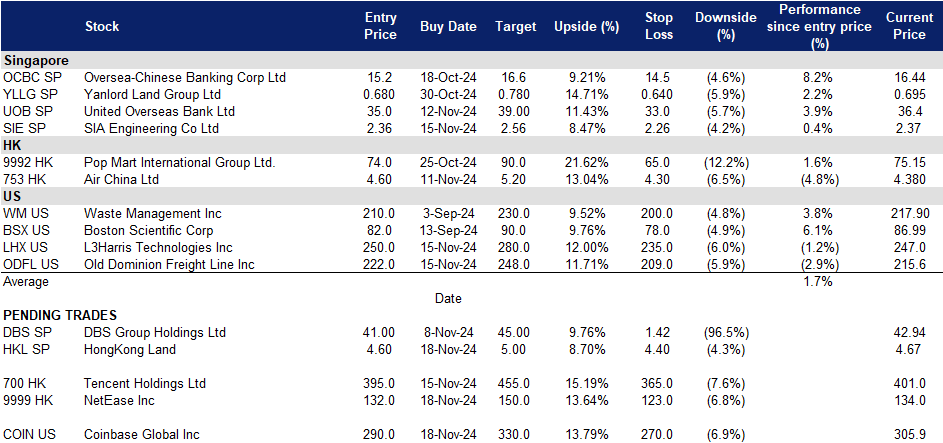

18 November 2024: HongKong Land (HKL SP), NetEase Inc. (9999 HK), Coinbase Global Inc (COIN US)

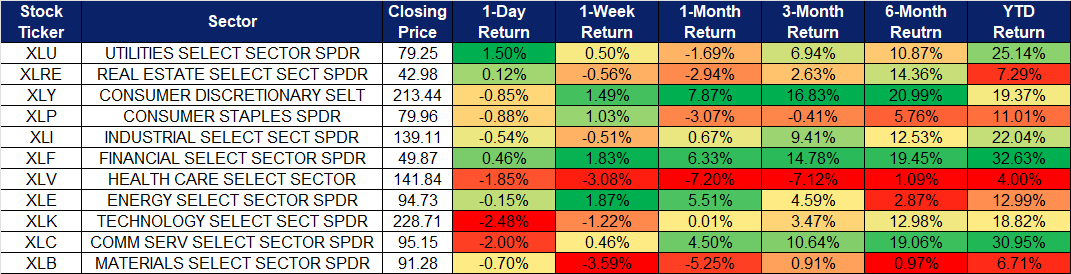

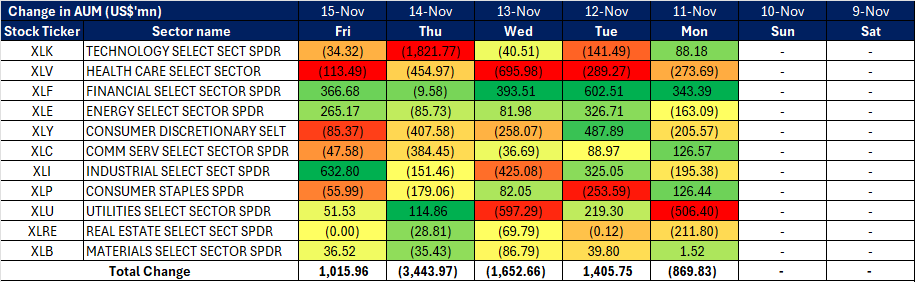

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

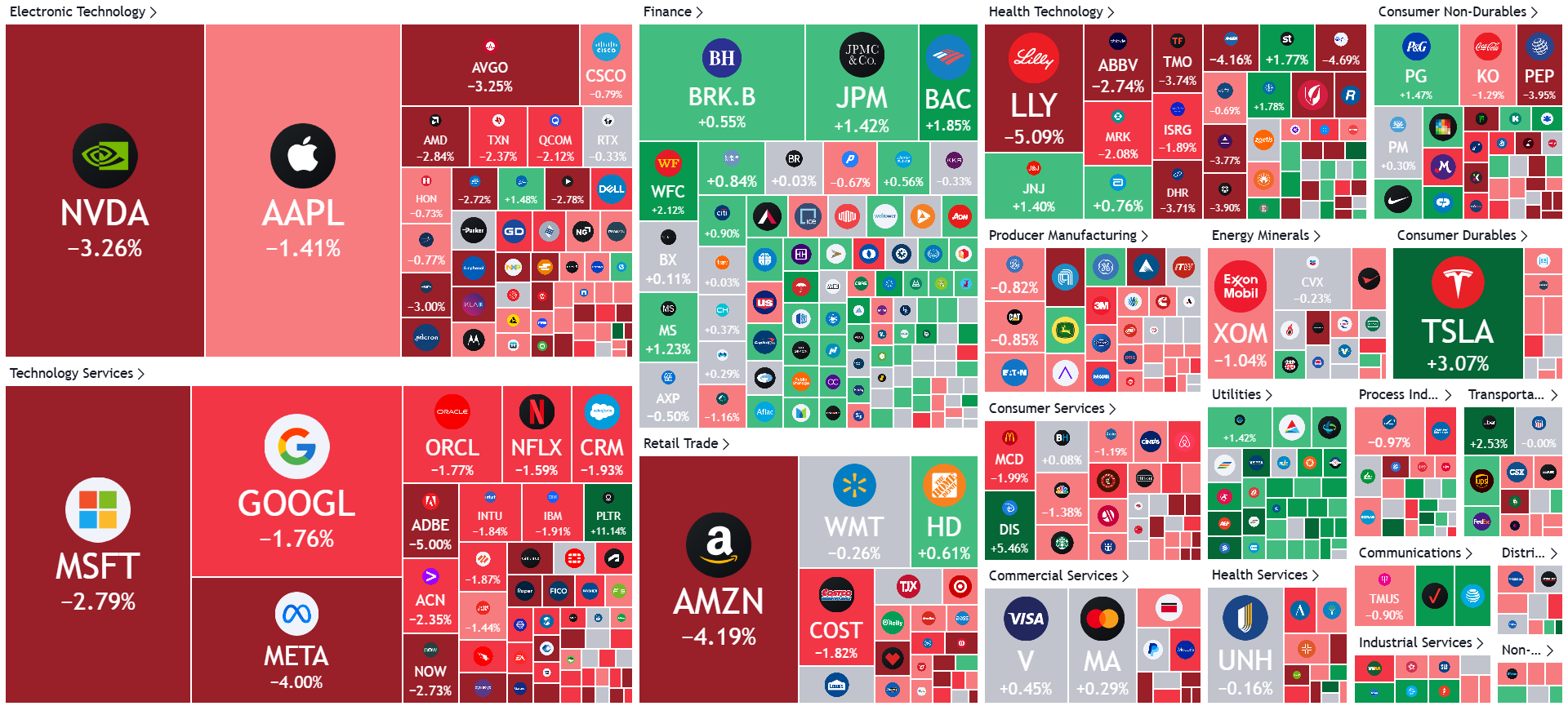

United States

Hong Kong

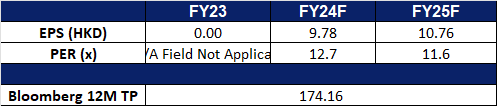

HongKong Land (HKL SP): Reshaping its portfolio

- BUY Entry – 4.6 Target– 5.0 Stop Loss – 4.4

- Hongkong Land is a major listed property investment, management and development group. The Group owns and manages more than 850,000 sq. m. of prime office and luxury retail property in key Asian cities, principally Hong Kong, Singapore, Beijing and Jakarta. The Group also has a number of high quality residential, commercial and mixed-use projects under development in cities across China and Southeast Asia, including a 43% interest in a 1.1 million sq. m. mixed-use project in West Bund, Shanghai.

- Profit recovery. Hongkong Land reported higher underlying profit for 3Q24 compared to the same period last year, driven by increased build-to-sell completions in China. However, contributions from investment properties declined slightly, mainly due to lower performance from its Hong Kong central portfolio, though cost management measures partially offset this drop. In the investment property segment, the company’s central office portfolio saw a vacancy rate of 7.6%, better than the overall market rate of 12.2%. Physical vacancy stood at 9.0%, affected by planned tenant movements. Rental reversions remained negative despite a slight increase in office inquiries. In Singapore, Hongkong Land’s office portfolio remained fully occupied with positive rental reversions. Vacancy rates dropped to 1.5% from 2.6% in 1H, and leasing momentum stayed strong, driven by demand for premium office space. The group’s contracted sales in Singapore totaled US$60mn for the period. Looking ahead, Hongkong Land’s shift towards focusing on investment properties in key Asian cities, improved liquidity and a solid balance sheet, Hongkong Land is well-positioned to capitalize on ongoing demand for premium office space and drive further value creation through its capital recycling plans.

