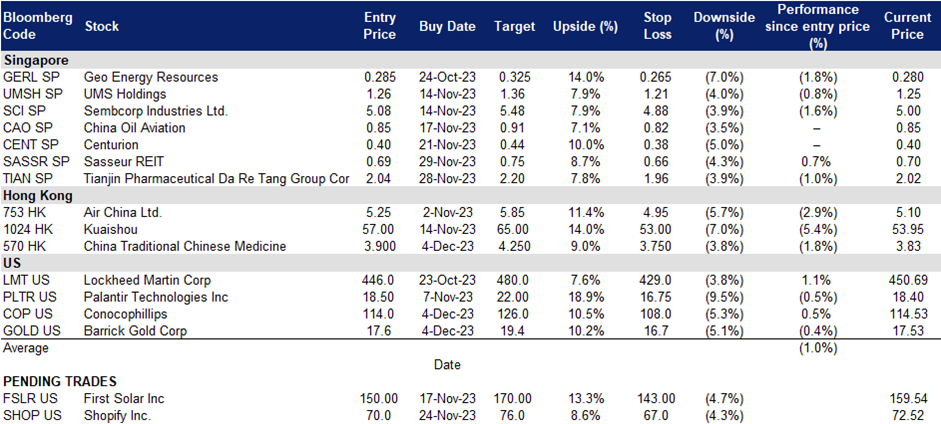

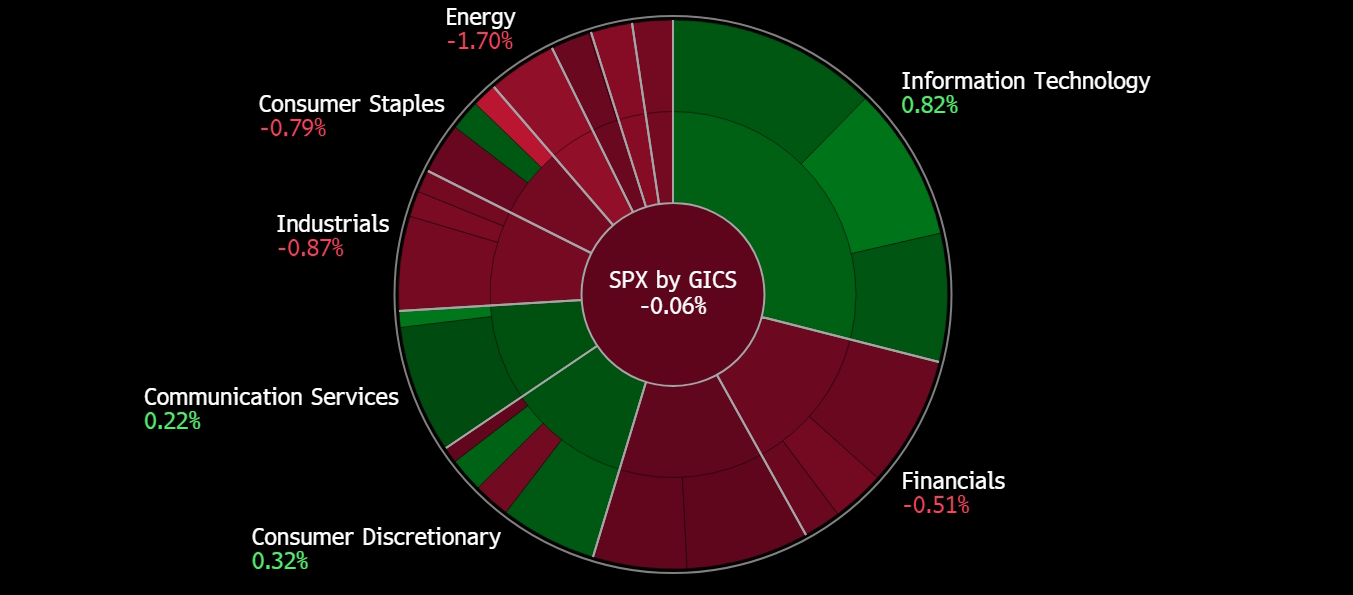

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

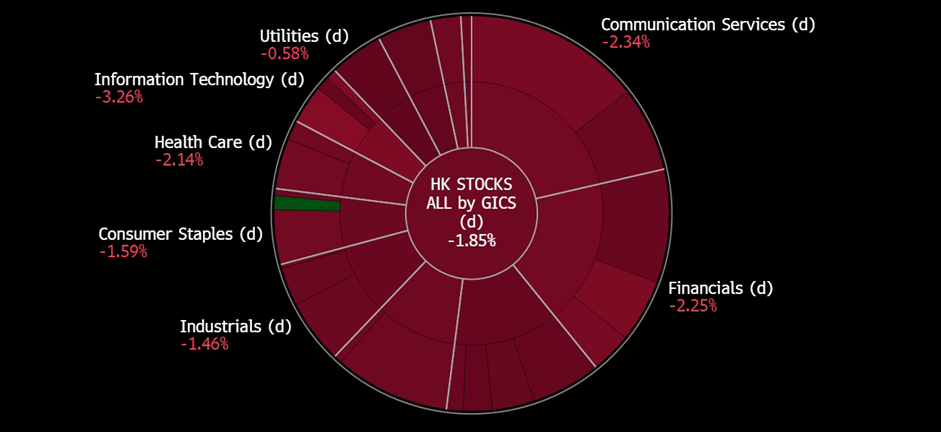

Hong Kong

Centurion Corp Ltd (CENT SP): Early signs of a re-rating catalyst

- RE-ITERATE BUY Entry 0.40 – Target – 0.44 Stop Loss – 0.38

- Centurion Corporation Limited specialises in owning and operating worker and student accommodation assets. It ranks among Singapore’s largest owner-operators of high-quality worker accommodations in Singapore and Malaysia. Additionally, the company manages student accommodation properties across Singapore, Australia, the United Kingdom, and the United States.

- Sale and leaseback agreement. On 4 December, Centurion announced that it had entered into a sale and leaseback agreement with Malaysia’s public sector pension fund, Kumpulan Wang Persaraan (Diperbadankan) [KWAP], involving two of its Malaysia assets, Westlite Bukit Minyak and Westlite Tampoi. KWAP will acquire these assets for RM 227mn, and Centurion will lease them back for a 15-year term. This strategic move aligns with Centurion’s portfolio rationalisation and asset-light growth strategy, allowing the company to recycle and deploy capital for further expansion in response to the rising demand for Purpose-Built Workers Accommodation (PBWA) in Malaysia. As of September 2023, Centurion’s Malaysia PBWA portfolio bed capacity was 26,603 beds, with a 93% financial occupancy rate in 3Q23. The company will continue to enhance its portfolio through initiatives like Asset Enhancement Initiatives (AEIs) and management contracts for new PBWAs.

- Rate cut expectations. Global inflation is on track to decline, and major central banks increasingly signal peak rates. The October US inflation was unchanged, and the core CPI rose by 0.2% MoM and 4.0% YoY, further reinforcing the expectations of the end of rate hikes as the Fed weigh the inflation target as the key factor to decide its key rate path. The ECB signalled that it would maintain the current key rates for a couple of quarters. British inflation fell more than expected in October, mitigating the pressure of further rate hikes. Australia hiked another 25bps in November, and economists expected that this would be the last rate hike.

- Potential valuation pump-up and re-rating. Centurion remains its asset-heavy model, and hence, the peak rate and ensuing rate cut cycle is the largest tailwind for the company. Besides, the overall portfolio is healthy along with recovering cash flows as worker and student dormitories are in demand in the post-COVID period. Furthermore, the potential lower refinancing rate and interest burden will help improve profitability.

- 3Q23 business updates. Total revenue increased by 15% YoY to S$51.0mn. 9M23 revenue increased by 10% YoY to S$149.0mn. The respective 9M23 financial occupancy of PBWA and PBSA were 96% and 90%, up from 88% and 84% in 9M22. As of 3Q23, the total asset under management was S$1.9bn with 66,607 operations beds in 34 properties in 15 cities globally.

