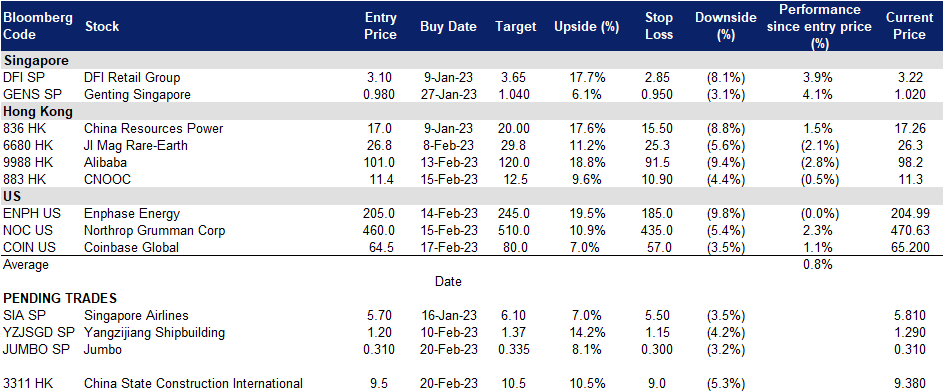

20 February 2023: Jumbo Group Ltd. (42R SP), China State Construction International Holdings Ltd (3311 HK)

Singapore Trading Ideas | Hong Kong Trading Ideas |United States Trading Ideas | Sector Performance | Trading Dashboard

Jumbo Group Ltd. (42R SP): Year of recovery

- Entry – 0.310 Target – 0.335 Stop Loss – 0.300

- Jumbo Group Ltd is a seafood restaurant group offering multiple dining concepts catering to all types of consumers. The Company offers restaurants in Singapore, China, and Japan.

- China’s re-opening play. China just recently announcement the re-opening of it borders to international visitors. Domestic and International tourists are expected to rise in the coming quarters. China is one of Jumbo Group key markets, and has 3 brands with 10 outlets located in China. The rise in international travel to China would definitely drive revenue for the company.

- Increase in tourism level in SG. With international borders re-opening, Singapore has become a global hot spot for tourists again. Singapore’s international visitor arrivals rose to 931,530 in January, setting a new record since the onset of the pandemic. Singapore’s tourism recovery is expected to reach back to pre-Covid level by 2024. Jumbo Group would be able to tap on this recovery as more tourists in Singapore would drive more revenue for the Group from its Singapore restaurants.

- Company Outlook. The company’s outlook is positive, as they are seeing an increase in consumer demand in its key market as more and more countries emerge from the pandemic and see a rise in tourism level. The harsh macroeconomic environment might pose some challenges due to high inflation and interest rates impacting consumer demand, but this is bound for a turnaround in the 2nd half of FY 23. This suggests that the company’s performance is likely to continue to improve in the near future.

- Updated market consensus of the EPS in FY23/24 is S$0.013/S$0.017 respectively. Bloomberg consensus average 12-month target price is S$0.35.

(Source: Bloomberg)

(Source: Bloomberg)

Genting Singapore Ltd (GENS SP): Tourism recovery

- RE-ITERATE Entry – 0.98 Target – 1.04 Stop Loss – 0.95

- Genting Singapore is best known for its award-winning flagship project Resorts World Sentosa, one of the largest fully integrated destination resorts in South East Asia. Genting Singapore is one of the constituent stocks of the FTSE Straits Times Index. The principal activities of Genting Singapore and its subsidiaries are in developing, managing and operating integrated resort destinations including gaming, hospitality, MICE, leisure and entertainment facilities.

- Arrivals to double. With Singapore’s tourism arrival figures expected to double from 6.3mn in 2022 to an estimated 13mn in 2023, mainly due to increasing travel demand from South-East Asia, Genting Singapore’s 2023 revenue is likely to see exponential growth in the new year. This revenue boost will likely translate to higher profits, which can then be used to continue fueling their expansion effort.

- RWS 2.0 expansion progress. RWS 2.0 project is on-going as planned, with both the construction of Minion Land at USS and, additions and upgrades to infrastructure facilities running smoothly. This expansion marks a shift in the company’s focus towards the affluent market. In 1Q23, it expects its remade Festive Hotel, turned boutique-style accomodation to reopen.

