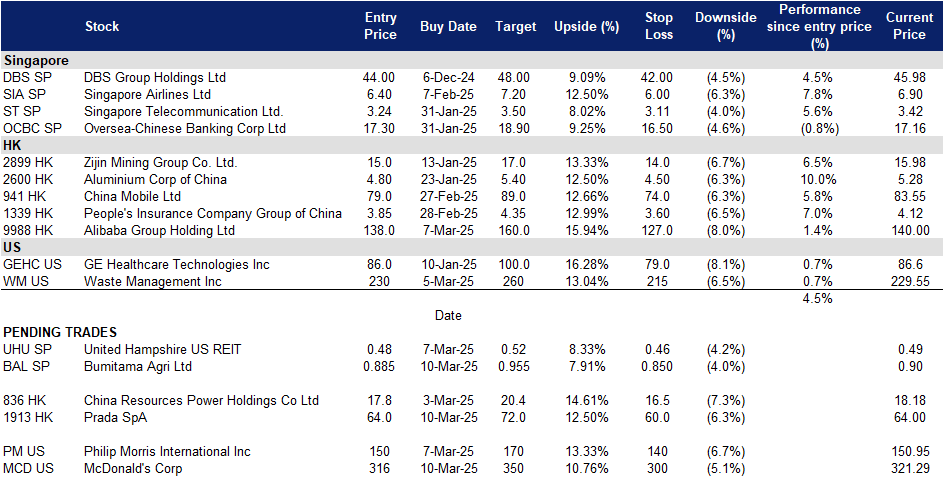

Bumitama Agri Ltd (BAL SP): Benefitting from high prices in the short-term

BUY Entry – 0.885 Target– 0.955 Stop Loss – 0.850

Bumitama Agri Ltd. produces CPO and PK, with its oil palm plantations located in Indonesia. The Company’s primary business activities are cultivating and harvesting our oil palm trees, processing FFB from its oil palm plantations, its plasma plantations and third parties into CPO and PK, and selling CPO and PK in Indonesia.

Fluctuations in palm oil prices. Malaysian palm oil futures have surged by nearly 1%, surpassing MYR 4,500 per tonne, marking a third consecutive rise. This increase follows reports of infestations in palm oil plantations across two Malaysian states, coupled with production disruptions caused by recent floods. Additionally, February inventories are projected to fall to their lowest levels in almost three years, further tightening supply. In India, the world’s largest importer, palm oil purchases are expected to pick up from March after unusually low imports in January and February, bolstering demand. In the near term, Indonesian palm oil output is expected to recover, but the government’s biodiesel blending plan may reduce overall supplies. Despite palm oil’s increasing prices, it is losing competitiveness against other vegetable oils like soybean oil, with prices likely to decline after the Ramadan period. While these fluctuations could impact short-term revenues, the anticipated recovery in Indonesian production and sustained biodiesel demand may benefit Bumitama Agri, positioning it for growth in the medium term.

Palm Oil Spot Price

(Source: Bloomberg)

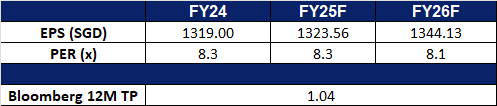

Continued growth. Bumitama Agri posted a 13.5% increase in net profit to 1.43tn rupiah (S$116.9mn) for 2H24, driven by higher average selling prices for palm products and a stronger Indonesian rupiah. Revenue also rose by 14.9%, totaling 9.13tn rupiah. While sales volumes for crude palm oil (CPO) and palm kernel (PK) products declined, the surge in CPO prices by 22.8% and PK prices by 70.8% boosted earnings. The company experienced a strong production quarter in Q4, with fresh fruit bunches (FFB) up 9% YoY. For FY24, net profit decreased by 6.6% to 2.29tn rupiah, and revenue grew 8.3% to 16.73tn rupiah. Bumitama anticipates strong biodiesel demand and seasonal factors will keep palm oil prices high in 1H25, despite challenges like adverse weather conditions and low seasonal production. Looking ahead, we anticipate continued resilience in Bumitama’s top lines as it efficiently navigate the fluctuating palm oil prices and seasonal production.

2H24 results review. Revenue increased 14.9% YoY to 9.13tn rupiah from 7.95tn rupiah. Net profit rose 13.5% to 1.43tn rupiah (S$116.9mn) for 2H24, above the 1.26tn rupiah in 2H23, translating to EPS of 825 rupiah in 2H24 from 727 rupiah in the period before.

Market Consensus.

