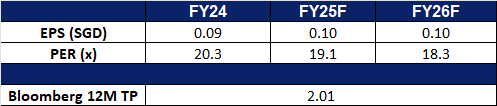

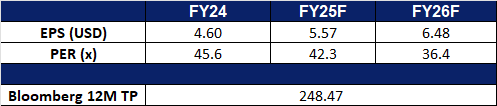

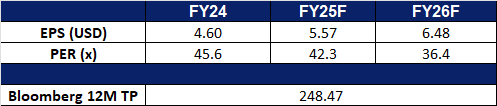

Sheng Siong Group Ltd is a retailer in Singapore. The Company operates a groceries chain across Singapore. Sheng Siong’s stores provide fresh and chilled produce, seafood, meat and vegetables, processed, packaged and preserved food products as well as general merchandise such as toiletries and essential household items.

Government vouchers to support near-term growth. Singapore’s FY25 voucher disbursement program, including S$800 in CDC Vouchers for households and up to S$800 in SG60 Vouchers for all Singapore Citizens, is expected to directly boost supermarket sales, with half the amount allocated for spend at participating supermarkets like Sheng Siong. These voucher schemes, alongside ongoing government support measures, will help sustain consumer spending momentum despite a cautious economic backdrop, providing a visible near-term revenue tailwind for Sheng Siong.

Value shopping to drive demand. Singapore’s core inflation rose to 0.7% in April 2025, ending six consecutive months of decline, mainly driven by rising food and services costs. However, the Monetary Authority of Singapore (MAS) and economists project inflation to remain modest for the rest of the year, with downside risks from weak global demand, persistent supply chain disruptions, and escalating tariff uncertainties. In this environment, Singaporean consumers are expected to remain price-conscious, driving sustained demand for affordable essentials and value-for-money house brand products. Sheng Siong, with its strong house brand offerings priced 5% to 20% below national brands, robust supply chain diversification, and disciplined cost management, is well-positioned to capture this structural shift towards value-driven consumption and defend margins amid inflationary and import cost pressures.

Strategic expansion partially linked to new HDB pipeline. Sheng Siong’s store network expansion is strategically tied to the Housing Development Board’s (HDB) pipeline, with over 50,000 new flats scheduled to be launched from 2025 to 2027 across growth areas. The Group is actively bidding for new supermarket sites within upcoming housing estates, having recently secured multiple tenders and two private retail spaces at KINEX and CATHAY. As HDB continues to roll out new developments, Sheng Siong is well-positioned to grow its footprint in high-density residential areas, supporting long-term revenue expansion.

1Q25 financial results. Sheng Siong reported 7.1% YoY growth in revenue for 1Q25, to S$403.0mn from S$376.2mn in 1Q24, mainly driven by the eight new stores opened compared to the same period last year alongside the festive sales for Hari Raya. Net profit for the period increased by 6.1% to S$38.5mn from the previous S$36.3mn. Comparable same store revenue in Singapore for 1Q25 increased marginally by 0.1%. China’s revenue increased marginally by 0.7%.

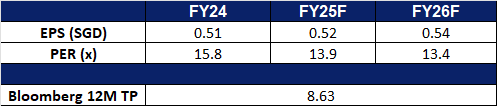

Keppel Limited is an asset manager and operator. The Company focuses on sustainability solutions spanning the areas of energy and environment, urban development, and digital connectivity, as well as provides critical infrastructure and services through its investment platforms and asset portfolios. Keppel serves clients worldwide.

Sale of asset in Vietnam. Keppel Ltd. continues to unlock value through disciplined asset monetization, recently raising $98 million from the sale of a 22.6% stake in Phase 3 of Saigon Centre in Ho Chi Minh City, Vietnam. This follows an earlier stake sale in late 2024, bringing total proceeds from Saigon Centre to approximately $160 million, with Keppel retaining a 41.4% stake. The company also divested a 42% stake in Palm City for $141 million in April. Despite investor concerns over Southeast Asia’s growth outlook, Keppel’s management reaffirms Vietnam as a core market for long-term investments in real estate, infrastructure, and digital connectivity, aligned with the group’s growth strategy.

