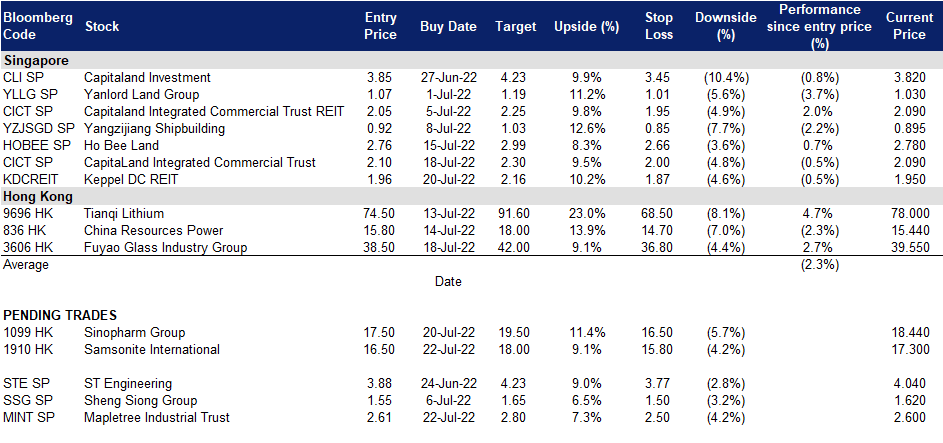

22 July 2022: Mapletree Industrial Trust (MINT SP), Samsonite International S.A. (1910 HK)

Singapore Trading Ideas | Hong Kong Trading Ideas | Market Movers | Trading Dashboard

Mapletree Industrial Trust (MINT SP): Undervalued industrial play looking to increase exposure to US data centres

- BUY Entry 2.61 – Target – 2.80 Stop Loss – 2.50

- Mapletree Industrial Trust (MINT) is a Singapore REIT established with the principal investment strategy of investing, directly or indirectly, in a diversified portfolio of income-producing real estate used primarily for industrial purposes, whether wholly or partially, in Singapore, as well as real estate-related assets. As of 9 June 2022, MINT has a portfolio of 141 industrial properties across Singapore and North America. As at 31 March 2022, its AUM stood at S$8.8bn.

- Industrial prices and rentals continue on ascent. Based on JTC’s 1Q22 report, prices and rentals of industrial properties continued to rise, with both indices expanding by 2.1% and 1.0% on a QoQ basis and 5.6%/2.4% on a YoY basis. On the outlook, an estimated 2.4m sqm of space could be completed by March 2022, the largest amount of supply to come on stream over the past 7 years. Barring any sharp economic slowdown, JTC believes that demand will remain robust and be able to soak up the strong supply pipeline.

- Data centre (DC) pivot could gather pace. Despite recently divesting a DC in Michigan, US due to lack of leasing traction, MINT appears to be on the lookout to add on to its DC portfolio there. Notably, in its recent presentation to investors, MINT outlined its ROFR on the remaining 50%-interest that it does not own in a portfolio of 13 North American DCs. The valuation of the entire portfolio as at 31 March 2022 stood at S$1.82bn. With gearing as at 31 March 2022 standing at 38.4%, and available debt facilities worth S$900m, MINT would have the financial muscle to acquire the remaining 50%-interest easily.

