Geo Energy Resources Limited is an integrated coal mining specialist. The Company owns and operates coal mines, offers mine contracting services to third party mine owners, and sells coal to both coal traders and coal export companies.

Infrastructure expansion and cost efficiency. Geo Energy’s US$150mn investment in the MBJ Integrated Infrastructure Project is on track for completion by 1H26. The project includes a 92km hauling road and jetty, which will reduce transportation costs by over US$10 per tonne and double production capacity to 25Mt per year. Additionally, thirdparty leasing of the infrastructure is expected to create additional revenue streams, enhancing long-term cash flow and profitability.

Strategic growth via acquisitions and investments. The acquisition of PT Golden Eagle Energy expands Geo Energy’s reserves and production capacity, securing longterm supply. A US$30mn investment from ResInvest increased its stake to 6.8%, while a US$50mn-US$100mn investment in MBJ infrastructure is expected to further support the company’s long-term expansion plans.

Favourable market outlook. Global coal demand is projected to reach 8.9 billion tonnes by 2027, with China’s record coal imports of 542.7Mt in 2024, a 14.4% YoY increase, sustaining market stability. Although prices have moderated, thermal coal remains above 2019 levels, ensuring profitability for producers like Geo Energy.

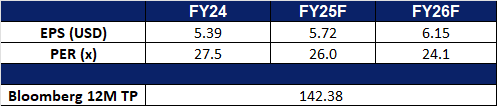

FY24 results review. Geo Energy reported FY24 revenue of US$401.9mn, a slight decline from FY23 due to lower ICI4 coal prices. Net profit fell to US$37.3mn, but cost efficiencies enabled the company to maintain a strong cash profit per tonne of US$10.37. FY24 total dividends amount to 1.0 S-cent per share.

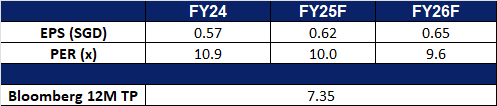

We have fundamental coverage with a BUY recommendation and a TP of S$0.71. Please read the full report here.

Market consensus

(Source: Bloomberg)

Sembcorp Industries Ltd (SCI SP): Risk off and rate cut expectations

Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

Rotation to defensive sectors and rising rate cut expectations. Escalating global trade tensions, driven by the broad tariff policies of the US, will gradually reshape global supply chains. World economic growth, especially in Asia, is expected to slow down substantially in the near term. Amidst macro headwinds, the utility sector is expected to outperform others. Meanwhile, expectations of rate cut are reviving. Lower interest rates would benefit Sembcorp by reducing financing costs, enhancing project viability, and potentially boosting demand for its energy and urban solutions. In a nutshell, investors favour assets with stability and visibility moving forward.

Proposed acquisition. Sembcorp Industries plans to increase its stake in Senoko Energy from 30% to a maximum of 70%, expanding its role in Singapore’s energy sector. The acquisition agreement, signed with KPIC Netherlands, Kyuden International, and Japan Bank for International Cooperation (JBIC), involves purchasing up to a 57.1% stake in Lion Power, which owns 70% of Senoko. The deal, valued at up to S$144mn, will be funded through internal cash and/or external borrowings and is expected to close in 2Q25. The Energy Market Authority has approved the acquisition, with Sembcorp committing to measures that ensure fair market competition. The acquisition is projected to be earnings accretive but will not significantly impact net tangible assets per share for FY25. This strategic move strengthens Sembcorp’s position in Singapore’s energy market and supports its commitment to the energy transition. With a larger stake in Senoko, Sembcorp can enhance operational synergies and contribute more effectively to sustainable and reliable energy solutions, aligning with its long-term growth strategy.