- Gross gaming revenue (GGR) recovery. Singapore’s GGR has been predicted to recover to more than 70% of pre-pandemic levels in 2023, boosted by China tourist arrivals. Pre-pandemic wise, GGR can usually be correlated to China tourist arrivals, with higher tourist arrivals leading to a higher GGR for Singapore. Therefore, with tourist arrival numbers from China recovering to near pre-pandemic levels, it is expected that GGR may make a similar recovery as well.

- Updated market consensus of the EPS growth in FY23/24 is 59.6%/10.1% YoY respectively, which translates to 20.5x/18.6x forward PE. Current PER is 64.5x. Bloomberg consensus average 12-month target price is S$0.98.

China State Construction International Holdings Ltd (3311 HK): Infrastructure expansion to uphold the economic recovery

- BUY Entry – 9.5 Target – 10.5 Stop Loss – 9.0

- China State Construction International Holdings Limited is an investment holding company principally engaged in construction contracts business. The Company is also engaged in infrastructure project investments, facade contracting business and infrastructure operation. The Company operates its business through four segments: Hong Kong, Mainland China, Macau and Overseas. Through its subsidiaries, the Company is also engaged in building construction, civil and foundation engineering works.

- Improving infrastructure. Following the relaxation of COVID-19 controls in December, the Chinese government has shifted focus to infrastructure investments to stimulate economic growth. Infrastructure projects across China have resumed after the Spring Festival holidays, with major projects totaling $7.4 billion already underway. The National Development and Reform Commission has approved 109 fixed-asset investment projects worth a combined 1.48 trillion yuan, covering transportation, energy, and water conservancy. In 2022, China’s fixed-asset investment increased by 5.1%, with infrastructure and manufacturing investments increasing by 9.4% and 9.1%, respectively. Experts predict that infrastructure investments will continue to play a leading role in boosting economic growth in 2023.

- Investment in digital infrastructure and technology. China is expected to see an increase in investment in 5G communications, distributed electricity grids, and computing power this year. Shenzhen, also known as China’s Silicon Valley, plans to add 10,000 5G base stations as part of its infrastructure expansion plan, which is in line with the Chinese government’s efforts to advance 5G infrastructure development in the country. Shenzhen aims to become the top city in mainland China in terms of internet speed by bolstering internet connectivity and digital economic activity in the city. Meanwhile, Henan province, which is home to the world’s largest iPhone factory, is investing $7.39 billion in a digital infrastructure expansion program to move its industries up the value chain. The program focuses on the development of advanced computing, satellite communications, integrated circuits, artificial intelligence, digital platforms, and 5G, following the State Council’s commitment to enhance China’s digital economy.

- Hong Kong’s need for public housing. The Hong Kong government plans to spend HK$26 billion on building temporary apartments in eight land plots to reduce the wait times for public housing. The light public housing units will be built using modular construction and will be between 13-31 square meters. The aim is to cut the waiting period for public housing to 4.5 years from 5.6 years. The government has rolled out a similar initiative called transitional housing.

- 3Q22 earnings. Revenue rose 38.9% YoY to HK$73,411,573,000, from HK$52,835,893,000 in 2021. The Group recorded an accumulated new contract value of approximately HK$125.74bn and a backlog of approximately HK$299.18bn.

- The updated market consensus of the EPS growth in FY22/23 is 15.8%/14.2% YoY respectively, which translates to 6.1x/5.3x forward PE. Current PER is 6.4x. FY23F/24F dividend yield is 4.9%/5.7% respectively. Bloomberg consensus average 12-month target price is HK$12.63.

(Source: Bloomberg)

CNOOC LTD (883 HK): Defensive oil

CNOOC LTD (883 HK): Defensive oil

- RE-ITERATE BUY Entry – 11.4 Target – 12.5 Stop Loss – 10.9

- CNOOC Ltd is a China-based investment holding company principally engaged in the exploration, production and sales of crude oil and natural gas. The Company operates three segments. Exploration and Production segment is engaged in conventional oil and gas business, shale oil and gas business, oil sands business and other unconventional oil and gas businesses. Trading segment is engaged in entrepot trade of crude oil in overseas areas. Corporate segment is engaged in headquarter management, assets management, research & development, and other businesses. The Company mainly operates businesses in China, Canada, the United Kingdom, Nigeria, and Brazil, among others.

