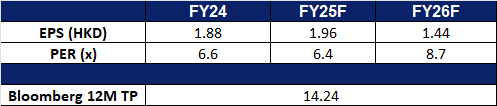

Geo Energy Resources Limited is an integrated coal mining specialist. The Company owns and operates coal mines, offers mine contracting services to third party mine owners, and sells coal to both coal traders and coal export companies.

Cost optimisation and extra revenue. The US$150 million integrated infrastructure project, featuring a 92 km hauling road and jetty with a total capacity of 40-50 million tonnes, is set to be a cornerstone of the company’s growth strategy. This initiative not only enhances cost efficiency, potentially generating US$400 million to US$500 million in EBITDA (assuming coal prices remain at the range of US$50) as the TRA mine is potentially scaled up, but also opens an additional revenue stream of US$120 million to US$150 million through the leasing of 15 million tonnes of road haulage to third party users.

Upbeat production guidance. Management has set an upbeat production target of 10.5 million to 11.5 million tonnes for 2025, representing a year-over-year increase of 32.9% to 45.6%. As of February, the company has already achieved 2.4 million tonnes.

Stable outlook for coal prices. The outlook for coal prices remains stable, supported by China’s GDP growth target of around 5% for 2025 and the implementation of proactive macro policies. The anticipated advancements in AI are expected to boost productivity and enhance consumption and investment confidence, stabilizing coal demand and supporting prices.

FY24 results review. Revenue decreased by 18% year-over-year to US$401.9 million, primarily due to lower sales volume and average selling price (ASP). Net profit fell 41% to US$37.3 million.

(Source: Bloomberg)

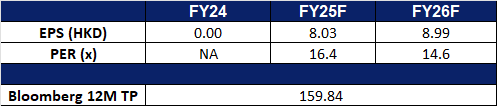

United Hampshire US REIT (UHU SP): Continued growth and expansion

United Hampshire US REIT operates as a real estate investment trust. The Company owns and operates shopping, storage, grocery, and necessity-based retail properties.

Favorable interest rate environment. The Federal Reserve cut interest rates by 25bps in December 2024, bringing the target range to 4.25% to 4.50%. Lower borrowing costs are expected to enhance United Hampshire US REIT’s financial flexibility and support growth. Projections for the Fed funds rate indicate a range of 3.50% to 3.75% by the end of 2025 and 3.25% to 3.50% by the end of 2026.

Strategic divestments. United Hampshire US REIT successfully divested properties, including Lowe’s and Sam’s Club in 2H24 and Supermarket at Albany in January 2025, at over 4% above valuation, demonstrating strong capital recycling efforts.

Strong demand for grocery-anchored strip centers amid limited new supply. Grocery-anchored retail properties remain highly resilient, with grocery store foot traffic increasing 12% from 2019 to 2024, according to Green Street. Service-based tenants, such as coffee shops, salons, and medical centers, further boost footfall, reinforcing the sector’s long-term stability. Hybrid work arrangements have also shifted consumer behavior, increasing demand for localized shopping experiences. Market rent growth for strip centers remained above historical averages in 2024, with a projected 3% annual growth from 2025 to 2029. Investment activity underscores confidence in the sector, Blackstone made its largest retail investment since 2011, acquiring 90 shopping centers for US$4bn, while CBRE expects US$10bn in open-air retail transactions in 2025. Despite strong demand, new strip mall construction remains constrained due to high costs, requiring a 65% rent increase to justify development. This gives existing landlords, including UHU REIT, strong pricing power to negotiate rent increases, securing long-term income growth. With a 97.5% committed occupancy rate and WALE of 8.1 years, UHU REIT is well-positioned to capitalize on these market dynamics.

2H24 results review. Revenue increased 0.4% YoY to US$36.4mn, while net property income dipped 1.6% to US$24.4mn, mainly due to divestments and higher property expenses. DPU declined 4.2% to 2.05 US cents, reflecting higher finance costs.

We have fundamental coverage with a BUY recommendation and a TP of S$0.60. Please read the full report here.

