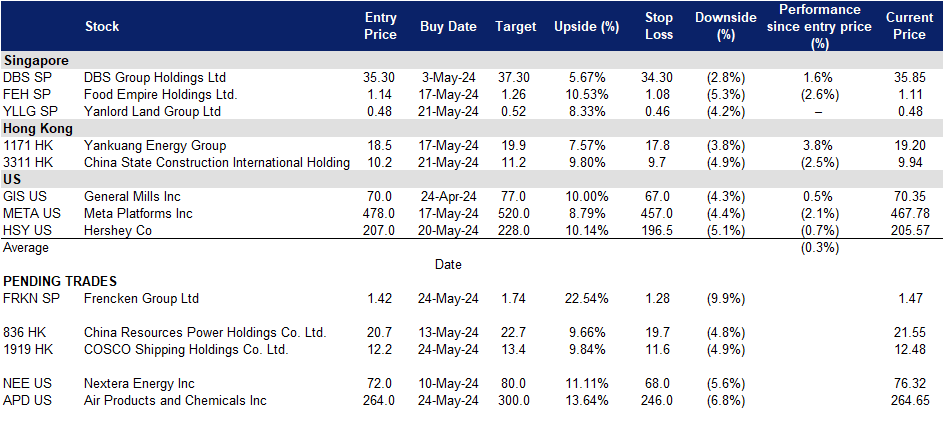

24 May 2024: Frencken Group Ltd (FRKN SP), COSCO Shipping Holdings Co. Ltd. (1919 HK), Air Products and Chemicals Inc (APD US)