- Pivoting to fund management. Hongkong Land announced a shift in its strategy to focus solely on investment properties in key Asian cities, exiting its residential and build-to-sell division. The company plans to raise US$6bn through divestments to support this new direction, leveraging its flagship mixed-use projects in Hong Kong, Singapore, and Shanghai. This strategic change follows the change of its CEO in April 2024, who previously led Mapletree Investments’ operations in Europe and the US. Part of the new strategy includes setting a goal to double underlying profit before interest, tax, and dividends by 2035, while growing its assets under management to US$100bn, including significant third-party capital. The company also plans to selectively inject assets into real estate investment trusts (REITs) and limit any single city’s contribution to no more than 40% of its profits. Additionally, it aims to recycle up to US$10bn in capital by 2035 to drive growth. The implementation of this strategy will be phased over several years, with progress measured in three stages. With the potential for significant capital recycling and a robust plan for profitability, Hongkong Land’s new direction appears promising, making it an attractive prospect for investors looking for stable returns in an evolving market.

- 3Q24 results review. HongKong Land reported higher underlying profit in 3Q24 compared to the same period in 2023, mainly driven by increased build-to-sell completions in China. However, total contributions from Investment Properties were slightly lower, primarily due to weaker performance in the Hong Kong central portfolio. This was partially offset by cost management measures that helped strengthen the Group’s financial position. As of 30 September 2024, net debt decreased to US$5.3bn from US$5.4bn, with a gearing ratio of 17%. Committed liquidity improved to US$3.2bn from US$3.0bn in June, and 67% of the Group’s debt is at fixed interest rates. Full-year 2024 underlying profits are expected to be significantly lower than the previous year. This decline is mainly due to a US$295mn non-cash provision in the Group’s China build-to-sell business, which was recognized in the first half of the year.

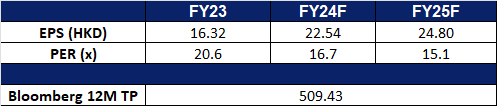

- Market Consensus.

(Source: Bloomberg)

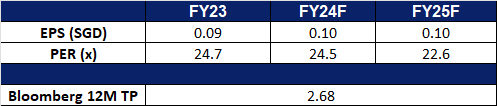

SIA Engineering Co Ltd (SIE SP): Maintain strength amidst flight recovery

- RE-ITERATE BUY Entry – 2.36 Target– 2.56 Stop Loss – 2.26

- SIA Engineering Co Ltd provides airframe and component overhaul services, line maintenance and technical ground handling services. The Company also manufactures aircraft cabin equipment, refurbishes aircraft galleys, repairs and overhauls hydromechanical aircraft equipment.

- Continued flight recovery. SIAEC saw total flights handled by the company’s line maintenance business reaching 95% of pre-COVID level as of September 2024. The increased flight activities contributed to an increased demand for aircraft maintenance, repair, and overhaul services. This recovery trend is expected to continue as more airlines ramp up flight schedules, alongside the arrival of the year-end peak travelling season, alongside more visa-free travel agreements between countries.

- Framework agreement with Xiamen Iport Group. SIAEC recently announced the signing of a non-binding Framework Agreement to explore a potential investment in Airport Aircraft Maintenance & Engineering (Fujian) (“Airport AME”), a subsidiary of IPORT Group that provides line maintenance and ground services at airports in Fujian, China. Under this Framework Agreement, both parties will work toward finalizing and signing definitive agreements, subject to regulatory requirements and necessary approvals. This partnership offers SIAEC opportunities for additional revenue sources over the long term.

- Subang base operational in 2H25. Base Maintenance Malaysia Sdn. Bhd. (BMM), a wholly owned subsidiary under SIAEC signed a lease agreement for Hangar facilities in Subang, Malaysia in December 2023. This adds 2 more hangar facilities with a combined capacity of six simultaneous aircraft checks with a lease term of 15 years to SIAEC’s portfolio. The hangars are expected to begin operations in the second half of 2025 and contribute to the group’s revenue growth.

