United States | Singapore | Hong Kong | Earnings

McDonalds Corp. (MCD US)

- Shares closed higher above the 200dEMA with a surge in volume. 5dEMA is about to cross the 200dEMA, and 20dEMA is about to cross the 50dEMA.

- MACD is positive and RSI is at an “overbought” level.

- Long – Entry 274, Target 290, Stop 266

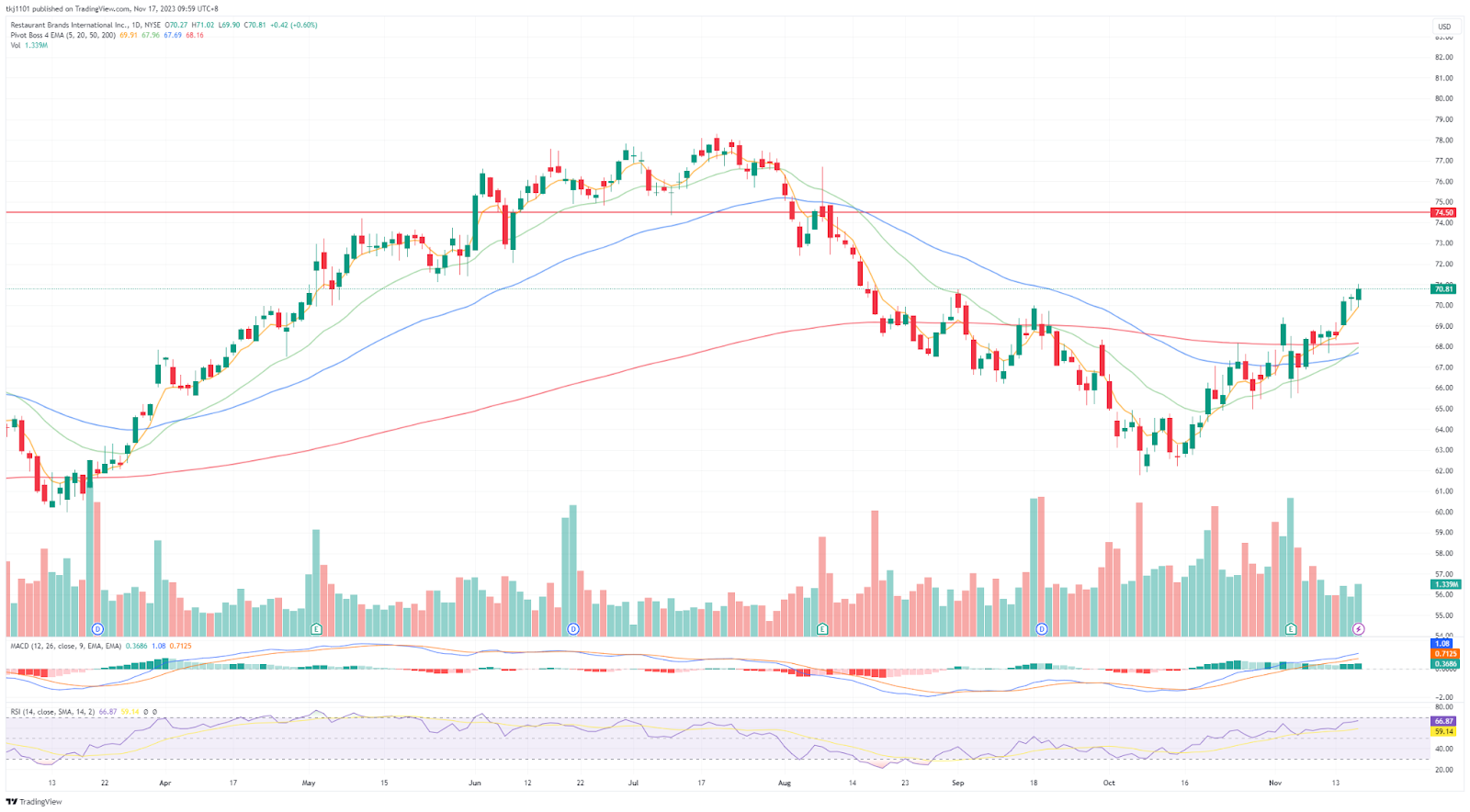

Restaurant Brands International Inc. (QSR US)

- Shares closed higher above the 5dEMA. 20dEMA just crossed the 50dEMA and is about to cross the 200dEMA.