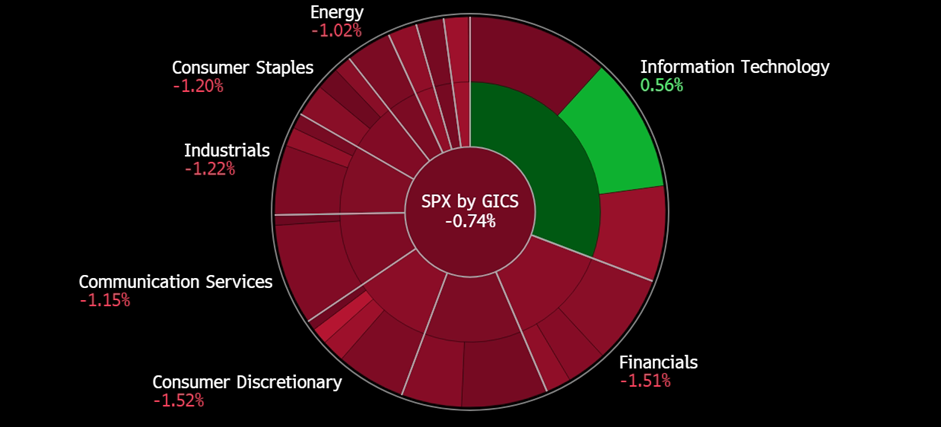

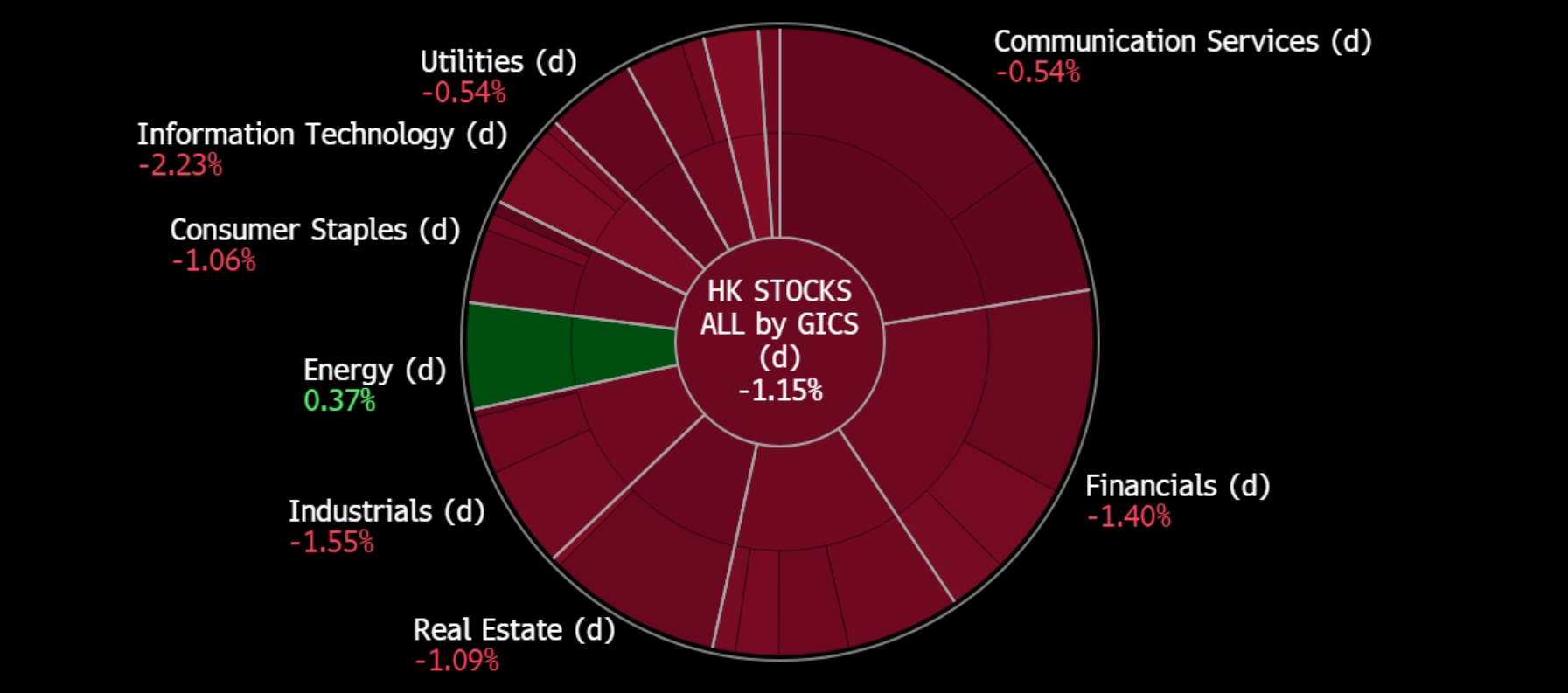

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

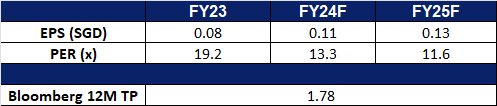

Frencken Group Ltd (FRKN SP): Semicon recovery on-track

- BUY Entry – 1.42 Target– 1.74 Stop Loss – 1.28

- Frencken Group Limited (“Frencken”) is a Global Integrated Technology Solutions Company that is listed on the Main Board of the Singapore Exchange. They provide comprehensive Original Design, Original Equipment, and Diversified Integrated Manufacturing solutions for world-class multinational companies in the analytical & life sciences, automotive, healthcare, industrial, and semiconductor industries.

- Nvidia delivering better than anticipated results again. Nvidia recently reported Q1 results which surpassed estimates, its revenue tripled YoY to US$26bn and it delivered profits that significantly exceeded expectations. The company projected higher-than-expected Q2 revenue of about US$28bn, surpassing analysts’ predictions of US$26.8bn. This positive outlook is driven by the strong demand for AI chips. Its CEO heralded this as the start of a new industrial revolution. Nvidia is currently bolstered by AI accelerators used by major tech firms like Amazon and Google. Despite high demand outpacing supply, Nvidia aims to diversify its market beyond hyperscalers to sectors like healthcare and automotive. This positive demand is expected to extend to Frencken’s semiconductor segment, which represents approximately 41% of its FY revenue.

- Good performance. Frencken Group’s revenue rose 12.2%YoY to S$193.6mn, with the mechatronics division seeing a 14.4% increase to S$170.1mn, primarily from the semiconductor, medical, and analytical life sciences segments. It reported a net profit of S$9mn for 1Q23, up 73% from S$5.2mn the previous year, driven by higher gross profit margins and revenue growth. The IMS division’s revenue remained stable at S$22.8mn, with a decline in the automotive segment offset by a significant increase in the consumer and industrial electronics segment. Gross profit margin improved to 13.7%. The company remains cautious due to global economic uncertainties and expects 1H24 revenue to be comparable to 2H23, with growth in semiconductor, medical, and analytical life sciences segments but softer automotive and industrial automation revenues. Frencken is anticipated to recover alongside the rest of the Semiconductor industry.