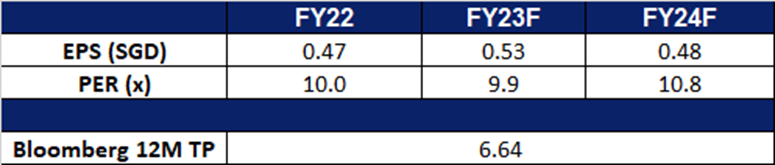

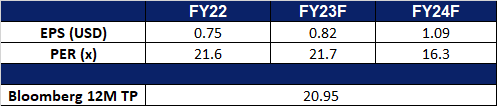

- Market consensus. We have a fundamental coverage with a BUY recommendation and a TP of S$0.56. Please read the full report here.

(Source: Bloomberg)

Tianjin Pharmaceutical Da Re Tang Group Corp Ltd (TIAN SP): Respiratory illness strikes Northern China

- RE-ITERATE BUY Entry 2.04 – Target – 2.20 Stop Loss – 1.96

- Tianjin Pharmaceutical Da Ren Tang Group Corporation Limited produces and sells traditional Chinese medicine, western medicine, health products, and healthcare instruments. The Company also manufactures gene-related biopharmaceutical products. Tianjin Pharmaceutical Da Ren Tang Group markets its products under the Great Wall, Cypress, and Health brand names.

- Respiratory symptoms spreading. China’s National Health Commission (NHC) responded to concerns about respiratory illness outbreaks, citing a surge in acute respiratory infections attributed to a combination of known pathogens, including influenza, rhinovirus, mycoplasma pneumoniae, and respiratory syncytial virus. Despite videos and social media showing crowded hospitals, the NHC assured the World Health Organisation (WHO) that no unusual or novel pathogens were detected, linking the rise to the easing of COVID-19 restrictions and the circulation of known pathogens. Influenza, respiratory syncytial virus, and adenovirus have been circulating since October. While China sees the surge as seasonal and linked to immunity debt, the WHO advises precautionary measures and stays in contact with Chinese authorities. The heightened concern may lead Chinese residents to stock up on medication and health supplements, benefiting companies like Tianjin Pharmaceutical, a producer of such health products.

- Resistance to antibiotics. Despite mycoplasma pneumonia showing resistance to a broad spectrum of antibiotics, it can be treated with other drugs like azithromycin, erythromycin, and clarithromycin. The State Council taskforce has ordered local governments to enhance preparedness for outbreaks of flu, COVID, and other infectious diseases, which may heighten the need for healthcare equipment and medications.

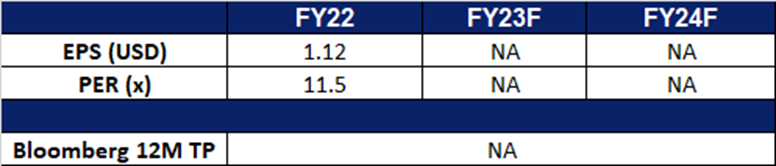

- 3Q23 business updates. Total revenue declined by 5% YoY to RMB$1,705mn. 9M23 revenue increased by 4% YoY to RMB$5,793mn. Issued cash dividend on 6 June 2023 amounting to RMB1.12 per ordinary share.

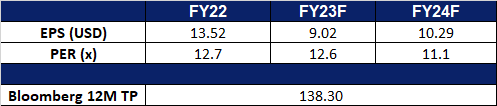

- Market Consensus.

(Source: Bloomberg)

China Traditional Chinese Medicine Holdings Co. Limited (570 HK): Protection for winter flu

- BUY Entry – 3.90 Target – 4.25 Stop Loss – 3.75

- China Traditional Chinese Medicine Holdings Co. Limited is principally engaged in the manufacture and sales of traditional Chinese medicine (TCM). The Company operates through 12 subsidiaries, including Sinopharm Group Dezhong (Foshan) Pharmaceutical Co., Ltd., Sinopharm Group Feng Liao Xing (Foshan) Pharmaceutical Co., Ltd., Sinopharm Group Guangdong Medi-World Pharmaceutical Co., Ltd., Sinopharm Group Luya (Shandong) Pharmaceutical Co., Ltd., Sinopharm Group Feng Liao Xing (Foshan) Medicinal Material & Slices Co., Ltd., Foshan Winteam Pharmaceutical Sales Company Limited, Sinopharm Group Tongjitang (Guizhou) Pharmaceutical Co., Ltd., Sinopharm Group Jingfang (Anhui) Pharmaceutical Co., Ltd., Sinopharm Group Longlife (Guizhou) Pharmaceutical Co., Ltd., Qinghai Pulante Pharmaceutical Co., Ltd., Guizhou Zhongtai Biological Technology Company Limited and its subsidiaries and Jiangyin Tianjiang Pharmaceutical Co., Ltd. and its subsidiaries.