- MACD is positive and RSI is constructive.

- Long – Entry 70.5, Target 74.5, Stop 68.5

Best World International Ltd. (BEST SP)

- Shares closed higher above the 50dEMA with constructive volume. The 5dEMA just crossed the 20dEMA.

- Both MACD and RSI are constructive.

- Long – Entry 1.70, Target 1.80, Stop 1.65

Starhub Ltd. (STH SP)

- Shares closed above the 5dEMA with constructive volume. 20dEMA just crossed the 20dEMA and 50dEMA.

- Both RSI and MACD are constructive.

- Long – Entry 1.07, Target 1.13, Stop 1.04

CGN Power Co Ltd (1816 HK)

- Shares closed above the 20dEMA.

- RSI is constructive and MACD is positive.

- Long – Entry 1.90, Target 2.00, Stop 1.85

Yankuang Energy Group Co Ltd (1171 HK)

- Shares closed above the 50dEMA. The 5dEMA crossed both the 20dEMA and 50dEMA.

- Both RSI and MACD are constructive.

- Long – Entry 13.86, Target 15.14, Stop 13.22

Alibaba Group Holding Ltd. (BABA)

- 2Q24 Revenue: $30.81B, +9.0% YoY, miss estimates by $230M

- 2Q24 Non-GAAP EPADS: $2.14, beat estimates by $0.05

- 3Q24 Guidance: No guidance provided. The short-term business focus will be rapid expansions of its business scale and market share.

- Share repurchase and dividend: In addition to its $40bn share repurchase program, its board of directors has approved an annual dividend for fiscal year 2023 in the amount of $0.125 per ordinary share or $1 per ADS.

- Comment: The group announced that it will not be proceeding with the full spinoff of its cloud group due to U.S. chip export restrictions, highlighting that these restrictions have made it more challenging for Chinese firms to get critical chip supplies from U.S. companies. Investors were hoping that a spinoff of the group’s cloud business would achieve a higher valuation due to its growth but was derailed by fresh U.S. export rules that also damaged the outlook for the business. Instead, the company will be focusing on developing a sustainable growth model for Cloud Intelligence Group under fluid circumstances. The company also postponed its plan to list its grocery business, Freshippo. 3Q24 recommended trading range: $70 to $85. Neutral Outlook.

阿里巴巴 (BABA)

- 24财年第二季营收:308.1亿美元, 同比增幅9.0%,逊预期2.3亿美元

- 24财年第二季Non-GAAP每股盈利:2.14美元,超预期0.05美元

- 24财年第三季指引:没有提供指导。短期业务重点将是迅速扩大业务规模和市场份额。

- 股票回购和股息:除了400亿美元的股票回购计划外,其董事会还批准了2023财年的年度股息,每股普通股0.125美元或每股美国存托凭证1美元。

- 短评:该集团宣布,由于美国的芯片出口限制,它将不会继续全面分拆其云业务,并强调这些限制使中国公司更难从美国公司获得关键芯片供应。投资者原本希望,该集团云业务的分拆将因其增长而获得更高的估值,但由于美国新的出口规定也损害了该业务的前景,该计划未能实现。相反,该公司将专注于在变化的环境下为云智能集团开发可持续的增长模式。该公司还推迟了其食品杂货业务盒马鲜生的上市计划。24财年第三季度建议交易区间:70美元至85美元。积极前景。

Walmart Inc. (WMT)

- 3Q23 Revenue: $160.8B, +5.2% YoY, beat estimates by $2.26B

- 3Q23 Non-GAAP EPADS: $1.53, beat estimates by $0.01

- FY23 Guidance: Net sales of $605.9B, adjusted operating income at $24.6B, adjusted EPS of $6.29. FY24 guidance: Net sales growth of 5.0%-5.5% vs 5.61% consensus ($639.85B consensus); Adj EPS of $6.40 to $6.48 vs $6.50 consensus, including expected $0.03 headwind from current year LIFO charges, $0.04 benefit YoY

- Comment: The company reported a solid set of results and raised its FY23 guidance. However, the guidance was still below the market’s and analysts’ expectations. The company still see challenges in consumer spending, with consumer showing ongoing discretion and making trade-offs to be able to afford the things they want given macroeconomic uncertainties. The company saw a slowdown in spending in late October, but sales have rebounded in November. While the company remains conservative, we expect sales to continue increasing as the holiday season arrives. 4Q23 recommended trading range: $150 to $175. Positive Outlook.

