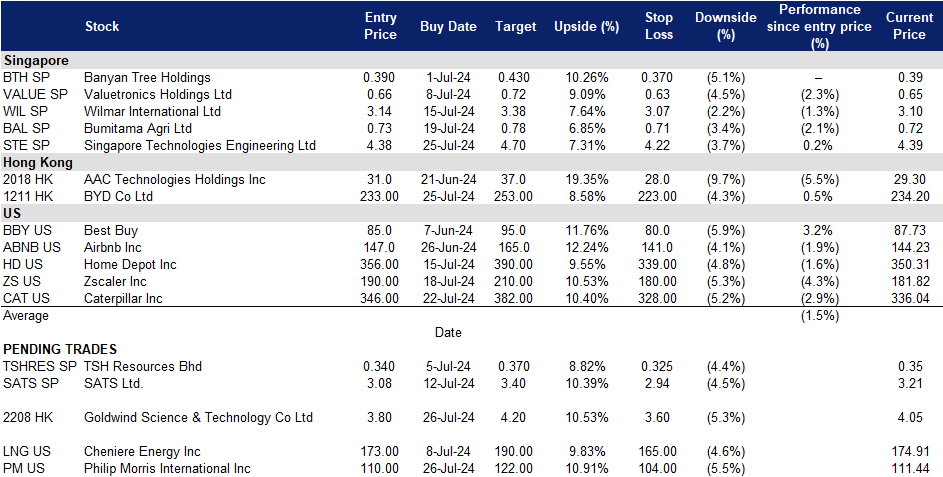

26 July 2024: Singapore Technologies Engineering Ltd (STE SP), Goldwind Science & Technology Co Ltd. (2208 HK), Philip Morris International Inc (PM US)