- Growing oil demand and curb in oil supply. Organization of the Petroleum Exporting Countries (OPEC) Secretary General predicts oil demand will surpass pre-pandemic levels, reaching almost 102 million barrels a day and demand is projected to further rise to 110 million barrels per day by 2025. On the other hand, Russia, the world’s third-largest oil producer, recently announced plans to cut crude production in March by 500,000 barrels per day (about 5% of output) in response to western curbs imposed on its exports due to the Ukraine conflict. With demand projected to increase and supply to decrease, oil prices will go up.

- China demand reccovery. Demand for both oil and gas has recovered following the removal of COVID-19 restrictions in December. China’s state-owned oil refiners have resumed imports of Russian crude oil, attracted by its affordability. This demand would also contribute to the rise in oil prices with supply being limited. Furthermore, import demand may rise further if China decides to replenish its stockpiles.

- LNG bid. The company has issued a tender to buy liquefied natural gas (LNG) cargoes for delivery from June 2023 to June 2024. It had previously issued a tender in December 2022 for LNG cargoes to be delivered between February and December 2023 as well.

- New joint project. Shell has signed a Joint Study Agreement with CNOOC, Guangdong Provincial Development and Reform Commission, and ExxonMobil for a carbon capture and storage (CCS) hub project in Daya Bay, China. The four parties aim to explore the development of the CCS hub to capture up to 10 million tonnes of CO2 a year, which could be China’s first offshore large-scale CCS hub. The project could help reduce significant CO2 emissions of the Daya Bay region, and the parties will assess the technical solution, develop the business model, and work with the government to develop enabling policies for the project. China has an estimated 2,400 gigatonnes of carbon storage capacity and over 40 CCUS pilot projects with a total capacity of 3 million tons.

- FY22 earnings guidance. Net profit attributable to equity shareholders estimated to have increased by 99% to 104% YoY in 2022 as compared with the same period last year, reaching between RMB139.6bn and RMB143.6bn. Net profit is estimated to be between RMB138.3bn and RMB142.3bn a YoY increase of 103% to 109%.

- The updated market consensus of the EPS growth in FY23/24 is -9.0%/-7.3% YoY respectively, which translates to 3.7x/4.0x forward PE. Current PER is 4.1x. FY23F/24F dividend yield is 10.8%/9.7% respectively. Bloomberg consensus average 12-month target price is HK$14.39.

(Source: Bloomberg)

