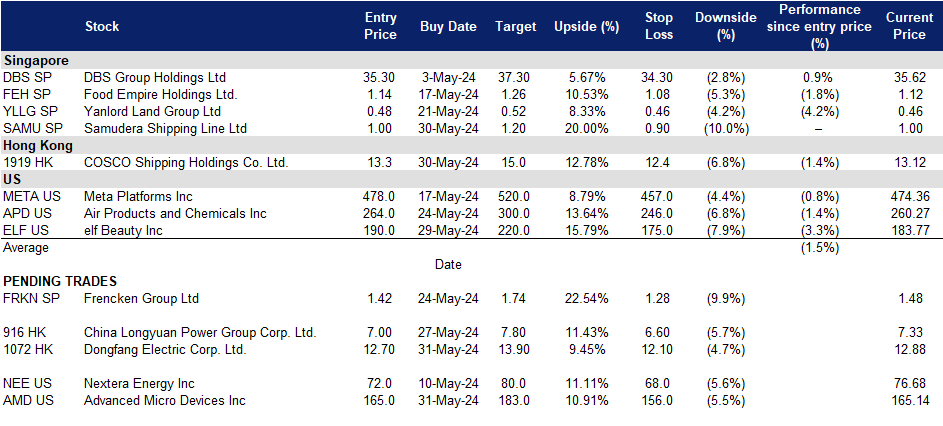

31 May 2024: Samudera Shipping Line Ltd (SAMU SP), Dongfang Electric Corp. Ltd. (1072 HK), Advanced Micro Devices Inc (AMD US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

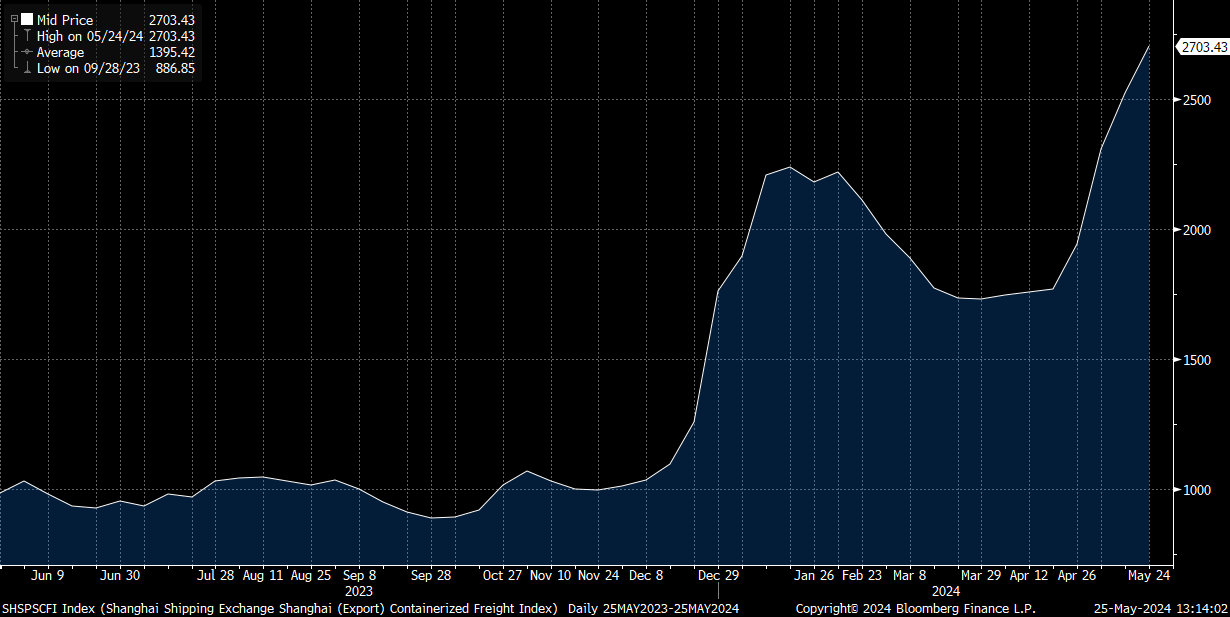

Samudera Shipping Line Ltd (SAMU SP): Freight rates going back upwards

- RE-ITERATE BUY Entry – 1.00 Target– 1.20 Stop Loss – 0.90

- Samudera Shipping Line Limited owns and operates ocean-going ships and provides containerized feeder shipping services. Through its subsidiaries, the Company also owns and charters vessels, provides sea and air freight forwarding, and operates shipping agency and container freight station services.