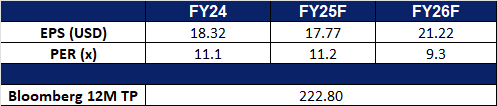

Jiangxi Copper Co Ltd is a China-based company mainly engaged in the mining, smelting and processing of copper and gold. The Company mainly conducts businesses through two segments. The Copper-related Industry segment is mainly engaged in the production and sales of copper and copper-related products. The Gold-related Industry segment is mainly engaged in the production and sales of gold and gold-related products. The Company’s products mainly include cathode copper, gold, silver, sulfuric acid, copper rods, copper tubes, copper foil, selenium, tellurium, rhenium and bismuth. The Company’s products are mainly used in electrical, electronic, light industry, machinery manufacturing, construction, transportation, military industry and other industries. The Company principally conducts its businesses in the domestic market.

Rising copper prices amidst tariffs plays. Copper futures held rangebound around $4.8 per pound recently, hovering near the highest levels since May last year. The announcement of a potential 25% tariff on copper imports by the United States has led to a significant surge in Comex copper prices and increased market volatility. Global copper inventory levels are rising, with a notable increase in Comex stocks due to arbitrage opportunities and anticipation of tariffs, while LME and SHFE inventories show varying trends. Economic uncertainties, including recession fears in the US and deflation in China, are adding to the risks in the copper market, despite ongoing demand from sectors like renewables and technology. The rise in global copper prices is bound to benefit Jiangxi Copper positively.

Copper Prices (1-year)

(Source: Bloomberg)

Expectations of higher copper exports in China. China recently issued more licenses allowing copper smelters to export metal tax-free, aiding local producers and paving the way for greater overseas sales at a time of upheaval in the global market.The license issuances mean that more than a dozen of major Chinese smelters have now been approved for the tolling trade, which involves exporting refined copper that’s been made from imported ore with tax exemptions. Furthermore, with Trump’s announcement of a potential 25% tariff on copper imports by the United States, companies are looking to import more copper before the tariffs kicks in. This is bound to increase copper demand in the near term.

More stake in SolGold and potential access to strategic assets. Jiangxi Copper recently acquired about 157mn shares in SolGold. Following the investment, Jiangxi Copper, through its subsidiary Jiangxi Copper (Hong Kong) Investment Company Limited, would increase its holding in SolGold from 6.95% to 12.19% of the company’s total issued share capital.By increasing its stake in SolGold, Jiangxi Copper gains a larger ownership share and consequently, more influence over SolGold’s decisions. This is particularly important concerning the Cascabel project, a major copper/gold asset. This strategic increase in ownership aligns with JCC’s objective of securing access to vital copper resources.

3Q24 results review. Revenue fell by 6.63% YoY to RMB123.3bn in 3Q24, compared with RMB132.0bn in 3Q23. Net profit fell 13.64% to RMB1.37bn in 3Q24, compared to RMB1.58bn in 3Q23. Basic EPS fell to RMB0.40 in 3Q24, compared to RMB0.46 in 3Q23.

Market consensus.

(Source: Bloomberg)

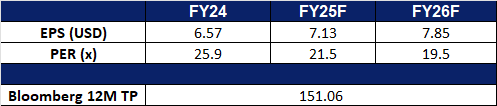

Alibaba Group Holdings Ltd. (9988 HK): Driving China’s digital future

Alibaba Group Holding Ltd provides technology infrastructure and marketing platforms. The Company operates through seven segments. China Commerce segment includes China retail commerce businesses such as Taobao, Tmall and Freshippo, among others, and wholesale business. International Commerce segment includes international retail and wholesale commerce businesses such as Lazada and AliExpress. Local Consumer Services segment includes location-based businesses such as Ele.me, Amap, Fliggy and others. Cainiao segment includes domestic and international one-stop-shop logistics services and supply chain management solutions. Cloud segment provides public and hybrid cloud services like Alibaba Cloud and DingTalk for domestic and foreign enterprises. Digital Media and Entertainment segment includes Youku, Quark and Alibaba Pictures, other content and distribution platforms and online games business. Innovation Initiatives and Others segment include Damo Academy, Tmall Genie and others.

