Trading Ideas 26 February 2025 : Singapore Technologies Engineering Ltd (STE SP), China Mobile Ltd (941 HK), Palo Alto Networks Inc (PANW US)

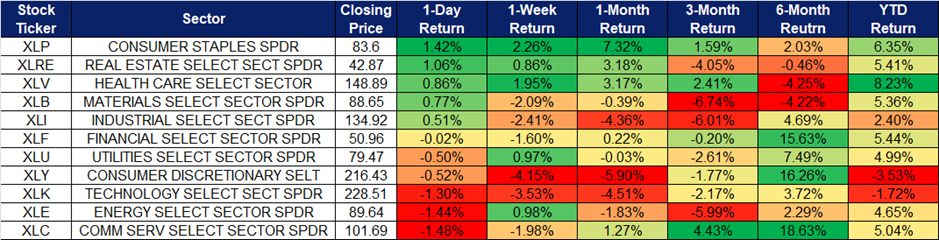

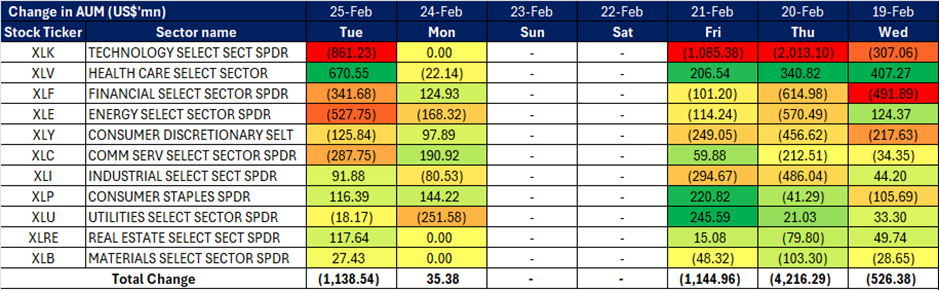

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

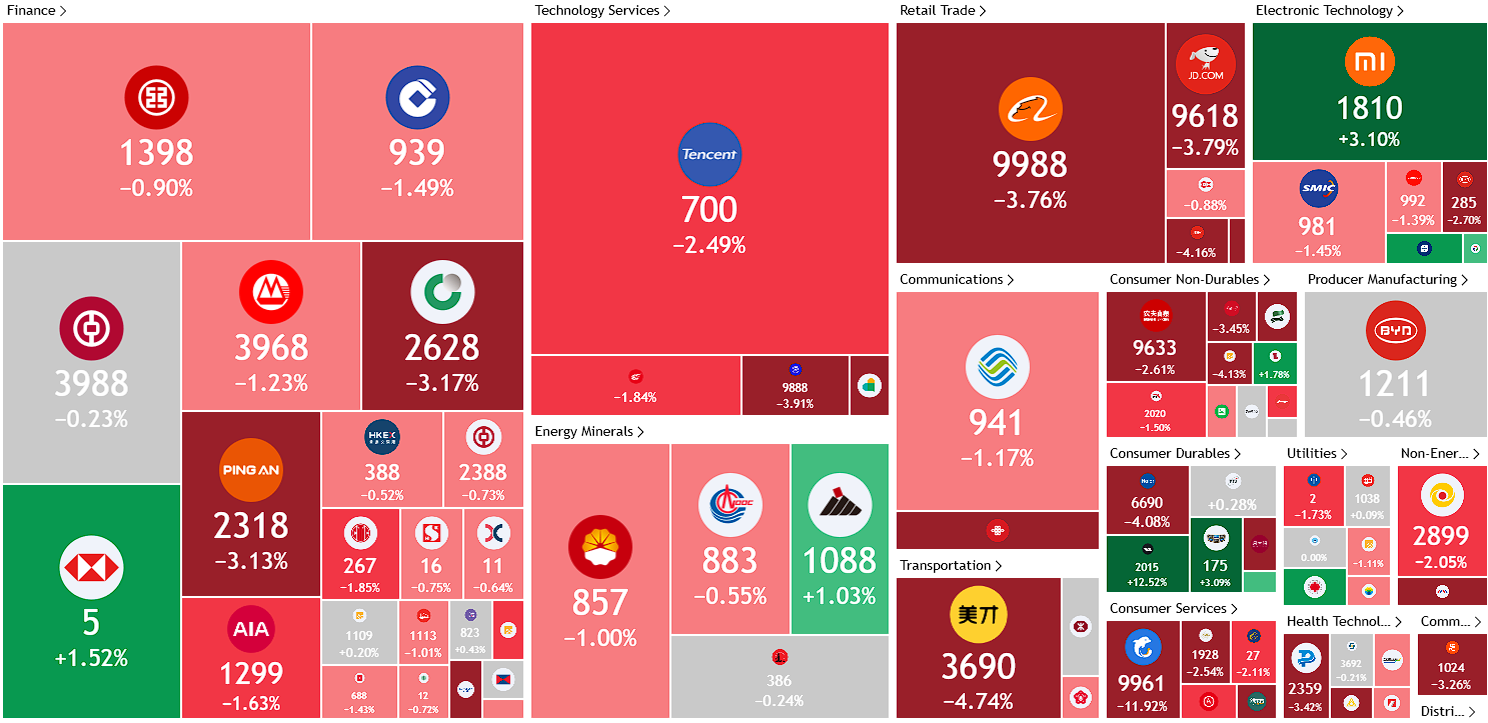

Hong Kong

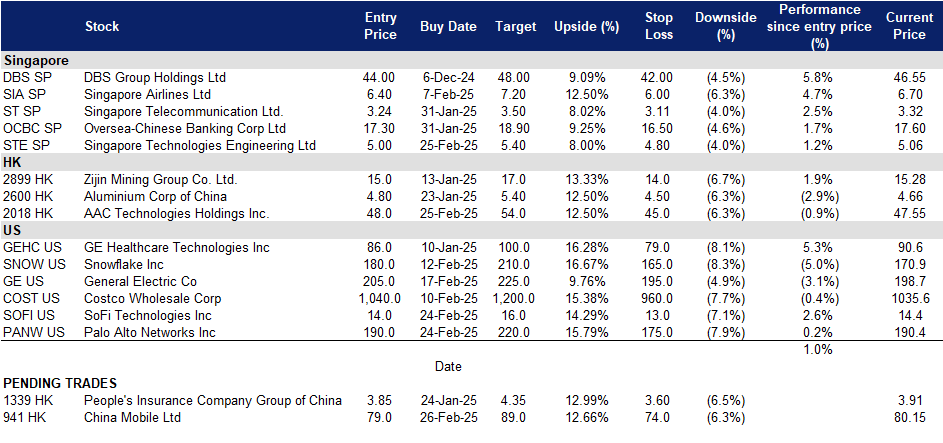

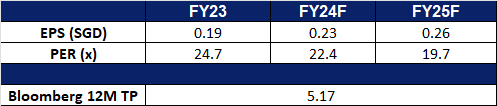

Singapore Technologies Engineering Ltd (STE SP): New Contracts in 4Q24

- RE-ITERATE BUY Entry – 5.00 Target – 5.40 Stop Loss – 4.80

- ST Engineering Ltd is a global technology, defence, and engineering group. The Company uses technology and innovation to solve problems and improve lives through its diverse portfolio of businesses across the aerospace, smart city, defence, and public security segments. ST Engineering serves clients worldwide.

- S$4.3 Billion in New Contracts. Earlier this month, ST Engineering announced that it secured S$4.3 billion in new contracts during 4Q24. This includes S$1.8 billion from its commercial aerospace segment, S$1.7 billion from the defense and public security segment, and S$700 million from urban solutions and satcom. The commercial aerospace division secured multiple contracts across its maintenance, repair, and overhaul (MRO) and aerostructures and systems sub-units, including a 15-year exclusive agreement with Akasa Air, a low-cost airline based in India. The continued strength of its order book underscores ST Engineering’s solid market position and sustained demand for aerospace solutions, driven by robust aviation industry growth.