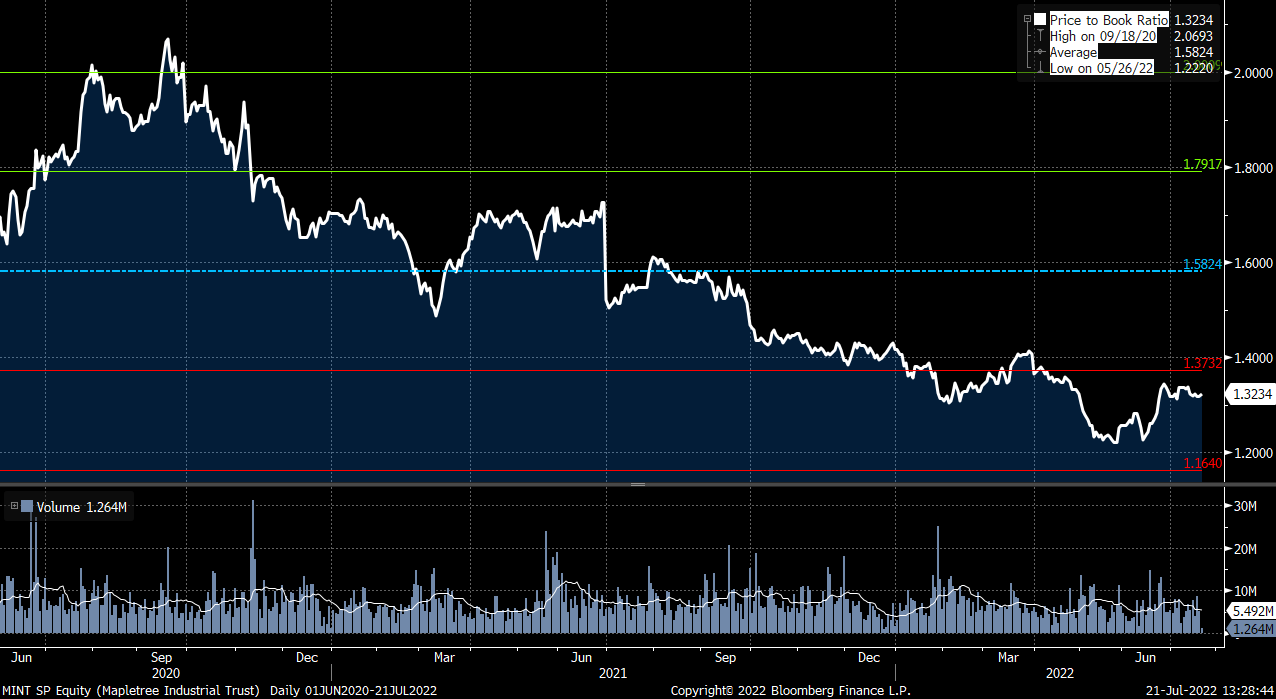

- Trading at >1sd away from 2-year average valuations. The Street currently has 11/5/0 BUY/HOLD/SELL ratings and an average TP of S$2.88. Based on consensus estimates, FY23F gross revenue and NPI should grow 5.5%/6.2% YoY, while FY22F DPU growth should edge 1.4% YoY higher to S$0.14 apiece. We believe that MINT is trading at a significant discount to its historical trading range considering that it is currently trading more than 1sd away from its 2-year mean of ~1.6x P/B. At current prices, MINT would trade at an attractive 5.4%/5.5% FY22F/23F yield.

Keppel DC REIT (KDCREIT SP): Undervalued DC play could see mean reversion post 1H22 results

- RE-ITERATE BUY Entry 1.96 – Target – 2.16 Stop Loss – 1.87

- Keppel DC REIT is the first pure-play data centre REIT listed in Asia on SGX. KDCREIT’s investment strategy is to invest in a portfolio of income-producing real estate assets which are used primarily for data centre purposes as well as real estate-related assets. With a portfolio of assets located in key data centre hubs across Asia Pacific and Europe, the Manager aims to deliver sustainable returns to investors by capturing value from the data centre industry.

- 1H22 results to see continued support from past acquisitions. Contributions from its previously acquired Eindhoven DC, Guangdong DC, London DC, and the completion of AEIs at its DC1 and Intellicentre3 development will continue to support topline revenue. Nonetheless, we expect NPI margins to continue to be afflicted by strong energy prices, we note that MSCI Global Energy Index only peaked in early June but has been on the downtrend ever since, indicating that energy prices may have peaked.

- Demand for DCs continues to be strong, supply deluge may provide a cap floor. According to Cushman & Wakefield, demand for contiguous 10MW or more blocks of DC capacity continues to be strong. In fact, 18 markets that the firm tracks are currently now in sub-teen vacancies, double the number from 2021. This has led to continued growth in data center construction globally, providing ample acquisition opportunities for KDCREIT. In 2022, Cushman & Wakefield is expecting 4.1 GW (2021: 2.9GW) of DC capacity to be developed. Notably, London (prior KDCREIT acquisition) is a key location that is developing supply rapidly. Other Markets include Hong Kong and Jakarta.