- Intra-Asia freight rates at 30-month high. Port congestion in Asia, diversions in the Red Sea, and increasing exports from Southeast Asia are driving intra-Asia freight rates to 30-month highs on some routes from China. Carriers and forwarders report rising intra-Asia volumes as long-haul ocean carriers redeploy vessels and skip regional trades to support mainline east-west services. High charter rates and a shortage of feeder vessels are preventing carriers from leasing additional ships to address the capacity shortfall.

Shanghai Shipping Exchange (Export) Containerized Freight Index

(Source: Bloomberg)

- Global shipping rates surge. A sudden container capacity crunch is causing global ocean freight rates to soar, with rates increasing by about 30% recently and expected to rise further, impacting consumer prices. This surge is driven by the peak shipping season, longer transit routes to avoid the Red Sea, and bad weather in Asia, leading carriers to skip ports and reduce time at ports, exacerbating supply chain issues. Spot rates have spiked by as much as US$1,500 on US routes, with container shortages severe due to high demand and delayed returns of empty containers. This situation is reminiscent of the Covid-19 pandemic, with logistics experts now facing shortages in trade lanes from Asia to Latin America, Europe, and the US West Coast. The ongoing congestion and higher rates are expected to persist, especially with an early start to the peak shipping season to avoid potential labour disruptions at East Coast and Gulf ports in the fall. Shipping companies are increasing rates and adding surcharges, with MSC announcing rates of US$8,000 to US$10,000 for 40-foot containers to the US West Coast. The higher rates are expected to benefit Samudera, enabling it to boost its revenue in response to the increased demand despite the higher prices.

- Reaping the benefits of its new additions. On 27 December, Samudera Shipping announced that it signed a memorandum of understanding to acquire two ethylene gas vessels for US$12.6mn, to be renamed Sinar Ternate and Sinar Tidore. Built in 2009 and 2010 and flagged in the Bahamas, the acquisition will be funded through bank borrowings and internal resources. This purchase aims to expand Samudera’s fleet and secure more charter contracts, capitalizing on the growing ethylene market in Indonesia, where ethylene is extensively used as a feedstock in petrochemical plants. It announced that the second vessel, Sinar Tidore was delivered on 24 April 2024. This will enable it to take on more charter contracts contributing to an increase in its revenue.

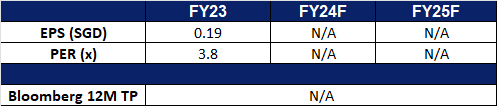

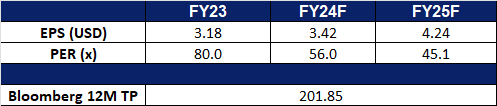

- FY23 results review. FY23 revenue fell by 41.2% to US$582.9mn and net profit decreased 68.6% YoY to USS$101.2mn. The decline was attributed to lower freight rates in the container shipping segment, despite a slight increase in container volume. In 1Q24, its container volume remained relatively stable, whereas freight rates declined to US$244 from US$371 per TEU. Its fleet size increased to 7 vessels. Additionally, both storage capacity and volume handled rose YoY, attributed to securing more management contracts and higher demand for storage capacity.

- Market Consensus

(Source: Bloomberg)

Frencken Group Ltd (FRKN SP): Semicon recovery on-track

- RE-ITERATE BUY Entry – 1.42 Target– 1.74 Stop Loss – 1.28

- Frencken Group Limited (“Frencken”) is a Global Integrated Technology Solutions Company that is listed on the Main Board of the Singapore Exchange. They provide comprehensive Original Design, Original Equipment, and Diversified Integrated Manufacturing solutions for world-class multinational companies in the analytical & life sciences, automotive, healthcare, industrial, and semiconductor industries.