- 1Q24 results review. 1Q24 revenue rose by 12.2% to S$193.6mn, compared to S$172.5mn in 1Q23. Net profit increased 73% YoY to S$9mn from S$5.2mn in the previous year due to higher revenue growth and gross profit margins. Gross profit margin improved to 13.7% in 1Q24 from 12.3% in 1Q23, attributing it to better operating leverage. In 1H24, Frencken expects to deliver revenue comparable to 2H23 revenue. The semiconductor, medical, and analytical life sciences segments are expected to improve, while the industrial automation and automotive segments are expected to soften.

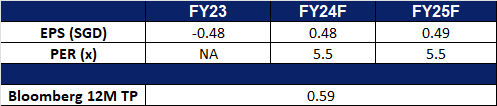

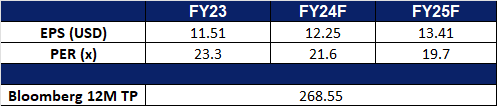

- Market Consensus

(Source: Bloomberg)

Yanlord Land Group Ltd (YLLG SP): More Bail-out measures for property market

- RE-ITERATE BUY Entry – 0.48 Target– 0.52 Stop Loss – 0.46

- Yanlord Land Group Ltd is a real estate development company. The Company develops high-end residential property projects in the Peoples Republic of China.

- Rolling out new measures. China recently announced new measures to revive its struggling property industry after data showed housing prices have dropped nearly 10% since the beginning of the year. Local state-owned enterprises will be asked to purchase unsold homes from distressed developers at significant discounts using loans from state banks, with many of these homes to be converted into affordable housing. The government also emphasized the importance of advancing the “three big projects,” which include affordable housing, urban renovation, and public infrastructure development.

- Lending rates expected to be maintained or lowered. China is anticipated to maintain its benchmark lending rates steady on 20 May. However, there is increasing expectation for a cut in the mortgage reference rate to stimulate the housing market. The survey of 33 market watchers found that 82% expect the one-year and five-year Loan Prime Rates (LPRs) to remain unchanged. The one-year LPR, currently at 3.45%, is primarily used for new and outstanding loans, while the five-year LPR, serving as the mortgage reference rate, stands at 3.95% following a February cut. A minority of respondents predict potential cuts to the five-year LPR by 5 to 20 basis points. Despite industrial output exceeding forecasts, the property sector and weak retail sales continue to weigh on the economy. The central bank recently left a key policy rate unchanged due to a weak currency, complicating further monetary easing. Expectations for a mortgage rate cut are growing following measures aimed at rescuing the property market.

- Lowering requirements for purchase and lower mortgage rates. The People’s Bank of China announced the creation of a 300 billion yuan relending facility for affordable housing and further reductions in mortgage interest rates and down payment requirements. Effective Saturday, the interest rate for first-time housing provident fund loans under five years will be reduced by 0.25 percentage points to 2.35%, while the rate for loans over five years will decrease by 0.25 percentage points to 2.85%. Additionally, the minimum down payment for first homes will be lowered from 20% to 15% of the purchasing price, and for second homes, from 30% to 25%.

- FY23 financial results. Yanlord Land reported higher revenue of RMB43.4bn for FY23, up 51% YoY, compared to RMB28.7bn in FY22. Gross profit rose by 7% to RMB9.29bn, compared with RMB7.75bn in FY22. The company reported a net loss of RMB722mn for FY23, compared to a profit of RMB2.87bn in FY22. Basic earnings per share was -RMB0.4834 in FY23, compared to RMB0.7934 in FY22.