- Post 1Q22 correction may have been overdone. Recall that in 1Q22, KDCREIT reported flat DPU of S$0.02466 apiece (+0.2% YoY). Investors were worried that NPI margin contraction to 91% from 91.5% could spill over especially in an inflationary environment. This has led to a number of Street downgrades, resulting in 5/7/1 BUY/HOLD/SELL ratings and an average TP of S$2.29. Based on consensus estimates, FY22F gross revenue should swell 7.8% YoY, while NPI should nodge a lower but still respectable 4.7% YoY increase. FY22F DPU growth should come in at 2% YoY to S$0.101 apiece. We believe that KDCREIT is trading at a significant discount to its historical trading range considering that it is currently trading ~2sd away from its 2-year mean of ~2.1x P/B. At current prices, KDCREIT would trade at an attractive 5.1%/5.4% FY22F/23F yield.

Samsonite International S.A. (1910 HK): Travelling peak season has come

- Buy Entry – 16.5 Target – 18.0 Stop Loss – 15.8

- Samsonite International S.A. is a Hong Kong-based company principally engaged in the design, manufacture, sourcing and distribution of luggages, business and computer bags, outdoor and casual bags, travel accessories and slim protective cases for personal electronic devices. The Company operates its business through three segments. The Travel Bag segment is engaged in travel products with suitcases and carry-ons of three main categories, including hard-side, soft-side and hybrid luggages. The Casual Bags segment is engaged in daily use, including different types of backpacks, female and male shoulder bags and wheeled duffel bags. The Business Bags segment is engaged in business use, including rolling mobile office bags, briefcases and computer bags.

- Air travel recovery continued to gain momentum. According to IATA, the total demand for air travel in May 2022 (measured in revenue passenger kilometers or RPKs) was up 83.1% YoY. Global traffic is now at 68.7% of pre-Covid levels. May domestic air travel was up 0.2% YoY. Overall, May domestic traffic was 76.7% of May 2019. International RPKs rose 325.8% YoY in May. May 2022 international RPKs reached 64.1% of May 2019 levels.

- 1Q22 results review. Net sales jumped by 67.7% YoY to US$576.6mn. Operating profit arrived at US$58.1mn compared to a loss of US$47mn during the same period last year. Profit attributable to the equity shareholders arrived at US$16.4mn in 1Q22 compared to a loss of US$72.7mn in 1Q21. The effects of the COVID-19 pandemic on demand for the company’s products moderated due to the continued rollout and effectiveness of vaccines leading governments in many countries to further loosen social-distancing, travel and other restrictions, which has led to the continuing recovery in travel. The company will announce 2Q22 results on 17th August.

- The updated market consensus of the EPS growth in FY22/23 is 1,100%/49.2% YoY, respectively, translating to 18.4×/12.3x forward PE. The current PER is 30.8x. Bloomberg consensus average 12-month target price is HK$22.43.

(Source: Bloomberg)

Sinopharm Group Co., Ltd. (1099 HK): A defensive counter amidst a market downturn

- RE-ITERATE BUY Entry – 17.5 Target – 19.5 Stop Loss – 16.5

- Sinopharm Group Co Ltd is a China-based company principally engaged in pharmaceutical and medical devices distribution business. The Company operates its business through four segments. Pharmaceutical Distribution segment is engaged in the distribution of pharmaceutical products to hospitals, other distributors, retail pharmacy stores and clinics. Medical Devices segment is engaged in the distribution of medical devices, as well as provides installation and maintenance services. Retail Pharmacy segment is engaged in the operation of chain pharmacy stores. Other Business segment is engaged in the distribution of laboratory supplies, manufacture and distribution of chemical reagents, production and sale of pharmaceutical products.

- 1Q22 earnings review. 1Q22 revenue grew by 6.86% YoY to RMB17.15bn. Net profit attributable to shareholders dropped by 23.25% YoY to RMB252.36mn. The decrease in profit was mainly attributable to the decline in the results of Sinopharm Accord’s associates due to the impact of the Covid-19 pandemic, which resulted in a corresponding decrease in investment income of Sinopharm Accord. At the same time, due to the impact of the pandemic, the retail sector has seen a decline in store traffic, and the new stores opened in 2021 cost a large initial investment, the benefits of which have not yet emerged, resulting in a decrease in the margin levels.