Strong government support. At the recent National People’s Congress, China announced a 10% increase in science and technology spending, allocating RMB398bn (US$55bn). The government aims to foster AI model applications, quantum computing, and 6G technologies, alongside publishing an AI education White Paper to expand its tech talent pool. The government aims to create a more innovation-friendly environment by fostering national laboratories, supporting young scientists, and improving data systems. AI development is a key focus, with increased backing for large-scale models and intelligent manufacturing. This supportive environment is expected to accelerate Alibaba’s AI innovations, enhance its cloud offerings, and solidify its role in China’s digital transformation.

Unveiling its AI model. Alibaba announced its QwQ-32B AI reasoning model, which it claims performs comparably to DeepSeek’s R1 despite having far fewer parameters. Accessible via Qwen Chat, the model enhances Alibaba’s chatbot services and strengthens its AI leadership. With China pushing AI adoption across industries, Alibaba is poised to benefit from rising demand for AI-powered solutions, boosting its cloud business and investor confidence.

AI and cloud investment roadmap. Alibaba’s RMB380bn (US$70bn) investment in cloud computing and AI infrastructure over the next three years surpasses its decade long spending in the sector. As China’s top cloud provider with a 36% market share as of 3Q24 and 13% YoY cloud revenue growth in 4Q24, mainly driven by the double-digit revenue growth of public cloud products, Alibaba’s investment is expected to enhance its AI and cloud capabilities, attract enterprise customers, and drive long-term growth.

4Q24 results review. Revenue increased 8% YoY to RMB280.2bn in 4Q24, compared with RMB260.3bn in 4Q23. Net income rose by 333% YoY to RMB46.4bn in 4Q24, compared to RMB10.7bn in 4Q23. Diluted earnings per share increased to RMB2.55 in 4Q24, compared to RMB0.71 in 4Q23.

Market consensus.

(Source: Bloomberg)

Allstate Corp (ALL US): Active management amid tariff impact

BUY Entry – 192 Target – 210 Stop Loss – 183

The Allstate Corporation provides property-liability insurance solutions. The Company sells private passenger automobile and homeowners insurance through independent and specialized brokers, as well as life insurance, annuity, and group pension products through agents. Allstate serves customers in the United States and Canada.

Increased concerns about a U.S. recession benefiting defensive sectors. Recent U.S. macroeconomic data shows that inflation remains high, while the labour market is beginning to cool, and consumer spending and confidence are declining. Trump’s tariff policy has triggered a global trade war, and the U.S. stance on the Russia-Ukraine issue has been questioned by its allies. With the concentration of negative factors, the market is averse to uncertainty, so major growth sectors have seen significant corrections, and funds have rotated to stronger defensive sectors.

Tariffs to benefit. Allstate Protection Auto Insurance continues to strengthen margins, with earned premiums rising 9.1% YoY, driven by rate increases. The auto combined ratio improved to 93.5 in 4Q24, reflecting higher premiums and better loss performance. Trump’s tariffs on steel and aluminium could further benefit Allstate by increasing vehicle prices, leading to higher insured values and premiums. Additionally, as consumers hold onto older vehicles longer, insurers may adjust rates to cover rising repair costs, further boosting Allstate’s profitability in the auto insurance sector.

Unlocking value. Allstate continues to optimize its portfolio by divesting non-core businesses and adjusting insurance pricing. The company announced estimated catastrophe losses of US$1.08bn for January, largely due to California wildfires. To streamline operations, Allstate has agreed to sell its Group Health business to Nationwide for US$1.25bn, marking another step in its plan to exit non-core segments. Combined with the earlier sale of Employer Voluntary Benefits, total expected proceeds from these divestitures will reach US$3.25bn, generating an estimated US$1bn financial book gain in 2025. Meanwhile, Allstate is actively adjusting insurance pricing to mitigate risk exposure and improve profitability. In California, homeowners insurance rates rose by an average of 34% in November, with another 30% increase for condo insurance planned in April. Similarly, Illinois homeowners saw about a 14% premium hike in February. These rate adjustments will help Allstate navigate increasing claims costs while bolstering its financial position.

4Q24 results. Revenue rose 11.3% YoY to US$16.51 billion, beating expectations by US$280 million. Non-GAAP earnings per share were US$7.67, beating expectations by US$1.39. The board of directors approved a quarterly common stock dividend of US$1.00, an increase of US$0.08 or 8.7% per share compared to the previous quarter. Additionally, they also authorised a US$1.5bn share repurchase program of outstanding common stock, which will remain in effect through 30 September 2026.