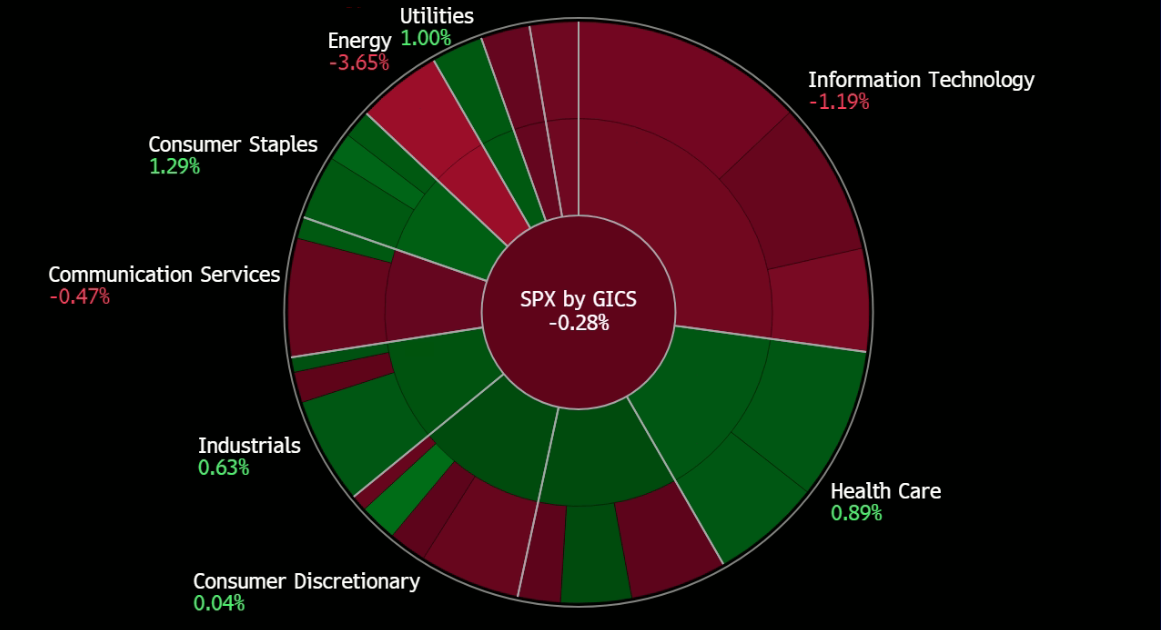

The United States market is closed today in observance of a public holiday, Presidents’ Day. The market will reopen on 21 February, Tuesday.

United States

News Feed |

1. Fed Officials Stress Need to Keep Raising Rates to Cool Prices |

3. US Producer Prices Exceed Forecast in Biggest Gain Since June |

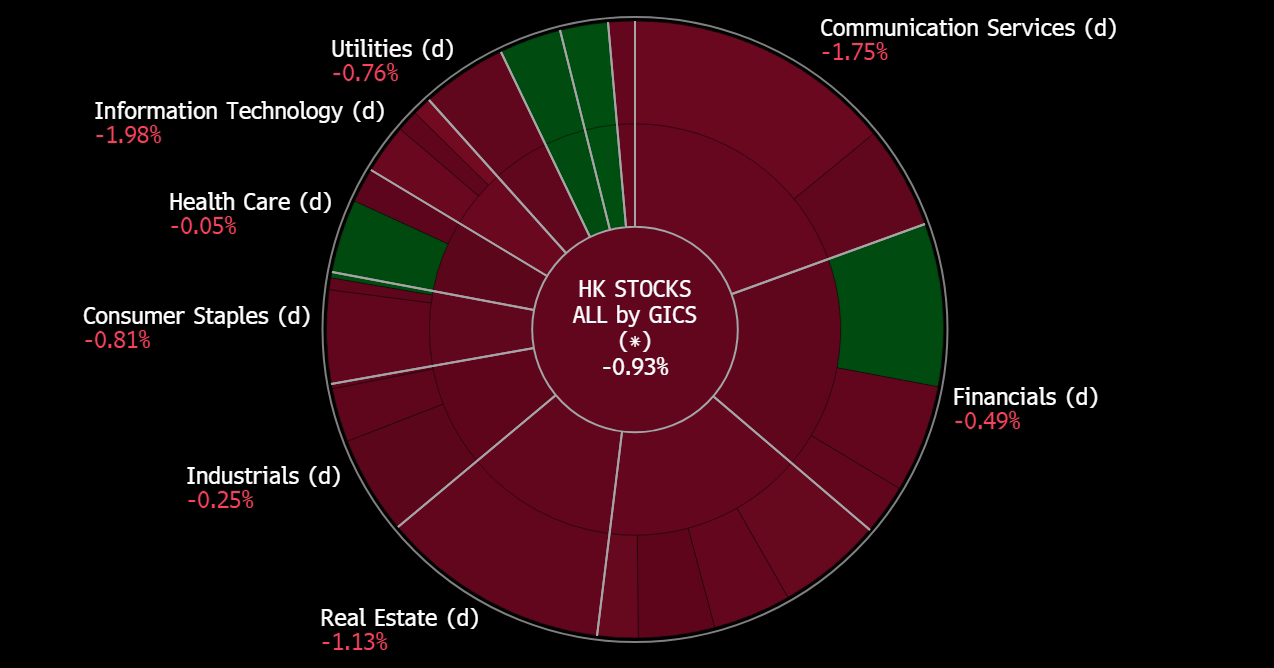

Hong Kong

Trading Dashboard Update: Cut loss on Sembcorp Marine (SMM SP) at S$0.13 and Occidental Petroleum (OXY US) at US$61.50. Add Coinbase Global (COIN US) at US$64.5