- A defensive stock amidst a market downturn. The Hong Kong market has been hammered by both a slowdown in China’s economy and geopolitical risks. Growth, value, and cyclical sectors, as well as other thematic stocks, have been sold off indiscriminately. However, this stock is relatively outperforming the rest as its business is largely immune to inflation and policy risks. The business driver is the distribution volume rather than profit margins. The growth in demand for medicines and medical devices is stable with low price sensitivity.

- The updated market consensus of the EPS growth in FY22/23 is -0.6%/9.9% YoY respectively, which translates to 5.8x/5.3x forward PE. The current PER is 8.3x. The FY22F/23F dividend yield is 5.2%/5.7%. Bloomberg consensus average 12-month target price is HK$23.37.

(Source: Bloomberg)

United States

Top Sector Gainers

| Sector | Gain | Related News |

| Motor Vehicles | +5.90% | Tesla shares jump on second-quarter report that was better than analysts feared Tesla Inc (TSLA US) |

| Medical Specialties | +3.66% | Danaher stock rises as Q2 sales soar beating estimates despite impact on COVID products Danaher Corp (DHR US) |

| Tobacco | +2.39% | Philip Morris: Remarkably Strong Q2 Excluding Currency And Russia Philip Morris International Inc (PM US) |

Top Sector Losers

| Sector | Loss | Related News |

| Major Telecommunications | -3.32% | AT&T shares fall after company says later payments, higher spending are hurting cash flow AT&T Inc (T US) |

| Oil Refining/Marketing | -2.98% | Oil slumps $3/bbl on gasoline stockpiles, rate hikes and resuming supply Marathon Petroleum Corp (MPC US) |

| Hotels/Resorts/Cruise lines | -2.35% | Cruise Stocks Fall After Carnival Sells $1 Billion of Shares Carnival Corp(CCL US) |

- Danaher Corp (DHR US) jumped 9.1% after the company reported better-than-expected earnings and revenue for its most recent quarter, citing higher sales that helped offset an increase in its expenses. Danaher posted adjusted earnings of $2.76 per share on revenue of $7.75 billion, compared to expected earnings of $2.35 per share on revenue of $7.3 billion, according to Refinitiv.

- Tesla Inc (TSLA US) rose 9.8% a day after the automaker reported earnings that were slightly better than Wall Street expected in the second quarter. Tesla posted adjusted earnings of $2.27 per share on $16.93 billion in revenue, compared to expected earnings of $1.81 per share on revenue of $17.10 billion, according to Refinitiv.

- AT&T Inc (T US) plunged 7.6% after AT&T trimmed its free cash flow guidance for the full year. AT&T topped analysts’ estimates on the top and bottom lines in the second quarter, posting adjusted earnings of 65 cents a share on revenues of $29.64 billion.

- Shares of both United Airlines Holdings Inc (UAL US) and American Airlines Group Inc (AAL US) dropped 10.2% and 7.4% respectively after both airlines reported quarterly results. United’s earnings fell short of Wall Street’s expectations, while American scaled back its growth plans. United posted its first profitable quarter since the start of the pandemic.

Singapore

- Rex International Holding Ltd (REXI SP), Dyna-Mac Holdings Ltd (DMHL SP) and Sembcorp Marine Ltd (SMM SP) shares fell 4.2%, 2.1% and 1.9% respectively yesterday. Oil prices fell more than $3 on Thursday after higher U.S. gasoline stockpiles stoked demand worries and returning energy supply from Libya and Russia eased supply concerns. Oil futures trading volumes have been thin and prices volatile as traders have to square tighter supply because of the loss of Russian barrels following the country’s invasion of Ukraine, with recessionary worries about weaker energy demand.

- Chip Eng Seng Corp Ltd (CHIP SP) shares fell 1.6% yesterday. It is terminating its sale contracts with purchasers of units in 28 Lyall South Perth, a proposed mixed-use development in Western Australia by the group’s 70 per cent-owned joint venture subsidiary. In a bourse filing on Thursday, the group said it has been unable to engage a builder to construct the project “on terms which are financially viable”, in light of rising construction costs in Western Australia due to supply chain disruptions brought about by the Covid-19 pandemic.