- LEAP-1B MRO Contract with Korean Air. ST Engineering’s commercial aerospace business has signed a five-year MRO contract to support the CFM LEAP-1B engines powering Korean Air’s Boeing 737 MAX fleet. This marks the company’s first contract with South Korea’s flag carrier. Under the agreement, ST Engineering will provide quick-turn services, including high-pressure turbine (HPT) repairs and Performance Restoration Shop Visit (PRSV) services, from its MRO facility in Singapore. The contract reinforces Korean Air’s confidence in ST Engineering as a trusted partner for high-quality engine services, supporting the airline’s long-term growth plans.

- Strategic Partnership with Kazakhstan Paramount Engineering (KPE). ST Engineering’s international defense business has secured a strategic partnership with Kazakhstan Paramount Engineering (KPE) to establish production capabilities for a new military vehicle. The amphibious, multi-purpose armored vehicle will be manufactured at KPE’s facility in Kazakhstan, based on ST Engineering’s battle-proven Terrex Infantry Fighting Vehicle, designed to operate effectively in open water conditions. ST Engineering will provide engineering and technical support for production, which is set to begin in 2025. This marks the company’s entry into the Central Asian market—its first defense vehicle contract with a licensed partner in the region—reinforcing its strategy to drive growth through localization, in-country support, and industry partnerships.

- 3Q24 results review. Revenue rose by 14.3% YoY to S$2,782mn in 3Q24, compared to S$2,433mn in 3Q23, driven by double-digit YoY growth in its commercial aerospace and defence and public security segments. In the 3rd quarter, its commercial aerospace revenue and defence and public security revenue grew 30.8% YoY to S$1.27bn and 7.3% YoY to S$1.05bn respectively.

- Market Consensus.

(Source: Bloomberg)

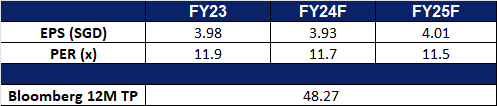

DBS Group Holdings Ltd (DBS SP): Budget’25 to boost economy

- RE-ITERATE BUY Entry – 44 Target– 48 Stop Loss – 42

- DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

- Potential benefits from budget. On 18 February, Prime Minister Lawrence Wong announced a bonanza of vouchers, credits, tax rebates and enhanced wage support for Singaporeans and corporations. Singapore’s budget 2025 introduced measures that could bolster local banks by stimulating economic activity and improving credit conditions. Infrastructure investments, including top-ups to key funds, are likely to drive higher loan demand. The 50% corporate tax rebate for SMEs may ease financial pressures, reducing asset quality risks for banks. Consumer-focused initiatives could support spending while mitigating inflationary risks, lowering non-performing loans. Additionally, incentives for SGX listings and fund management may enhance capital market activity, benefiting banks through increased trading volumes and demand for financial products. Overall, the budget measures are expected to create a favourable environment for Singapore banks, driving loan growth, improving asset quality, and supporting broader financial sector activity.

- Leadership changes ahead of CEO transition. DBS Bank has appointed Derrick Goh as its first Group Chief Operating Officer (COO), effective 1 April, overseeing operations and transformation. He will also join the bank’s executive committee. Koh Kar Siong will take over as head of audit and join the management committee. Additionally, Jimmy Ng, current head of operations, will retire on 1 July but continue as a senior adviser for AI until year-end. These changes come as Piyush Gupta prepares to step down as CEO on 28 March, with Tan Su Shan, deputy CEO since August 2024, set to succeed him. The leadership changes at DBS Bank signal a strategic transition aimed at sustaining growth and strengthening its operational and digital transformation efforts. DBS’ leadership changes reinforce its commitment to operational efficiency, and governance, ensuring continued growth amid evolving global banking trends. The bank is well-positioned for sustained profitability and market leadership under its new executive team.