Market consensus

(Source: Bloomberg)

Philip Morris International Inc (PM US): Zyn-ergy in action

Philip Morris International Inc. operates as a tobacco company working to deliver a smoke-free future and evolving its portfolio for the long term to include products outside of the tobacco and nicotine sector. The Company offers cigarettes, e-vapor, and oral smoke-less products. Philip Morris International serves customers worldwide.

Potential sale of business. Philip Morris (PM) International’s decision to explore the sale of its U.S. cigar business aligns with its broader strategy to transition away from traditional tobacco products. By divesting this asset, the company can reallocate resources toward its growing smoke-free product portfolio, such as Zyn nicotine pouches and IQOS heated tobacco devices. This shift not only supports long-term revenue growth but also enhances PM’s positioning in the evolving nicotine market. The expected US$1bn sale proceeds could fund further innovation and expansion, accelerating its goal of achieving two-thirds of sales from smoke-free products by 2030.

Decline in smoking rates. With global smoking rates continuing to fall due to health concerns and regulatory pressures, PM’s pivot toward alternative nicotine products is a crucial move. Traditional cigarettes face declining demand, but the company’s strong performance in Zyn and IQOS demonstrates its ability to adapt to changing consumer preferences. By focusing on harm-reduction alternatives, PM ensures revenue stability despite a shrinking cigarette market. This proactive approach not only mitigates risks associated with declining smoking trends but also strengthens the company’s position as an industry leader.

FDA approved. The FDA’s authorization of Zyn nicotine pouches marks a major milestone for PM, validating its harm-reduction strategy and providing a competitive edge in the U.S. market. With official regulatory backing, PM can further promote Zyn as a safer alternative to traditional tobacco, attracting more adult smokers looking to switch. This approval also opens doors for expansion into other regions where similar regulatory acceptance could drive growth. As health-conscious consumers seek alternatives, PM is well-positioned to capitalize on the increasing demand for smokeless nicotine products.

4Q24 results. Revenue grew 7.3% YoY to US$9.71bn, beating estimates by US$270mn. Non-GAAP EPS was US$1.55, beating expectations by US$0.05. The company projected FY25 adjusted annual earnings per share in the range of US$7.04 to US$7.17, above analysts’ estimate of US$7.03. It also forecast ZYN shipments to the U.S. would rise by between 34% and 41% in 2025, while IQOS shipments would also see between 10% and 12% growth.

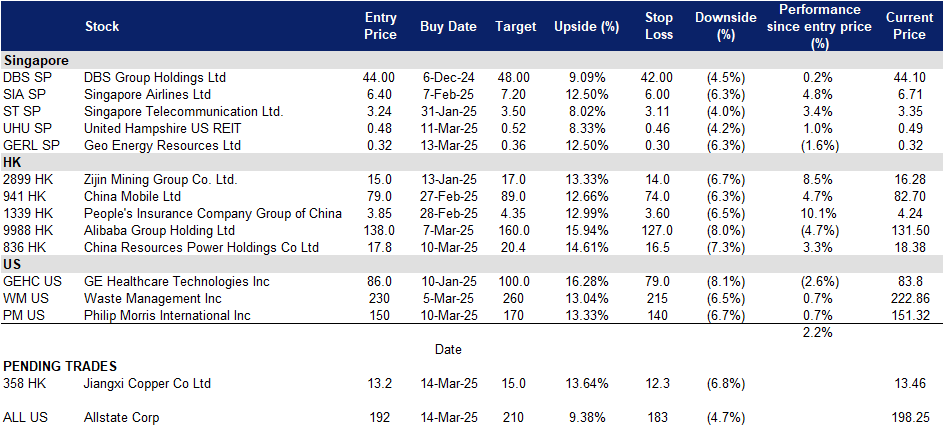

Trading Dashboard Update: Add Geo Energy Resources Ltd (GERL SP) at S$0.32.Cut loss on Oversea-Chinese Banking Corp Ltd (OCBC SP) at S$16.5, Prada SpA (1913 HK) at HK$60 and McDonald’s Corp (MCD US) at US$300.