- Nvidia delivering better than anticipated results again. Nvidia recently reported Q1 results which surpassed estimates, its revenue tripled YoY to US$26bn and it delivered profits that significantly exceeded expectations. The company projected higher-than-expected Q2 revenue of about US$28bn, surpassing analysts’ predictions of US$26.8bn. This positive outlook is driven by the strong demand for AI chips. Its CEO heralded this as the start of a new industrial revolution. Nvidia is currently bolstered by AI accelerators used by major tech firms like Amazon and Google. Despite high demand outpacing supply, Nvidia aims to diversify its market beyond hyperscalers to sectors like healthcare and automotive. This positive demand is expected to extend to Frencken’s semiconductor segment, which represents approximately 41% of its FY revenue.

- Good performance. Frencken Group’s revenue rose 12.2%YoY to S$193.6mn, with the mechatronics division seeing a 14.4% increase to S$170.1mn, primarily from the semiconductor, medical, and analytical life sciences segments. It reported a net profit of S$9mn for 1Q23, up 73% from S$5.2mn the previous year, driven by higher gross profit margins and revenue growth. The IMS division’s revenue remained stable at S$22.8mn, with a decline in the automotive segment offset by a significant increase in the consumer and industrial electronics segment. Gross profit margin improved to 13.7%. The company remains cautious due to global economic uncertainties and expects 1H24 revenue to be comparable to 2H23, with growth in semiconductor, medical, and analytical life sciences segments but softer automotive and industrial automation revenues. Frencken is anticipated to recover alongside the rest of the Semiconductor industry.

- 1Q24 results review. 1Q24 revenue rose by 12.2% to S$193.6mn, compared to S$172.5mn in 1Q23. Net profit increased 73% YoY to S$9mn from S$5.2mn in the previous year due to higher revenue growth and gross profit margins. Gross profit margin improved to 13.7% in 1Q24 from 12.3% in 1Q23, attributing it to better operating leverage. In 1H24, Frencken expects to deliver revenue comparable to 2H23 revenue. The semiconductor, medical, and analytical life sciences segments are expected to improve, while the industrial automation and automotive segments are expected to soften.

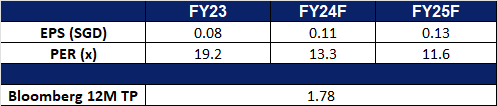

- Market Consensus

(Source: Bloomberg)

Dongfang Electric Corp. Ltd. (1072 HK): Boom in renewable energy

- BUY Entry – 12.70 Target 13.90 Stop Loss – 12.10

- Dongfang Electric Corp Ltd is a China-based company mainly engaged in the manufacturing and sales of power generation equipment. The Company operates five major reporting segments: Clean and High-Efficiency Energy Equipment segment, Renewable Energy Equipment segment, Engineering and Trade segment, Modern Manufacturing Service Industry segment, and Emerging Growth Industry segment. The Company’s main products include water turbine generator sets, steam turbine generators, wind turbine generator sets, power station steam turbines and power station boilers as well as gas turbines. The Company distributes its products within the domestic market and to overseas market.

- Expectations of higher electricity demand. China is projected to experience accelerated growth in electricity demand this year, with an anticipated increase of 8.3%, according to the National Energy Administration (NEA). The NEA forecasts power consumption to reach 9.96 trillion kilowatt-hours in 2024, up from a 6.7% growth rate in 2023. In April, China’s electricity consumption saw robust expansion, rising 7% year-over-year to 741.2 billion kilowatt-hours, driven by significant growth in industrial power generation. On the renewables end, solar power output soared by 21.4% year-over-year, while hydropower output increased by 21%. The NEA also expects solar and wind energy to contribute at least 17% of China’s electricity in 2024, up from 12% in 2023, following substantial expansion in renewable capacity over the past year.

- Surge in new-energy power generation. China’s installed capacity for power generation from clean energy sources surged in Q1 2024, driven by growing domestic demand as the country pursues high-quality and green development. According to the National Energy Administration (NEA), solar power installations reached approximately 660 million kilowatts in Q1 2024, a 55% year-over-year increase. Wind power installations grew by 21.5% year-over-year, totaling around 460 million kilowatts. As China’s economy continues to recover, energy demand is expected to rise. The demand for renewable energy and products in China is projected to remain strong as the country aims to expand its renewable capabilities and reduce CO2 emissions in 2024.