- Interim dividend. The company declared an interim 1HFY25 dividend of 2 SG cents per share, no change from 1HFY24.

- 1H24 results review. SIA Engineering reported revenue of S$576.2mn for 1HFY24/25, up 12.1% YoY, compared to S$514.0mn in 1HFY23/24, as the company continues to benefit from the recovery of demand for aircraft MRO services. The company also reported a 1HFY24/25 operating profit of S$3.4mn, compared to an operating profit of S$0.1mn in 1HFY23/24. Group profit after tax came in at S$68.8mn in 1HFY24/25, up 16.0% YoY, compared to S$59.3mn in 1HFY23/24, largely attributed to a higher share of profits of JVs and Associated companies.

- We have fundamental coverage with a BUY recommendation and a TP of S$2.59. Please read the full report here.

- Market Consensus.

(Source: Bloomberg)

NetEase Inc. (9999 HK): Return of gaming titles

- BUY Entry – 132 Target – 150 Stop Loss – 123

- NetEase Inc is a China-based technology company. The Company operates through four business segments. The Online Game Service segment is engaged in developing and operating online game services that cover mobile games and personal computer (PC) games. The games include Westward Journey, Onmyoji series and others. The Youdao segment provides intelligent learning services. Its products and services include Online Courses, Youdao Dictionary, Youdao Dictionary Pen, Youdao Listening Treasure, Youdao Smart Learning Lamp, Youdao Translator King, Youdao Super Dictionary and others. The Cloud Music segment provides online music services and social entertainment services. Products offered by the Innovation and Others segment include Yanxuan, NetEase Live, advertising services, high-end email and other value-added services. The Company mainly operates its businesses in the domestic and overseas markets.

- Continued robust gaming portfolio. NetEase recently reintroduced two popular Blizzard games, World of Warcraft (WoW) and Hearthstone, to the Chinese market in August and September 2024, respectively. Their return followed a resolution of the dispute between Blizzard and NetEase, which arose after Blizzard ended its 14-year partnership with NetEase over intellectual property control. Under a new agreement, several Blizzard titles have been brought back to China, sparking renewed enthusiasm among the player community. The relaunch of these games has been met with significant engagement. World of Warcraft experienced a 50% increase in daily active players compared to pre-shutdown levels, while Hearthstone saw growth exceeding 150%. Furthermore, the company also recently announced more exciting titles in the making, including Destiny: Rising and MARVEL Mystic Mayhem, and new games, such as Marvel Rivals and Where Winds Meet, set for launch in December. These titles are expected to contribute to stronger gaming revenue for NetEase in 2025, reinforcing the company’s growth trajectory.

- Further approval of games. China’s gaming industry continues its recovery with the approval of 128 new game titles in October 2024, sustaining the steady approval pace seen throughout the year. Throughout 2024, China has consistently approved over 100 domestic titles monthly, with foreign game approvals occurring roughly every two months, signaling government support to rejuvenate the industry after regulatory restrictions in 2021. The regular flow of new approvals has significantly boosted market confidence, with industry projections estimating a compound annual growth rate (CAGR) of 7.63% from 2024 to 2029. The number of gamers in China reached a record high of over 674 million by the end of the first half of 2024. This consistent approval of new games, along with market recovery, is expected to drive continued growth in sales for companies across the sector.

- Partnership with Kakao Entertainment. NetEase has signed an agreement with Kakao Entertainment to bring new K-pop music exclusively to China. Starting October 24, 2024, NetEase Cloud Music will feature Kakao Entertainment’s latest releases exclusively for the first 30 days, coinciding with their global launch. Kakao Entertainment’s extensive portfolio spans music, online fiction, comics, film, and media. It is home to renowned artists such as IU and STAYC, labels like Starship Entertainment (representing Monsta X, IVE, and CRAVITY), and IST Entertainment (managing Apink, The Boyz, and VICTON). Additionally, Kakao Entertainment retains distribution rights to music by several internationally acclaimed acts. This collaboration marks a key milestone in NetEase Cloud Music’s efforts to expand its content copyright portfolio and strengthen its position in the competitive streaming market. NetEase anticipates deepening its partnership with Kakao Entertainment in the future, leveraging the growing popularity of K-pop in China. The exclusive access to new K-pop releases is expected to attract more fans to the platform, enhancing user engagement and driving subscriber growth.

