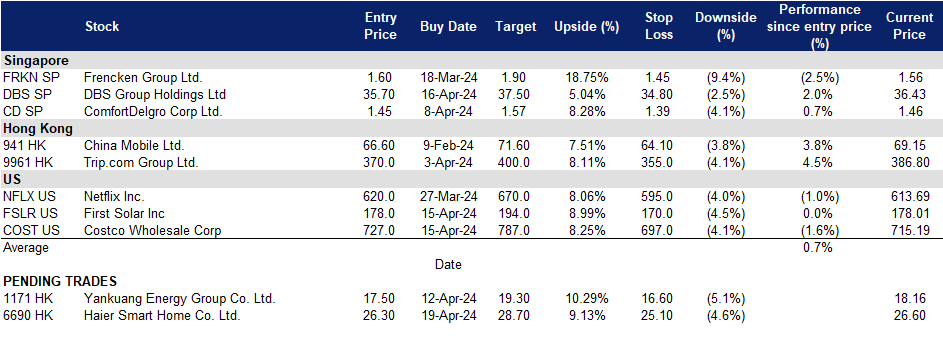

19 April 2024: Frencken Group Ltd. (FRKN SP), Haier Smart Home Co. Ltd. (6690 HK), Netflix Inc (NFLX US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

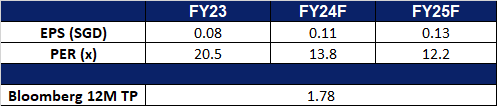

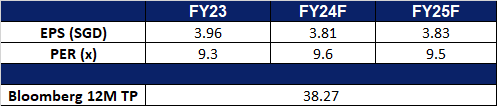

Frencken Group Ltd. (FRKN SP): Tailwinds from the barometer of semicon

- RE-ITERATE Entry – 1.60 Target– 1.90 Stop Loss – 1.45

- Frencken Group Limited (“Frencken”) is a Global Integrated Technology Solutions Company that is listed on the Main Board of the Singapore Exchange. They provide comprehensive Original Design, Original Equipment and Diversified Integrated Manufacturing solutions for world-class multinational companies in the analytical & life sciences, automotive, healthcare, industrial and semiconductor industries.

- Good 2Q24 guidance from TSMC. Taiwan Semiconductor Manufacturing Co. (TSMC) reported a 9% increase in net profit for the first quarter of 2024, surpassing market expectations amid a surge in demand for semiconductors utilized in artificial intelligence applications. TSMC also recently disclosed its fastest sales growth since 2022, indicating that the rising demand for chips driving AI development is starting to offset the effects of a slowdown in the smartphone market. Looking ahead to 2Q24, the company anticipates strong support from the robust demand for its cutting-edge 3-nanometer and 5-nanometer technologies, forecasting revenue to fall between $19.6bn and $20.4bn. Additionally, TSMC projects a more than twofold increase in revenue contribution from server AI processors this year. Despite challenges, the company maintains its expectation for revenue to grow by at least 20% this year as the broader semiconductor market rebounds. This positive trajectory is expected to extend to Frencken’s semiconductor segment, which represented approximately 40% of its Q3 revenue.

- Continued demand for AI Chips. Applied Materials, Frencken’s main customer, announced an earnings beat for FY23 and expects continued outperformance as customers ramp up next-generation chip technologies critical to AI and the Internet of Things. Their key customer, Taiwan Semiconductor Manufacturing Co., also delivered a good set of results for 1Q24 and provided a promising guidance for 2Q24, riding on a wave of global AI development. These strong demands for AI chips would translate to more revenue growth for Frencken.

- FY23 results review. FY23 revenue declined by 5.5% to $742.9mn, compared to $786.1mn in FY22. Net profit plunged 38.1% YoY to $32.0mn due to challenging business conditions for the technology sector, compared to $51.6mn in FY22. Gross profit margin contracted to 13.2% in FY23 from 15.1% in FY22, attributing it to lower revenue, inflationary cost pressures as well as increased depreciation expenses.