Accelerating asset monetization. Keppel Ltd. has achieved over $7.3 billion in asset monetization since the launch of its $17.5 billion divestment programme in 2020, with recent divestments of Computer Generated Solutions (CGS) and Wanjiang Logistics Park in China unlocking more than $80 million in value. These sales, led by the company’s Accelerating Monetization Task Force (AMTF), contribute to Keppel’s target of monetizing $10 billion – $12 billion by end-2026. With another $550 million in real estate transactions under negotiation, Keppel is well-positioned to continue delivering strong results.

Driving sustainable infrastructure in healthcare. Keppel’s Infrastructure Division is collaborating with Ng Teng Fong General Hospital (NTFGH) and Jurong Community Hospital (JCH) to explore integrating the hospitals into Keppel’s 29,000 RT District Cooling System (DCS) in Jurong Lake District. This partnership could significantly enhance energy efficiency, reduce carbon footprint, lower operating costs, and optimise hospital space by replacing on-site cooling towers with district cooling. The proposed integration leverages advanced technologies such as thermal energy storage and intelligent controls, potentially setting a new sustainability benchmark in Singapore’s healthcare sector and advancing Keppel’s leadership in green infrastructure solutions.

1Q25 financial results. Keppel Ltd reported over 25% YoY growth in net profit for 1Q25, excluding contributions from its legacy O&M assets. The strong performance was driven by steady earnings from Infrastructure, improved results from the Real Estate segment, and a notable uplift in Asset Management. Recurring income accounted for more than 80% of net profit, excluding legacy O&M assets, highlighting the quality and stability of earnings. Year-to-date, Keppel has monetised approximately $347 million in assets, primarily through divestments in China and Vietnam. In addition, asset management fees rose 9% YoY to $96 million, reflecting the growing scale and resilience of Keppel’s asset-light business model.

Market consensus

(Source: Bloomberg)

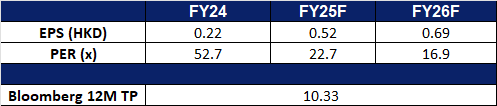

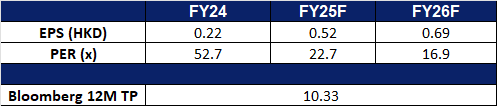

Hong Kong Exchanges and Clearing Ltd. (388 HK): Hottest IPO market

BUY Entry – 390 Target – 430 Stop Loss – 370

Hong Kong Exchanges and Clearing Limited (HKEX) is principally engaged in the operation of stock exchanges. The Company operates through five business segments. The Cash segment includes various equity products traded on the Cash Market platforms, the Shanghai Stock Exchange and the Shenzhen Stock Exchange. The Equity and Financial Derivatives segment includes derivatives products traded on Hong Kong Futures Exchange Limited (HKFE) and the Stock Exchange of Hong Kong Limited (SEHK) and other related activities. The Commodities segment includes the operations of the London Metal Exchange (LME). The Clearing segment includes the operations of various clearing houses, such as Hong Kong Securities Clearing Company Limited, the SEHK Options Clearing House Limited, HKFE Clearing Corporation Limited, over the counter (OTC) Clearing Hong Kong Limited and LME Clear Limited. The Platform and Infrastructure segment provides users with access to the platform and infrastructure of the Company.

Hong Kong regained global IPO leadership. Deloitte has upgraded its forecast for Hong Kong’s IPO market, projecting over HK$200 billion from 80 listings in 2025, as the city reclaimed its position as the world’s top fundraising venue in the first half, outpacing both Nasdaq and the New York Stock Exchange. This resurgence, driven by a 33% YoY increase in IPO deals and several mega A+H listings, highlights renewed investor confidence and robust global capital inflows. With nearly 200 IPO applications in the pipeline, including several large-cap names, and ongoing exchange reforms aimed at enhancing liquidity and attracting international investors, HKEX is well-positioned to sustain its strong IPO momentum and reinforce its role as a leading global financial hub.

