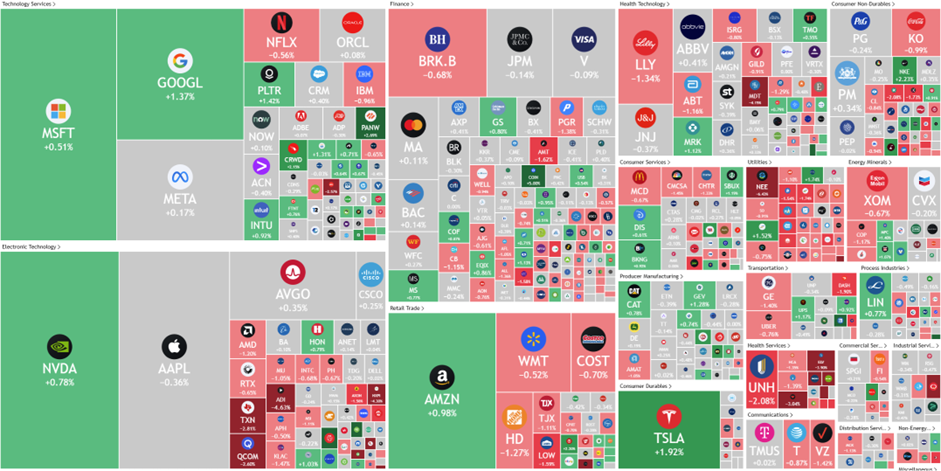

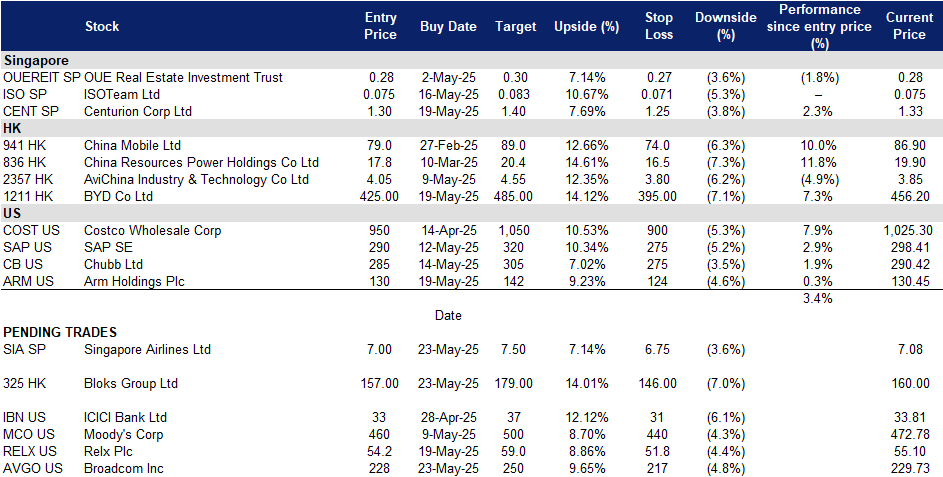

Singapore Airlines Ltd (SIA SP): Inbound travellers go GAGA

BUY Entry – 7.00 Target– 7.50 Stop Loss – 6.75

Singapore Airlines Limited provides air transportation, engineering, pilot training, air charter, and tour wholesaling services. The Company’s airline operation covers Asia, Europe, the Americas, South West Pacific, and Africa.

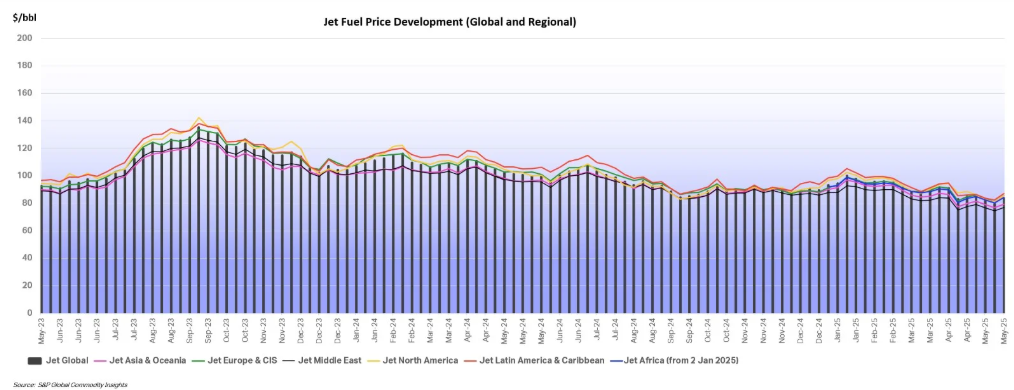

Jet fuel price to remain low. The jet fuel market is expected to maintain relatively low prices in 2025, continuing the trend from late 2024. The International Air Transport Association (IATA) projects an average jet fuel cost of US$87/bbl, or US$2.0714/gal, with total fuel expenditures expected to drop to US$248 billion nearly 5% lower than in 2024. While refinery disruptions could temporarily impact prices, overall stability is expected. Additionally, fuel costs are projected to comprise 26.4% of total airline expenses, down from 28.4% in 2024, contributing to improved profitability for airlines. As of the week ending 16 May 2025, the global average jet fuel price rose 5.1% compared to the week before to US$83.76/bbl.