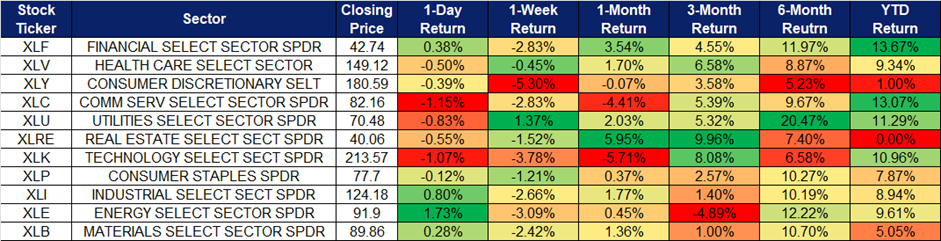

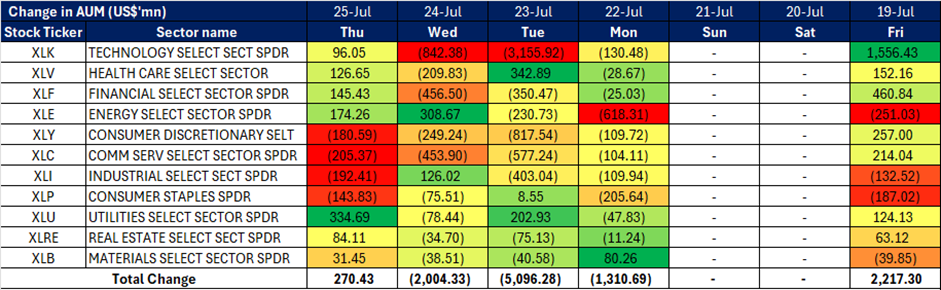

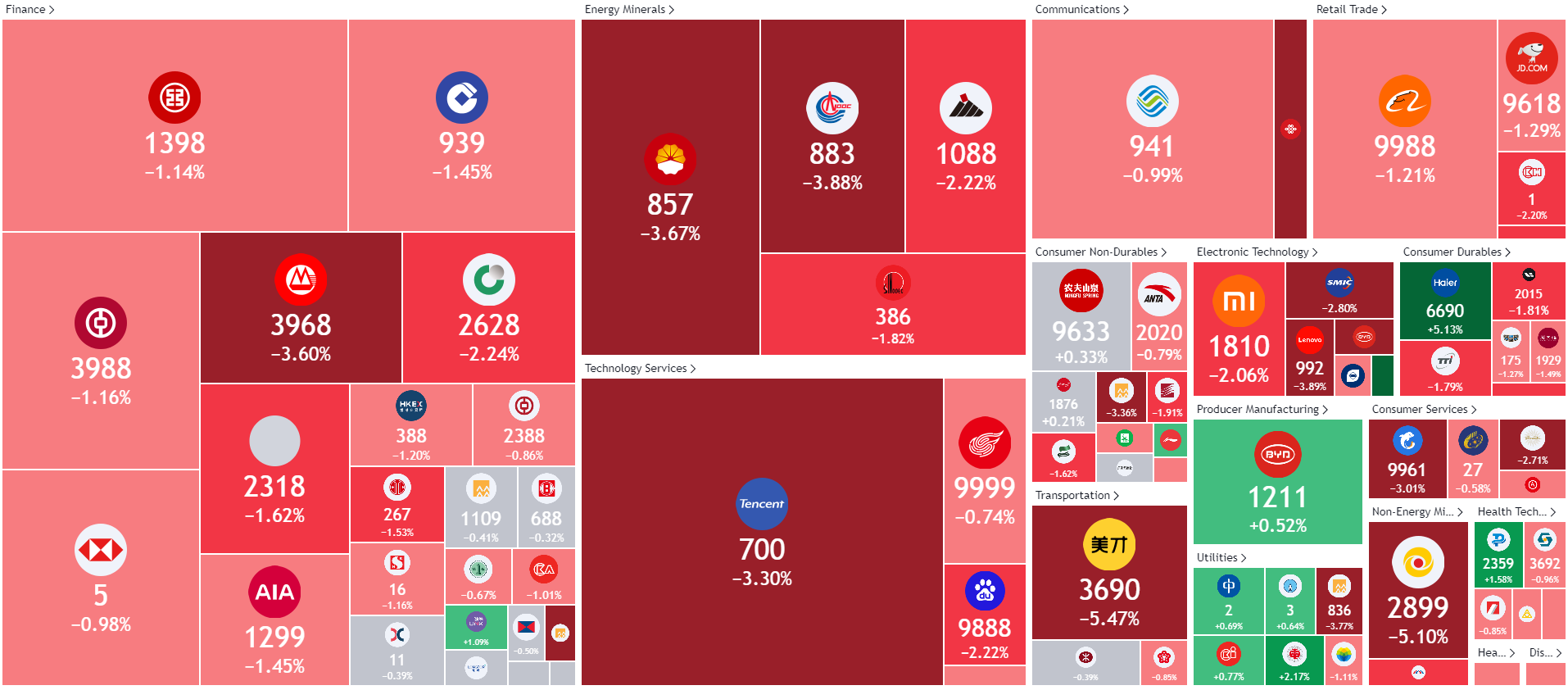

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

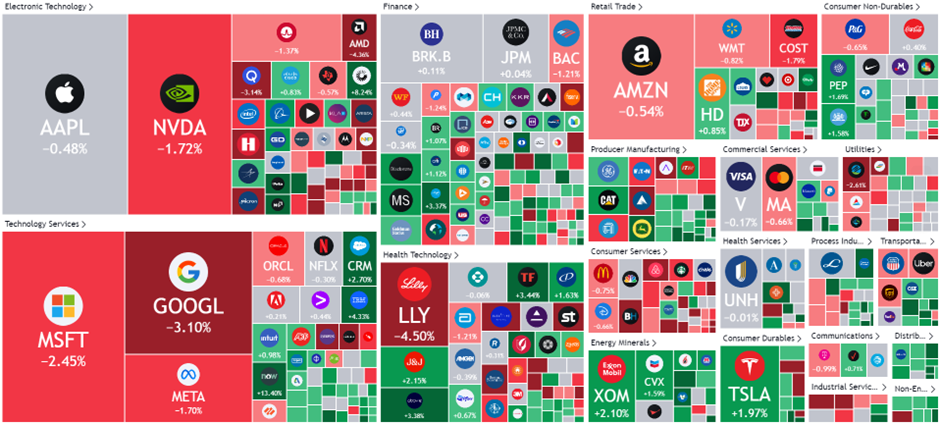

United States

Hong Kong

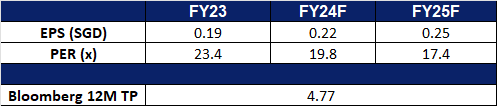

Singapore Technologies Engineering Ltd (STE SP): Deepening collaborations and partnerships

- RE-ITERATE BUY Entry – 4.38 Target– 4.70 Stop Loss – 4.22

- ST Engineering Ltd is a global technology, defence, and engineering group. The Company uses technology and innovation to solve problems and improve lives through its diverse portfolio of businesses across the aerospace, smart city, defence, and public security segments. ST Engineering serves clients worldwide.