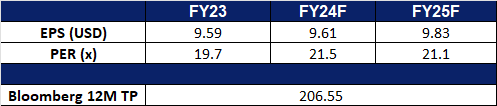

- Market Consensus

(Source: Bloomberg)

COSCO Shipping Holdings Co. Ltd. (1919 HK): Rebounding freight rates

- BUY Entry – 12.20 Target 13.40 Stop Loss – 11.60

- COSCO SHIPPING Holdings Co., Ltd., formerly China COSCO Holdings Company Limited, is an investment holding company principally engaged in container shipping and related businesses. The Company is engaged in container shipping, dry bulk shipping, the management and operation of container terminals, container leasing and the provision of logistics services. The Company operates its business through two segments. The Container Shipping segment is engaged in the transportation of goods across the Pacific, Asia and Europe, and other international routes. The Terminal Operation and Investment segment is engaged in the operation and management of ports. The Company is also involved in the management and leasing of containers.

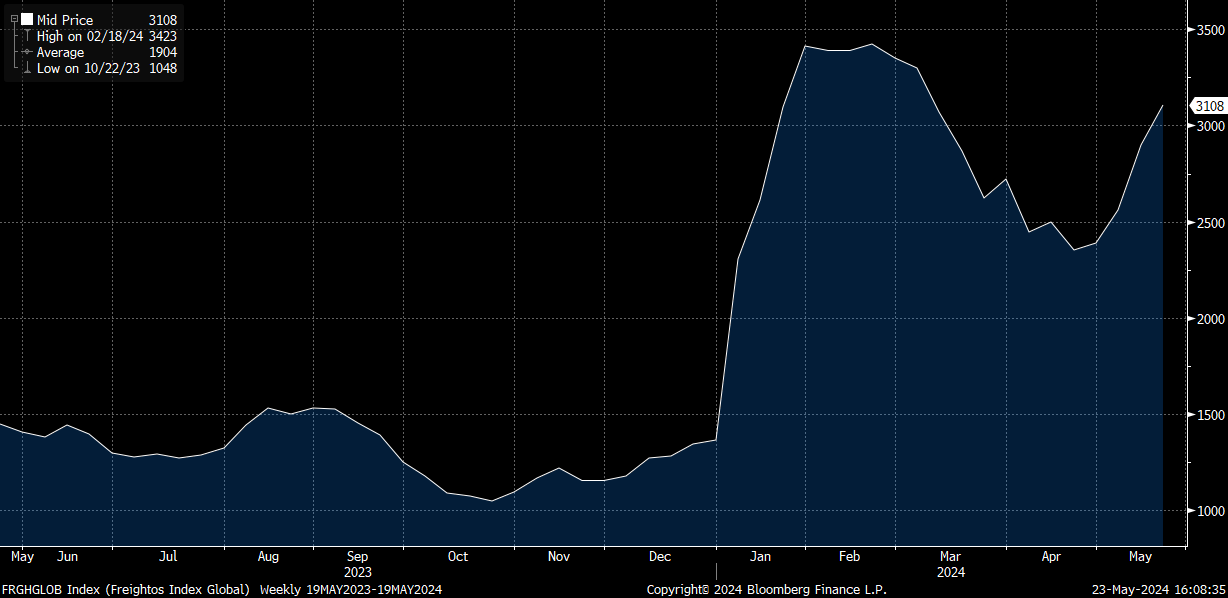

- Rebounding freight rates. The Freightos Baltic Index has rebounded since the end of April 2024, reaching its highest point since September 2022. This reflects a broader trend in the container shipping industry, marked by robust demand and supply chain disruptions. The increased demand for sea freight is primarily due to shifting consumer behaviors and a growing reliance on e-commerce platforms. Additionally, ocean carriers are being forced to divert routes away from the Red Sea, opting instead to navigate around Africa’s Cape of Good Hope due to ongoing vessel attacks, further straining the supply chain by extending shipping times. This rebound in freight rates is expected to positively impact COSCO Shipping.

Freightos Baltic Index

(Source: Bloomberg)

- More shipping routes. Cosco Shipping recently launched a new container service connecting Tianjin Port in China to the East Coast of South America. The service began operations last week, facilitating trade between China and countries in the region by reducing sailing time from 54 to 40 days and increasing reefer shipping capacity. The company will deploy 12 vessels, each with a capacity of 14,000 TEU, offering weekly sailings. Given that China has been Brazil’s largest trading partner for 15 consecutive years, this additional container service is poised to drive long-term revenue growth for the company.

