Geo Energy Resources Limited is an integrated coal mining specialist. The Company owns and operates coal mines, offers mine contracting services to third party mine owners, and sells coal to both coal traders and coal export companies.

Infrastructure expansion and cost efficiency. Geo Energy’s US$150mn investment in the MBJ Integrated Infrastructure Project is on track for completion by 1H26. The project includes a 92km hauling road and jetty, which will reduce transportation costs by over US$10 per tonne and double production capacity to 25Mt per year. Additionally, thirdparty leasing of the infrastructure is expected to create additional revenue streams, enhancing long-term cash flow and profitability.

Strategic growth via acquisitions and investments. The acquisition of PT Golden Eagle Energy expands Geo Energy’s reserves and production capacity, securing longterm supply. A US$30mn investment from ResInvest increased its stake to 6.8%, while a US$50mn-US$100mn investment in MBJ infrastructure is expected to further support the company’s long-term expansion plans.

Favourable market outlook. Global coal demand is projected to reach 8.9 billion tonnes by 2027, with China’s record coal imports of 542.7Mt in 2024, a 14.4% YoY increase, sustaining market stability. Although prices have moderated, thermal coal remains above 2019 levels, ensuring profitability for producers like Geo Energy.

FY24 results review. Geo Energy reported FY24 revenue of US$401.9mn, a slight decline from FY23 due to lower ICI4 coal prices. Net profit fell to US$37.3mn, but cost efficiencies enabled the company to maintain a strong cash profit per tonne of US$10.37. FY24 total dividends amount to 1.0 S-cent per share.

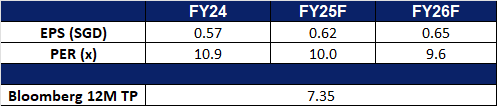

We have fundamental coverage with a BUY recommendation and a TP of S$0.71. Please read the full report here.

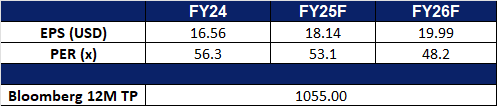

Market consensus

(Source: Bloomberg)

Sembcorp Industries Ltd (SCI SP): Risk off and rate cut expectations

Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

Rotation to defensive sectors and rising rate cut expectations. Escalating global trade tensions, driven by the broad tariff policies of the US, will gradually reshape global supply chains. World economic growth, especially in Asia, is expected to slow down substantially in the near term. Amidst macro headwinds, the utility sector is expected to outperform others. Meanwhile, expectations of rate cut are reviving. Lower interest rates would benefit Sembcorp by reducing financing costs, enhancing project viability, and potentially boosting demand for its energy and urban solutions. In a nutshell, investors favour assets with stability and visibility moving forward.

Proposed acquisition. Sembcorp Industries plans to increase its stake in Senoko Energy from 30% to a maximum of 70%, expanding its role in Singapore’s energy sector. The acquisition agreement, signed with KPIC Netherlands, Kyuden International, and Japan Bank for International Cooperation (JBIC), involves purchasing up to a 57.1% stake in Lion Power, which owns 70% of Senoko. The deal, valued at up to S$144mn, will be funded through internal cash and/or external borrowings and is expected to close in 2Q25. The Energy Market Authority has approved the acquisition, with Sembcorp committing to measures that ensure fair market competition. The acquisition is projected to be earnings accretive but will not significantly impact net tangible assets per share for FY25. This strategic move strengthens Sembcorp’s position in Singapore’s energy market and supports its commitment to the energy transition. With a larger stake in Senoko, Sembcorp can enhance operational synergies and contribute more effectively to sustainable and reliable energy solutions, aligning with its long-term growth strategy.

Increased dividend payout. Sembcorp raised its dividend to S$0.23 per share, from its previous S$0.13 in FY23, reflecting a higher payout ratio, signaling confidence in sustained profitability. The company’s net profit before exceptional items remained above S$1bn for a second consecutive year. Sembcorp’s gas and related services segment saw a 10% decline in profit to S$727mn, impacted by a 34% drop in Singapore’s wholesale electricity prices. However, the company solidified its position as the leading power provider for data centers and acquired a 30% stake in Senoko Energy. Additionally, it fully exited coal-fired power assets with the divestment of its 49% stake in Chongqing Songzao. Sembcorp’s renewable energy portfolio grew to 13.1 GW in 2024, progressing toward its 2028 goal of 25 GW. The company remains focused on executing its 2024-2028 strategic plan to meet Asia’s evolving energy needs. With a stronger commitment to dividends and an expanding clean energy portfolio, the company is poised to capitalize on Asia’s transition to sustainable energy while maintaining financial stability.