Expansion of secondary listing market. HKEX is accelerating its global expansion by targeting secondary listings from Southeast Asia, the Middle East, and beyond. The exchange plans to open a representative office in Riyadh to deepen ties with the Saudi market and has already seen successful listings from Singaporean and Thai companies. Growing interest from mainland Chinese firms seeking offshore capital and rising participation from U.S. investors further strengthen HKEX’s competitive position. The IPO pipeline has more than doubled since December 2024 and the exchange has reclaimed its spot as the world’s largest listing venue by volume in 2025. HKEX’s proactive outreach and increasing cross-border listings underscore its transformation into a premier international fundraising platform.

Supportive monetary policy. The People’s Bank of China’s decision to maintain stable benchmark interest rates reflects confidence in the resilience of China’s economic recovery and creates a supportive backdrop for corporate capital raising. Stable rates reduce financial market uncertainty, support corporate valuations, and encourage both IPO and secondary listing activity. Recent signs of improving consumer demand, resilient export performance, and policy stability in China further underpin the capital markets environment. This is expected to drive sustained interest from mainland Chinese companies seeking offshore funding, as well as continued investor appetite for equity issuance, supporting the Hong Kong Stock Exchange’s long-term growth prospects.

1Q25 results review. Q1 revenue and other income of HK$6,857mn was 32% higher than 1Q24. Profit attributable to shareholders was HK$4,077mn, 37% higher than 1Q24. Basic EPS increased to HK$3.23 from HK$2.35 the same period last year.

Market consensus.

(Source: Bloomberg)

Yeahka Ltd. (9923 HK): Stablecoins as a cross-border payment tool

Yeahka Ltd is an investment holding company. Through its subsidiaries, the Company is principally engaged in the provision of one-stop payment services, merchant solution services and in-store e-commerce services to retail merchants and consumers. The Company operates three businesses. One-stop payment services business provides merchants for their acceptance of non-cash payments from consumers, through connecting the merchants with the payment networks. Merchant solutions services business includes the provision of various SaaS products with scenario-specific functionalities integrated with the payment services, data analysis services or SaaS terminals with operating system can be customized by customers as needed, agency services to customers, online marketing services to customers, technology services to insurance companies, small-sized loans. The Company also provides in-store e-commerce services. The Company conducts its businesses in the domestic market.

US Senate passed stablecoin regulation bill. The U.S. Senate has passed the “Genius Act” a bill to regulate stablecoins, which now requires the approval of the House of Representatives and President Donald Trump. If enacted stablecoins need to be backed by liquid assets such as the US dollar or short-term treasuries, with issuers required to disclose reserve composition monthly. This is expected to provide regulatory and legislative clarity, paving the way for corporate adoption of stablecoins across industries and drive wider acceptance of digital payments and cross-border transactions. With more large enterprises and financial institutions likely to adopt stablecoins for faster, lower-cost payments, Yeahka could benefit by integrating stablecoin into its payment infrastructure, enhancing its digital payment solutions and potentially opening new revenue streams.

Hong Kong stablecoins positioned as a cross-border payment solution. Hong Kong recently announced progress on regulating stablecoins, with new legislation set to take effect later this year. Under the upcoming law, issuers must obtain a license from the Hong Kong Monetary Authority (HKMA) and adhere to stringent requirements, including those related to reserve assets and operational standards. These stablecoins are expected to become a key enabler of cross-border payments, particularly benefiting issuers in Hong Kong and Chinese enterprises expanding internationally. With the potential to reduce settlement times from days to minutes, stablecoins aim to address longstanding inefficiencies in cross-border transactions, such as high costs, delays, and limited transparency. This structural improvement in payment infrastructure is expected to spur demand for cross-border payment services, directly benefiting Yeahka, which offers comprehensive payment solutions, merchant services, and in-store e-commerce capabilities.