Increased dividend payout. Sembcorp raised its dividend to S$0.23 per share, from its previous S$0.13 in FY23, reflecting a higher payout ratio, signaling confidence in sustained profitability. The company’s net profit before exceptional items remained above S$1bn for a second consecutive year. Sembcorp’s gas and related services segment saw a 10% decline in profit to S$727mn, impacted by a 34% drop in Singapore’s wholesale electricity prices. However, the company solidified its position as the leading power provider for data centers and acquired a 30% stake in Senoko Energy. Additionally, it fully exited coal-fired power assets with the divestment of its 49% stake in Chongqing Songzao. Sembcorp’s renewable energy portfolio grew to 13.1 GW in 2024, progressing toward its 2028 goal of 25 GW. The company remains focused on executing its 2024-2028 strategic plan to meet Asia’s evolving energy needs. With a stronger commitment to dividends and an expanding clean energy portfolio, the company is poised to capitalize on Asia’s transition to sustainable energy while maintaining financial stability.

FY24 financial results. Sembcorp Industries Ltd reported net profit of S$1,011mn for FY24, a 7% incline YoY, compared to S$942mn in FY23. Due to the Group’s strong performance, the Board of Directors approved a total dividend of S$0.23 per ordinary share for FY24, an increase from the S$0.13 distributed for FY23.

Market consensus

(Source: Bloomberg)

Trip.com Group Ltd. (9961 HK): Upcoming seasonality play

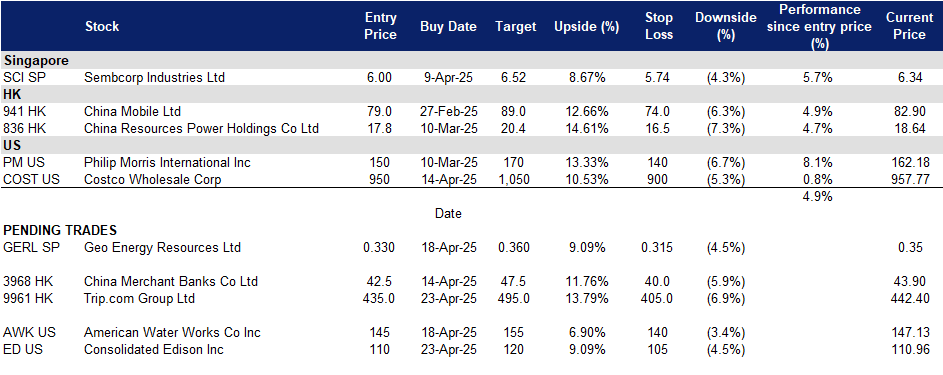

BUY Entry – 435 Target – 495 Stop Loss – 405

Trip.com Group Ltd is a China-based company mainly engaged in the operation of one-stop travel platform. The Company’s platform integrates a comprehensive suite of travel products and services and differentiated travel content. Its platform aggregates its product and service offerings, reviews and other content shared by its users based on their real travel experiences, and original content from its ecosystem partners to enable leisure and business travelers to have access to travel experiences and make informed and cost-effective bookings. Users come to its platform for any type of trip, from in-destination activities, weekend getaways, and short-haul trips, to cross-border vacations and business trips.

Upcoming May Day Holidays. The May Day holidays in China, officially observed from May 1 to May 5, are expected to drive a significant uptick in travel activity. The holiday travel rush is anticipated to span from April 29 to May 6, with peak passenger flow projected on May 1. Short-haul outbound travel is showing strong momentum, supported by rising demand for both group tours and independent travel. Market data reveals a 60% year-over-year increase in group tour bookings and a 29% rise in independent travel among mainland Chinese tourists. Additionally, flight bookings for the holiday period have exceeded 750,000 for both outbound and inbound routes. This surge in travel demand is likely to benefit Trip.com Group Ltd. positively.