Expected boost in tourism. Singapore is set to experience a surge in tourism following the recent release of BTS’ Jin music video shot in key locations such as the National Gallery, Gardens by the Bay, and Goldhill Plaza, in collaboration with the Singapore Tourism Board (STB). Leveraging the global popularity of K-pop, the video is expected to inspire more travellers to visit Singapore. Additionally, major events like Lady Gaga’s Asia-exclusive concert at the National Stadium, along with the Singapore Grand Prix, MICE events, and other sell-out concerts, will continue to drive demand in the hospitality and retail sectors. The STB’s initiatives, including partnerships with global brands like Wiggle Wiggle and Pop Mart International, further aim to attract visitors, with 2025 tourism receipts projected between S$29 billion and S$30.5 billion and arrivals expected to range from 17 million to 18.5 million. These developments will create significant opportunities for Singapore Airlines to capture increased passenger demand, especially from inbound international travellers.

Seasonality chart – SIA

(Source: Bloomberg)

Seasonal rise in travel. With the upcoming summer holidays, both inbound and outbound travel demand is anticipated to rise. This seasonal uptick in travel is likely to benefit Singapore Airlines by increasing passenger traffic, contributing to higher flight bookings and demand for its services during peak travel periods. The airline is well-positioned to capitalize on this increased travel activity, boosting its revenue and enhancing its global connectivity.

FY24 results review. Revenue increased 2.8% YoY to S$19.5bn, driven by resilient demand for air travel and cargo uplift during the year. It delivered record S$2.8bn in net profit, boosted by the one-off non-cash accounting gain of S$1.1bn from the Air India-Vistara merger. Proposed final dividend of S$0.30 per share for FY2024/25, resulting in a total dividend of S$0.40 per share for the year.

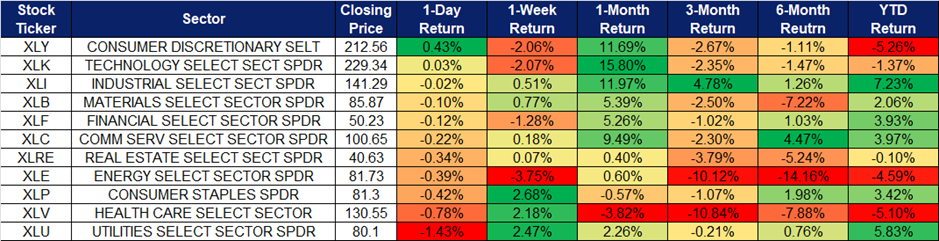

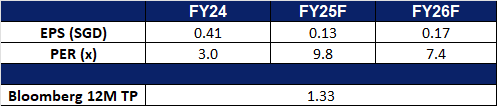

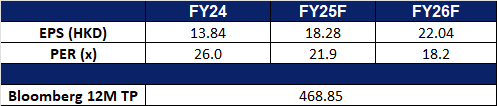

Market consensus

(Source: Bloomberg)

Centurion Corp Ltd (CENT SP): Continued strength amid global uncertainties

Centurion Corporation Limited provides purpose-built workers and student accommodation services. Centurion owns, develops, and manages quality and purpose-built workers accommodation assets. Centurion serves customers worldwide.

Expanding global footprint. As of 31 March 2025, Centurion operated 69,929 beds across 37 assets with AUM of S$2.6 billion. Revenue from PBWAs rose 15% to S$53.4 million, while PBSAs grew modestly by 2% to S$15 million. The group’s new Build-to-Rent asset in China began operations, with occupancy at 48% and expected to increase. Centurion is actively expanding its footprint, with dormitory redevelopments in Singapore and Malaysia, and PBSA developments underway in Australia. Despite occupancy softness in Malaysia and Australia, the company remains confident in sustaining performance through strategic management of rental rates and occupancy.

REIT listing exploration. Centurion is exploring a potential REIT structure comprising stabilized PBWA and PBSA assets in mature markets like Singapore, Malaysia, and the UK. This could unlock asset value, enhance capital recycling, and deliver stable income for shareholders via a potential dividend-in-specie.