(Source: Bloomberg)

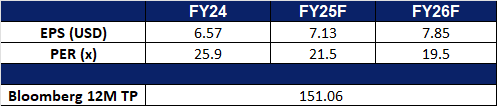

United Hampshire US REIT (UHU SP): Continued growth and expansion

United Hampshire US REIT operates as a real estate investment trust. The Company owns and operates shopping, storage, grocery, and necessity-based retail properties.

Favorable interest rate environment. The Federal Reserve cut interest rates by 25bps in December 2024, bringing the target range to 4.25% to 4.50%. Lower borrowing costs are expected to enhance United Hampshire US REIT’s financial flexibility and support growth. Projections for the Fed funds rate indicate a range of 3.50% to 3.75% by the end of 2025 and 3.25% to 3.50% by the end of 2026.

Strategic divestments. United Hampshire US REIT successfully divested properties, including Lowe’s and Sam’s Club in 2H24 and Supermarket at Albany in January 2025, at over 4% above valuation, demonstrating strong capital recycling efforts.

Strong demand for grocery-anchored strip centers amid limited new supply. Grocery-anchored retail properties remain highly resilient, with grocery store foot traffic increasing 12% from 2019 to 2024, according to Green Street. Service-based tenants, such as coffee shops, salons, and medical centers, further boost footfall, reinforcing the sector’s long-term stability. Hybrid work arrangements have also shifted consumer behavior, increasing demand for localized shopping experiences. Market rent growth for strip centers remained above historical averages in 2024, with a projected 3% annual growth from 2025 to 2029. Investment activity underscores confidence in the sector, Blackstone made its largest retail investment since 2011, acquiring 90 shopping centers for US$4bn, while CBRE expects US$10bn in open-air retail transactions in 2025. Despite strong demand, new strip mall construction remains constrained due to high costs, requiring a 65% rent increase to justify development. This gives existing landlords, including UHU REIT, strong pricing power to negotiate rent increases, securing long-term income growth. With a 97.5% committed occupancy rate and WALE of 8.1 years, UHU REIT is well-positioned to capitalize on these market dynamics.

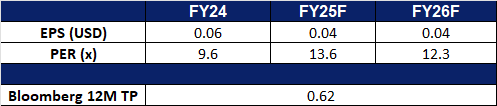

2H24 results review. Revenue increased 0.4% YoY to US$36.4mn, while net property income dipped 1.6% to US$24.4mn, mainly due to divestments and higher property expenses. DPU declined 4.2% to 2.05 US cents, reflecting higher finance costs.

We have fundamental coverage with a BUY recommendation and a TP of S$0.60. Please read the full report here.

Market Consensus.

(Source: Bloomberg)

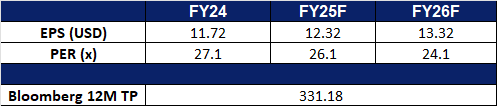

Prada SpA (1913 HK): An outlier of the luxury market

BUY Entry – 64 Target – 72 Stop Loss – 60

Prada SpA is an Italy-based company engaged in fashion industry. The Company is a parent of the Prada Group. The Company, along with its subsidiaries, is engaged in the design, production and distribution of leather goods, handbags, clothing, eyewear, fragrances, footwear and accessories. Prada SpA manufactures jackets, trousers, skirts, dresses, sweaters, blouses, as well as perfumes and watches, among others. The Company trades its products through several brands, such as Prada, Miu Miu, The Church and The Car Shoe. Prada SpA operates in approximately 70 countries through directly operated stores, franchise operated stores, a network of selected multi-brand stores and department stores. Prada Spa operates through a numerous subsidiaries, including Artisans Shoes Srl, Angelo Marchesi Srl, Prada Far East BV, Tannerie Megisserie Hervy SAS and Prada SA, among others.

Outperforming competitors. Prada SpA saw a 17% revenue increase in 2024, exceeding analyst expectations, driven by the rising popularity of its Miu Miu brand among young affluent shoppers. Miu Miu’s retail sales surged 84% in Q4, fuelled by the demand for items like Arcadie handbags and cashmere cardigans. Prada outpaced luxury competitors such as Kering and LVMH, with strong growth among Gen Z consumers. Regionally, Asia Pacific (including China) grew by 13%, Japan experienced a 46% surge, while the Americas showed slower growth. Leadership changes, including Silvia Onofri taking over Miu Miu, further solidified the brand’s success. With a 15% overall revenue growth to €5.43 billion and a 25% rise in net profit, Prada’s performance remains robust. Miu Miu’s 93% sales increase and significant gains across regions, especially in Japan and the Middle East, reinforce the company’s positive outlook. Given its strong brand momentum, regional expansion, and investor confidence, Prada is well-positioned for continued growth and success in 2025.