FY24 financial results. Sembcorp Industries Ltd reported net profit of S$1,011mn for FY24, a 7% incline YoY, compared to S$942mn in FY23. Due to the Group’s strong performance, the Board of Directors approved a total dividend of S$0.23 per ordinary share for FY24, an increase from the S$0.13 distributed for FY23.

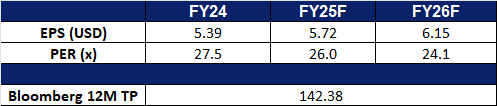

Market consensus

(Source: Bloomberg)

American Water Works Co Inc (AWK US): Strengthening portfolio defences

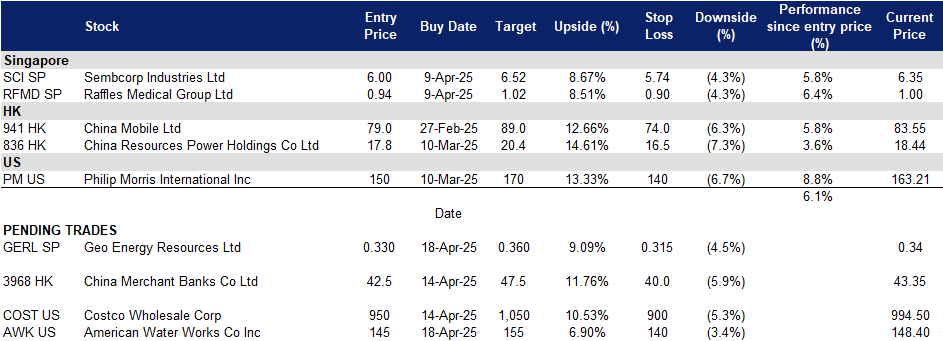

BUY Entry – 145 Target – 155 Stop Loss – 140

American Water Works Co., Inc. provides drinking water, wastewater, and other water-related services in multiple states and Ontario, Canada. The Company’s primary business involves the ownership of regulated water and wastewater utilities that provide water and wastewater services to residential, commercial, and industrial customers.

Resilient utility stock in a defensive sector. Amidst escalating trade tensions and an increasingly uncertain macroeconomic outlook, American Water Works stands out as a defensive and stable investment choice due to its business model of providing essential clean water and wastewater treatment services. With its operations and revenue entirely derived from the U.S. domestic market, the company largely avoids global supply chain disruptions and tariff impacts, positioning it as a safe haven during market volatility.

Defensive advantages of essential public services. The company demonstrates its resilience by relying on a regulated utility model to achieve stable cash flow and consistently growing dividends. In fiscal year 2024, its dividend grew by 8.6% year-over-year, and its current dividend yield is 2.06%. The company has set long-term annual earnings per share growth target of 7%-9%, highlighting its shareholder-focused strategy. The company also plans to invest $170 billion to $180 billion in capital expenditures between 2025 and 2029, with a total investment of $400 billion to $420 billion by 2034, dedicated to enhancing infrastructure efficiency, expanding customer reach, and driving the acquisition pipeline. As a utility company focused on the U.S. market, AWK offers low volatility, stable returns, and long-term capital appreciation potential, making it highly attractive in uncertain times.

4Q24 results. Revenue increased by 16.5% YoY to US$1.20bn, exceeding expectations by US$90mn. GAAP earnings per share were US$1.22, beating expectations by US$0.10. The company distributed a dividend of US$0.765/share quarterly dividend, in line with previous.

Costco Wholesale Corporation is a membership warehouse club The Company sells all kinds of food, automotive supplies, toys, hardware, sporting goods, jewelry, electronics, apparel, health, and beauty aids, as well as other goods. Costco Wholesale serves customers worldwide.

Tariff implementation drives short-term demand for essential goods. As of April 10, the U.S. has imposed a 10% tariff on global imports and a 145% tariff on goods imported from China. In 2024, the total value of U.S. imports from China amounted to US$438.9 billion, with the majority being essential daily goods. Following the announcement of the tariff policy, panic buying emerged in the U.S., leading to a sharp increase in short-term demand for essential consumer products.