Trip.com Group share price seasonality chart

(Source: Bloomberg)

New Initiatives to Attract Consumers. Trip.com Group recently launched its 2025 Word-of-Mouth Travel Rankings, offering users a fresh way to explore global destinations across its platforms. The rankings feature 16 themed global lists and “Recommended Itineraries,” combining user reviews, AI-driven insights, and curated content to streamline the travel planning process—from inspiration to booking. These itineraries link top-rated hotels, attractions, restaurants, and nightlife experiences, reflecting real user journeys and enabling personalized planning through Trip.com’s intelligent recommendation system. Travelers can explore seasonal highlights, save customized routes, and receive tailored suggestions based on their preferences and travel dates. The rankings cover 291 destinations, over 1,500 hotels, 800 attractions, 800 restaurants, and nearly 400 night tour options—enhancing the overall user experience and engagement on the platform.

Expanding Strategic Partnerships. Trip.com has also deepened its partnership with Emirates, further integrating flights, hotels, and loyalty programs to enrich travel offerings in key global markets. The next phase of this collaboration will focus on unlocking growth opportunities in new markets and customer segments. Both companies plan to expand Trip.com’s global footprint by leveraging Emirates’ extensive international network and coordinating joint promotional campaigns, particularly in Asia and Europe—strategic regions for both partners.

FY24 earnings. Revenue increased by 19.8% YoY to RMB53.4bn in FY24, compared to RMB44.6bn in FY23. Net Profit increased by 72.2% to RMB17.2bn in FY24, compared to RMB10.0bn in FY23. Basic earnings per share is RMB26.1 in FY24, compared to a basic earnings per share of RMB24.8 in FY23.

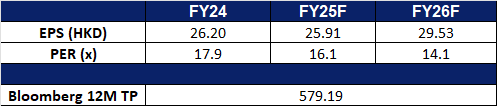

Market consensus.

(Source: Bloomberg)

China Merchants Bank Co Ltd. (3968 HK): Expecting more stimulus to combat U.S. tariffs

China Merchants Bank Co Ltd is a China-based company mainly engaged in banking business. The Company operates three segments. The Wholesale Finance Business segment provides financial services to corporate clients, government agency clients, and interbank clients, including loan and deposit services, settlement and cash management services, trade finance and offshore business, investment banking services, borrowing, repurchase, asset custody services, and others. The Retail Finance Business segment provides financial services to individual customers, including loan and deposit services, bank card services, wealth management, private banking, and other services. The company also operates the Other Businesses segment.

Expecting additional Stimulus to Counter U.S. Tariffs. China’s top leadership convened on recently to discuss further stimulus measures in response to heightened U.S. tariffs, according to sources. The meeting reportedly centered on support for the housing sector, consumer spending, and technological innovation. Financial regulators and related agencies are also preparing measures to help stabilize financial markets. These potential further stimulus efforts are likely to benefit China Merchants Bank (CMB), given the alignment with its core business strengths. Increased loan demand, improved asset quality, and growth opportunities in emerging sectors could follow.

Stock Repurchase and Capital Support Initiatives. Chinese commercial banks have stepped up support for stock repurchase and share increase programs, with total credit commitments surpassing RMB 300bn. These efforts aim to help listed companies stabilize valuations and optimize capital structures, contributing to broader market stabilization. As of April 6, China Merchants Bank had initiated 288 such projects, totaling RMB 104.8bn. This initiative has supported loan growth and boosted interest income, while also reinforcing broader economic resilience.

FY24 earnings. Revenue fell marginally by 0.58% YoY to RMB337.1bn in FY24, compared to RMB339.1bn in FY23. Profit increased by 1.22% to RMB148.4bn in FY24, compared to RMB146.6bn in FY23. Basic earnings per share was RMB5.66 in FY24, compared to a basic earnings per share of RMB5.63 in FY23.

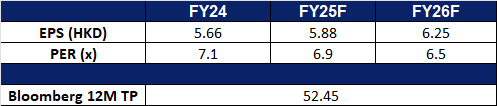

Market consensus.

