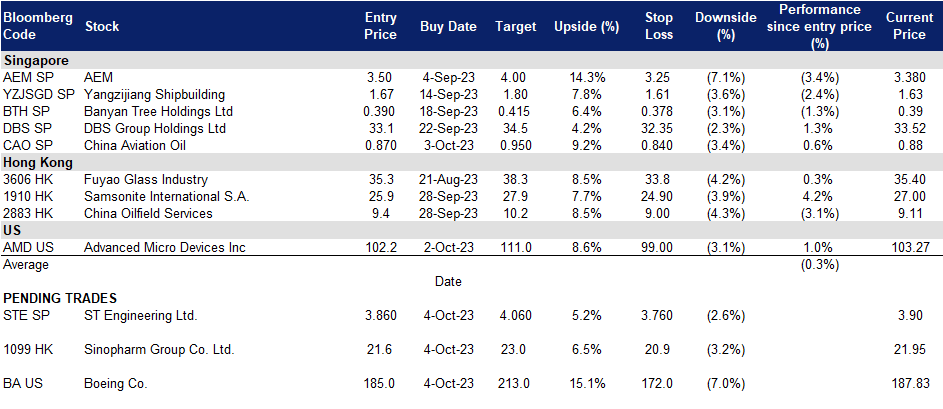

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

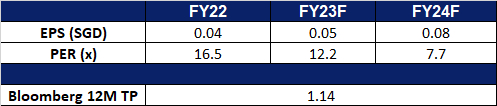

ST Engineering Ltd. (STE SP): Expanding services

- BUY Entry 3.86 – Target – 4.06 Stop Loss – 3.76

- ST Engineering Ltd is a global technology, defence, and engineering group. The Company uses technology and innovation to solve problems and improve lives through its diverse portfolio of businesses across the aerospace, smart city, defence, and public security segments. ST Engineering serves clients worldwide.

- Increasing MRO support. The company recently announced that its Commercial Aerospace business has secured multi-year contracts to provide Japan Airlines with its component Maintenance-By-the-Hour (MBH) solutions, strengthening a longstanding relationship with the airline in integrated MRO support. The company also recently secured a contract with Lion Air, setting in stone a 5-year contract to provide MRO solutions for Lion Air Group’s fleet of Boeing 737 MAX aircraft.

- New airframe MRO facility. The company recently announced that the company has begun to build its 4th airframe MRO facility in Singapore at a cost of around S$170mn, following the company’s announcement that it secured new MRO contracts with Japan Airlines and Lion Air. The new facility would include three maintenance bays designed to accommodate widebody aircraft, along with a fourth line equipped for both painting and maintenance tasks. ST Engineering anticipates that the initial maintenance line will become operational by mid-2025, with the entire facility being fully operational a year thereafter.

- 1H23 results review. 1H23 revenue increased by 13.9% to S$4.86bn, compared to S$4.27bn in 1H22. Net profit rose by 1.1% YoY to S$285.4mn, compared to S$282.4mn in 1H22. Diluted EPS rose to 8.95 SG cents, compared to 8.93 SG cents in 1H22.

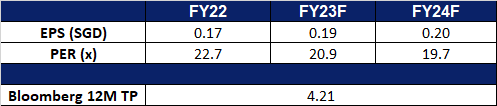

- Market consensus. FY23F/24F dividend yield is 4.14% and 4.24% respectively.

(Source: Bloomberg)

China Aviation Oil Singapore Corp. Ltd. (CAO SP): Tourism outshines amidst gloomy economic recovery

China Aviation Oil Singapore Corp. Ltd. (CAO SP): Tourism outshines amidst gloomy economic recovery

- RE-ITERATE BUY Entry 0.87 – Target – 0.95 Stop Loss – 0.84

- China Aviation Oil Singapore Corporation Limited supplies jet fuel to foreign and domestic airlines flying through China’s airports. The Company also trades in other oil products such as fuel oil, gas oil, crude oil, and petrochemical products, including physical and paper swaps, and futures trading.