- Launch of a self-operated warehouse in the US. Cosco Shipping has recently launched its self-operated fulfilment warehouse in the U.S., marking a significant step in enhancing its capacity to meet the growing logistics demands of cross-border businesses. The warehouse is designed to cater to medium and large-goods sellers, offering both standardized and customized logistics solutions for a variety of products, including home appliances and furniture. This strategic move not only adapts to the expanding needs of logistics services but also supports the growth of the global cross-border e-commerce industry.

- 1Q24 results review. Revenue increased 1.94% YoY to RMB48.3bn in 1Q24, compared with RMB47.4bn in 1Q23. Net profit fell 5.23% to RMB6.76bn in 1Q24, compared to RMB7.13bn in 1Q23. Basic earnings per share was RMB0.42 in 1Q24, compared to RMB0.44 in 1Q23.

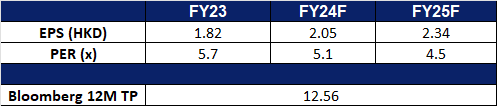

- Market consensus.

(Source: Bloomberg)

China State Construction International Holdings. (3311 HK): Property downtrend reversal

- RE-ITERATE BUY Entry – 10.20 Target 11.20 Stop Loss – 9.70

- China State Construction International Holdings Limited is an investment holding company principally engaged in construction contracts business. The Company is also engaged in infrastructure project investments, facade contracting business and infrastructure operation. The Company operates its business through four segments: Hong Kong, Mainland China, Macau and Overseas. Through its subsidiaries, the Company is also engaged in building construction, civil and foundation engineering works.

- Rolling out new measures. China recently announced new measures to revive its struggling property industry after data showed housing prices have dropped nearly 10% since the beginning of the year. Local state-owned enterprises will be asked to purchase unsold homes from distressed developers at significant discounts using loans from state banks, with many of these homes to be converted into affordable housing. The government also emphasized the importance of advancing the “three big projects,” which include affordable housing, urban renovation, and public infrastructure development.

- Lowering requirements for purchase and lower mortgage rates. The People’s Bank of China announced the creation of a 300 billion yuan relending facility for affordable housing and further reductions in mortgage interest rates and down payment requirements. Effective Saturday, the interest rate for first-time housing provident fund loans under five years will be reduced by 0.25 percentage points to 2.35%, while the rate for loans over five years will decrease by 0.25 percentage points to 2.85%. Additionally, the minimum down payment for first homes will be lowered from 20% to 15% of the purchasing price, and for second homes, from 30% to 25%.

- FY23 earnings. Revenue increased 11.5% YoY to HK$113.7bn in FY23, compared with HK$102.0bn in FY22. Net profit rose 15.2% to HK$9.16bn in FY23, compared to HK$7.96bn in FY22. Basic earnings per share was HK$1.82 in FY23, compared to HK$1.58 in FY22.

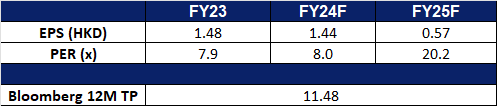

- Market consensus.

(Source: Bloomberg)

Air Products and Chemicals Inc (APD US): Natural gas demand to surge

- Entry – 264 Target –300 Stop Loss – 246

- Air Products and Chemicals, Inc. produces industrial atmospheric and specialty gases and performance materials and equipment. The Company’s products include oxygen, nitrogen, argon, helium, specialty surfactants and amines, polyurethane, epoxy curatives, and resins. Air Products and Chemicals products are used in the beverage, health, and semiconductor fields.

- Short squeeze spreads to the futures market. Short squeezes have once again emerged in the US market last week, similar to the short squeeze battle in early 2021, with investors looking for products with high short interest and buying them in large quantities. US natural gas futures soared 15.98% last week, and among the many futures, natural gas was the most heavily shorted, having fallen to a 30-year low in February. Upstream companies have gradually reduced capacity and exported large quantities in the past year to reduce inventory. The Middle East situation has changed natural gas trade routes, so oil and gas companies have begun to restore upstream production capacity. The bottom of the natural gas cycle has emerged. Air Products and Chemicals is highly correlated with natural gas prices.