- Special bonus and capital return amid record profits. DBS will distribute a one-time S$1,000 bonus to all staff except senior managers, totaling S$32 million, as a reward for their contribution to its record performance. This bonus will benefit 90-95% of employees. The bank also announced a capital return dividend of S$0.15 per share per quarter for FY25, with plans for similar distributions over the next two years. This is part of its strategy to reduce excess capital through dividends, special payouts, and share buybacks. For 4Q24, DBS reported a net profit of S$2.52 billion, 11% YoY increase, bringing its full-year net profit to a record S$11.29 billion, up 12% YoY. Despite macroeconomic uncertainty, interest rate trends and geopolitical risks, DBS managed to outperform expectations. We believe that the bank remains well-positioned for long-term growth, backed by record earnings, strong leadership succession, and continued investment in technology.

- 4Q24 results review. Total income for 4Q24 rose 11% to S$5.51bn and net profit rose 11% YoY to S$2.52bn, compared with S$2.27bn from the year-ago period. DBS’ full-year net profit was brought to a new record high of S$11.29bn, up 12% from the year-ago period. DBS declared Q4 dividend at S$0. 0.15 per share per quarter to be paid out over financial year 2025; it expects to pay out a similar amount of capital in the next two years.

- Market Consensus.

(Source: Bloomberg)

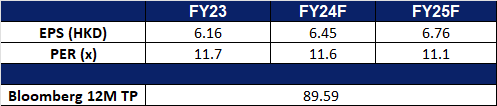

China Mobile Ltd (941 HK): Riding the AI wave

- BUY Entry – 79.0 Target – 89.0 Stop Loss – 74.0

- China Mobile Ltd is a company mainly engaged in the provision of communication and information services. The Company’s businesses include customer market business, home market business, business market business and new market business. The customer market business mainly provides fifth-generation mobile communication technology (5G) mobile services and brand differentiated service operations. The home market business mainly provides home wired broadband services, mobile housekeeping smart services and smart home value-added services. The business market business is engaged in the research and development and sales of cloud computers and Internet of Things card services. The new market business includes international business, equity investment, digital content and financial technology.

- AI integration. Earlier this month, China Mobile, along with other major Chinese telecom companies, announced the integration of DeepSeek’s artificial intelligence (AI) models into their services and products. The move follows a broader trend among the country’s top tech firms, including Alibaba Group, Tencent Holdings and Baidu Inc, which have ramped up support for DeepSeek’s latest AI models on their respective platforms. While these telecom giants have been developing their own large language models (LLMs) over the past two years amid a global AI boom spurred by OpenAI, they primarily leverage DeepSeek’s models for cloud-based applications. China Mobile, in particular, has incorporated DeepSeek’s full suite of models—from DeepSeek-V1 to the latest DeepSeek-R1—into its computing platform. This enables businesses of all sizes to access the models, deploy application programming interfaces (APIs), and build new AI agents on its platform.

- Growth in smart devices and 5G adoption. China’s mobile phone market experienced robust growth in 2024, with total shipments increasing by 8.7% to 314 million units. Notably, December 2024 saw a significant YoY surge of 22.1%, reaching 34.53 million units. 5G smartphones dominated the market, accounting for 88.1% of December shipments and 86.6% of total annual shipments. This trend is supported by China’s rapidly expanding 5G infrastructure, which now includes over 4.25 million 5G base stations and serves more than 1 billion 5G users. The rise in smart device adoption, particularly 5G-enabled phones, is expected to drive an expansion of China Mobile’s customer base, as more users seek high-speed connectivity and advanced mobile services.

