Technical Analysis – 2 February 2024

United States | Singapore | Hong Kong | Earnings

UR Energy Inc. (URG US)

- Shares closed at a 52-week high with constructive volume.

- MACD is positive, RSI is at an “overbought” level.

- Long – Entry 1.94, Target 2.10, Stop 1.86

Energy Fuels, Inc. (UUUU US)

- Shares closed higher above the 5dEMA with a surge in volume. 20dEMA is about to cross the 50dEMA.

- MACD is positive, RSI is constructive.

- Long – Entry 7.80, Target 8.50, Stop 7.45

SATS Ltd. (SATS SP)

- Shares closed higher above the 20dEMA with a surge in volume. 5dEMA is about to cross the 20dEMA.

- MACD is about to turn positive, RSI is constructive.

- Long – Entry 2.80, Target 3.00, Stop 2.70

The Hour Glass (HG SP)

- Shares closed higher above the 20dEMA with constructive volume. 5dEMA is about to cross the 20dEMA.

- MACD just turned positive, RSI is turning constructive.

- Long – Entry 1.55, Target 1.65, Stop 1.50

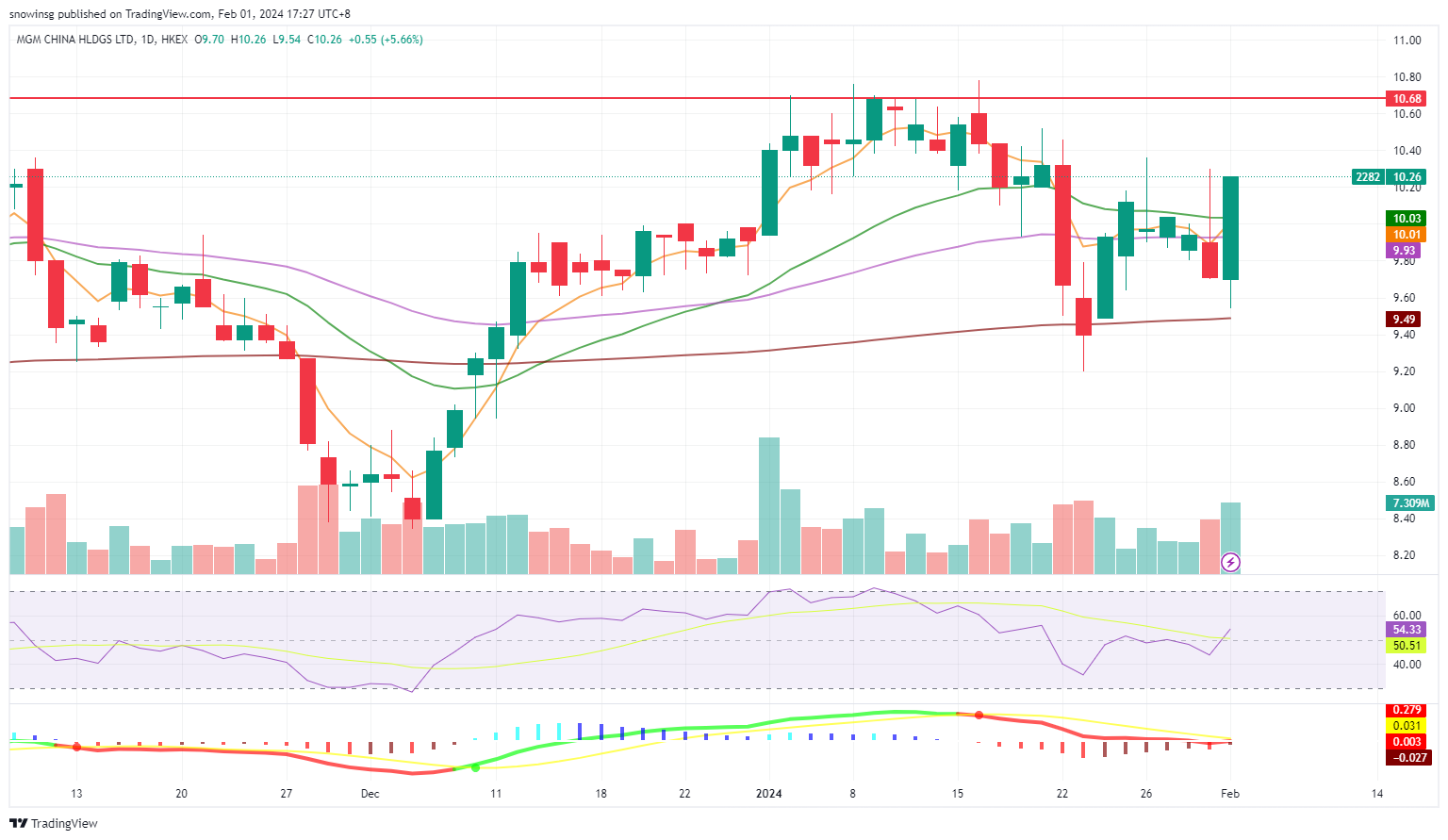

MGM China Holdings Ltd (2282 HK)

- Shares closed above the 20dEMA with rising volume. The 5dEMA crossed the 50dEMA and is about to cross the 20dEMA.

- RSI is constructive, while MACD is about to turn positive.

- Long – Entry 9.92, Target 10.68, Stop 9.54

Galaxy Entertainment Group Ltd (27 HK)

- Shares closed above the 50dEMA with an incline in volume.

- RSI is constructive and MACD is positive.

- Long – Entry 41.7, Target 44.5, Stop 40.3

Boeing Co (BA)

- 4Q23 Revenue: $22.02B, +10.2% YoY, beat estimates by $940M

- 4Q23 Non-GAAP EPS: –$0.47, beat estimates by $0.32

- FY24 Guidance: No guidance due to 737 Max 9 crisis. FY25 to FY26 target of reaching $10bn of free cash flow, $100bn in revenue and annual deliveries of about 800 planes.