Potential acquisition. Prada is reportedly nearing a deal to acquire Versace from Capri Holdings for nearly €1.5 billion (US$1.6 billion). The deal could be finalized by March 2025, as discussions progress following a smooth due diligence process. Prada was given preferential access to Versace’s financial data after Capri announced the sale. Capri acquired Versace in 2018 for €1.83 billion, including debt. Other fashion companies have also shown interest in purchasing Versace. Should the acquisition go through, Prada’s purchase of Versace would further solidify its position as a key player in the luxury market, expanding its portfolio and enhancing its competitive edge against other global luxury giants. This strategic move could open new growth opportunities, particularly in enhancing its presence in high-end fashion, and boosting global brand recognition.

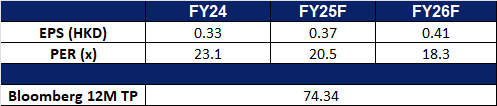

FY24 results review. Revenue increased 17.0% YoY to €5,431.6mn in FY24, compared with €4,726.4mn in FY23. Retail net sales of the Prada brand increased by 4.2% and Miu Miu by 93.2%, at constant exchange rates. Group net income rose by 25.0% YoY to €838.9mn in FY24, compared to €671.0mn in FY23. Proposed dividend distribution of €0.164 per share

Market consensus.

(Source: Bloomberg)

Alibaba Group Holdings Ltd. (9988 HK): Driving China’s digital future

Alibaba Group Holding Ltd provides technology infrastructure and marketing platforms. The Company operates through seven segments. China Commerce segment includes China retail commerce businesses such as Taobao, Tmall and Freshippo, among others, and wholesale business. International Commerce segment includes international retail and wholesale commerce businesses such as Lazada and AliExpress. Local Consumer Services segment includes location-based businesses such as Ele.me, Amap, Fliggy and others. Cainiao segment includes domestic and international one-stop-shop logistics services and supply chain management solutions. Cloud segment provides public and hybrid cloud services like Alibaba Cloud and DingTalk for domestic and foreign enterprises. Digital Media and Entertainment segment includes Youku, Quark and Alibaba Pictures, other content and distribution platforms and online games business. Innovation Initiatives and Others segment include Damo Academy, Tmall Genie and others.

Strong government support. At the recent National People’s Congress, China announced a 10% increase in science and technology spending, allocating RMB398bn (US$55bn). The government aims to foster AI model applications, quantum computing, and 6G technologies, alongside publishing an AI education White Paper to expand its tech talent pool. The government aims to create a more innovation-friendly environment by fostering national laboratories, supporting young scientists, and improving data systems. AI development is a key focus, with increased backing for large-scale models and intelligent manufacturing. This supportive environment is expected to accelerate Alibaba’s AI innovations, enhance its cloud offerings, and solidify its role in China’s digital transformation.

Unveiling its AI model. Alibaba announced its QwQ-32B AI reasoning model, which it claims performs comparably to DeepSeek’s R1 despite having far fewer parameters. Accessible via Qwen Chat, the model enhances Alibaba’s chatbot services and strengthens its AI leadership. With China pushing AI adoption across industries, Alibaba is poised to benefit from rising demand for AI-powered solutions, boosting its cloud business and investor confidence.

AI and cloud investment roadmap. Alibaba’s RMB380bn (US$70bn) investment in cloud computing and AI infrastructure over the next three years surpasses its decade long spending in the sector. As China’s top cloud provider with a 36% market share as of 3Q24 and 13% YoY cloud revenue growth in 4Q24, mainly driven by the double-digit revenue growth of public cloud products, Alibaba’s investment is expected to enhance its AI and cloud capabilities, attract enterprise customers, and drive long-term growth.

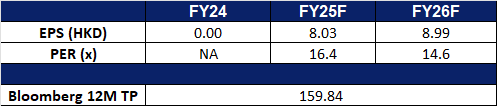

4Q24 results review. Revenue increased 8% YoY to RMB280.2bn in 4Q24, compared with RMB260.3bn in 4Q23. Net income rose by 333% YoY to RMB46.4bn in 4Q24, compared to RMB10.7bn in 4Q23. Diluted earnings per share increased to RMB2.55 in 4Q24, compared to RMB0.71 in 4Q23.

Market consensus.