1Q25 results review. Revenue increased 13% YoY to S$69.0 million from S$61.1 million in 1Q24, attributable to higher contributions from positive rental revisions across all PBSAs and PBWAs and strong financial occupancies in both Singapore and the United Kingdom, partially offset by lower occupancy in Malaysia and Australia assets.

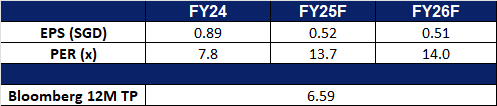

We have fundamental coverage with a BUY recommendation and a TP of S$1.38. Please read the full report here.

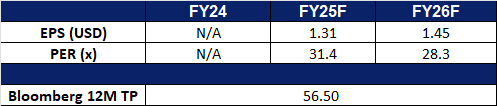

Market consensus

(Source: Bloomberg)

Bloks Group Ltd (325 HK): “Cheap” form of therapy

BUY Entry – 157 Target – 179 Stop Loss – 146

Bloks Group Ltd is an investment holding company primarily engaged in the design, development and sales of assembly toys. The Company’s main products include assembly character toys and brick-based toys. The Company’s self-developed intellectual properties (IPs) include Magic Blocks and Hero Infinity. The Company’s licensed IPs include Ultraman, TRANSFORMERS, Naruto, Marvel: Infinity Saga and Spidey and His Amazing Friends, Minions, Pokemon and others. The Company mainly conducts its business in the domestic market.

Rise of China’s “Goods Economy”. Bloks Group is well-positioned to capture the momentum of China’s expanding “Goods Economy” (Guzi Economy), driven by Gen Z and Millennials’ emotional and identity-driven consumption habits. Demand is surging for ACGNC (anime, comics, games, novels, cosplay)-themed collectibles, such as blind boxes, as younger consumers increasingly view these goods as expressions of self and lifestyle. By aligning its product development and branding with culturally resonant trends, and through further investments in R&D, Bloks is poised to grow in the trillion-yuan industry both domestically and globally, alongside peers like Pop Mart.

Scalable SKU driven growth strategy. Bloks Group’s FY24 sales surged 155.6% YoY to RMB 2,240.9mn from RMB 876.7mn, supported by a robust IP portfolio and SKU (stock keeping unit) expansion. With over 50 licensed IPs and strong in-house development, the company aims to launch 800 new SKUs in 2025. Its strategy centers on broadening demographic appeal, from children to adult collectors, while growing its international presence through an omnichannel distribution model and content-driven marketing. Bloks will continue to enhance R&D and manufacturing capabilities to deliver high-quality, culturally resonant, and competitively priced assembly character toys that appeal across age groups and geographies.

FY24 earnings. Revenue rose by 155.6% YoY to RMB2,240.9mn in FY24, compared to RMB876.7mn in FY23. Gross profit increased 184.1% from RMB414.9mn in FY23 to RMB1,178.8mn in FY24, primarily due to a 212.5% increase in gross profit from assembly character toy sales, which was partially offset by a 64.6% decrease in gross profit from brick-based toy sales. Loss for the year was RMB398.0mn in FY24, up by 91.8% YoY from the loss of RMB207.5mn in FY23.

BYD Co Ltd is a China-based company mainly engaged in the manufacture and sales of transportation equipment. The Company’s main businesses include automobile business mainly based on new energy vehicles, mobile phone components and assembly business, secondary rechargeable batteries and photovoltaic business. The Company’s passenger car brands include two major series of products, ‘Dynasty’ and ‘Ocean’. The Company conducts its business in the domestic market and overseas markets.

Expansion in the European market. BYD has announced plans to establish its European headquarters in Hungary, reinforcing its commitment to expanding in the region. As part of a strategic cooperation agreement signed with the Hungarian government on May 15, the company will relocate its European base from the Netherlands to Hungary. BYD will invest HUF 100 billion (€250 million) to set up a business and development centre in Budapest, with the Hungarian government contributing a HUF 20 billion grant. The initiative will launch with two key projects: one focused on integrating intelligent technologies into modern mobility solutions, and another aimed at advancing next-generation electromobility technologies. This move underscores BYD’s ongoing efforts to strengthen its presence in the European market.

Increasing popularity of BYD cars. BYD has recently achieved notable sales growth across multiple international markets, emerging as a top-selling brand in several countries. In Singapore, BYD became the best-selling car brand in early 2025, overtaking Toyota for the first time, according to government data—highlighting its growing appeal as a leading electric vehicle (EV) manufacturer. In April 2025, BYD also outperformed Tesla in key European markets, including Spain, Italy, France, the UK, and Germany. Across 14 European countries, BYD recorded sales of 11,123 units, significantly ahead of Tesla’s 6,253 units. In Australia, the BYD Sealion 7 surpassed the Tesla Model Y to become the country’s best-selling electric vehicle. This growing international market share underscores BYD’s rising popularity among consumers and reflects its successful strategy to accelerate global expansion in the EV segment.