- China experiencing a respiratory illness outbreak. Seasonally, respiratory illness cases increase during winter season, especially in the norther part of China. However, a recent surge in flu and pneumonia cases in China raised concerns about whether COVID spread resumed. No new virus has been detected so far, and experts believe that the three-year lockdown policy protected most Chinese residents from COVID virus, and hence, a lack of antibodies contributes to people’s weakened immunity against COVID-like flu and pneumonia.

- Traditional Chinese medicines in demand. Thought traditional Chinese medicine is not the specialised drugs to treat flu or pneumonia, it is considered a supplementary treatment. Families are stocking up on traditional Chinese medicines and pills in case members have similar symptoms. The authorities have recently released the 2023 Winter Influenza Chinese Medicine Prevention and Treatment Plan for Beijing. Consequently, the demand for these medicines is likely to increase throughout the winter and early spring seasons.

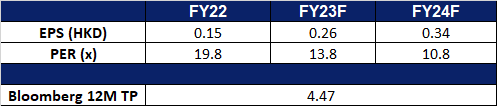

- 1H23 results update. Revenue jumped by 57.4% YoY to RMB9.3bn. GPM was 51.1%, up 0.7ppts YoY. Net profit jumped by 40.0% YoY to RMB557.2mn. NPM was 6.2%, up 0.3 ppts.

- Market consensus.

(Source: Bloomberg)

(Source: Bloomberg)

Air China Ltd. (753 HK): Flights to increase going forward

- RE-ITERATE BUY Entry – 5.25 Target – 5.85 Stop Loss – 4.95

- Air China Limited is a China-based company principally engaged in the provision of air passenger transportation, freight transportation, postal transportation and maintenance services in Mainland China, Hong Kong, Macau and foreign regions. The Company is also engaged in domestic and international business aviation businesses, plane business, aircraft maintenance, airlines business agents, ground and air express services related to main businesses, duty free on boards, retail business on boards and aviation accident insurance sales agents business.

- Returning to Profit. Air China returned to profitability during the initial nine months of the year, driven by a substantial increase in business and leisure travel after Beijing eased stringent COVID-19 restrictions. With the increase in deployment of transportation capacity by the company, and driven by the increase in both passenger load factor and price, the loss decreased significantly with growth in profit.

- More flights between China and the US. The US Department of Transportation announced that flights between China and the US will increase to 70 a week starting on 9 November, from the current 48 a week. The average flights between the two counties averaged 340 a week in the pre-COVID period. Recently, China and the US top officials started visiting each other, signalling some improvements in China-US relations.

- Rising seasonal travel demand. With the peak travel season coming up in November, travel demand is bound to pick up as consumers make their plans to travel for the end of the year, to escape the winter cold, or to experience the winter season. This winter holiday is also the first winter holiday since China’s reopening in Jan earlier this year, and hence is likely to see a rise in travel volume over the period. Chinese airlines have also seen a rise in scheduled flights for winter-spring, scheduling 96,651 domestic cargo and passenger flights each week for the upcoming winter-spring season, an increase of 33.95% from the same period in 2019-2020, according to the Civil Aviation Administration of China (CAAC). 516 new domestic routes will also be opened from Oct 29 to March 30 next year,, providing 7,202 flights each week, according to the CAAC. In terms of international flights, 150 domestic and foreign airlines plan to arrange 16,680 flights per week, reaching 68 foreign countries.

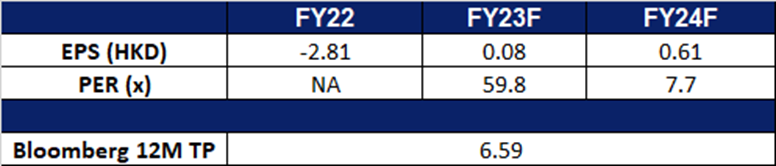

- 3Q23 earnings. Revenue rose to RMB45.86bn, up 152.89% YoY. Net profit was RMB 4.07bn, returning to profit for the first time for the year. Basic earnings per share was RMB0.28.