- Market Consensus

(Source: Bloomberg)

DBS Group Holdings Ltd (DBS SP): Increase shareholders returns

- RE-ITERATE BUY Entry – 35.7 Target– 37.5 Stop Loss – 34.8

- DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

- Bonus share issuance. On 19 April, DBS will pay out its Q4 final dividend amounting to 54 Singapore cents per share. On 30 April, DBS is expected to issue one bonus share for every 10 shares held and these shares will qualify for dividends from 1Q24. The increase in dividend payout and issuance of bonus shares is to increase capital returns to its shareholders.

- Expectations of monetary policy to remain unchanged. The Monetary Authority of Singapore (MAS) is expected to maintain its current monetary policy in the upcoming review. Despite inflation showing some volatility, core inflation remains above the central bank’s target. MAS may consider easing monetary settings in the second half of the year if inflation stabilizes. While inflation in Singapore remains elevated, forecasts suggest moderation throughout the year. Global central banks are cautiously adjusting interest rates, and MAS is likely to follow suit gradually, balancing growth and inflation concerns. Analysts suggest MAS may not rush to relax policy, considering Singapore’s role as a bellwether for global growth and the ongoing export-driven economic recovery. Policy easing, if any, is anticipated in October at the earliest, with MAS managing monetary policy through adjustments to the Singapore dollar’s exchange rate against its main trading partners. With the monetary policy expected to remain unchanged, DBS will continue to benefit from the high net interest margins for the coming quarters, allowing it to maintain its FY23 net interest income levels.

- New sustainability initiative. On 3 April, DBS Bank and Enterprise Singapore launched a programme to support local companies in becoming more sustainable. The initiative offers training, guidance, and financing options to SMEs and mid-cap companies, with around 100 expected to join the first cohort. Companies will receive support from sustainability specialists and can choose basic or intermediate training levels. By the end of the programme, participating firms should have a clear sustainability action plan. Enterprise Singapore will finance 70% of eligible activities per company until March 2026. The initiative aims to help businesses future-proof themselves, cut costs, and meet growing demand for sustainability.

- FY23 results review. FY23 revenue rose by 22.2% YoY to S$20.1bn, compared to S$16.5bn in FY22. Net profit increased 25.5% YoY to S$10.3bn, compared to S$8.19bn in FY22. Basic EPS rose to S$3.87 in FY23 compared to S$3.15 in FY22. FY23 total dividend amounted to S$1.92 per share.

- Market Consensus

(Source: Bloomberg)

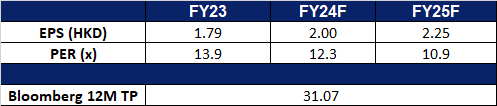

Haier Smart Home Co. Ltd. (6690 HK): Appliances trade-in program

- BUY Entry – 26.30 Target – 28.70 Stop Loss – 25.10

- Haier Smart Home Co., Ltd., formerly QINGDAO HAIER CO., LTD., is a China-based company principally engaged in the research, development, manufacture and sales of household electrical appliances. The Company’s main products include refrigerators/freezers, washing machines, air-conditioners, water heaters, kitchen appliances products, small home appliances and U-home smart home products. The Company also provides the customers with integrated smart home solutions. The Company is also involved in channel integration service business, including logistics, as well as the distribution of home appliances and other products. The Company distributes its products in domestic market and to overseas markets.

- Trade-in program for consumer products. The National Development and Reform Commission has unveiled a plan to drive large-scale equipment renewal and consumer goods trade-ins. With annual demand for equipment in crucial sectors projected to surpass 5 trillion yuan ($691 billion), the initiative aims to rejuvenate China’s equipment and consumer goods industries, as well as stimulate consumer spending appetites, bolster consumption recovery and inject new momentum into economic growth through comprehensive renewal initiatives. The central government of China will collaborate with local authorities to allocate funds to support consumers in trading in or upgrading their old home appliances for newer green, smart home appliances. This program is expected to boost demand for Haier’s products.