- Strategic cooperation agreement to deepen AI development. China Mobile recently announced a strategic cooperation agreement with Chengdu City to deepen collaboration across multiple sectors. Under this agreement, the two parties will enhance infrastructure development in AI, 5G-A, and next-generation networks, drive technological innovation and commercialization, and strengthen partnerships in areas such as supply chains, industrial investment, and intelligent hardware. They will also explore opportunities in smart cities, the data industry, 5G-powered industrial internet applications, and the low-altitude economy, fostering high-quality growth in Chengdu’s electronic information and audio-entertainment industries. This initiative is expected to further position China Mobile to capitalize on China’s expanding AI landscape.

- 9M24 earnings. Revenue rose by 2.0% YoY to RMB791.5bn in 9M24, compared to RMB775.6bn in 9M23. Profit attributable to equity shareholders was RMB110.9bn, up by 5.1% YoY from RMB105.5bn. Basic earnings per share was RMB5.18 in 9M24, compared to a basic earnings per share of RMB4.94 in 9M23.

- Market consensus.

(Source: Bloomberg)

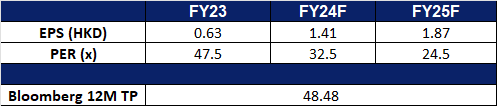

AAC Technologies Holdings Inc. (2018 HK): New Iphone 16e

- RE-ITERATE BUY Entry – 48.0 Target – 54.0 Stop Loss – 45.0

- AAC Technologies Holdings Inc is a China-based investment holding company. The Company operates its businesses through four segments: Optics Business segment, Acoustics Business segment, Electromagnetic Drives/Precision Mechanics Business segment and Micro Electro-Mechanical Systems (MEMS) Business segment. The Company’s main products include acoustic products, electromagnetic drives and precision mechanics, optic products and MEMS components and other products.

- Apple’s Budget AI Phone. Apple has unveiled the iPhone 16e—a budget-friendly smartphone infused with AI capabilities—targeting mid-market consumers both domestically and in key growth regions such as China and India. Abandoning the previous SE naming, this model directly challenges popular Android devices at a time when competitors like Samsung and Huawei are rapidly integrating AI features. Priced to start at US$599—a US$170 increase over the former entry-level model—the iPhone 16e offers features nearing those of Apple’s flagships, including a high-performance chip that powers Apple Intelligence with ChatGPT-like access. This competitive pricing lowers the barrier for adopting Apple’s AI ecosystem, potentially boosting sales and benefiting suppliers like AAC Technologies.

- Positive Profit Alert. AAC Technologies recently issued a profit alert, citing a strong recovery in the global smartphone market, a shift toward higher-specification products that improved its product mix, and enhanced operational efficiency. The company now expects its net income to rise to between RMB1,700mn and RMB1,815mn —a YoY increase of roughly 130% to 145%. Furthermore, the successful completion of the first tranche acquisition of Acoustics Solutions International B.V. in February 2024 has added to the Group’s profit and bolstered its growth prospects in the automotive market. This strong financial position allows the company to continue driving growth in its business.

- CES 2025 Showcase. At CES 2025, the world’s largest consumer electronics and technology event, AAC Technologies demonstrated groundbreaking advances in sensory interaction across visual, audio, and haptic domains. The company presented its extensive portfolio, featuring innovations in smart automotive systems, acoustics, haptics, XR, optics, precision manufacturing, micro-motors, VCM, sensors, and semiconductors. With a broad range of self-developed products and solutions designed for diverse applications, AAC Technologies once again set new industry benchmarks—a move expected to attract heightened attention across multiple sectors and further strengthen its market position.

- 1H24 earnings. Revenue rose by 22.0% YoY to RMB11.2bn in 1H24, compared to RMB9.22bn in 1H23. Net profit rose significantly YoY to RMB537mn in 1H24, compared to RMB150mn in 1H23. Basic EPS rose to RMB0.46 in 1H24, compared to RMB0.13 in 1H23.

- Market consensus.