- Renewable energy collaboration. The 2024 Hungary Renewable Energy Business Investment Summit, which convened industry leaders from Hungary and China, highlights promising prospects for collaboration in renewable energy initiatives. In 2023, Hungary attracted a record-breaking 13 billion euros (approximately 14.1 billion U.S. dollars) in foreign direct investment, with Chinese investors contributing 7.6 billion euros. Recognizing the significance of strong partnerships with China in advancing their energy and climate objectives, Hungary stands to gain substantial benefits. This alliance is poised to particularly benefit power generation equipment manufacturers like Dongfang Electric.

- 1Q24 earnings. Operating revenue rose by 2.28% YoY to RMB15.1bn in 1Q24, compared to RMB14.7bn in 1Q23. Net profit fell by 11.12% YoY to RMB905.8mn in 1Q24, compared to RMB1.02bn in 1Q23. Basic EPS fell to RMB0.29 in 1Q24, compared to RMB0.33 in 1Q23.

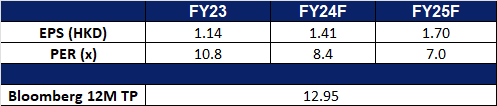

- Market consensus.

(Source: Bloomberg)

China Longyuan Power Group Corp. Ltd. (916 HK): Seasonal uptrend

- RE-ITERATE BUY Entry – 7.00 Target 7.80 Stop Loss – 6.60

- China Longyuan Power Group Corp Ltd is a China-based company mainly engaged in power sales business. The company operates three segments. Wind Power segment constructs, manages and operates wind power plants and produces electricity and sells it to grid companies. Coal Power segment constructs, manages and operates coal-fired power plants and produces electricity and sells it to power grid companies. All Others segment is mainly engaged in manufacturing and selling power generation equipment, providing consulting services, providing maintenance and training services to wind power enterprises and other renewable energy power generation and sales.

- Increasing electricity demand and upcoming summer season. In 2024, China is projected to generate 9.96tn kilowatt hours (kWh) of power, as per the National Energy Administration, reflecting a growth rate of 5.3%. The International Energy Agency predicts a 5.1% rise in electricity demand, while the China Electricity Council anticipates a 6% increase, surpassing GDP forecasts. Additionally, the upcoming summer season is expected to further boost electricity demand as consumers turn to air conditioning to escape the rising temperatures.

- Transition to green energy. China’s power storage capacity is poised for significant growth, driven by rapid advancements in renewable energy, innovative technologies, and ambitious government policies promoting sustainable development. In the first quarter of 2024, the nation’s energy storage capacity expanded substantially, with installed new-type energy storage reaching 35.3 gigawatts by the end of March, a 2.1-fold increase year-over-year. China has become a leader in renewable energy adoption, particularly focusing on enhancing its energy storage capabilities. The surging demand for energy storage solutions, essential for integrating intermittent renewable sources like wind and solar into the power grid, has spurred extensive investments in storage projects nationwide. This momentum is expected to continue, positioning China to dominate the global energy storage market in the coming years.

- Raising Capital. China Longyuan Power Group successfully issued RMB 2.0 billion in ultra short-term debentures with a 113-day term and a 1.77% coupon rate on May 22, 2024. Underwritten by Industrial Bank Co., Ltd., this issuance is intended to enhance the company’s working capital and repay debt, thereby strengthening its liquidity position.

- 1Q24 results review. Revenue increased marginally by 0.1% YoY to RMB9.88bn in 1Q24, compared with RMB9.87bn in 1Q23. Net profit rose by 1.34% to RMB2.76bn in 1Q24, compared to RMB2.72bn in 1Q23.

- Market consensus.

(Source: Bloomberg)

Advanced Micro Devices Inc (AMD US): Exciting new products

- BUY Entry – 165 Target –183 Stop Loss – 156

- Advanced Micro Devices, Inc. (AMD) produces semiconductor products and devices. The Company offers products such as microprocessors, embedded microprocessors, chipsets, graphics, video and multimedia products and supplies it to third-party foundries, as well as provides assembling, testing, and packaging services. AMD serves customers worldwide.