- Hot tourism during the Golden Week holiday. According to the Ministry of Culture and Tourism, the number of domestic tourism trips during the Mid-Autumn Festival and National Day holiday is expected to reach 896 million, up 86% YoY, and revenue from domestic tourism is expected to be RMB782.5bn, up 138% year-on-year. During the eight-day holiday, the cultural tourism market in the Yangtze River Delta and Pearl River Delta regions such as Shanghai, Suzhou, Chengdu and other popular tourist cities is extremely hot, and the bookings of hotels and air tickets have increased at least 5 times over the same period last year.

- Air traffic to surge in Shanghai airports. Shanghai Pudong Airport and Hongqiao Airport are expected to handle 17,000 flights (including 11,000 flights in Pudong Airport and 6,000 flights in Hongqiao Airport), with an average daily flight takeoff and landing of 2,161 flights, an increase of 71.6% YoY. The passenger traffic is expected to be 2.602 mn (including 1.585 mn in Pudong Airport and 1.017 mn Hongqiao Airport), and the average daily passenger flow was 325,000 people, an increase of 131.7% YoY. Cities such as Guangzhou, Shenzhen, Beijing, Xi ‘an and Chengdu are expected to become popular travel destinations in China. Internationally, Thailand, Japan and South Korea are expected to be popular destinations. Flights from Shanghai to Northeast Asia, Southeast Asia, the Middle East and other regional directions will further increase.

- 1H23 results review. 1H23 revenue plunged by 32.4% to US$6.3bn. Gross profit plunged by 50.6% YoY to US$10.6mn. Total supply and trading volume decreased by 16.1% YoY to 9.5mn tonnes. Net profit decreased by 1.07% YoY to US$19.4mn.

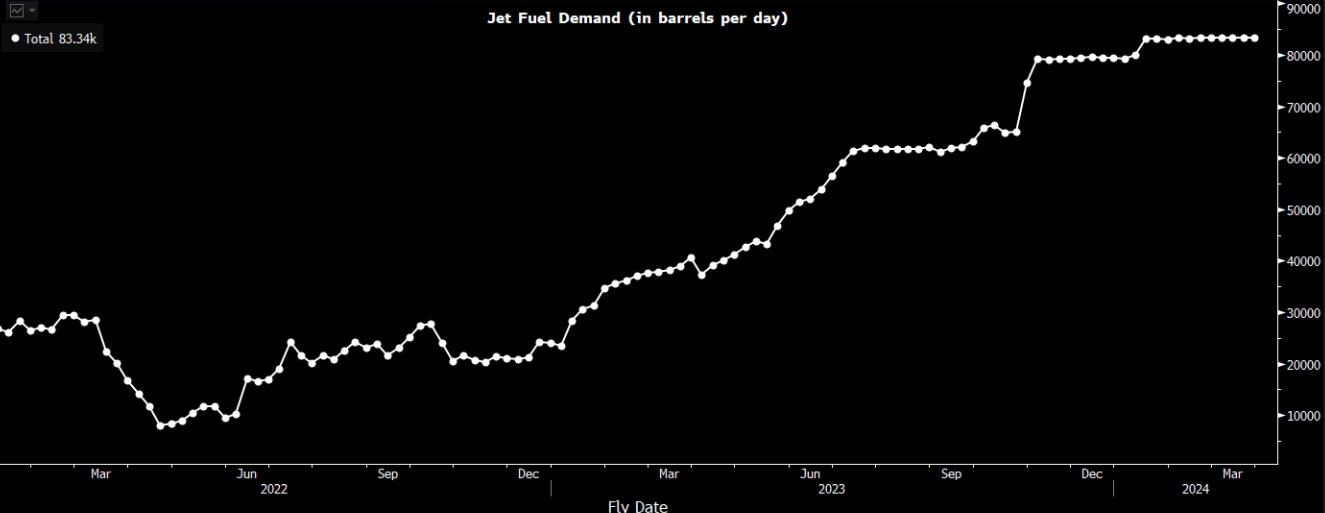

Scheduled jet fuel demand at Pudong International Airport

(Source: Bloomberg)

- Market consensus.