- Launch of new products in India. Haier India recently launched its new S800QT QLED TV in India. This new TV comes in 4 sizes and will be available for purchase at a starting price of Rs 38,990 across the offline and online channels which are available in the country. The company also recently launched a new range of super heavy-duty air conditions in India, which comes with the company’s Hexa Inverter and Supersonic cooling technologies, giving up to 20 times faster cooling experience than “conventional air conditioners. The new range of Haier Heavy-Duty air conditioners will be available at all leading stores with a starting price of Rs 49,990. These new products are expected to generate more sales for the company.

- Introduction HomeGPT. Recently at Shanghai’s Appliance & Electronics World Expo 2024, Haier introduced HomeGPT, the first large language model for smart homes. Haier’s new technologies can have conversations with users that seem almost natural and take orders. This new technology is likely to take smart home living to a new level in the future. This integration of AI with home appliances is bound to drive growth for the company in the future.

- FY23 earnings. Revenue rose by 7.3% YoY to RMB261.4bn in FY23, compared to RMB243.6bn in FY22. Net profit increased 13.6% YoY to RMB16.7bn in FY23, compared to RMB14.7bn in FY22. Basic EPS rose to RMB1.79 in FY23, compared to RMB1.58 in FY22.

- Market Consensus.

(Source: Bloomberg)

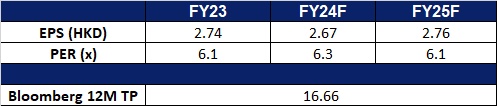

Yankuang Energy Group Co. Ltd. (1171 HK): Demand for coal surging

- RE-ITERATE BUY Entry – 17.50 Target – 19.30 Stop Loss – 16.60

- Yankuang Energy Group Co Ltd is a China-based international comprehensive energy company engaged in coal and coal chemical industry. The Company operates in five segments. The Coal Mining segment is engaged in underground and open-cut mining, preparation and sale of coal and potash mineral exploration. The Smart Logistics segment provides railway transportation services. The Electricity and Heating Supply segment provides electricity and related heat supply services. The Equipment Manufacturing segment is engaged in the manufacture of comprehensive coal mining and excavating equipment. The Chemical Products segment is engaged in the production and sale of chemical products. The coal products mainly include thermal coal, pulverized coal injection (PCI), and coking coal. The coal chemical products mainly include methanol, ethylene glycol, acetic acid, ethyl acetate and crude liquid wax, among others. The Company distributes products in the domestic market and to overseas markets.

- Power demand is driving record-high thermal coal imports. In March, China significantly increased its imports of seaborne thermal coal to levels not seen in three months, capitalizing on lower international prices to meet surging domestic power needs. With power consumption soaring by 11% in January and February compared to the same period in 2023, and power generation growing by 6.9% in 2023—outpacing the overall economic growth of 5.2%—the demand for thermal coal surged. As the world’s largest coal producer and importer, China witnessed arrivals of seaborne thermal coal reaching 29.7mn metric tons in March, marking a notable increase from 23.03mn tons in February and surpassing the 28.62mn tons recorded in March 2023.

- Increased coal-fired power capacity. Despite its pledge to “strictly control” the use of coal, China spearheaded a worldwide surge in new coal-fired power plants last year, surpassing levels not seen in nearly a decade. According to the annual survey from Global Energy Monitor (GEM), China alone contributed two-thirds of the newly added coal-fired power capacity, installing 47.4 gigawatts (GW) out of the global total of 69.5GW. Furthermore, China initiated the construction of an additional 70.2GW of coal-power capacity in 2023, accounting for 95% of global construction starts and marking the country’s swiftest pace of groundbreaking since 2015. This uptick in coal-fired power capacity is expected to sustain heightened demand for coal in the foreseeable future.