Expansion of payment licenses to accelerate global growth. Yeahka recently announced that it has been granted a Money Transmitter License (MTL) by financial regulators in Arizona, USA. This follows the earlier acquisition of a Money Services Business (MSB) license, marking another key milestone in the company’s international expansion strategy. With both licenses in place, Yeahka is now positioned to provide secure, compliant, and efficient payment services in the U.S., supporting its broader goal of scaling operations in overseas markets.

Capital raise to fuel strategic initiatives. Earlier this year, Yeahka successfully raised US$25 million in equity capital. Approximately 40% of the proceeds will be allocated to expanding the company’s presence across Asia, while another 40% will be invested in research and development—particularly in the integration of artificial intelligence into its proprietary platforms. These investments are expected to enhance Yeahka’s digital ecosystem and support long-term growth.

FY24 results review. Revenue fell by 21.9% YoY to RMB3.09bn in FY25, compared with RMB3.95bn in FY24. Net profit rose to RMB73.0mn in FY25, compared to RMB10.1mn in FY24. Basic EPS increased to RMB0.22 in FY25, compared to RMB0.03 in FY24.

Market consensus.

(Source: Bloomberg)

International Business Machines (IBM US): Capitalizing on mainframe expansion and quantum computing

BUY Entry – 276 Target – 300 Stop Loss – 264

International Business Machines is a global technology company focused on software, cloud services, artificial intelligence, and consulting services.

Steady growth in the global mainframe market. The global mainframe market is driven by the increasing demand for high-performance computing and robust data processing and cybersecurity solutions. It is expected to grow from $3.5 billion in 2024 to $6.8 billion by 2033, with a compound annual growth rate of 8.4%. IBM’s Z series mainframes hold a significant market share and maintain leadership in the mainframe market. The newly launched z17 mainframe is designed to meet the high computational demands of generative AI and the security needs of critical workloads for large enterprises, particularly in the financial services sector. As global demand for high-performance and highly secure infrastructure continues to rise, the company has strong growth momentum in this area.

Investment in quantum computing. Since the end of last year, quantum computing has gained market attention and is seen as another major technological revolution outside of artificial intelligence, with related company stocks soaring. IBM is actively developing quantum computing, planning to invest $30 billion over the next five years in research and development of quantum computing and mainframe technology, as part of its commitment to a total investment plan of $150 billion in the U.S. The company aims to launch practical quantum computers by 2029 and achieve a more advanced “Starling” system with approximately 200 logical qubits by 2033.

Business less affected by geopolitical risks. The company’s global operations cover both software and hardware, as well as consulting services, providing a higher level of risk resilience. Its core businesses, such as mainframe manufacturing and cloud services, have strong demand, resulting in relatively stable revenue growth during volatile economic cycles.

1Q25 results. Revenue grew 0.6% to US$14.54bn, exceeding expectations by US$150mn. Non-GAAP earnings per share were US$1.60, surpassing estimates by US$0.17. The company expects full-year revenue growth of 5% (fixed rate).

GE Electric Co (doing business as GE Aerospace) operates as an aircraft engine supplier company. The Company provides jet and turboprop engines, as well as integrated systems for commercial, military, business, and general aviation aircraft. GE Aerospace serves customers worldwide.

Healthy cash position. GE Aerospace reported US$1.5 bn in cash from operating activities and US$1.4bn in free cash flow in 1Q25, with revenue rising 11% YoY to $9.0bn and operating profit reaching $2.1bn, a 23.8% profit margin, supported by a robust commercial services backlog of over US$140bn as of Q1 that underpins long-term earnings visibility.

Defense orders to bolster growth. Amid ongoing geopolitical instability, GE Aerospace stands to benefit from rising defense budgets, highlighted by its US$5bn contract win with the U.S. Air Force for F110-GE-129 engines, which will support sustained military demand alongside its sizable commercial services backlog.

