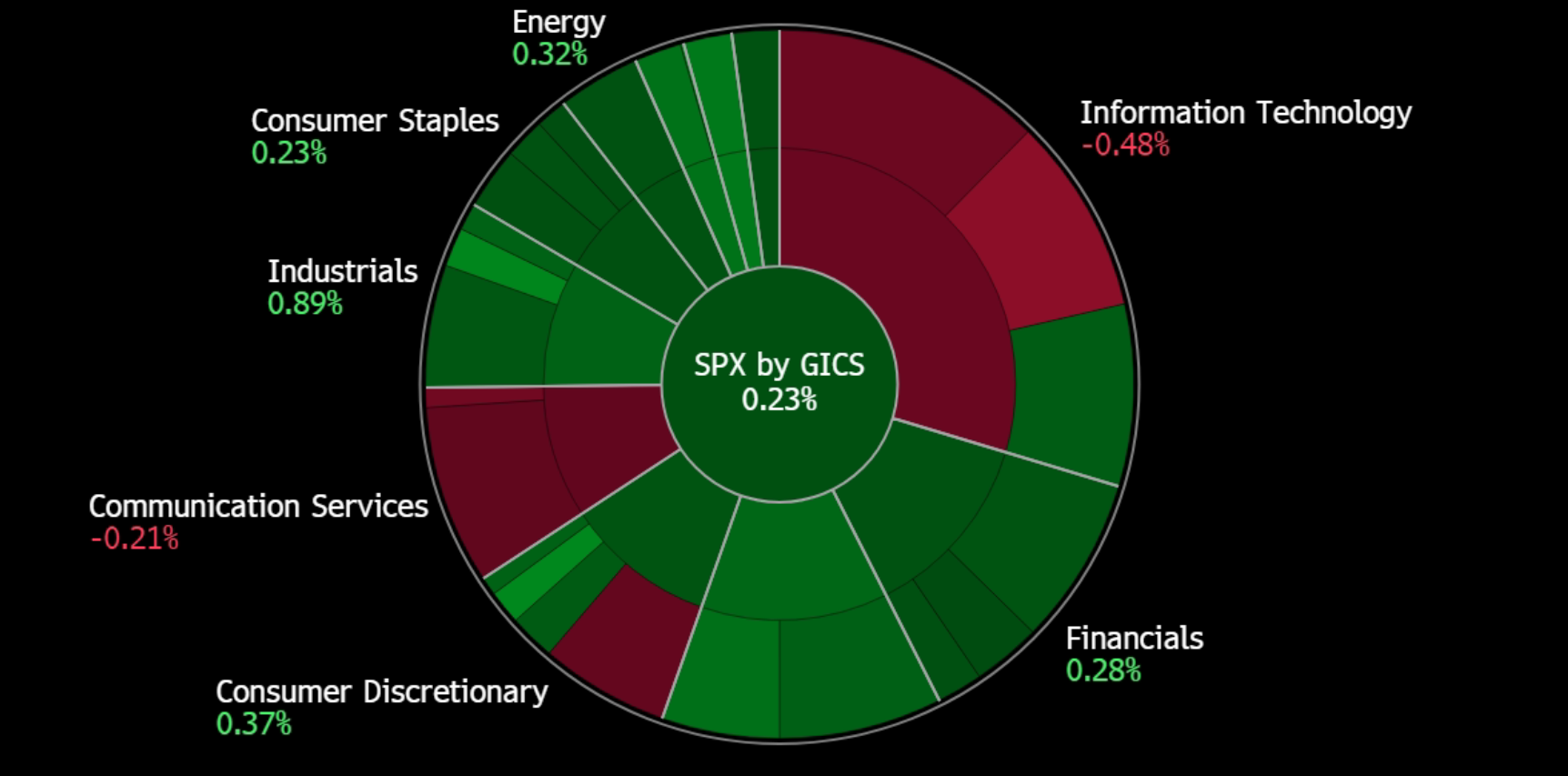

United States

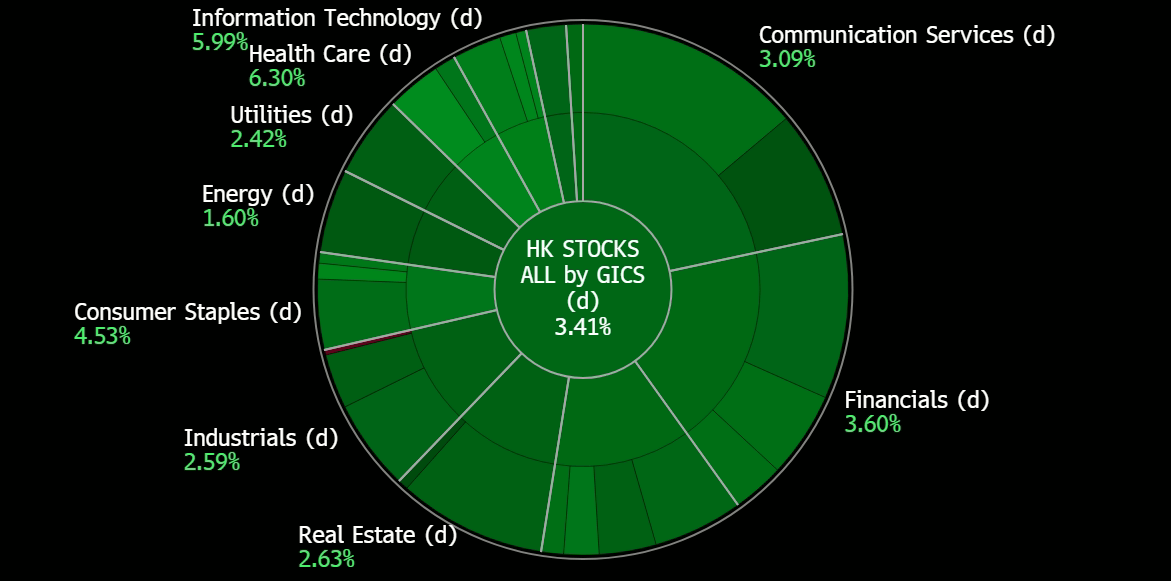

Hong Kong

News Feed |

3. Xi set to discuss China stock market with financial regulators |

4. Warnings, liquidity boost and proverbs — China’s tools for propping up its stock market |

Keppel Ltd (KEP SP): Continue to growth in 2024

- RE-ITEREATE BUY Entry – 7.24 Target– 7.68 Stop Loss – 7.02

- Keppel Limited is an asset manager and operator. The Company focuses on sustainability solutions spanning the areas of energy and environment, urban development, and digital connectivity, as well as provides critical infrastructure and services through its investment platforms and asset portfolios. Keppel serves clients worldwide.

- Profitability on the rise. Keppel reported a record net profit of S$4.1bn for FY23, marking a more than 4 times increase from the previous year’s profit of S$927mn. The surge was attributed to gains from the divestment of Keppel Offshore & Marine, contributing S$3.3bn, and S$996mn from continuing operations. Return on equity rose to 37.9%, compared to 8.1% in FY22. 2H23 increased by 36% to S$551mn. Its three business segments of infrastructure, real estate, and connectivity performed well. Keppel plans to become a global asset manager and operator, delivering a total shareholder return of 61.1% for 2023. Infrastructure net profit rose by 135% to S$699mn. The proposed final cash dividend is 19 cents per share, bringing the total cash dividend for FY23 to 34 cents per share. Keppel’s CEO highlighted the transformative year, including the successful divestment of the offshore and marine business and the acquisition of a 50% stake in European asset manager Aermont Capital for S$517mn. The company aims to grow its funds under management to $200bn by 2030, leveraging Aermont’s expertise in real estate. Despite challenging conditions in certain markets, Keppel’s real estate segment contributed S$426mn to the net profit for FY23. Looking ahead, Keppel anticipates recurring income growth and expansion in fund management and deal-making volume in 2024.

- S$1bn of sustainability-linked loans. Keppel recently introduced a sustainability-linked financing framework and secured S$1bn in sustainability-linked revolving loans from DBS Bank and United Overseas Bank. The framework outlines key performance indicators and sustainability targets, including a 50% reduction in Keppel’s absolute scope 1 and 2 carbon emissions by 2030 compared to the 2020 baseline. The company also aims to increase its portfolio of renewable energy assets to 7GW by 2030, with an interim target of 4.9GW by the end of 2027. Keppel secured S$500mn in sustainability-linked revolving credit facilities from each bank, with tenures of up to three years.

