Keppel Limited is an asset manager and operator. The Company focuses on sustainability solutions spanning the areas of energy and environment, urban development, and digital connectivity, as well as provides critical infrastructure and services through its investment platforms and asset portfolios. Keppel serves clients worldwide.

Sale of asset in Vietnam. Keppel Ltd. continues to unlock value through disciplined asset monetization, recently raising $98 million from the sale of a 22.6% stake in Phase 3 of Saigon Centre in Ho Chi Minh City, Vietnam. This follows an earlier stake sale in late 2024, bringing total proceeds from Saigon Centre to approximately $160 million, with Keppel retaining a 41.4% stake. The company also divested a 42% stake in Palm City for $141 million in April. Despite investor concerns over Southeast Asia’s growth outlook, Keppel’s management reaffirms Vietnam as a core market for long-term investments in real estate, infrastructure, and digital connectivity, aligned with the group’s growth strategy.

Accelerating asset monetization. Keppel Ltd. has achieved over $7.3 billion in asset monetization since the launch of its $17.5 billion divestment programme in 2020, with recent divestments of Computer Generated Solutions (CGS) and Wanjiang Logistics Park in China unlocking more than $80 million in value. These sales, led by the company’s Accelerating Monetization Task Force (AMTF), contribute to Keppel’s target of monetizing $10 billion – $12 billion by end-2026. With another $550 million in real estate transactions under negotiation, Keppel is well-positioned to continue delivering strong results.

Driving sustainable infrastructure in healthcare. Keppel’s Infrastructure Division is collaborating with Ng Teng Fong General Hospital (NTFGH) and Jurong Community Hospital (JCH) to explore integrating the hospitals into Keppel’s 29,000 RT District Cooling System (DCS) in Jurong Lake District. This partnership could significantly enhance energy efficiency, reduce carbon footprint, lower operating costs, and optimise hospital space by replacing on-site cooling towers with district cooling. The proposed integration leverages advanced technologies such as thermal energy storage and intelligent controls, potentially setting a new sustainability benchmark in Singapore’s healthcare sector and advancing Keppel’s leadership in green infrastructure solutions.

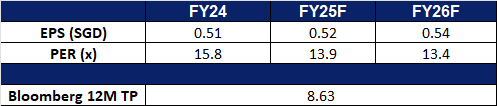

1Q25 financial results. Keppel Ltd reported over 25% YoY growth in net profit for 1Q25, excluding contributions from its legacy O&M assets. The strong performance was driven by steady earnings from Infrastructure, improved results from the Real Estate segment, and a notable uplift in Asset Management. Recurring income accounted for more than 80% of net profit, excluding legacy O&M assets, highlighting the quality and stability of earnings. Year-to-date, Keppel has monetised approximately $347 million in assets, primarily through divestments in China and Vietnam. In addition, asset management fees rose 9% YoY to $96 million, reflecting the growing scale and resilience of Keppel’s asset-light business model.

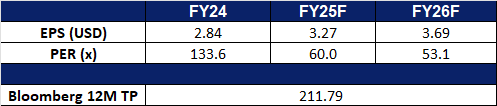

Market consensus

(Source: Bloomberg)

Wee Hur Holdings Ltd (WHUR SP): Potential rate cut tailwinds

Wee Hur Holdings Ltd provides building construction services and acts as the management or main contractor in construction projects for both private and public sectors. The Company’s clients from the private sector include property owners and developers, and those from the public sector comprise government bodies and statutory boards.

Fueling rate cut expectations. The softer-than-expected U.S. consumer price index (CPI) in May, which rose just 0.1% compared to the 0.3% forecast, has strengthened market expectations for near-term interest rate cuts. According to the CME FedWatch Tool, there is now a 59.1% probability of a Fed rate cut by September. If inflation continues to cool, monetary policy may ease sooner than anticipated. For Wee Hur Holdings, this potential shift in the interest rate environment could translate into lower borrowing costs, improved cash flow, and enhanced profitability. It also opens opportunities to refinance existing debt on more favorable terms, strengthening the company’s balance sheet and improving its financial flexibility to pursue growth initiatives.

Opportunities from Singapore’s public housing boom. Wee Hur’s construction arm recently secured two significant Housing & Development Board (HDB) projects valued at a combined S$440 million, underscoring the company’s strong positioning in Singapore’s public sector construction market. These projects come as part of a broader national housing push, with 19,600 Build-To-Order (BTO) flats planned for 2025 and over 50,000 units expected from 2025 to 2027. This government-led housing expansion presents a consistent pipeline of opportunities for Wee Hur to secure additional contracts, diversify its revenue streams, and strengthen its market share in Singapore’s construction landscape

Financial flexibility through multi-currency note programme. Wee Hur recently announced a S$500 million multi-currency medium-term note (MTN) programme which provides the company with strategic financial agility. This programme enables Wee Hur to proactively refinance existing borrowings, fund new investments and acquisitions, and support ongoing capital expenditures and working capital needs.