沃尔玛 (WMT)

- 23财年第三季营收:1,608亿美元, 同比增幅5.2%,超预期22.6亿美元

- 23财年第三季GAAP每股亏损:1.53美元,超预期0.01美元

- 23财年指引:净销售额为6059亿美元,调整后营业利润为246亿美元,调整后每股收益为6.29美元。24财年指引:净销售额增长5.0%-5.5%,市场预期为5.61%(6398.5亿美元);预期每股收益为6.40美元至6.48美元,而市场预期为6.50美元,其中包括今年后进先出费用预计为0.03美元的阻力,同比收益为0.04美元

- 短评:该公司公布了一系列强劲的业绩,因为他们专注于价格竞争力和运营效率。该公司专注于以更低的价格推动需求,并削减成本以提高利润率,这已显示出成效,其2009年的营业利润率为4.3%,而去年同期为4.0%。在经济疲软的情况下,中国10月份的零售额超过了增长,显示出消费者支出的弹性。在今年早些时候的光棍节促销活动中,该公司的交易量和订单量以及用户参与度也创下了纪录。即将到来的节日也可能刺激消费者支出。23财年第四季度建议交易区间:150美元至175美元。积极前景。

Applied Materials, Inc. (AMAT)

- 4Q23 Revenue: $6.72B, -0.4% YoY, beat estimates by $220M

- 4Q23 Non-GAAP EPS: $2.12, beat estimates by $0.13

- 1Q24 Guidance: Expect net sales to be approximately $6.47B vs consensus of $6.37B, plus or minus $400M; Non-GAAP adjusted diluted EPS is expected to be in the range of $1.72 to $2.08 vs consensus of $1.83.

- Comment: The company reported a strong set of earnings. Consumer demand also proved to be resilient despite the macroeconomic uncertainties. While results from companies such as Intel and Advanced Micro Devices indicate that the market is showing signs of recovery, the company is still likely to face export challenges between the U.S. and China. The media also reported that the company was under criminal investigation by the Justice Department for sending its equipment to a Chinese company without the required licenses, with hundreds of millions of dollars of equipment being involved. 2Q24 recommended trading range: $130 to $150. Neutral Outlook.

应用材料 (AMAT)

- 23财年第四季营收:67.2亿美元, 同比跌幅0.4%,超预期2.2亿美元

- 23财年第四季Non-GAAP每股盈利:2.12美元,超预期0.13美元

- 24财年第一季指引:预计净销售额约为64.7亿美元,而市场预期为63.7亿美元,上下浮动4亿美元;Non-GAAP调整后的稀释每股收益预计在1.72美元至2.08美元之间,而市场预期为1.83美元。

- 短评:该公司报告了一系列强劲的收益。尽管宏观经济存在不确定性,但消费需求也被证明具有弹性。尽管英特尔(Intel)和超微半导体(AMD)等公司的业绩显示市场正在出现复苏迹象,但该公司仍有可能面临中美之间的出口挑战。媒体还报道称,该公司正在接受司法部的刑事调查,因为它在没有获得必要许可证的情况下向一家中国公司提供设备,涉及价值数亿美元的设备。24财年第二季度建议交易区间:130美元至150美元。中性前景。

Ross Stores Inc. (ROST)

- 3Q23 Revenue: $4.92B, +7.7% YoY, beat estimates by $80M

- 3Q23 Non-GAAP EPS: $1.33, beat estimates by $0.11

- FY23 Guidance: EPS is expected to be in the range of $5.30 to $5.36 versus $4.38 last year.

- 3Q23 Dividend: The company declares a $0.335/share quarterly dividend, in line with the previous. Payable Dec. 29; for shareholders of record Dec. 5; ex-div Dec. 4.

- Comment: The company reported a strong set of results and increased its guidance, highlighting that consumers reacted well to the company’s off-price merchandise. Consumer spending still remains shaky amidst ongoing macroeconomic uncertainties and geopolitical tensions, but the company remain confident in the resilience of the off-price sector and the company’s ability to operate successfully within it, as consumers continue to look for cheap and value goods. With interest rates at their peak, alongside the upcoming festive season and holidays, consumer spending is likely to improve for the rest of the year. 4Q23 recommended trading range: $120 to $140. Positive Outlook.