(Source: Bloomberg)

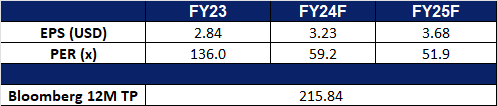

Palo Alto Networks Inc (PANW US): Solidifying its position in network security

- RE-ITERATE BUY Entry – 190 Target – 220 Stop Loss – 175

- Palo Alto Networks, Inc. provides network security solutions. The Company offers firewalls that identify and control applications, scan content to stop threats, prevent data leakage, integrated application, user, and content visibility. Palo Alto Networks serves customers worldwide.

- Global cloud spending expected to grow rapidly in 2025. According to Gartner’s latest forecast, global end-user spending on public cloud services is expected to grow from US$595.7bn in 2024 to US$723.4bn in 2025. Spending on cybersecurity is projected to increase from US$183.9bn in 2024 to US$212.0bn in 2025. With the widespread adoption of artificial intelligence, more investments are flowing into the security software market, including application security, data security and privacy protection, and infrastructure protection. The cybersecurity market is expected to grow at a compound annual growth rate (CAGR) of 11% until 2030.

- Leading player in the firewall market. The company holds a 20% market share in the firewall industry, serving over 80,000 customers worldwide, including large enterprises, government agencies, and financial institutions. The company maintains a customer retention rate of over 90%, demonstrating the high demand and stability of its products. Its cloud security platform, including Prisma Cloud and Cortex XSOAR, is expanding rapidly in the market. In 4Q24, Prisma Cloud achieved a 38% YoY growth rate.

- Rule of 40. The Rule of 40 is a key metric for measuring the profitability and growth of Software-as-a-Service (SaaS) companies. In the most recent quarter, the sum of the company’s revenue growth rate and EBITDA profit margin reached 48.6, reflecting strong performance.

- 2Q25 results. Revenue grew 14.1% YoY to US$2.26bn, beating estimates by US$20mn. Non-GAAP EPS was US$0.81, exceeding expectations by US$0.03. The company raised its FY25 revenue forecast to US$9.14bn – US$9.19bn, up from the previous guidance of US$9.12bn – US$9.17bn.

- Market consensus

(Source: Bloomberg)