- China reinstates coal tariffs. At the start of 2024, China has reinstated tariffs on coal imports. The reinstated tariffs include a 6% levy on coal for electricity and heating and a 3% tariff on coking coal used in steelmaking. Russia, South Africa, Mongolia, and the United States will be impacted by these tariffs, while Indonesia and Australia remain exempt due to free trade agreements with China. The implementation of these tariffs is likely to drive up domestic coal production and demand as there is less competition from foreign coal companies. This allows domestic producers like Yankuang Energy to extend their competitive edge in the Chinese market.

- FY23 earnings. Revenue fell by 23.4% YoY to RMB118.4bn in FY23, compared to RMB154.6bn in FY22. Net profit fell 41.3% YoY to RMB23.0bn in FY23, compared to RMB39.1bn in FY22. Basic EPS fell to RMB2.39 in FY23, compared to RMB4.10 in FY22.

- Market Consensus.

(Source: Bloomberg)

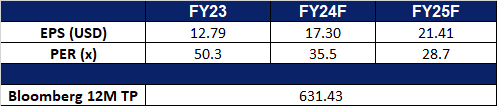

Netflix Inc (NFLX US): Signalling more price hikes

- RE-ITERATE BUY Entry – 620 Target – 670 Stop Loss – 595

- Netflix, Inc. operates as a subscription streaming service and production company. The Company offers a wide variety of TV shows, movies, anime, and documentaries on internet-connected devices. Netflix serves customers worldwide.

- Prices increasing once again. Netflix has warned investors and users of potential price hikes in 2024, aiming to reflect improvements and drive further investment in its service. Despite offering an ad tier at US$6.99 per month since 2022, uptake has been modest, with 23mn monthly active users reported. With over 260mn global subscribers, Netflix added 13.1mn in its recent fourth quarter, signalling satisfaction with current pricing. The company’s recent acquisition of WWE’s Raw for over US$5bn and plans to increase content investment suggest potential leverage for future price increases. While a specific timeline for hikes was not disclosed, Netflix’s pattern suggests it’s inevitable. While Netflix has not disclosed a specific timeline for price hikes, its historical pattern suggests they are inevitable. The company has experienced positive subscriber growth following its crackdown on password sharing and previous price increases. It is expected that price hikes will continue across countries as Netflix deems it has delivered sufficient additional entertainment value. Netflix Singapore recently announced a price hike across its tiers.

- Stepping into live sports action. Netflix is set to host a highly anticipated boxing match between Mike Tyson and Jake Paul, streaming exclusively on the platform on 20 July. This event marks Netflix’s ambitious venture into live sports and entertainment. Tyson, a former heavyweight champion known for his ferocity in the ring, will face off against Paul, a YouTuber-turned-fighter with a burgeoning boxing career. The match will take place at AT&T Stadium in Texas and signifies Netflix’s commitment to becoming a premier destination for at-home entertainment. This move follows Netflix’s recent acquisition of streaming rights to WWE’s “Raw” and highlights the platform’s growing presence in sports programming.

- 4Q23 earnings review. Revenue rose by 12.5% YoY to US$8.83bn, beating estimates by US$120mn. GAAP EPS was US$2.11, missing estimates by US$0.11. In 1Q24 revenue is expected to be US$9.24bn vs consensus of US$9.26bn, and EPS of US$4.49 vs US$4.14 consensus. Expect global average revenue per member (ARM) to be up YoY on a F/X neutral basis in Q1.

- Market consensus.

(Source: Bloomberg)

First Solar Inc (FSLR US): Next sector to benefit from the AI wave

- RE-ITERATE BUY Entry – 178 Target – 194 Stop Loss – 170

- First Solar, Inc. designs and manufactures solar modules. The Company uses a thin film semiconductor technology to manufacture electricity-producing solar modules.