- Collaboration to boost Cybersecurity. SPTel, a joint venture between ST Engineering and SP Group, has launched its Quantum-Safe Services, enhancing its National Quantum-Safe Network Plus (NQSN+) by integrating advanced quantum encryption products from ST Engineering, Nokia, and Fortinet. This initiative aims to provide comprehensive network protection against quantum threats. Appointed by Singapore’s Infocomm Media Development Authority, SPTel and SpeQtral are developing Southeast Asia’s first quantum-safe infrastructure, supporting the nation’s Digital Connectivity Blueprint. The services, designed for compatibility with existing IT infrastructures, secure data across physical, data link, and network layers using Nokia’s DWDM, ST Engineering’s encryptors, and Fortinet’s next-generation firewall. This initiative addresses the emerging “harvest now, decrypt later” threat and aims to fortify cyber defences in critical industries such as healthcare and finance. As cyber threats continue to rise globally, the demand for such services will increase, which would be beneficial for the adoption of ST Engineering’s encryptors.

- Strong order book. ST Engineering’s order book remains robust, valued at $27.7bn as of its first quarter 2024 business updates. The company anticipates delivering $6.5bn worth of orders for the remainder of the year. In the first quarter of 2024, ST Engineering secured additional contracts totaling $3.0bn. This includes $839 mn in the commercial aerospace sector, $1,645mn in the defense and public security market, and $542mn in the urban solutions and satcom industry. These new contract wins, along with a consistently strong order book, highlight the sustained high demand for ST Engineering’s services.

- Deepening LEAP engine support for Safra Aircraft Engines. ST Engineering recently announced that its Commercial Aerospace business has deepened its support for Safran Aircraft Engines1 by entering into a two-year agreement, with an option for extension, to provide module repair offload support for the CFM LEAP-1A and LEAP-1B engines. Under the agreement, Safran Aircraft Engines will offload module repair work on the high pressure turbine (HPT) rotor assembly and stage 2 HPT nozzle assembly of the LEAP-1A and LEAP-1B engines to ST Engineering. This collaboration addresses the growing MRO demand for LEAP engines as operators ramp up their flying operations. ST Engineering’s offload support augments Safran Aircraft Engines’ MRO capacity and optimises the turnaround time of engine shop visits for customers. This agreement strengthens the partnership with Safran Aircraft Engines and support for LEAP engines operators, and well positions the company to address the rising demand for quick-turn and performance restoration shop visits for LEAP engines.

- 1Q24 results review. Revenue rose by 18% YoY to S$2,703mn in 1Q24, compared to S$2,289mn in 1Q23, driven by double-digit YoY growth in its commercial aerospace and defence and public security segments. In the first quarter, its commercial aerospace revenue and defence and public security revenue grew 32% YoY to S$1.2bn and 14% YoY to S$1.1bn respectively.

- Market Consensus.

(Source: Bloomberg)

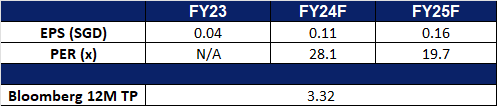

SATS Ltd (SATS SP): Service improvement amidst air travel recovery

- RE-ITERATE BUY Entry – 3.08 Target– 3.40 Stop Loss – 2.94

- SATS Ltd. provides gateway services and food solutions. The Company specializes in airfreight, ramp and baggage handling; passenger services; aviation security services; aircraft cleaning; and cruise centre management. It also provides airline catering; institutional catering; aviation laundry; and food distribution and logistics. SATS has presence across Asia and the Middle East.