罗斯百货 (ROST)

- 23财年第三季营收:49.2亿美元, 同比增幅7.7%,超预期8,000万美元

- 23财年第三季Non-GAAP每股盈利:1.33美元,超预期0.11美元

- 23财年指引:每股收益预计在5.30美元至5.36美元之间,去年为4.38美元。

- 23财年第三季股息:该公司宣布每股0.335美元的季度股息,与之前一致。12月29日付息日;12月5日股东登记日;12月4日除息日。

- 短评:该公司公布了一系列强劲的业绩,并提高了预期,强调消费者对该公司的折扣商品反应良好。在当前的宏观经济不确定性和地缘政治紧张局势中,消费者支出仍然不稳定,但随着消费者继续寻找廉价和物有所值的商品,该公司对折扣部门的弹性和公司在其中成功运营的能力仍然充满信心。随着利率达到峰值,加上即将到来的节日和假期,消费者支出可能会在今年剩余时间里有所改善。23财年第四季度建议交易区间:120美元至140美元。积极前景。

NetEase Inc. (NTES)

- 3Q23 Revenue: $3.7B, +11.6% YoY, miss estimates by $80M

- 3Q23 Non-GAAP EPADS: $1.84, beat estimates by $0.37

- 4Q23 Guidance: No guidance provided.

- Dividend and share repurchase: declared a Q3 dividend of 49.5 cents per US share and introduced a share repurchase program of up to $5bn.

- Comment: In the third quarter, NetEase delivered mixed results, reporting $3.74bn in sales, reflecting a noteworthy 16% YoY increase in earnings and a 9% rise in sales. Specifically, revenue from Games and Related Value-Added Services exceeded estimates, reaching 21.78bn yuan, while Innovative Businesses and Others fell slightly short with net revenue of 1.98bn yuan against the estimated 2.17bn yuan. Youdao and Cloud Music reported lower-than-expected net revenues at 1.54bn yuan and 1.97bn yuan respectively. The adjusted net income per ADS was 13.30 yuan, and gross profit, spanning Games and Related Value-Added Services, Youdao, Cloud Music, Innovative Businesses and others, surpassed estimates with higher gross profit margins in all sectors. NetEase’s CEO, attributes the robust results to the company’s diverse and strong games portfolio, resulting in a nearly 12% YoY increase in total net revenues. Video games constituted 80% of NetEase’s revenue, with Ding highlighting the success of flagship titles like ‘Fantasy Westward Journey’ and newer hits such as ‘Racing Master,’ ‘Justice’ mobile game, and ‘Dunk City Dynasty.’ Despite falling short of revenue expectations, the company demonstrated a positive trend in Q3, with sales surpassing costs. This suggests a potential for sustained growth in the company’s bottom line. 4Q23 recommended trading range: $110 to $125. Positive Outlook.

网易 (NTES)

- 23财年第三季营收:37.0亿美元, 同比增幅11.6%,逊预期8,000万美元

- 23财年第三季Non-GAAP每股亏损:1.84美元,超预期0.37美元

- 23财年第四季指引:不提供指引。

- 短评:第三季度,网易的业绩喜忧参半,销售额为37.4亿美元,利润同比增长16%,销售额同比增长9%。具体而言,游戏及相关增值服务的收入超过预期,达到217.8亿元,而创新业务和其他业务的净收入略低于预期,为19.8亿元,而预期为21.7亿元。bbb和云音乐的净收入分别为15.4亿元和19.7亿元,低于预期。调整后的每广告净收入为13.30元,毛利超过预期,涵盖游戏及相关增值服务、有道、云音乐、创新业务等,各领域毛利均高于预期。网易首席执行官将强劲的业绩归功于公司多样化和强大的游戏组合,导致总净收入同比增长近12%。视频游戏占网易收入的80%,丁磊强调了《梦幻西游》等旗舰游戏以及《赛车大师》、《正义》手机游戏和《灌篮城王朝》等较新的热门游戏的成功。尽管收入低于预期,但该公司在第三季度表现出积极的趋势,销售额超过了成本。这表明该公司的利润有持续增长的潜力。23财年第四季度建议交易区间:110美元至125美元。积极前景。