Launch of the new BYD e7. BYD is set to officially launch its new all-electric sedan, the e7, this Saturday, targeting the shared mobility and taxi service market. Designed with commercial use in mind, the e7 features a long 2,820 mm wheelbase and a 100 kW (134 hp) electric motor, offering a top speed of 150 km/h. The vehicle will be available with two battery options—48 kWh and 57.6 kWh—providing CLTC ranges of up to 450 km and 520 km, respectively. With its spacious design and practical range, the BYD e7 is expected to attract strong demand from corporate and fleet customers, further supporting the company’s growth in the commercial EV segment.

1Q25 earnings. Operatingrevenue rose by 36.4% YoY to RMB170.4bn in 1Q25, compared to RMB124.9bn in 1Q24. Profit attributable to equity shareholders was RMB9.15bn in 1Q25, up by 100.4% YoY from RMB4.57bn in 1Q24. Basic earnings per share was RMB3.12 in 1Q25, compared to a basic earnings per share of RMB1.57 in 1Q24.

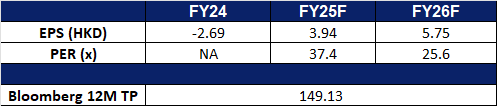

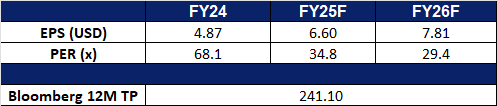

Market consensus.

(Source: Bloomberg)

Broadcom Inc. (AVGO US): Enabling scalable AI through NVLink integration

BUY Entry – 228 Target – 250 Stop Loss – 217

Broadcom Inc. designs, develops, and supplies semiconductor and infrastructure software solutions. The Company offers storage adapters, controllers, networking processors, motion control encoders, and optical sensors, as well as infrastructure and security software to modernize, optimize, and secure the complex hybrid environments. Broadcom serves customers worldwide.

Nvidia’s NVLink fusion opens new opportunities. Nvidia’s recent decision to open its NVLink Fusion interconnect to third parties will allow companies like Broadcom to integrate advanced chip-to-chip communication into AI systems without heavy internal R&D investment. This shift democratizes high-speed connectivity, accelerating adoption of complex multi-chip AI architectures. As a result, Broadcom stands to benefit from increased demand for its networking and interconnect solutions, reinforcing its role in enabling scalable AI infrastructure.

Breakthrough in co-packaged optics strengthens AI leadership. Broadcom’s third-generation 200G/lane co-packaged optics (CPO) platform delivers over 30% power savings and is backed by a strong ecosystem, making it a cornerstone for next-generation AI data center connectivity. With a roadmap extending to 400G/lane, Broadcom is poised to lead the transition to high-radix, power-efficient hyperscale networks, essential for meeting the exponential growth in AI workloads.

1Q25 results. Revenue rose 24.7% YoY to US$14.92bn from US$11.96bn in 1Q24. Non-GAAP EPS rose to US$1.60 from US$1.10 in 1Q24. Broadcom declared a quarterly dividend of $0.59 per share. For the second quarter it expects revenue of approximately US$14.9bn, a 19% increase from the prior year period.

RELX PLC is a global provider of information and analytics for professional and business customers across industries. The Group serves customers in more than 180 countries and has offices in about 40 countries.

AI-driven product innovation. Relx actively integrates artificial intelligence into its product lines, such as Elsevier’s ScienceDirect AI, which can quickly summarize millions of research articles, and Lexis+AI, which assists legal professionals with case summarization and document drafting, enhancing user efficiency.

Stable subscription revenue model. Approximately 54% of the company’s revenue comes from subscription services, covering fields such as academic publishing, legal information, and risk analytics, providing stable cash flow and a profit margin of up to 34%. The Legal and Science, Technical, and Medical (STM) divisions contribute over half of the group’s revenue, with only around 20% and 25% of revenue from one-time transactions in these divisions, respectively, while the remainder comes from long-term contracts or subscriptions.

Active stock buybacks. The company spent £1 billion on share buybacks in 2024 and plans to increase this to £1.5 billion in 2025.

FY24 results. Revenue rose 7% YoY to £9,434mn from £9,161mn in FY23. Adjusted EPS increased 5% to 120.1p (9% growth in constant currency) from 114.0p. RELX declared a semi-annual dividend of $0.5586 per share, payable on 25 June to shareholders of record as of 9 May. The company also announced a £1.5bn share buyback for 2025, exceeding market expectations, which ranged between £1.05bn and £1.4bn.