- Power supply deal with large chipmaker. Keppel’s infrastructure business recently secured a multi-year agreement to supply electricity to contract chipmaker GlobalFoundries’ Singapore operations. The chipmaker operates a US$4bn semiconductor fabrication plant in Singapore serving 200 clients globally in the automotive and 5G technology sectors. Starting May, Keppel’s existing power plants will provide 150 to 180 megawatts of electricity annually to GlobalFoundries’ site. GlobalFoundries is expected to be a long-term buyer from Keppel Sakra Cogen Plant (KSC), which is being developed in collaboration with Mitsubishi Power and Jurong Engineering. GlobalFoundries is anticipated to contract about 25% of KSC’s total generation capacity for over 15 years. KSC, set to be completed in 2026 with a total annual capacity of about 600MW, aims to reduce up to 70,000 metric tons or 10% of annual carbon dioxide emissions at GlobalFoundries’ Singapore site. The plant’s use of hydrogen as feedstock enhances its potential to provide even lower-carbon power in the future. GlobalFoundries has the option to switch part of the power supplied by Keppel to renewable energy sources as part of its goal to achieve a 25% reduction in total greenhouse gas emissions by 2030.

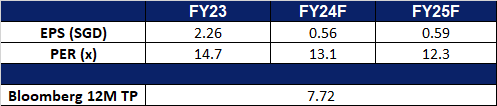

- FY23 results review. FY23 revenue increased by 5% YoY to S$6,967mn from S$6,620mn. Net profit rose 339% YoY to S$4,067mn from S$927mn. Earnings per share rose 337% to 227.6 cents from 52.1 cents in FY22.

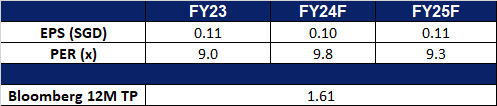

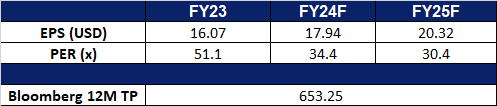

- Market Consensus.

(Source: Bloomberg)

Food Empire Holdings Ltd (FEH SP): A growing empire

Food Empire Holdings Ltd (FEH SP): A growing empire

- RE-ITEREATE BUY Entry – 1.35 Target– 1.45 Stop Loss – 1.30

- Food Empire Holdings Limited manufactures and markets instant beverage products, frozen convenience food, confectionery and snack food. The Company exports its products to markets such as Russia, Eastern Europe, Central Asia, the Middle East and Indochina.

- Expansion Plans. Food Empire is constantly seek opportunities to spearhead itself in a different market, mainly focusing on acquisitions. The company is currently exploring several new markets where they can grow its business, before diving into expanding its business into these new markets to prevent incurring additional losses. The company also recently proposed a dual primary listing on the main board of the stock exchange of Hong Kong Ltd. This can potentially help Food Empire to generate more capital to grow their business internationally.

- Resilient consumer demand. Consumer demand remained relatively steady despite ongoing geopolitical tensions worldwide, in a high-interest-rate environment. Demand for coffee remained strong across the company’s key markets. However, Russia saw a slight decline in revenue mainly due to the depreciation of the Russian Ruble against the US dollar.

- Completion of Malaysia’s NDC plant. The company expects its NDC plant in Malaysia to commence operation in 1Q24, pending approval and clearance from the Malaysian government. The new plant is expected to begin commercial production in the coming months but would still require more time to ramp up to full capacity. This plant would increase the production capacity for the group to generate more revenue.

- 3Q23 results review. 3Q23 revenue decreased by 1.6% YoY to US$106.8mn from US$108.6mn. Net profit fell 30.6% YoY to US$15.7mn from US$22.6mn. Net profit margin fell by 6.1 percentage points to 14.7% in 3Q23, compared with 20.8% in 3Q22.

- Market Consensus. We have a fundamental coverage with a BUY recommendation and a TP of S$1.45. Please read the full report here.

(Source: Bloomberg)

Trip.com Group Ltd. (9961 HK): Tailwinds of seasonality

- BUY Entry – 303 Target – 327 Stop Loss – 291

- Trip.com Group Ltd is a China-based company mainly engaged in the operation of one-stop travel platform. The Company’s platform integrates a comprehensive suite of travel products and services and differentiated travel content. Its platform aggregates its product and service offerings, reviews and other content shared by its users based on their real travel experiences, and original content from its ecosystem partners to enable leisure and business travelers to have access to travel experiences and make informed and cost-effective bookings. Users come to its platform for any type of trip, from in-destination activities, weekend getaways, and short-haul trips, to cross-border vacations and business trips.