- Comment: Boeing reported a narrower-than-expected quarterly loss and better-than-expected revenue and free cash flow. The company’s executives reaffirmed their financial targets for 2025-2026, aiming for a free cash flow of approximately $10 billion and 737 production of 50 per month. The recent mid-air cabin-panel blowout incident involving a 737 MAX jet has prompted increased regulatory scrutiny, impacting production and market share. Despite challenges, Boeing would continue to keep its 737 suppliers producing at higher rates and would be willing to hold more inventory, which would benefit some of its suppliers to catch up with the current rate hikes. Its CEO emphasized the company’s commitment to quality and readiness to slow down if needed to address issues. The MAX safety concerns continue to pose uncertainties for Boeing’s recovery. Investors should monitor the ongoing National Transportation Safety Board investigation for further updates on the MAX safety issues. 1Q24 recommended trading range: $190 to $230. Neutral Outlook.

波音(BA)

- 23财年第四季营收:220.2亿美元, 同比增幅10.2%,超预期9.4亿美元

- 23财年第四季Non-GAAP每股亏损:0.47美元,超预期0.32美元

- 24财年指引:由于737 Max 9危机,暂无指引。2025年至2026年目标实现1,000亿美元的营收,每年交付约800架飞机,自由现金流达到100亿美元。

- 短评:波音报告的季度亏损比预期小,营收和自由现金流均好于预期。公司高管重申了2025-2026年的财务目标,力争自由现金流约100亿美元和每月737生产50架飞机。最近涉及737 MAX飞机的空中舱板爆炸事件引起了更多监管审查,影响了生产和市场份额。尽管面临挑战,波音将继续要求其737供应商保持较高产能,并愿意持有更多的库存,以帮助一些供应商赶上当前的产能提升。公司首席执行官强调了公司对质量的承诺,并表示在需要时愿意减缓以解决问题。MAX飞机安全问题继续给波音的复苏带来不确定性。投资者应密切关注国家运输安全委员会对MAX安全问题的调查,以获取进一步更新。24财年第一季度建议交易区间:190美至230美元。中性前景。

- 4Q23 Revenue: DKK 65.86B, 37.0% YoY

- 4Q23 GAAP EPS: DKK 4.91

- FY24 Guidance: Expect sales growth at a constant exchange rate (CER) of 18% to 26%. Operating profit growth at CER 21% to 29%. Financial items (net) gain of around DKK1.3bn and capital expenditure (PPE) around DKK45bn. Depreciation, amortisation and impairment losses around DKK10bn and free cash flow (excluding impact for business development) DKK64-74bn.