Sales maintained steady growth in March. For the retail month of March, comparable sales rose by 6.4% YoY, with the U.S. market growing 7.5%, Canada increasing by 4.1%, and other international markets up by 2.9%. E-commerce comparable sales surged by 16.2% during the quarter. Excluding the impacts of currency and fuel prices, total comparable sales grew by 9.1% YoY, with the U.S. still showing strong growth of 8.7%. For the five-week period ending April 6, total net sales rose 8.6% to US$25.51 billion.

Combining both defensive and growth attributes. Unlike traditional supermarkets that rely on low margins and high volume, Costco maintains ultra-low wholesale pricing and derives most of its profits from membership fees. Membership growth and fee increases are long-term growth drivers. As of December 2024, the number of paid household memberships reached 77.4 million, up around 8% YoY, with total cardholders reaching 138.8 million. The global membership renewal rate was 90.4%. Starting September 1, 2024, membership fees in the U.S. and Canada increased, basic membership rose from US$60 to US$65, and executive membership from US$120 to US$130. In South Korea, membership fees will increase by 7.5% to 15.2% in May 2025. The company currently operates 897 warehouses across 13 countries and plans to open 29 new locations in 2025, with 12 of them outside the U.S.

2Q25 results. Revenue increased by 9.0% YoY to US$63.72bn, exceeding expectations by US$640mn. GAAP earnings per share were US$4.02, missing expectations by US$0.09.

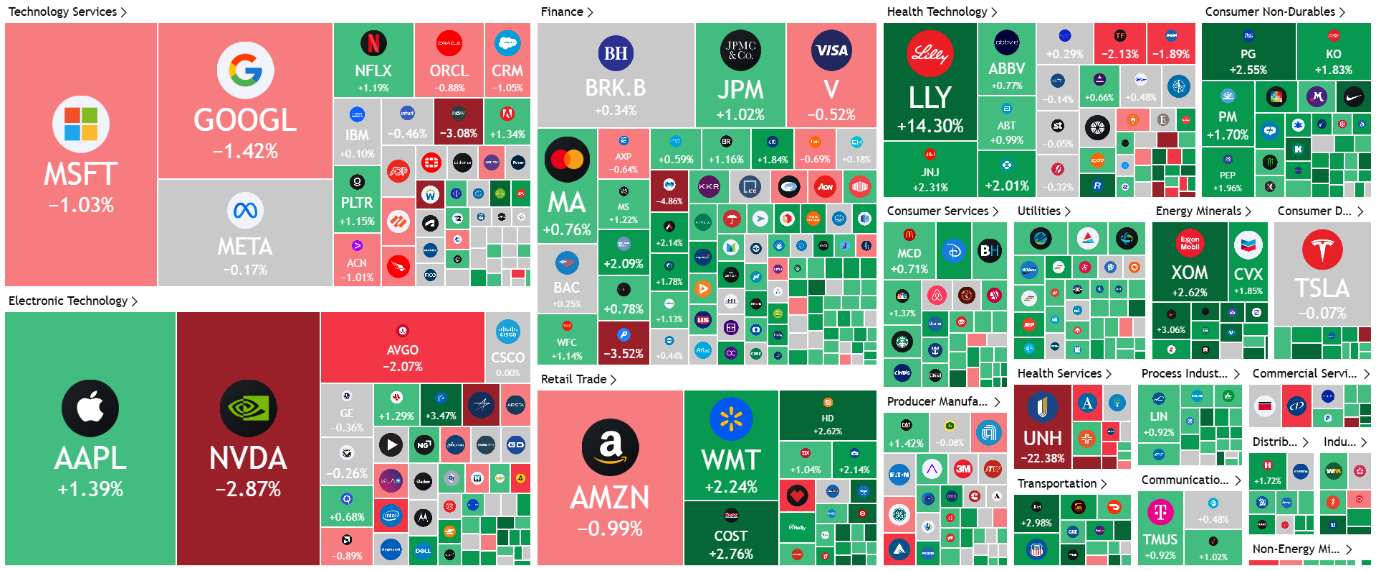

Trading Dashboard Update: Take profit on Centurion Corp (CENT SP) at S$1.20 and Weilong Delicious Global Holdings Ltd (9985 HK) at HK$17. Add UnitedHealth Group Inc (UNH US) at US$560. Cut loss on UnitedHealth Group Inc (UNH US) at US$530.