- Unveiling the next generation of high-performance PC. At the upcoming Computex event, taking place from 4 June to 7 June, in Taiwan, AMD is expected to reveal its next-generation Zen 5 Ryzen 9000 series desktop processors. According to online sources, the launch is targeted for July, earlier than anticipated. The Ryzen 9000 series is expected to maintain the same core counts as previous generations, with six, eight, 12, and 16 core parts, and will not adopt a hybrid core architecture like Intel’s recent CPUs. AMD’s new processors will rely on the Zen 5 architecture for performance improvements. Additionally, AMD is rumoured to skip the 700-series naming for its motherboards, opting for the 800-series, aligning with Intel’s expected 800-series chipset release. The Ryzen 9000 CPUs will be compatible with existing AM5 motherboards with a BIOS update, while Intel’s upcoming processors will require a new socket and support only DDR5 memory, making upgrades more expensive for Intel users. This exciting new launch is highly anticipated at the event as it will bring about new developments in the PC world.

- Pending partnership with Samsung. According to the Korea Economic Daily, Samsung and AMD are set to deepen their partnership to produce next-generation chips using 3-nanometer (nm) process technology. While currently limited to Apple’s Mac lineup via Taiwan’s TSMC, Samsung’s 3nm technology features gate all around (GAAFET) transistors, an upgrade over FinFET transistors, allowing for improved electrical flow. GAAFET transistors use either nanowires or nanosheets, each with different trade-offs in efficiency and current flow. AMD CEO has indicated plans to mass-produce AMD’s future products with this technology, highlighting the performance and efficiency benefits of GAAFET. This partnership positions Samsung and AMD against TSMC in the competitive semiconductor fabrication industry. Samsung aims to leverage its early adoption of GAAFET transistors to gain market share, while TSMC plans to transition to nanosheet transistors with its 2nm process.

- Aim to establish new R&D facilities in Taiwan. The Taiwanese government aims to support both AMD and NVIDIA in establishing R&D centres in Taiwan to maintain a balanced relationship. AMD is planning to invest 5bn yuan to set up its facility in Taiwan, and cities like Tainan and Kaohsiung are being considered as potential locations. This decision came after Team Red applied for Taiwan’s subsidy program, and local governments collaborated with the firm to make it happen. AMD’s CEO is scheduled to visit Taiwan next week to confirm the plans for the R&D centre and to be involved in other developments related to the supply chain. The establishment of new R&D facilities in Taiwan aims to further advance the development of next-generation AI and semiconductors.

- 1Q24 earnings review. Revenue rose by 2.2% YoY to US$5.47bn, exceeding estimates by US$20mn. Non-GAAP EPS was US$0.63, beating estimates by US$0.01. 2Q24 sales revenue is expected to be approximately US$5.7bn, plus or minus US$300mn vs. US$5.69bn consensus. Non-GAAP gross margin is expected to be approximately 53%.

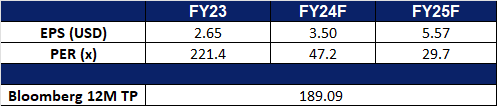

- Market consensus.

(Source: Bloomberg)

elf Beauty Inc (ELF US): Affordable dupes

- RE-ITERATE BUY Entry – 190 Target –220 Stop Loss – 175

- e.l.f. Beauty, Inc. operates as a cosmetic company. The Company offers beauty products such as eyeliners, lipsticks, creams, brushes, powder, and skin care products for eyes, lips, face, and paw. e.l.f. Beauty serves customers worldwide.

- High inflation and downgraded consumption. Ongoing inflation has dampened consumer confidence in the United States. When it comes to purchasing beauty and skincare products, consumers are leaning towards affordable yet high-quality brands. ELF has a strong presence on social media platforms like TikTok and Meta, and its target audience consists mainly of young people due to the company’s competitively priced products.

- 4Q24 earnings review. Revenue rose by 71.3% YoY to US$321mn, exceeding estimates by US$28.74mn. Non-GAAP EPS was US$0.53, beating estimates by US$0.20. Full-year FY24 sales exceeded the US$1bn mark.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add Samudera Shipping Line Ltd (SAMU SP) at S$1.00, COSCO Shipping Holdings Co. Ltd. (1919 HK) at HK$13.3 and elf Beauty Inc (ELF US) at US$190. Stop loss on Hershey Co. (HSY US) at US$196.5 and General Mills Inc (GIS US) at US$67.