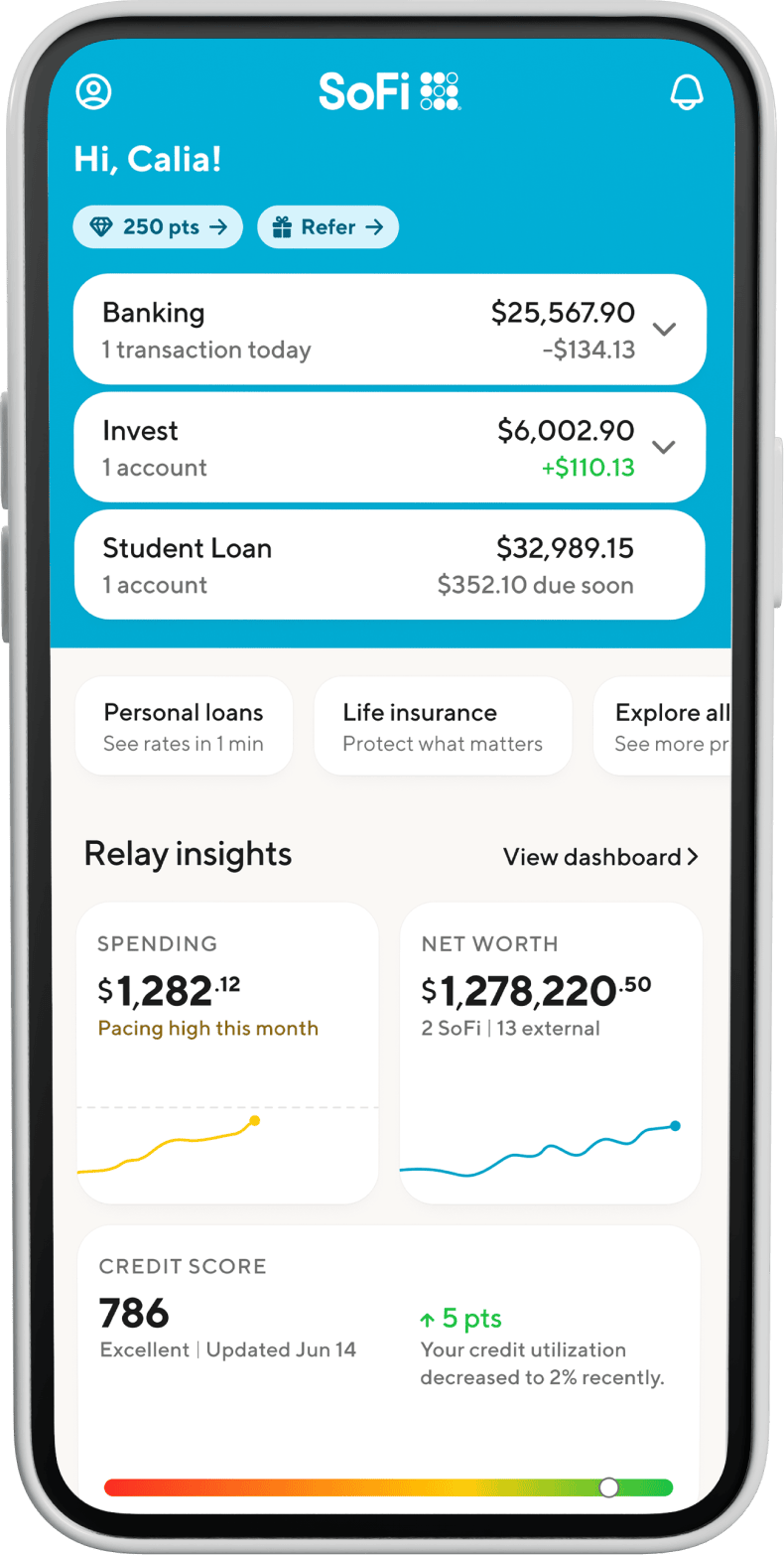

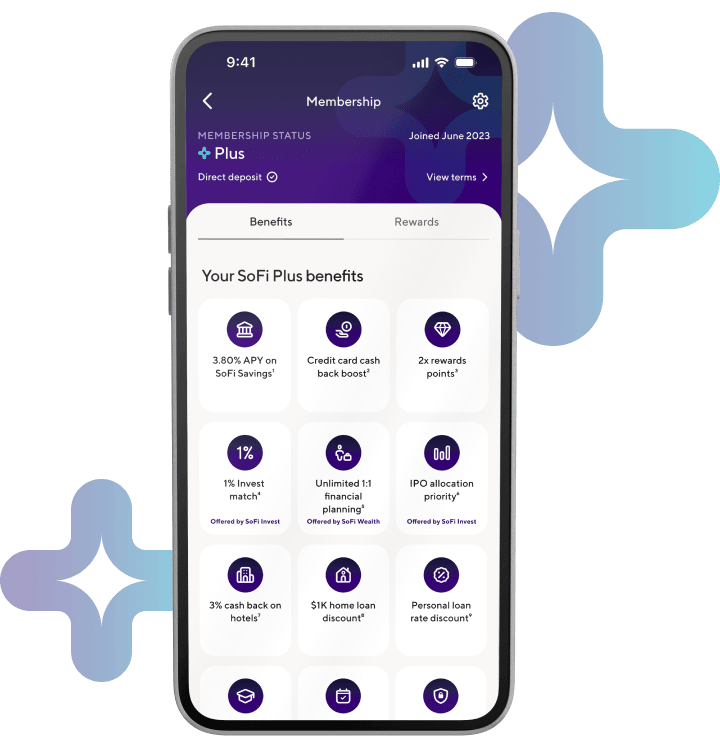

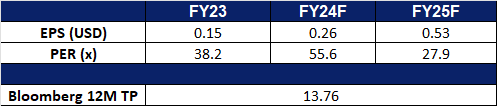

SoFi Technologies Inc (SOFI US): Unlock rewarding financial membership

SoFi Technologies Inc (SOFI US): Unlock rewarding financial membership

- RE-ITERATE BUY Entry – 14 Target – 16 Stop Loss – 13

- SoFi Technologies, Inc. is an online personal finance company and online bank. The Company provides financial products including student and auto loan refinancing, mortgages, personal loans, credit card, investing, and banking through both mobile app and desktop interfaces. SoFi Technologies serves customers in the United States.