(Source: Bloomberg)

Consolidated Edison Inc. (ED US): Solid dividends and defensive appeal

BUY Entry – 110 Target – 120 Stop Loss – 105

Consolidated Edison, Inc., through its subsidiaries, provides a variety of energy related products and services. The Company supplies electric service in New York, parts of New Jersey, and Pennsylvania as well as supplies electricity to wholesale customers.

Highly defensive utility stock. In a macroeconomic environment characterized by increasing trade tensions, inflationary pressures, and regulatory uncertainty, Consolidated Edison stands out due to its highly defensive business model. As a fully regulated provider of electricity, natural gas, and steam services focused entirely on the U.S. domestic market, the company’s operations are largely insulated from the direct impacts of international trade conflicts or global supply chain disruptions. This allows it to provide stable returns during periods of global market volatility, making it a reliable income-generating asset.

Dependable dividend income with a strong track record. The company boasts a solid dividend history, with 51 consecutive years of stable dividend increases and an average annual growth rate of 5.59%. Its current 12-month trailing yield is 2.98%, and it maintains a long-term dividend payout ratio target of 55%-65% of adjusted earnings. The transparent regulatory framework under which it operates in New York State provides a high degree of predictability and stability to its revenue. Looking ahead, the company plans to invest $38 billion in capital expenditures between 2025 and 2029, which is expected to drive an average annual growth of 8.2% in its utility asset base. Furthermore, the simplification of its capital structure, with no long-term debt at the parent company level, further enhances its financial resilience. In today’s uncertain global landscape, the company’s U.S. domestic focus and provision of essential public services make it a high-quality choice for conservative and income-oriented investment portfolios.

4Q24 results. Non-GAAP earnings per share were US$0.98, beating expectations by US$0.02. The company declared a $0.85/share quarterly dividend, in line with previous, payable 16 June; for shareholders of record 14 May. It expects its adjusted profit for 2025 to be between US$5.50 and US$5.70 per share, the midpoint of which was below Wall Street estimates of US$5.63 per share. Consolidated Edison expects its capital expenditure to be US$5.12bn in 2025 and US$8.07bn in 2026.

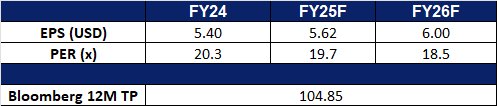

Market consensus

(Source: Bloomberg)

American Water Works Co Inc (AWK US): Strengthening portfolio defences

American Water Works Co., Inc. provides drinking water, wastewater, and other water-related services in multiple states and Ontario, Canada. The Company’s primary business involves the ownership of regulated water and wastewater utilities that provide water and wastewater services to residential, commercial, and industrial customers.

Resilient utility stock in a defensive sector. Amidst escalating trade tensions and an increasingly uncertain macroeconomic outlook, American Water Works stands out as a defensive and stable investment choice due to its business model of providing essential clean water and wastewater treatment services. With its operations and revenue entirely derived from the U.S. domestic market, the company largely avoids global supply chain disruptions and tariff impacts, positioning it as a safe haven during market volatility.

Defensive advantages of essential public services. The company demonstrates its resilience by relying on a regulated utility model to achieve stable cash flow and consistently growing dividends. In fiscal year 2024, its dividend grew by 8.6% year-over-year, and its current dividend yield is 2.06%. The company has set long-term annual earnings per share growth target of 7%-9%, highlighting its shareholder-focused strategy. The company also plans to invest $170 billion to $180 billion in capital expenditures between 2025 and 2029, with a total investment of $400 billion to $420 billion by 2034, dedicated to enhancing infrastructure efficiency, expanding customer reach, and driving the acquisition pipeline. As a utility company focused on the U.S. market, AWK offers low volatility, stable returns, and long-term capital appreciation potential, making it highly attractive in uncertain times.

4Q24 results. Revenue increased by 16.5% YoY to US$1.20bn, exceeding expectations by US$90mn. GAAP earnings per share were US$1.22, beating expectations by US$0.10. The company distributed a dividend of US$0.765/share quarterly dividend, in line with previous.