- Comment: Novo Nordisk reported robust 2023 revenue and earnings, fuelled by a 31% increase in sales (36% at constant exchange rates) to DKK232.3bn. The company’s weight loss drug Wegovy and diabetes drug Ozempic contribute significantly to sales growth. Full-year operating profit rises by 37% in kroner and 44% at constant exchange rates. Novo Nordisk anticipates sales growth between 18% and 26% in constant exchange rates in 2024, driven by strong demand for Wegovy and Ozempic. Its CEO welcomes competition in the obesity market, anticipating prices of Wegovy to decline as volumes of weekly injection increase, emphasizing the company’s commitment to patient care. The company acknowledges increased pressure on its supply chain but continues to invest in expanding production capacity to meet rising demand. 1Q24 recommended trading range: $105 to $125. Positive Outlook.

诺和诺德(NVO)

- 23财年第四季营收:658.6亿丹麦克朗, 同比增幅37.0%

- 23财年第四季GAAP每股盈利:4.91丹麦克朗美元

- 24财年指引:预计销售额将以不变汇率(CER)增长18%至26%,运营利润预计以CER增长21%至29%。财务项目(净额)约为丹麦克朗13亿,资本支出(PPE)约为丹麦克朗450亿。折旧、摊销和减值损失约为丹麦克朗100亿,而自由现金流(不包括业务发展的影响)预计在丹麦克朗640亿至740亿之间。

- 短评:诺和诺德报告了2023年强劲的营收和盈利,销售额同比增长31%(在不变汇率下增长36%)达到丹麦克朗2,323亿。公司的减肥药Wegovy和糖尿病药Ozempic对销售增长有着显著的贡献。全年运营利润在克朗计算增长了37%,在不变汇率下增长了44%。诺和诺德预计2024年销售额在不变汇率下将增长18%至26%,主要受到Wegovy和Ozempic强劲需求的推动。首席执行官对肥胖市场的竞争表示欢迎,预计随着每周注射量的增加,Wegovy的价格将下降,并强调公司对患者护理的承诺。公司承认其供应链面临增加的压力,但仍在投资扩大生产能力以满足不断增长的需求。24财年第一季度建议交易区间:105美至125美元。积极前景。

Mastercard Inc (MA)

- 4Q23 Revenue: $6.5B, +13% YoY, beat estimates by $20M

- 4Q23 Non-GAAP EPS: $3.18, beat estimates by $0.10

- 1Q24 Guidance: No guidance provided.

- Comment: Mastercard reported a strong set of results as the payments processor benefited from resilient consumer spending during the holiday shopping season. However, the company also saw an increase in operating expenses, attributed primarily to higher personnel costs. With consumer sentiment rebounding to the highest level since July 2021, the company is likely to experience an uptick in transaction volume in the near term. Hopes of a “soft landing” for the economy and bets on interest rate cuts by the U.S. Federal Reserve also encouraged big-ticket purchases and more travel. 3Q24 recommended trading range: $435 to $480. Positive Outlook.

万事达(MA)

- 23财年第四季营收:620.2亿美元, 同比增幅13.0%,超预期2,000万美元

- 23财年第四季Non-GAAP每股盈利:3.18美元,超预期0.10美元

- 24财年指引:不提供指引。

- 短评:万事达卡报告了强劲的业绩,作为支付处理器,受益于假日购物季节中消费者支出的坚挺。然而,该公司的运营费用也出现了增加,主要归因于人员成本的上升。随着消费者信心自2021年7月以来的最高水平回升,公司可能在短期内看到交易量的增加。对经济实现“软着陆”的期望以及美联储降息的赌注也鼓励了大宗购买和更多的旅行。24财年第一季度建议交易区间:435美至480美元。积极前景。

Qualcomm Inc (QCOM)

- 1Q24 Revenue: $9.92B, +5.0% YoY, beat estimates by $410M

- 1Q24 GAAP EPS: $2.75, beat estimates by $0.38

- 2Q24 Guidance: Expect adjusted earnings of between $1.73 and $1.93 per share on revenue of $8.9 billion to $9.7 billion. Consensus expectations, according to LSEG, were for earnings of $2.25 per share on $9.3 billion of revenue.