- 3Q24 results review. Revenue fell by 3.9% YoY to RMB26.2bn in 3Q24, compared with RMB27.3bn in 3Q23. Net profit declined by 14.1% to RMB6.71bn in 3Q24, compared to RMB7.81bn in 3Q23. Basic earnings per share was RMB2.04 in 3Q24, compared to RMB2.44 in 3Q23, representing a 16.4% YoY increase.

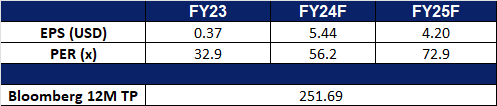

- Market consensus.

(Source: Bloomberg)

Tencent Holdings Ltd. (700 HK): Video gaming boom

- RE-ITERATE BUY Entry – 395 Target – 455 Stop Loss – 365

- Tencent Holdings Ltd is an investment holding company primarily engaged in the provision of value-added services (VAS), online advertising services, as well as FinTech and business services. The Company primarily operates through four segments. The VAS segment is mainly engaged in the provision of online games, video account live broadcast services, paid video membership services and other social network services. The Online Advertising segment is mainly engaged in media advertising, social and other advertising businesses. The FinTech and Business Services segment mainly provides commercial payment, FinTech and cloud services. The Others segment is principally engaged in the investment, production and distribution of films and television program for third parties, copyrights licensing, merchandise sales and various other activities.

- Strong profits in 3Q24 buoyed by growth in the video gaming segment. Tencent Holdings, the operator of China’s largest social media platform and the world’s top gaming company by revenue, surpassed analyst expectations with a 47% profit increase in Q3 2024, driven by renewed momentum in its gaming segment. The company reported a profit of 53.2 billion yuan for the quarter, up from 36.2 billion yuan a year earlier, beating the consensus estimate of 45.3 billion yuan. This growth was fueled by strong performance in its gaming business, where established titles maintained consistent engagement globally, complemented by contributions from newer games with long-term potential. Additionally, Q3 marked Tencent’s first full-quarter revenue from Dungeon & Fighter (DnF) Mobile, which launched in May and quickly gained popularity in China. Tencent’s mobile titles continued to perform well, and its August release, Black Myth: Wukong, a global success inspired by the Chinese classic Journey to the West, also bolstered Tencent’s investment portfolio, as the company holds a stake in the game’s developer.

- Further approval of games. China’s gaming industry continues its recovery with the approval of 128 new game titles in October 2024, sustaining the steady approval pace seen throughout the year. This latest batch includes Tencent-backed releases like Supercell’s Squad Busters and the eagerly awaited Goddess of Victory: Nikke, maintaining strong market momentum following the successful launch of Black Myth: Wukong. Throughout 2024, China has consistently approved over 100 domestic titles monthly, with foreign game approvals occurring roughly every two months, signaling government support to rejuvenate the industry after regulatory restrictions in 2021. The regular flow of new approvals has significantly boosted market confidence, with industry projections estimating a compound annual growth rate (CAGR) of 7.63% from 2024 to 2029. The number of gamers in China reached a record high of over 674 million by the end of the first half of 2024. This consistent approval of new games, along with market recovery, is expected to drive continued growth in sales for companies across the sector.

- Continued focused on new growth opportunities in AI. In its latest earnings release, Tencent outlined plans to pursue new growth avenues by advancing the adoption of its proprietary Hunyuan large language model across various industries and enhancing its AI infrastructure for enterprise clients. The company emphasized that it is already realizing tangible benefits from integrating AI across its products and operations, including in areas like marketing services and cloud computing, and remains committed to investing in AI-driven technologies, tools, and solutions to support users and partners. Tencent is also exploring new overseas opportunities in cloud computing, aiming to leverage global demand for AI technology to counteract increasing competition in China, where both established players and startups are engaged in intense price competition. These initiatives could pave the way for additional growth in the coming years.