(Source: Bloomberg)

McDonald’s Corp (MCD US): Delivering value to customers

BUY Entry – 316 Target – 350 Stop Loss – 300

McDonald’s Corporation franchises and operates fast food chain. The Company offers various food products and soft drinks, and non alcoholic beverages. McDonald’s serves customers worldwide.

Increased concerns about a U.S. recession benefit defensive sectors. Recent U.S. macroeconomic data shows that inflation remains high, while the labour market is beginning to cool, and consumer spending and confidence are declining. Trump’s tariff policy has triggered a global trade war, and the U.S. stance on the Russia-Ukraine issue has been questioned by its allies. With the concentration of negative factors, the market is averse to uncertainty, so major growth sectors have seen significant corrections, and funds have rotated to stronger defensive sectors.

Launch of the new McValue platform. McDonald’s launched the new McValue platform on January 7 this year, aiming to provide customers with affordable options and increase dining value. The platform includes a $5 value package, buy one get one free, local dining deals, and app exclusive deals. The platform is favoured by consumers in a high inflation and consumption downgrade environment and increases the company’s sales and market share.

Application of artificial intelligence technology. McDonald’s plans to introduce artificial intelligence technology in 43,000 restaurants worldwide to speed up service and improve customer and employee experience. These upgrades include smart kitchen equipment, AI-driven drive-thru services, and management tools for order accuracy and predictive maintenance. McDonald’s is working with Google Cloud to use edge computing for real-time data processing, with the goal of increasing the number of customers from 175 million to 250 million by 2027.

4Q24 results. Revenue fell 0.3% YoY to US$6.39 billion, missing expectations by US$90 million. Non-GAAP earnings per share were US$2.83, missing expectations by US$0.03. The company raised its full-year 2025 operating profit margin to 45% to 50%, exceeding 46.3% in 2024. The company plans to open more than 2,200 stores in 2025, an increase of more than 4%.

Market consensus

(Source: Bloomberg)

Philip Morris International Inc (PM US): Zyn-ergy in action

Philip Morris International Inc. operates as a tobacco company working to deliver a smoke-free future and evolving its portfolio for the long term to include products outside of the tobacco and nicotine sector. The Company offers cigarettes, e-vapor, and oral smoke-less products. Philip Morris International serves customers worldwide.

Potential sale of business. Philip Morris (PM) International’s decision to explore the sale of its U.S. cigar business aligns with its broader strategy to transition away from traditional tobacco products. By divesting this asset, the company can reallocate resources toward its growing smoke-free product portfolio, such as Zyn nicotine pouches and IQOS heated tobacco devices. This shift not only supports long-term revenue growth but also enhances PM’s positioning in the evolving nicotine market. The expected US$1bn sale proceeds could fund further innovation and expansion, accelerating its goal of achieving two-thirds of sales from smoke-free products by 2030.

Decline in smoking rates. With global smoking rates continuing to fall due to health concerns and regulatory pressures, PM’s pivot toward alternative nicotine products is a crucial move. Traditional cigarettes face declining demand, but the company’s strong performance in Zyn and IQOS demonstrates its ability to adapt to changing consumer preferences. By focusing on harm-reduction alternatives, PM ensures revenue stability despite a shrinking cigarette market. This proactive approach not only mitigates risks associated with declining smoking trends but also strengthens the company’s position as an industry leader.

FDA approved. The FDA’s authorization of Zyn nicotine pouches marks a major milestone for PM, validating its harm-reduction strategy and providing a competitive edge in the U.S. market. With official regulatory backing, PM can further promote Zyn as a safer alternative to traditional tobacco, attracting more adult smokers looking to switch. This approval also opens doors for expansion into other regions where similar regulatory acceptance could drive growth. As health-conscious consumers seek alternatives, PM is well-positioned to capitalize on the increasing demand for smokeless nicotine products.

4Q24 results. Revenue grew 7.3% YoY to US$9.71bn, beating estimates by US$270mn. Non-GAAP EPS was US$1.55, beating expectations by US$0.05. The company projected FY25 adjusted annual earnings per share in the range of US$7.04 to US$7.17, above analysts’ estimate of US$7.03. It also forecast ZYN shipments to the U.S. would rise by between 34% and 41% in 2025, while IQOS shipments would also see between 10% and 12% growth.

Trading Dashboard Update: Add Alibaba Group Holding Ltd (9988 HK) at HK$138. Cut loss on General Electric (GE US) at US$195, Costco (COST US) at US$960, and Palo Alto Networks (PANW US) at US$175.