- Air passenger traffic not slowing. According to the International Air Transport Association, in 2024, the airline industry has recovered from the COVID-19 crisis, with total traffic surpassing 2019 levels in February. Domestic travel returned to pre-COVID levels in spring 2023, while international routes have also recently recovered. Most regions are expected to exceed 2019 levels in 2024, with Asia Pacific leading growth at 17.2% YoY. Over the next 20 years, global passenger journeys are expected to increase by an average of 3.8% annually, resulting in over 4 billion additional journeys by 2043 compared to 2023. This yearly rise in global travel will contribute to SATS revenue growth in the coming years.

- Business restructuring. SATS recently announced the division of its airport ground handling services into separate units for Singapore and the Asia-Pacific region to stimulate company growth. The restructuring of its Gateway Services business resulted in the creation of two new units: the Singapore Hub and Gateway Services Asia-Pacific. The Singapore Hub will focus on enhancing aviation hub competitiveness in Singapore, while Gateway Services Asia-Pacific will aim to expand the group’s market share by managing operations in overseas airports.

- Lounge improvements. SATS unveiled its upgraded Premier Lounge at Changi Airport Terminal 3 recently, featuring Singaporean dishes like laksa, chicken rice, and prawn noodles, along with interior designs by local artists and students. The lounge includes a new Executive space with private pods, dining service, and travel-friendly amenities. SATS plans to extend similar refurbishments to its other lounges in Terminals 1 and 2 over the next few years. The lounge also offers pasta made by robot chefs, products from SATS Gourmet Solutions, and collaborations with six renowned local food and beverage brands. SATS CEO highlighted the aim to enrich travellers’ experiences with a blend of food, culture, and hospitality. Refurbishments to the lounges in different terminals will offer more comfort and incentive for travellers at Singapore Changi Airport to visit the lounges.

- FY24 results review. Total revenue rose by 192.9% YoY to S$5.15bn in FY24, compared to S$1.76bn in FY23. Core PATMI rose by 331.3% to S$78.5mn in FY24, compared to S$18.2mn in FY23. Basic EPS was 3.8 Scents in FY24, compared to -2.2 Scents in FY23.

- Market Consensus.

(Source: Bloomberg)

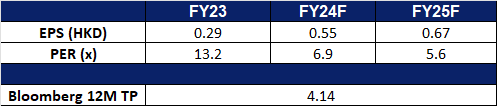

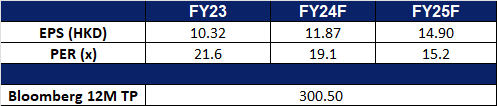

Goldwind Science & Technology Co Ltd. (2208 HK): Wind power is favourable again

- BUY Entry – 3.80 Target 4.20 Stop Loss – 3.60

- Goldwind Science & Technology Co Ltd, formerly Xinjiang Goldwind Science & Technology Co Ltd, is a China-based company that provides overall solutions for wind turbines, wind power services and wind farm development. The Company operates its businesses through four segments. The Wind Turbine Manufacturing and Sales segment is mainly engaged in the research and development, manufacturing and sales of wind turbines and their parts. The Wind Power Service segment mainly provides wind power-related consultants, wind farm construction and maintenance and transportation services. The Wind Farm Development segment is mainly engaged in the development and operation of wind farms. Other segment is mainly engaged in financial leasing and water treatment development and operation business. The Company conducts its businesses both in the domestic market and overseas markets.

- Increasing use of renewable energy in China. China’s renewable energy utilization has reached or exceeded advanced international levels, demonstrating rapid progress in sustainable energy. The country has maintained strong momentum in renewable energy adoption, with a utilization rate of 97.6%, surpassing 95% for six consecutive years since 2018. Last year, newly installed renewable energy capacity rose to 290 million kW, 2.4 times that of 2022, accounting for 79% of the total new power generation capacity nationwide, making it the primary source of new power generation. This surge in capacity has spurred significant investments in solar, wind, and hydropower projects across the country. These efforts are part of China’s broader strategy to peak carbon emissions before 2030 and achieve carbon neutrality before 2060. Goldwind is likely to benefit from the increased investment and spending in renewable energy.