- 3Q24 results review. Revenue increased 8% YoY to RMB167.2bn in 3Q24, compared with RMB154.6bn in 3Q23. Net profit rose 47% to RMB54.0bn in 3Q24, compared to RMB36.8bn in 3Q23. Basic earnings per share was RMB5.762 in 3Q24, compared to RMB3.828 in 3Q23, representing a 51% YoY increase.

- Market consensus.

(Source: Bloomberg)

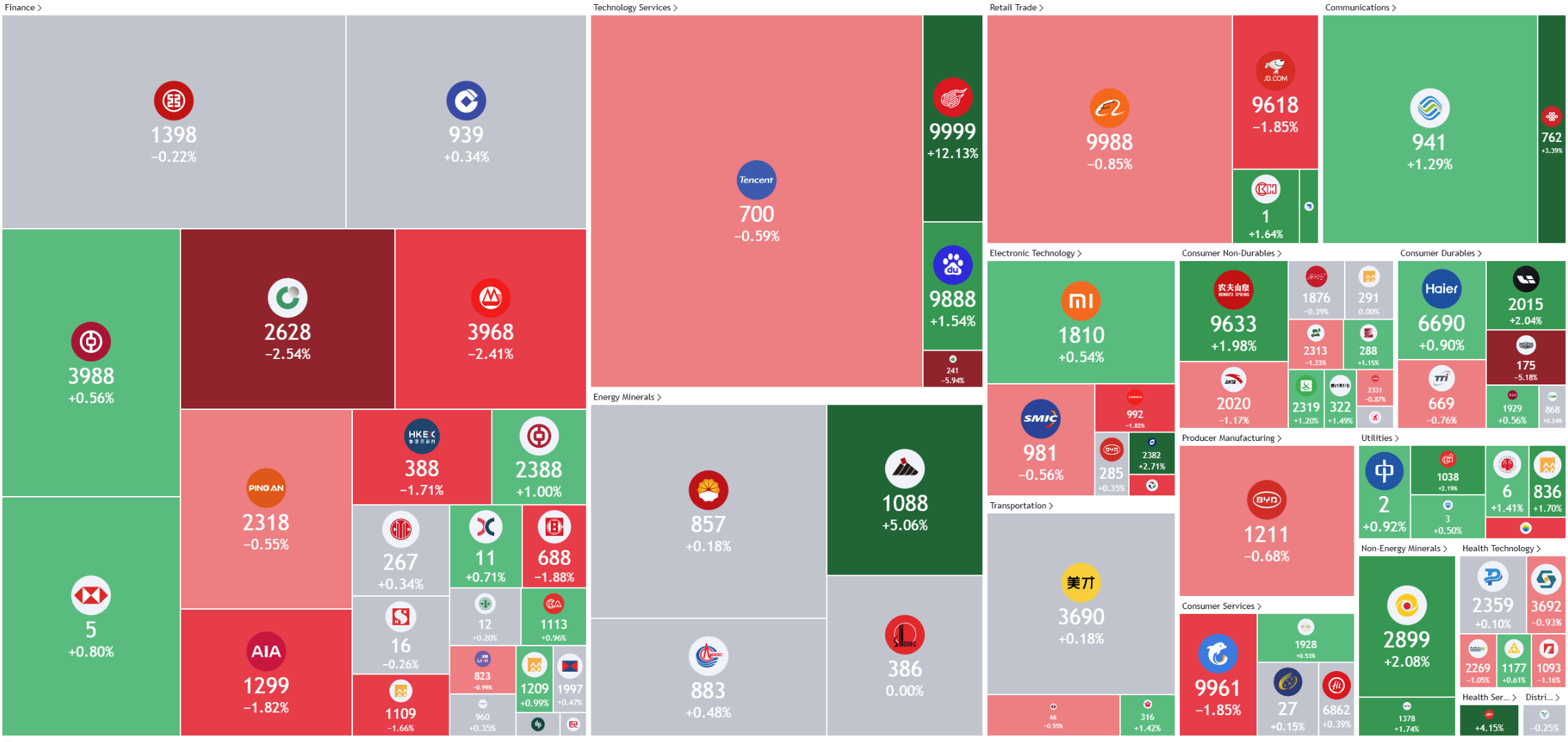

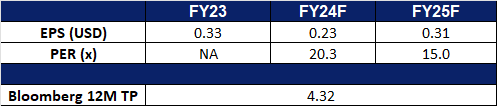

Coinbase Global Inc (COIN US): Bitcoin to US$100K

- BUY Entry – 290 Target – 330 Stop Loss – 270

- Coinbase provides financial infrastructure and technology for the crypto-economy in the United States and internationally. The company provides consumers with a primary financial account in the crypto economy; and a marketplace that provides institutional investors with a liquidity pool to trade crypto assets. It also provides technology and services that enable developers to build crypto products and securely accept crypto assets as payment.