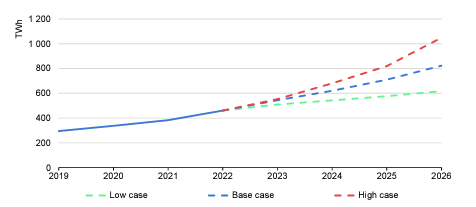

- Doubled electricity demand from data centres towards 2026. The 2024 IEA electricity report shows that global electricity demand from data centres, cryptocurrencies, and artificial intelligence (AI) is projected to nearly double by 2026, reaching between 620 and 1,050 terawatt-hours (TWh), with a base case of just over 800 TWh, up from 460 TWh in 2022. This surge in demand, driven by the expansion of digitalization, poses challenges and opportunities for various regions. In the United States, data centre electricity consumption is forecasted to rise rapidly, with Virginia’s data centre sector becoming a significant economic driver. China anticipates doubling its data centre electricity demand by 2030, while the European Union aims to bolster sustainable practices in data centres to align with decarbonization goals. In Ireland, data centres are expected to consume almost one-third of the country’s electricity by 2026. Efforts to enhance energy efficiency and regulatory measures are underway globally to mitigate the environmental impact of escalating electricity consumption in data centres. First Solar stands to benefit from the projected surge in electricity demand as solar energy can help these data centres to mitigate the environmental impact of escalating electricity consumption by providing renewable and sustainable power sources, thus contributing to the reduction of carbon emissions and promoting greener operations.

Global electricity demand from data centres, AI and cryptocurrencies

(Source: IEA electricity 2024 report)

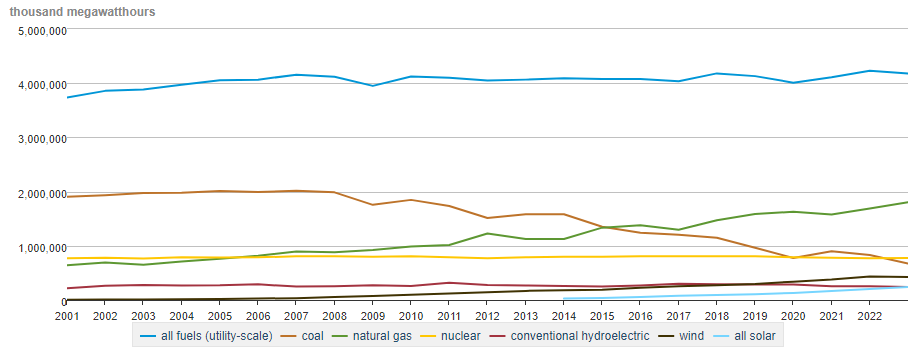

- Solar demand to grow. In the coming years, solar panel installations are predicted to substantially increase in the United States to meet the soaring electricity demand, driven particularly by data centres, electric vehicles, and heating/cooling systems. This surge comes as legacy power plants retire, and solar emerges as a cost-effective and rapid solution. Solar energy, being one of the fastest-growing energy sources in the US, is expected to expand significantly despite challenges like permitting delays and increased capital costs. In response to the growing demand, solar companies plan to boost their manufacturing capacity, buoyed by tax incentives under President Biden’s Inflation Reduction Act.

Net electricity generation in the United States

(Source: US Energy Information Administration)

- 4Q23 earnings review. Revenue was US$1.16bn, rising 16.0% YoY, missing expectations by US$160mn. GAAP earnings per share were US$3.25, beating expectations by US$0.13. The company issued FY24 guidance for revenue of US$4.4B to US$4.6B and EPS US$13 to US$14, compared to analyst consensus estimates of US$4.56B of revenue and EPS of US$13.26. FSLR also forecast full-year sales volumes of 15.6 to 16.3 GW, gross margin of US$2bn to US$2.1bn, and operating income of US$1.5bn to US$1.6bn on sales volume of 15.6 to 16.3 GW, which includes anticipated Section 45X tax credits of US$1bn to US$1.05bn and US$85mn to US$95mn of production start-up expense; year-end net cash balance is projected at US$900mn to US$1.2bn.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add Comfort Delgro Corp. Ltd. (CD SP) at S$1.45. Cut loss on China Aviation Oil Corp. Ltd. (CAO SP) at S$0.91 and Shandong Gold Mining Co. Ltd. (1787 HK) at HK$18.0.