- Livestream collaboration and upcoming visa free travel. Trip.com recently collaboration with the Tourism Authority of Thailand (TAT) and Thailand’s Ministry of Tourism & Sports, hosting a livestream session that showcased the different charms of Thailand. Through the livestream, a wide range of deals were sold, with the transaction grossing over THB100mn in total. This showcased the popularity of Thailand as a tourist destination amongst the Chinese. With China and Thailand waiving visa requirements permanently from March, Trip.com would be able to benefit from the expectations of the increase in travel bookings in 2024 in these 2 countries.

- Trip.vision application. Trip.com just unveiled its Trip.vision application, which is designed to leverage the advanced capabilities of Apple’s latest mixed-reality headset, the Apple Vision Pro. With Trip.Vision, users can virtually explore destinations such as Antarctica, the Maldives, Mount Everest and others, and also check out 360-degree panoramic videos accompanied by voiceovers and attraction information. This application is likely to captivate and entice consumers, driving more travel bookings as consumers virtually immerse themselves in different travel destinations before making a booking to experience it firsthand.

- Lunar New Year Travel Surge. Trip.com saw an increase in travel bookings over the upcoming Lunar New Year Festival. Bookings for trips to and from China over the period have soared more than 900% YoY, supported by easier visa policies, especially in the Asia Pacific region. Both outbound and inbound travel saw increased demand, with inbound travel reservations surging more than 10 times as tourists flock to China to experience the festivity. Furthermore, with around 9bn people travelling between regions in China in 1Q24, this also set s a new record high in the post-COVID period and nearly the pre-pandemic level of 2019.

- 3Q23 earnings. Revenue increased by 99.4% YoY to RMB13.74bn in 3Q23, compared to RMB6.89bn in 3Q22. Net profit rose to RMB4.62bn in 3Q23, compared to RMB266mn in 3Q22. Basic EPS of RMB7.05 in 3Q23, compared to RMB0.41 cents in 3Q22.

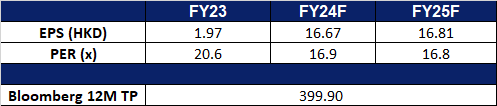

- Market consensus.

(Source: Bloomberg)

Sands China Ltd. (1928 HK): Expect more visits during Chinese New Year

- RE-ITEREATE BUY Entry – 21.4 Target – 23.4 Stop Loss – 20.4

- Sands China Ltd. is an investment holding company principally engaged in the development and operation of integrated resorts in Macao. The Company operates many places, including gaming areas, meeting space, convention and exhibition halls, retail and dining areas and entertainment venues. The Company operates its business through six segments: The Venetian Macao, Sands Cotai Central, The Plaza Macao, Sands Macao, Ferry and Other Operations and The Parisian Macao. Through its subsidiaries, the Company is also engaged in the provision of high speed ferry transportation services. The Company’s subsidiaries include Cotai Ferry Company Limited, Hotel (Macau) Limited and Development Limited.

- Lunar New Year travel seasonality. Anticipating the upcoming Lunar New Year in early February, China is preparing for a surge in travel with an expected 9.0 billion domestic journeys as individuals travel to their hometowns to celebrate the festive season. Projections include 80 million air trips, reflecting a 9.8 percent increase compared to pre-pandemic levels in 2019. Beijing airports are expected to witness a significant 60 percent rise in passenger numbers during this travel rush. This heightened travel activity is likely to benefit Sands China, as the increased volume is expected to drive demand for hotel bookings.

- Macau Japan Spring Festival. Commencing on Thursday and extending until March 30, the CONTEMPO Macau Japan Spring Festival’s first edition is underway at Sands China’s integrated resorts. This two-month-long festival encompasses a diverse range of events, featuring popular idol performances, a captivating kimono culture exhibition, immersive culinary experiences, and art presentations. The primary objective is to foster cultural exchanges and collaboration between Macau and Japan, aiming to not only facilitate industry interactions but also encourage increased visitor flow between the two regions.

- Partnership with Tencent and Maoyan. Sands China has recently formed a strategic alliance with Tencent Video and Maoyan Entertainment, aiming to capitalize on their strengths to promote collaboration. This partnership will involve organizing significant offline events, developing lifestyle and entertainment content, and undertaking online marketing and promotional activities. These joint efforts are geared towards sustaining the diversification of Macau’s tourism industry and bolstering the city’s reputation as a premium destination.