Market Consensus.

(Source: Bloomberg)

Barrick Gold Corp (GOLD US): A rate-cut bet

- BUY Entry – 17.6 Target – 19.4 Stop Loss – 16.7

- Barrick Gold Corporation is an international gold company with operating mines and development projects in the United States, Canada, South America, Australia, and Africa.

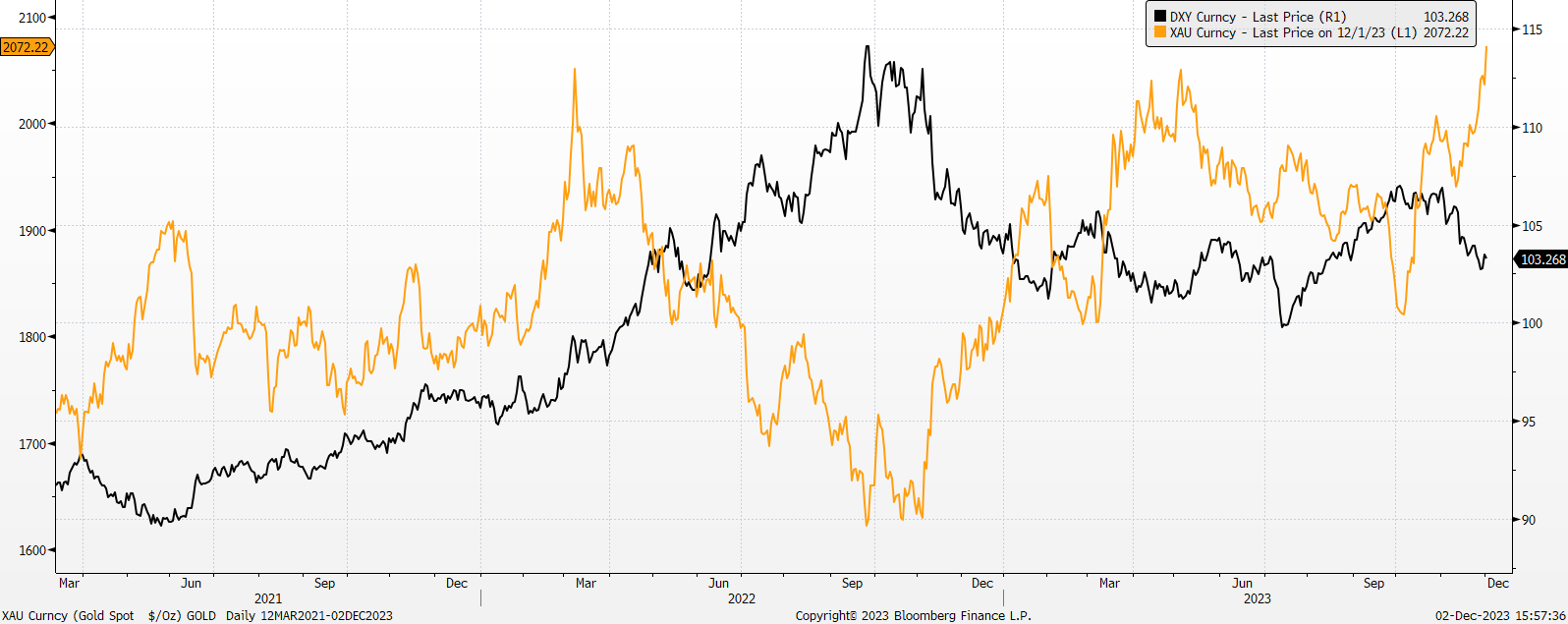

- Inflation easing. The anticipated conclusion of the current interest rate hike cycle is slated for the upcoming year. The Federal Reserve’s trajectory for US interest rate adjustments remains anchored in the pivotal long-term 2% inflation target, as underscored by recent addresses from various branch chairmen. Notably, recent inflation data suggests a notable easing of inflationary pressures in the United States. In October, the personal consumption expenditures (PCE) price index, rose 0.2%, in line with expectations, showing a 3.5% increase YoY. Personal income and spending both rose 0.2%, meeting estimates and suggesting consumers are keeping pace with inflation. Despite headline inflation remaining flat at 3% for the month, energy price decreases offset food price increases. Goods prices fell 0.3%, while services rose 0.2%, with notable gains in international travel, health care, and food services. Continuing unemployment claims surged to 1.93mn, the highest since 27 November 2021. This has prompted the market to accelerate its timeline for anticipating a Federal Reserve interest rate reduction, now anticipated in the second quarter of the coming year. Concurrently, both the 10-year and 30-year US bond interest rates, along with the US dollar index, have experienced recent declines. Conversely, the price of gold has rebounded, surging to levels reminiscent of May this year and surpassing the significant $2,000/oz threshold once more.

Gold Price vs Dollar Index

(Source: Bloomberg)

- Geopolitical unease remains elevated. Despite recent alleviation in tensions between China and the United States, the overall outlook remains cautious. As we approach 2024, anticipated geopolitical uncertainties loom, notably with the Taiwan election in January and the US election in November. The prevailing risk aversion continues to underpin elevated gold prices.

- 3Q23 results. Revenue rose 13% YoY, to US$2.86bn. Non-GAAP EPS beat estimates by US$0.04 at US$0.24. Expect stronger 4Q23 results, but FY23 gold production to be slightly below previous guidance range of US$4.2mn/oz to US$4.6mn/oz.

- Market consensus.

(Source: Bloomberg)

Conocophillips (COP US): OPEC+ production cut expectations