- Expanding presence. Goldwind Science & Technology recently acquired its first overseas wind turbine manufacturing plant in Brazil. In May, the company finalized an agreement with General Electric to acquire the Camacari assembly plant in Bahia state. The plant is set to begin mass production of wind turbines by the end of 2024, creating over 1,000 jobs in the region. Goldwind highlighted that this investment will enhance local supply chains and capitalize on the region’s abundant wind resources.

- Project in the Philippines. In May, Goldwind signed an agreement with Singapore-based renewables developer The Blue Circle to supply turbines for a 100.8-MW wind project in the Philippines. Under the agreement, Goldwind will supply, commission, and service 17 units of its GW 165-6.0 MW wind turbines for The Blue Circle’s Kalayaan 2 project in Laguna Province. The contract also includes ten years of service for the turbines.

- 1Q24 earnings. The company’s operating revenue rose to RMB6.98bn in 1Q24, +25.42% YoY, compared to RMB5.56bn in 1Q23. The company’s net profit fell by 73.06% YoY to RMB332mn, compared to RMB1.23bn in 1Q23. Basic earnings per share fell to RMB0.0726 in 1Q24, compared to RMB0.286 in 1Q23.

- Market consensus.

(Source: Bloomberg)

BYD Co Ltd. (1211 HK): Aggressive expansion

- RE-ITERATE BUY Entry – 233 Target 253 Stop Loss – 223

- BYD Co Ltd. is a China-based company principally engaged in the manufacture and sales of transportation equipment. The Company is also engaged in the manufacture and sales of electronic parts and components and electronic devices for daily use. The Company’s products include rechargeable batteries and photovoltaic products, mobile phone parts and assembly, and automobiles and related products. The Company mainly conducts its businesses in China, the United States and Europe.

- Expansion in Vietnam. BYD recently unveiled its plans to aggressively expand its dealership network in Vietnam, posing a formidable challenge to local rival VinFast. Last week, the company opened its first 13 dealerships in the country and aims to increase this number to around 100 by 2026. Currently offering three models, BYD plans to expand its lineup to six models by October.

- More manufacturing plants. Earlier this month, BYD opened an electric vehicle plant in Thailand, marking its first factory in Southeast Asia, a rapidly growing EV market where the company has become a dominant player. The $490mn facility will have an annual production capacity of 150,000 vehicles, including plug-in hybrids. It will also assemble batteries and other critical components for BYD’s vehicles. BYD recently signed a $1 billion deal to establish a manufacturing plant in Turkey as part of its ongoing international expansion. The new plant will have an annual production capacity of up to 150,000 vehicles and is expected to begin operations by the end of 2026. This expansion aims to reduce the company’s future expenses by minimizing tariffs and import duties incurred when shipping vehicles from China to the EU.

- Record Sales in 2Q24. BYD sold a record number of electric and hybrid cars in the second quarter, according to sales data compiled by Bloomberg News. Nearly one million vehicles were sold during this period, marking a strong rebound after a slow start to the year. The surge in sales was driven by price cuts and new technology, which spurred consumer purchases. BYD’s strategy of reducing prices across most models, sacrificing profitability, aimed to compete with petrol models from foreign brands.

- 1Q24 earnings. The company operating revenue rose to RMB124.9bn, +3.97% YoY, compared to RMB120.2bn in 1Q23. The company’s net profit rose to RMB4.57bn, +10.62% YoY, compared to RMB4.13bn in 1Q23. Basic earnings per share were RMB1.57 in 1Q24, compared to RMB1.42 in 1Q23.

- Market consensus.

(Source: Bloomberg)

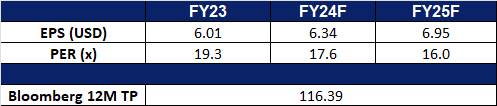

Philip Morris International Inc (PM US): Zynpocalypse

- BUY Entry – 110 Target – 122 Stop Loss – 104

- Philip Morris International Inc. (PMI) operates as a tobacco company working to deliver a smoke-free future and evolving its portfolio for the long term to include products outside of the tobacco and nicotine sector. The Company offers cigarettes, e-vapor, and oral smoke-less products. Philip Morris International serves customers worldwide.