- 1H23 earnings. Revenue increased by 216.4% YoY to US$2,895mn in 1H23, compared to US$915mn in 1H22. Net profit of US$175mn in 1H23, compared to a net loss of US$760mn in 1H22. Basic EPS of US2.16 cents in 1H23, compared to US9.39 cents in 1H22.

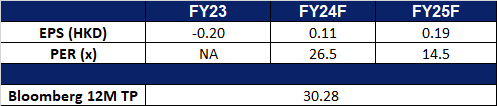

- Market consensus.

(Source: Bloomberg)

Palantir Technologies Inc (PLTR US): Record breaking year

- RE-ITEREATE BUY Entry – 16.5 Target – 24.0 Stop Loss – 15.5

- Palantir Technologies Inc. develops software to analyze information. The Company offers solutions support many kinds of data including structured, unstructured, relational, temporal, and geospatial. Palantir Technologies serves customers worldwide.

- Earnings exceeded estimates. In FY23, Palantir achieved a record profit of US$209.8mn which exceeded profit estimates, marking its first profitable full year, buoyed by robust demand for its AI solutions. The company secured 103 deals exceeding US$1mn each in Q4, with US commercial revenue spiking by 70%. Palantir foresees at least a 40% increase in US commercial revenue for 2024, reflecting a shift towards commercial clients. However, growth in the government segment slowed, partly attributed to contract timing and AI scaling. Palantir’s adjusted 2024 profit forecast surpassed expectations, while its revenue projection aligned with estimates. The significant impact of AI is reflected in Palantir’s growth in revenue for Q4 and is expected to continue to drive growth in the current year. Notably, the company’s fourth-quarter results mark its fifth straight quarter of profitability, which makes it eligible for inclusion in the S&P 500.

- Catching up. The recent market surge in the S&P 500 and Nasdaq, driven by strong performances from tech giants like Meta and Microsoft, suggests growing investor confidence in the potential of AI. This trend is likely to benefit smaller and mid-sized AI companies, as evidenced by the 19% jump in Palantir’s share price after positive earnings results and future guidance were released.

- 4Q23 earnings review. Revenue rose by 19.6% YoY to US$608.35mn, beating estimates by US$5.55mn. Non-GAAP EPS was US$0.08, in-line with estimates. In 1Q24 it expects revenue to be between US$612mn- US$616mn and FY24 revenue to be between US$2.652bn- US$2.668bn.

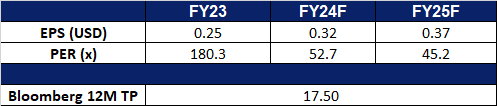

- Market consensus.

(Source: Bloomberg)

Adobe Inc (ADBE US): A lagging AI-themed stock

- RE-ITEREATE BUY Entry – 612 Target – 650 Stop Loss – 593

- Adobe Inc. develops, markets, and supports computer software products and technologies. The Company’s products allow users to express and use information across all print and electronic media. Adobe offers a line of application software products, type products, and content for creating, distributing, and managing information.

- Artificial intelligence application layer explodes. The artificial intelligence application layer explodes. Artificial intelligence stands at the forefront of the upcoming technological revolution, with distinct leaders emerging in various application domains. Microsoft dominates the office software realm, while Adobe leads in drawing and editing applications. The current surge of start-ups focused on short video and drawing artificial intelligence indicates a rapid evolution in this sector, suggesting it could be the first to achieve mature applications of AI.

- Abandoned the acquisition of Figma. In December of 2023, Adobe decided to halt its $20bn acquisition of Figma due to regulatory pressures from the EU and British authorities. This announcement was well-received by the market. While technological revolutions often spark waves of mergers and acquisitions among related startups, the subsequent return to market rationality often reveals overvaluations in many target companies. Therefore, the termination of Adobe’s acquisition of Figma may ultimately be beneficial for the company, allowing it to judiciously allocate cash toward acquisitions or stock buybacks.

- 4Q23 results. Revenue increased to US$5.05bn, an increase of 11.5% YoY, exceeding expectations by US$30mn. Non-GAAP earnings per share were $4.27, beating expectations by $0.13. Revenue in the first quarter of FY24 is expected to be US$5.1bn to US$5.15bn, compared with market expectations of US$5.15bn. Non-GAAP earnings per share were between $4.35 and $4.40, compared with consensus expectations of $4.27.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add Keppel Ltd (KEP SP) at S$7.24, Las Vegas Sands Corp (LVS US) at US$50 and Jumbo Group Ltd (JUMBO SP) at S$0.265.