(Source: Bloomberg)

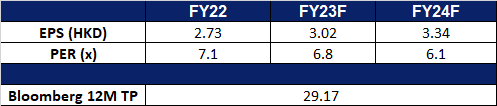

Sinopharm Group Co. Ltd. (1099 HK): Staying defensive

- BUY Entry – 21.6 Target – 23.0 Stop Loss – 20.9

- Sinopharm Group Co Ltd is a China-based company principally engaged in pharmaceutical and medical devices distribution business. The Company operates its business through four segments. Pharmaceutical Distribution segment is engaged in the distribution of pharmaceutical products to hospitals, other distributors, retail pharmacy stores and clinics. Medical Devices segment is engaged in the distribution of medical devices, as well as provides installation and maintenance services. Retail Pharmacy segment is engaged in the operation of chain pharmacy stores. Other Business segment is engaged in the distribution of laboratory supplies, manufacture and distribution of chemical reagents, production and sale of pharmaceutical products.

- Extensive partnerships. Just last quarter, Sinopharm entered into a partnership with Malaysia’s EW Group. Sinopharm can leverage the knowledge and skills of the EW Group in research, development, formulation, and manufacturing of nutraceuticals, skincare, cosmeceuticals, and therapeutic products. Concurrently, Sinopharm can utilize its extensive global reach and distribution network to support EW Group’s global aspirations. As part of this partnership, more than 1,000 unique products from EW Group will be available for sale and distribution through Sinopharm. Earlier this year, Sinopharm also entered into a partnership with Pfizer, where the company would help Pfizer seek approval to market 12 innovation drugs in China through 2025.

- mRNA vaccines show positive effectiveness. A recent study showed that three types mRNA vaccines VGPox 1-3 developed by Sinopharm were able to provide effective protection against monkeypox. In August, China saw a persistent increase in monkeypox infections, with a total of 501 reported cases, including five involving females. The number of monkeypox infections in June and July was 106 and 491 respectively. This increase in monkeypox cases within China is bound to drive sales for Sinopharm as well.

- 1H23 earnings. Revenue rose by 15.10% YoY to RMB301.0bn, compared to RMB261.5bn in 1H22. Net profit rose 10.67% YoY to RMB6.89bn, compared to RMB6.22bn in 1H22. Basic EPS rose by 11.9% YoY to RMB1.32, compared to RMB1.18 in 1H22.

- Market Consensus. FY23F/24F dividend yield is 4.43% and 4.94% respectively.

(Source: Bloomberg)