- Trump supports cryptocurrencies. During his 2024 campaign, Trump expressed strong support for cryptocurrencies, attending the Bitcoin Conference and pledging to establish the United States as a global hub for digital currency. In a public speech, he proposed positioning the US as a Bitcoin superpower and suggested purchasing 2 million Bitcoins and 10 million Ethereum as federal reserve assets. Fox News reported that the Pennsylvania House of Representatives has introduced legislation to classify Bitcoin as a reserve asset. Additionally, market speculation suggests that Trump may remove Gary Gensler, the current SEC Chairman known for his strict regulatory stance on the cryptocurrency industry.

- Bitcoin hits all-time high. Following the US election, Bitcoin surged past its earlier trading range, hitting an all-time high of $93,000. Market analysts anticipate that Bitcoin will surpass $100,000 by year-end. Historical trends from previous Bitcoin halving cycles, which have shown 18-month price growth after each halving, support this outlook. With the most recent halving occurring on April 19, the upward trend is expected to continue into the coming year.

Bitcoin cycle after halving date

(Source: Bloomberg)

- 3Q24 results. Revenue increased 79.5% YoY to US$1.21 billion, missing expectations by US$40 million. GAAP earnings per share were $0.28, missing estimates of $0.42. The company’s revenue guidance for the subscription and services segment in the fourth quarter was US$505 million to US$580 million, compared with US$556 million in the third quarter.

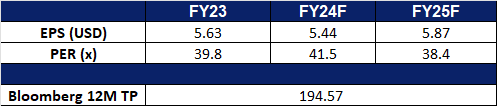

- Market consensus.

(Source: Bloomberg)

Old Dominion Freight Line Inc (ODFL US): Domestic logistics to benefit from Trump’s re-election

- RE-ITERATE BUY Entry – 222 Target – 248 Stop Loss – 209

- Old Dominion Freight Line, Inc. is an inter-regional and multi-regional motor carrier. The Company primarily transports less-than-truckload shipments of general commodities, such as consumer goods, textiles, and capital goods. Old Dominion Freight Line serves regional markets throughout the United States.

- Increased domestic trucking demand. President-elect Donald Trump’s proposed tariffs on imports, particularly from China, aim to encourage more domestic manufacturing and reduce reliance on foreign-made goods. In the short term, domestic manufacturers may frontload imports of commodities and components to avoid potential tariff hikes, likely causing temporary freight rates and domestic trucking rate increases due to demand spikes. Long term, once tariffs are enacted and US manufacturing scales up, demand for domestic logistics is expected to rise, benefiting carriers like Old Dominion Freight Line as they transport goods produced domestically across the US.

- Declining oil prices. Trump’s energy policies, focused on boosting US oil production and lowering gasoline costs, are anticipated to lead to a decline in oil prices. This drop would reduce operating costs for domestic trucking companies, benefiting their bottom lines. With the US as the world’s largest oil producer, increased production would further boost global oil supply, exerting downward pressure on prices. Additionally, Trump’s limited emphasis on climate change may delay a transition from diesel engines, potentially prolonging low fuel costs for companies like Old Dominion Freight Line, and supporting further improvements to its bottom lines.

- 3Q24 results. Revenue decreased by 3.3% YoY to US$1.47bn, missing expectations by US$20mn. GAAP earnings per share were US$1.43, beating expectations by US$0.01.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add SIA Engineering Co Ltd (SIE SP) at S$2.36, L3Harris Technologies Inc (LHX US) at US$250 and Old Dominion Freight Line Inc (ODFL US) at US$222. Cut loss on Hong Kong Exchanges and Clearing Ltd (388 HK) at HK$301.