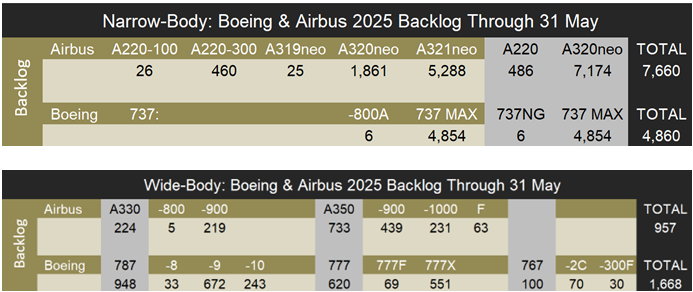

Record commercial engine deals. GE Aerospace secured a historic engine deal with Qatar Airways for over 400 engines, alongside additional commitments from ANA Holdings, Malaysia Aviation Group, and Korean Air, further building its commercial services backlog. According to Forecast International’s 2025 production estimates, as of 31 May, Airbus’s backlog represents 10.5 years of production and Boeing’s backlog approximately 11.5 years, highlighting the tight commercial aviation supply chain and potentially prolonging demand for GE’s engines, spares, and aftermarket services.

Airbus and Boeing report May 2025 commercial aircraft orders backlog:

1Q25 results. Revenue increased by 11% YoY to US$9.0bn, missing expectations by US$50mn. Non-GAAP earnings per share was US$1.49, surpassing estimates by US$0.22. The company maintained its full-year revenue forecast for FY25 to in low double digit and adjusted EPS of between US$5.10 to US$5.45, with the mid-point below consensus of US$5.42. It also expects operating profit to be US$7.8bn – US$8.2bn and free cash flow to be between US$6.3bn – US$6.8bn.

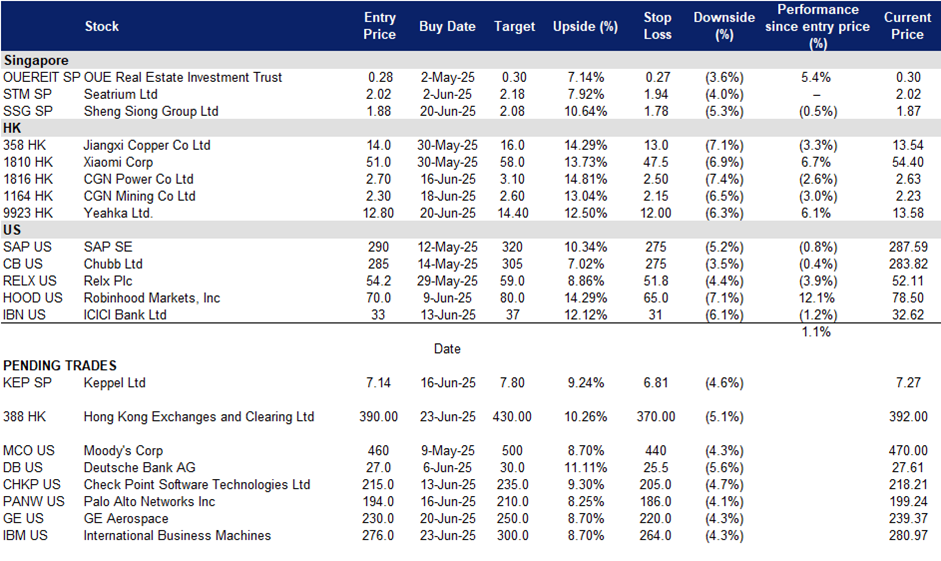

Trading Dashboard Update: Cut loss on Singapore Airlines (SIA SP) at S$6.75, SATS Ltd (SATS SP) at S$2.96 and Wee Hur Holdings Ltd (WHUR SP) at S$0.44.