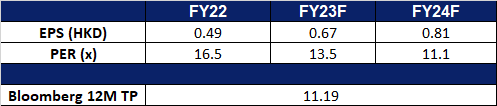

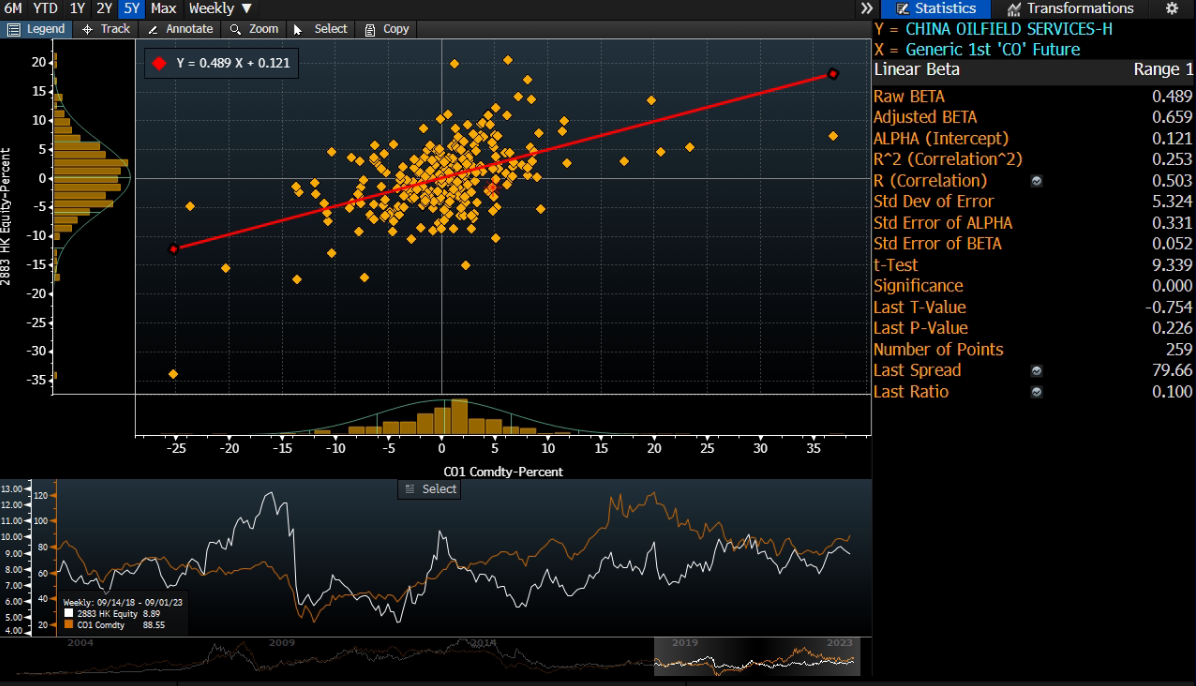

China Oilfield Services (2883 HK): Capturing Oil Demand

- RE-ITERATE BUY Entry – 9.40 Target – 10.20 Stop Loss – 9.00

- China Oilfield Services Limited is a comprehensive oilfield service provider. The Company mainly operates through four business segments. The Drilling Services segment is mainly engaged in the provision of oilfield drilling services. The Oil Field Technical Services segment is mainly engaged in the provision of oilfield technical services, including the logging, drilling fluids and directional drilling services. The Geophysical and Engineering Exploration Services segment is mainly engaged in the provision of seismic prospecting and engineering exploration services. The Marine Support Services segment is engaged in the transportation of supplies, including the delivery of crude oil, as well as refined oil and gas products. The Company mainly operates its businesses in domestic and overseas markets.

- New Drilling Rig Service Contracts. China Oilfield Services recently announced that its wholly owned subsidiary, COSL Drilling Europe, has entered into multiple drilling rig service agreements with two multinational oil firms in Norway, each with a set term and an option to extend for up to five years. The total value of the contracts with fixed terms is around 4.7 billion RMB.

- Demand for oil to outgrow supply. World oil demand is surging to record levels, with growth being driven by a number of factors, including a rebound in air travel, increased oil use in power generation, and strong demand from China’s petrochemical industry. Demand is expected to rise by 2.2 mb/d in 2023, reaching 102.2 mb/d. China is expected to account for more than 70% of this growth. Additionally, major oil-producing countries, including Saudi Arabia, also recently announced that they would be extending the voluntary oil cuts to year-end, putting more constraints on oil supply, and driving up oil prices in the near term. Saudi Arabia will be extending its voluntary oil cut of 1mn barrels per day to the end of 2023, and Moscos will be extending its voluntary oil cut of 300,000 barrels per day to end of 2023, with both countries to still review the cuts monthly. Consequently, the cost of oil is anticipated to increase within the market.

- 1H23 earnings. Revenue rose by 24.1% YoY to RMB18.9bn, compared to RMB15.2bn in 1H22. Net profit rose 31.0% YoY to RMB1.46bn, compared to RMB1.11bn in 1H22. Basic EPS rose by 21.1% YoY to RMB28.06, compared to RMB23.17 in 1H22.

- Market Consensus.