- NIO Inc (NIO SP) shares fell 1.5% yesterday. A Reuters report stated that 41 different cities in China are implementing some form of COVID-19 lockdown as cases spike once again across the country. Earlier this week the lockdown in Macau was extended, and now investors have concerns that key EV hubs like Shanghai and the Anhui Province will see lockdowns of their own. Any new lockdowns imposed would certainly have another impact on production this quarter, and Chinese EV investors are getting out before it happens.

Hong Kong

Top Sector Gainers

| Sector | Gain | Related News |

| Industrial Goods | +1.43% | China’s Industrial Activity Shows Signs of Weathering Covid Outbreaks Xinyi Glass Holdings Ltd (868 HK) |

| Alcoholic Drinks & Tobacco | +1.19% | NA Budweiser Brewing Company APAC Ltd (1876 HK) |

| Apparel | +0.52% | Biden Expects to Speak With China’s Xi Within Next 10 Days Li Ning Co. Ltd (2331 HK) |

Top Sector Losers

| Sector | Loss | Related News |

| Insurance | -1.87% | China to Repay More Victims Next Week in Biggest Bank Scam AIA Group Ltd (1299 HK) |

| Gamble | -1.73% | Macau Casino Crash Shifts World’s Gambling Crown to Las Vegas Galaxy Entertainment Group (27 HK) |

| Property Management & Agency | -1.41% | Property crisis traps China in a market paradox Country Garden Services Holdings Co Ltd (6098 HK) |

- Country Garden Services Holdings Co Ltd (6098 HK) and Longfor Group Holdings Ltd (0960 HK) shares fell 8.8% and 7.2% respectively yesterday. According to CRIC China, from January to June this year, there were 1,666 real estate project companies that were continuously overdue, accounting for 62.5% of all overdue companies, and the proportion was higher compared to previous months. According to the statistics of the China Index Research Institute, July and August of this year are the second peak of debt repayment during the year, and the balance due in both months exceeds 100 billion yuan respectively. Analysts said that the confidence in the new home sales market has been hit and the debt repayment peak of real estate companies is approaching, and the drying up of housing companies’ liquidity may heighten credit risk.

- Inner Mongolia Yitai Coal Co Ltd (3948 HK) shares fell 8.0% yesterday. It was reported that since April 19, the cumulative decline of coking coal has exceeded 38%. On July 20, there were media reports that the Market Committee of the China Coking Association recently held a market analysis meeting. The participants said that in view of the current industry operating conditions, increasing production restrictions and striving for cash flow are the only way out for companies to successfully tide over the difficult period. The participating companies have agreed to limit production by more than 50% from now on, which will lead to joint production restrictions with regional companies.

- NagaCorp Ltd (3918 HK) shares fell 6.6% yesterday. Bank of America Securities released a research report reiterating its “buy” rating on NagaCorp, lowered its 2022/23 EBITDA forecast by 2%/11%, and lowered its target price by 10% from HK$11.5 to 10.4 Hong Kong dollar. The company reported EBITDA of $130 million for the first half of the year, slightly below the bank’s forecast. It also believes that the valuation of NagaCorp is attractive, which is equivalent to 6.6 times the estimated enterprise value to EBITDA next year. It may also benefit from the development of the Naga 3 project.

- ZhongAn Online P&C Insurance Co Ltd (6060 HK) shares fell 10.4% yesterday. The group issued a profit warning that for the six months ended June 30, 2022, ZhongAn Insurance is expected to record a net loss in the range of approximately RMB 650 million to RMB 750 million. For the six months ended June 30, 2021, Zhong An Insurance’s net profit was RMB 604 million. In response, a number of major banks lowered their target prices. The bank believes that most of the factors responsible for the loss in the first half of the year are one-offs, and expects the company to record a year-on-year improvement in CoR in the second half of the year, as actual claims may be lower than in the second quarter as the lockdown gradually eases.

Trading Dashboard Update: No stock additions/deletions.