- Introduction of plus premium membership. SoFi Technologies introduced over eight new benefits to its premium financial membership, SoFi Plus, providing members with over US$1,000 in annual value. These benefits include preferred pricing on products and services, complimentary financial planning, rewards, and access to special events, Members can access SoFi Plus for US$10/month or for free with direct deposit. To mark the launch, SoFi introduced the ‘Power of Plus’ sweepstakes, giving six winners the opportunity to achieve major financial milestones, such as purchasing a home, paying off student debt, or funding a dream vacation. Existing perks, like preferred IPO allocations, a high APY on savings, and boosted cash back rewards on credit cards, remain available. The introduction of these enhanced benefits and the sweepstakes represents a strategic effort by SoFi to grow its customer base, increase Assets Under Management (AUM), and strengthen its competitive position in the digital financial services market. By offering tangible value and aligning with customers’ financial aspirations, SoFi aims to drive customer acquisition, retention, and engagement, while solidifying its edge over competitors. This initiative positions SoFi as a member-centric financial platform, well-equipped to expand its market share and reinforce its reputation in the industry.

SoFi Mobile Interface SoFi Plus

(Source: SoFi)

- Competitive edge. Despite providing weaker-than-expected quarterly and full-year guidance, SoFi’s “one-stop shop” approach and user-friendly digital platform differentiate it from traditional financial institutions, attracting a tech-savvy and potentially underserved customer base. It’s strategy of offering a wide range of financial products and services, such as lending, investing, banking, insurance, financial planning is paying off. Its financial services segment saw remarkable 84% revenue growth, indicating successful product expansion.

- Rapid growth. SoFi demonstrated impressive growth in 4Q24, with record new member additions of 785,000 and a total membership exceeding 10.1mn, up 34% YoY. FY24 GAAP revenue increased 26% to US$2.7bn, and adjusted net revenue also grew by 26% to US$2.6bn, driven by strong performance across multiple segments. Total deposits reached US$26bn, with a significant portion coming from direct deposit members, highlighting increasing customer engagement and stickiness. Management anticipates continued strong member growth in 2025, projecting at least 2.8 million new members, a 28% YoY increase.

- 4Q24 results. Revenue grew 19.3% YoY to US$734.13mn, beating expectations by US$51.93mn. Non-GAAP EPS of US$0.05, exceeding estimates by US$0.01. Total member and product adds in Q4 reached 785,000 and 1.1mn, respectively, setting new quarterly records. For 1Q25, it expects adjusted revenue of US$725mn to US$745mn and GAAP EPS of US$0.03. FY25 the company expects to deliver US$3.200bn to US$3.275bn in revenue and GAAP EPS of US$0.25 to US$0.27.

- Market consensus

(Source: Bloomberg)

Trading Dashboard Update: Take profit on Horizon Robotics (9960 HK) at HK$8.6 and IFAST (IFAST SP) at S$8.40. Add Singapore Technologies Engineering Ltd (STE SP) at S$5.00, AAC Technologies Holdings Inc (2018 HK) at HK$48, GDS Holdings Ltd (9698 HK) at HK$47, SoFi Technologies Inc (SOFI US) at US$14 and Palo Alto Networks Inc (PANW US) at US$190. Cut loss on Yidu Tech Inc (2158 HK) at HK$7.5, GDS Holdings Ltd (9698 HK) at HK$43 and Kratos Defense & Security Solutions Inc (KTOS US) at US$24.6.