Share price and Brent crude oil price correlation

(Source: Bloomberg)

(Source: Bloomberg)

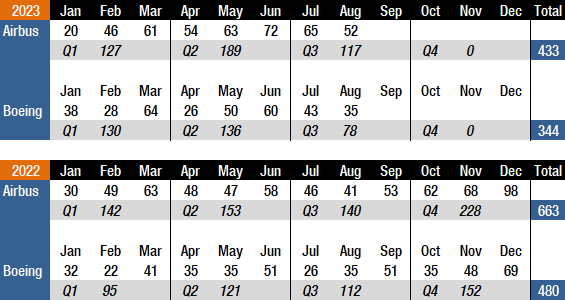

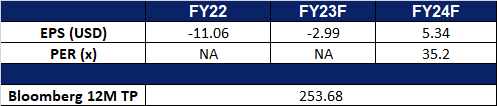

Boeing Co (BA US): Oversold

- BUY Entry – 103 Target – 111 Stop Loss – 99

- The Boeing Company, together with its subsidiaries, designs, develops, manufactures, sells, services, and supports commercial jetliners, military aircraft, satellites, missile defence, human space flight and launch systems, and services worldwide.

- Plan to ramp up 737 production. The company plans to ramp up its bestselling 737 production to a minimum of 57 per month by July 2025. The plan revives the company’s unmet target before the COVID period. Currently, the company targets to produce 42 737 jets per month by the end of 2023.

- Supply chain constraints led to August deliveries lower. The company delivered 35 aircraft in August, down from 43 in July, reaching the lowest level since April 2023. Management attributed the miss to supply chain disruptions which also occurred on Airbus. However, its CEO remained positive on the travel demand recovery which he believed was more resilient than expected, according to his interview on CNBC.

Airbus and Boeing aircraft deliveries

(Source: Flight Plan)

- Bad September hit again. The stock fell 14.44% last month, the worst-performing month in a year. Last September, the stock lost 24.44%. It only had two up days; the rest were down days last month. The plunge was similar to other tourism counters due to rising inflation concerns. Boeing is oversold and is expected to rebound in 4Q23.

- Market consensus.

(Source: Bloomberg)

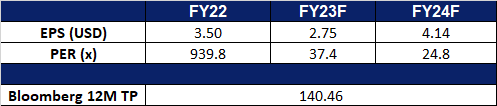

Advanced Micro Devices Inc (AMD US): Darkhorse

Advanced Micro Devices Inc (AMD US): Darkhorse

- RE-ITERATE BUY Entry – 103 Target – 111 Stop Loss – 99

- Advanced Micro Devices, Inc. (AMD) produces semiconductor products and devices. The Company offers products such as microprocessors, embedded microprocessors, chipsets, graphics, video and multimedia products and supplies it to third-party foundries, as well as provides assembling, testing, and packaging services. AMD serves customers worldwide.

- Microsoft‘s demand for AMD AI chips. Microsoft’s Chief Technology Officer, Kevin Scott’s, stated that AMD is strengthening its position in artificial intelligence (AI), an area currently dominated by Nvidia. There is currently a growing demand for powerful chips to support large language models like OpenAI’s ChatGPT. While Nvidia’s GPUs have been handling much of this workload, AMD announced plans to sample its MI300X chip tailored for AI models. Microsoft, a long-time partner of AMD, has a vested interest in diversifying high-powered chip options. Scott’s comments at the Code Conference also hinted at potential collaboration between Microsoft and AMD on AI-related silicon, which could impact Nvidia’s role in the AI chip market. These had led to an increase in AMD’s share price.

- First to ship AI chips for PC. AMD has been shipping its AI-enabled x86 CPU chip for PCs, the Ryzen 7040 Series, since May, with plans to expand AI technology to more desktop and laptop Ryzen CPUs next year. AMD integrated AI technology from the Xilinx Versal adaptive SoC into the Ryzen 7040, becoming the first company to deliver AI on-PC processing. While AMD has not provided specific AI benchmarks, it highlights the benefits of dedicated performance, improved security, and cost-effectiveness. The Ryzen AI platform includes software tools for running AI models on select laptops, optimising performance at low power. AMD’s quick integration of Xilinx assets demonstrates its commitment to AI.

- 2Q23 results. Revenue rose to US$5.36bn, down 18.2% YoY, beating expectations by US$40mn. Non-GAAP EPS beat estimates by US$0.01 at US$0.58.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Take profit on CrowdStrike (CRWD US) at US$171. Add China Aviation Oil (CAO SP) at S$0.87 and Advanced Micro Devices (AMD US) at US$102.2.