- Comment: Qualcomm posted robust results, shipping $6.69 billion in handset chips during the December quarter, marking a 16% YoY increase and signaling a positive turn for the smartphone market after two years of decline. The company secured a chip supply deal with Samsung for the flagship Galaxy S24 model, emphasizing a global partnership. Management notes the stabilization of the Android market post a challenging 2023. Beyond smartphones, Qualcomm, a major player in the smartphone industry, is actively applying its chip technology to diverse markets such as PCs, cars, and virtual reality headsets. 2Q24 recommended trading range: $140 to $170. Positive Outlook.

高通(QCOM)

- 24财年第一季营收:99.2亿美元, 同比增幅5.0%,超预期4.1亿美元

- 23财年第一季Non-GAAP每股盈利:2.75美元,超预期0.38美元

- 24财年指引:预计调整后每股收益介于1.73美元至1.93美元之间,营收介于89亿美元至97亿美元。根据伦敦证券交易所(LSEG)的共识预期,每股收益为2.25美元,营收为93亿美元。

- 短评:高通发布了强劲的业绩,仅在12月季度便发货66.9亿美元的手机芯片,同比增长16%,标志着智能手机市场在两年下滑后出现了积极的转机。该公司与三星签订了旗舰机型Galaxy S24的芯片供应协议,强调了全球合作伙伴关系。管理层指出在经历了2023年的挑战后,Android市场已经趋于稳定。除了智能手机,作为智能手机行业的主要参与者,高通还积极将其芯片技术应用于诸如个人电脑、汽车和虚拟现实头显等多样化市场。24财年第二季度建议交易区间:140美至170美元。积极前景。

Wolfspeed Inc. (WOLF)

- 2Q24 Revenue: $208.4M, +19.9% YoY, beat estimates by $1.99M

- 2Q24 GAAP EPS: -$1.00, beat estimates by $0.06

- 3Q24 Guidance: Target revenue from continuing operations in a range of $185 million to $215 million. GAAP net loss from continuing operations is targeted at $134 million to $155 million, or $1.07 to $1.23 per diluted share.

- Comment: Wolfspeed exceeded expectations, achieving record quarterly design wins totaling $2.9 billion. Management attributes this success to the effective execution of our strategy, reinforcing our vision for Wolfspeed and silicon carbide’s future. However, the company anticipates third-quarter revenue below estimates, as slower electric vehicle sales growth impacts the demand for its semiconductors. Notably, major EV companies like Tesla project muted demand for EVs in 2024, with a lower volume growth rate compared to 2023, indirectly affecting the demand for Wolfspeed’s products. 3Q24 recommended trading range: $25 to $35. Neutral Outlook.

Wolfspeed (WOLF)

- 24财年第二季营收:2.084亿美元, 同比增幅19.9%,超预期199万美元

- 24财年第二季GAAP每股亏损:1.0美元,超预期0.06美元

- 24财年第三季指引:目标从持续经营中实现营收范围在1.85亿美元至2.15亿美元。预计从持续经营中的GAAP净亏损为1.34亿美元至1.55亿美元,每股摊薄亏损为1.07美元至1.23美元。

- 短评:Wolfspeed超出了预期,取得了总额为29亿美元的创纪录季度设计赢。管理层将这一成功归因于我们战略的有效执行,加强了我们对Wolfspeed和碳化硅未来的愿景。然而,由于电动汽车销售增长放缓影响了对其半导体的需求,公司预计第三季度营收将低于预期。值得注意的是,像特斯拉等主要电动汽车公司预计2024年电动汽车需求疲软,增长率较2023年较低,间接影响了Wolfspeed产品的需求。24财年第一季度建议交易区间:25美至35美元。中性前景。