- Signs of recession benefitting defensive stocks. Recent US economic data points to a potential slowdown. While inflation is cooling, the labour market is softening, consumer spending and confidence are waning, and manufacturing is contracting. These factors have spurred concerns about a soft economic landing, leading to sharp corrections in growth sectors and a shift of investor funds towards more defensive assets.

- Business transformation. The company has successfully pivoted in response to the global anti-smoking movement. By aggressively marketing smoke-free and heated tobacco products, it has not only survived but thrived. This quarter, canned oral product shipments surged 23.5%, primarily driven by nicotine pouches, while heated tobacco product sales climbed 10.2% globally, with particular strength in Japan (up 12.5%) and Europe (up 6.8%). However, a European Union ban on flavoured heated tobacco has forced a downward revision of IQOS’s full-year growth forecast to 13%. Despite this, the company remains optimistic, with the CEO highlighting strong business momentum and raising full-year earnings per share guidance to between US$6.67 and US$6.79. The company expects further revenue growth in the second half, driven by nicotine pouch expansion, IQOS launches in new markets, and rising cigarette prices.

- Investing heavily to address the Zyn shortage. Philip Morris’ US$600mn commitment to a new Colorado manufacturing facility underscores the surging demand for its nicotine pouches. Acquired from Swedish Match for US$16bn in 2022, Zyn has become a major growth driver, even popular among Wall Street professionals. Despite supply chain challenges, including a temporary halt to online sales, Zyn sales soared 50.3% YoY in Q2. To meet this unprecedented demand, Philip Morris is expanding production capacity and has raised its annual sales target to 580 million cans from the previous 560 million cans.

- 2Q24 earnings review. Revenue rose by 5.6% YoY to US$9.47bn, beating estimates by US$280mn. Non-GAAP earnings per shares was US$1.59 beating expectations by US$0.03. For FY24, the company expects full-year adjusted EPS of US$6.33 to US$6.45 vs. US$6.33 consensus and the prior forecast of US$6.26 to US$6.38.

- Market consensus.

(Source: Bloomberg)

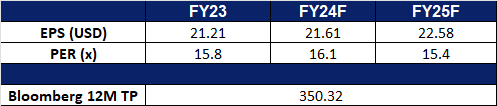

Caterpillar Inc (CAT US): Rotation to infrastructure

Caterpillar Inc (CAT US): Rotation to infrastructure

- RE-ITERATE BUY Entry – 346 Target – 382 Stop Loss – 328

- Caterpillar Inc. designs, manufactures, and markets construction, mining, and forestry machinery. The Company also manufactures engines and other related parts for its equipment, and offers financing and insurance. Caterpillar distributes its products through a worldwide organization of dealers.

- Interest rate cut cycle to benefit mining activities and real estate development. Stimulated by expectations of interest rate cuts, major base metals and precious metals have performed well this year. Copper prices once hit a record high, and aluminium prices also hit a two-year high; they are currently experiencing a correction, but they still maintain positive returns year-to-date. Gold prices recently broke through a record high of US$2,450 per ounce, while silver prices maintained a high of US$30 per ounce. It is expected that precious metals will continue to maintain an upward trend after the interest rate cut cycle starts, thus stimulating mining companies to increase mining activities, thereby driving demand for related construction machinery. In addition, real estate development is expected to recover under the interest rate cut cycle, thereby stimulating construction activities, which will in turn benefit the construction machinery sector.

- Sector rotation. The recent US election has had a greater impact on the stock market, and funds have begun to deploy Trump-themed transactions. Trump advocates the return of manufacturing to the United States, and the infrastructure industry is one of the profit sectors. In addition, Trump also advocates expanding US infrastructure. Looking back at Caterpillar’s performance during Trump’s administration, it hit a record high in the year after he entered the White House, with a return of more than 90% in the same year.

- 1Q24 earnings review. Revenue fell by 0.6% YoY to US$15.8bn, missing estimates by US$190mn. Non-GAAP earnings per shares was US$5.60 beating expectations by US$0.47.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add Singapore Technologies Engineering Ltd. (STE SG) at S$4.38 and BYD Co. Ltd. (1211 HK) at HK$233.0. Cut loss on Sunny Optical Technology Group (2382) at HK$46.10 and Zillow Group (Z US) at US$49.0.