- Electricity demand will drive natural gas demand. The future energy landscape is changing, leading to increased demand for natural gas in the medium to long term. Natural gas is the primary raw material for power generation in Western countries. China has already established market leadership in the photovoltaic and electric vehicle industries, and hydrogen energy is seen as the next vital area for all countries to focus on. Over the past two years, hydrogen energy and energy storage have been the fastest growing segments within the new energy industry segment.

APD stock vs Natural gas price trend

(Source: Bloomberg)

- 2Q24 earnings review. Revenue fell by 8.4% YoY to US$29.3bn, below estimates by US$130mn. Non-GAAP EPS was US$2.85, beating estimates by US$0.15. For FY24, adjusted EPS is expected to be between US$12.20 and $12.50, compared to the consensus estimate of US$12.31.

- Market consensus.

(Source: Bloomberg)

Hershey Co (HSY US): Decline in cocoa prices

- RE-ITERATE Entry – 207.0 Target –228.0 Stop Loss – 196.5

- The Hershey Company manufactures chocolate and sugar confectionery products. The Company’s principal products includes chocolate and sugar confectionery products, gum and mint refreshment products, and pantry items, such as baking ingredients, toppings, and beverages.

- Recent cocoa price decline. Cocoa prices have surged to nearly $10,000 per metric ton in March 2024, driven by a global shortage caused by climate change-induced droughts in West Africa, structural issues like underinvestment in cocoa farms, and increased investor speculation. This has led to higher costs for chocolate brands, many of which are passing these costs onto consumers, resulting in reduced demand and a shift towards other snacks. Some manufacturers are reducing product sizes or using less cocoa to cope. Cocoa prices dropped significantly to around US$7,277 per metric ton from record high of US$11,722 per metric ton earlier in the year, driven by a shortage of cocoa beans due to heavy rains and disease. This price decline was due to favourable climate changes which is expected to improve cocoa supply. Even though Hershey’s is largely covered on cocoa for the year, the decline in cocoa prices is beneficial for the company as will result in increased profit margins.

- New product varieties. Hershey recently showcased new products and retail strategies at the 2024 Sweets & Snacks Expo in Indianapolis, held from 14 May to 16 May, highlighting its expanding sweet and salty portfolio. New offerings include Reese’s Caramel Big Cup, Kit Kat Pink Lemonade, and Hershey’s Crunchy Waffle Cone Bars, among others. The company is also introducing Reese’s Medals for the Olympic Games. Hershey utilized augmented reality and image recognition to optimize merchandise placement and sales. With increasing foodservice demand, Hershey advises retailers to implement mobile ordering and foodservice features to enhance customer engagement. Effective merchandising at both assisted and self-checkout terminals is emphasized to maximize unplanned purchases and improve the shopping experience. Its new offerings cater to customer preferences, and the new flavours are likely to attract more customers to purchase these snacks.

- Delivered good results. Hershey exceeded Wall Street expectations for first-quarter sales and profit, driven by higher prices and steady consumer demand for its chocolates and candy. Despite raising prices to offset commodity costs, Hershey faced minimal resistance from customers, especially during holidays like Easter and Thanksgiving. Net sales rose 8.9% YoY to US$3.25bn, surpassing the expected US$3.11bn. Confectionary sales in North America, which makes up 80% of revenue, increased to US$2.70bn. Excluding items, earnings were US$3.07 per share, above the US$2.76 estimate. The company’s gross margin fell by 170 basis points to 44.9%.

- 1Q24 earnings review. Revenue rose by 8.7% YoY to US$3.25bn, beatings estimates by US$140mn. EPS was US$3.07, beating estimates by US$0.31. For 2Q24, it expects to deliver revenue between US$36.5bn to US$39.0bn. For FY24, Hershey expects net sales to increase by 2% to 3% versus estimated growth of 3.43% and adjusted earnings per share are expected to remain unchanged.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Take profit on Banyan Tree Holdings Ltd (BTH SP) at S$0.42, First Solar Inc (FSLR US) at US$210 and Lenovo Inc (992 HK) at HK$11. Cut loss on Baidu, Inc. (9888 HK) at HK$104.0 and ComfortDelgro Corp. Ltd. (CD SP) at S$1.38.