- RE-ITERATE BUY Entry – 114 Target – 126 Stop Loss – 108

- ConocoPhillips explores for, produces, transports, and markets crude oil, natural gas, natural gas liquids, liquefied natural gas, and bitumen on a worldwide basis.

- OPEC+ meeting. OPEC+ is in discussions regarding a potential additional oil supply cut for the first quarter of 2024 to bolster the market, with the exact details yet to be finalised. The group, responsible for over 40% of global oil supply, is already implementing cuts of about 5mn barrels per day (bpd). Sources suggest the proposed cut could be as much as 1mn bpd, though uncertainties remain, and the meeting may retain the existing policy. The talks, initially delayed due to a dispute over output quotas for African producers, will proceed on Thursday. Brent crude oil is currently around $83 per barrel. With the possible output cut, oil prices will once again rise due to the reduction of supply in the market.

Brent price chart

(Source: Bloomberg)

- US oil production rose. US crude oil, gasoline, and distillate inventories increased as refiners raised output despite subdued fuel demand, according to the Energy Information Administration (EIA). Crude inventories rose by 1.6mn barrels, with East Coast stockpiles reaching their highest since January 2021. Refinery crude runs increased, and refinery utilisation rates rose to 89.8% of total capacity. The return of refinery capacity after maintenance, coupled with weak demand during the Thanksgiving holiday, contributed to the supply situation. Despite the inventory builds, Brent and West Texas Intermediate crude futures gained, showing that the increase in crude inventory did not affect the prices much and the focus remains on the OPEC+ meeting outcome.

- 3Q23 results. Production rose 3% YoY, to 1.81mn boe/day. Non-GAAP EPS beat estimates by US$0.07 at US$2.16. Expect Q4 revenue of US$8.69bn vs US$8.54bn consensus. Net income fell from US$4.5bn in 3Q22 to US$2.8bn in 3Q23. Forecast its 4Q23 production to be between 1.86mn to 1.9mn boe/day and raised its Fy23 forecast to be about 1.82mn boe/day. FY23 adjusted operating costs was also raised to US$8.6bn from the prior US$8.3bn.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add China Tradditional Chinese Medicine (570 HK) at HK$3.9, Conocophillips (COP US) at US$114 and Barrick Gold Corp (GOLD US) at US$17.6. Cut loss on Sembcorp Industries Ltd (SCI SP) at S$5.20, Sunny Optical Technology Group (2382 HK) at HK$68, Trip.com Group Ltd (9961 HK) at HK$262 and Netflix Inc (NFLX US) at US$462.