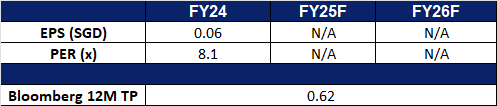

2H24 financial results. Wee Hur’s revenue decreased by 27% to S$91.67 million, compared to S$125.64 million for 2H23, mainly due to reduced construction activities and fewer units sold in the Group’s industrial development property, partially offset by stronger contributions from the Group’s first Purpose-Built Dormitory in Singapore. The Group’s net profit from continuing operations experienced a significant decline, turning into a loss of S$18.09 million in 2H24, compared to a profit of S$147.47 million 2H23. For FY24, total net profit decreased by 54% to S$56.98 million, from S$124.77 million in FY23. The decline was primarily driven by the same factors that affected the 2H24, including lower contributions from the share of profit from investments in joint ventures, higher finance expenses, and higher impairments, fair value losses, and currency exchange losses. The Group declared a final dividend of S$0.008 per ordinary share for FY24.

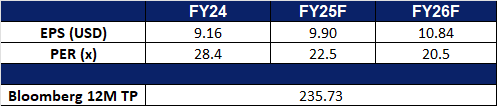

Market consensus

(Source: Bloomberg)

CGN Power Co Ltd. (1816 HK): AI boom to continue driving energy demand

BUY Entry – 2.70 Target – 3.10 Stop Loss – 2.50

CGN Power Co Ltd is a China-based company principally engaged in the production and sale of electricity. The Company primarily operates its businesses through two segments. The Nuclear Power Business Operation, Power Sales and Related Technical Services segment is primarily engaged in the construction, operation and management of nuclear power plants, the sale of electricity generated by such nuclear power plants, and the organization of the design and scientific research work for the development of nuclear power plants. The Engineering Construction and Related Technical Services segment is primarily engaged in the construction and management of nuclear power plant engineering projects, and provides construction installation and design services. The Company is also engaged in nuclear waste disposal, related investment and import and export businesses, commodity sales and other businesses, and the provision of labor services.

New nuclear reactors approved, reinforcing long-term growth potential. In April 2025, China’s State Council approved the construction of 10 additional nuclear reactors, underscoring the country’s continued strategic commitment to nuclear energy as a key pillar of its clean energy transition. This marks the fourth consecutive year that China has greenlit at least 10 new reactors. Of the newly approved projects, four have been allocated to CGN Power, designated for deployment at its Fangchenggang and Taishan sites. With 30 reactors currently under construction—representing nearly half of all global builds—China is on track to overtake the United States as the world’s largest producer of nuclear energy by the end of the decade. According to the China Electricity Council, national nuclear power capacity is expected to reach 65 gigawatts by the end of 2025, up from under 60 gigawatts in 2024. This sustained expansion positions CGN Power to benefit meaningfully over the long term.

AI-driven electricity demand to support long-term energy consumption growth. China’s accelerating adoption of artificial intelligence (AI) technologies continues to drive a surge in electricity demand, particularly from data centres. In 2024, data centres in China consumed approximately 140 billion kilowatt-hours (kWh) of electricity, up 31% year-on-year—significantly outpacing the 6.8% increase in total national power consumption. According to the China Academy of Information and Communications Technology (CAICT), this figure could reach 400 billion kWh by 2030, lifting data centres’ share of total power usage from under 2% to as high as 6%. Complementing this trend, the government recently announced a RMB60 billion state-backed fund to support early-stage AI projects, while major Chinese tech firms continue to ramp up AI infrastructure investments. This growing AI momentum is set to further bolster electricity demand, creating a supportive environment for baseload energy providers like CGN Power.

Consistent and attractive dividend profile. CGN Power declared a final dividend of RMB0.095 per share for FY2024, implying a dividend yield of 3.82% and a payout ratio of 44.36%. The company has maintained a stable payout ratio of around 43%–44% in recent years, offering investors a consistent and relatively attractive income stream compared to broader industry peers.

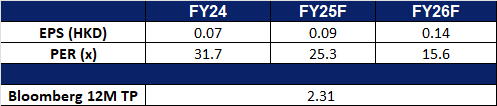

1Q25 earnings. Revenue rose by 4.41% YoY to RMB20.0bn in 1Q25, compared to RMB19.2bn in 1Q24, primarily due to an increase in on-grid power generation of the subsidiaries. Net profit fell by 16.1% to RMB3.03bn in 1Q25, compared to RMB3.48bn in 1Q24, primarily due to the comprehensive effects of an increase in power volume of market transactions, an decrease in power price and the progress of research and development. Basis EPS fell to RMB0.06 in 1Q25, compared to RMB0.071 in 1Q24.

Market consensus.

(Source: Bloomberg)

CGN Mining Co Ltd. (1164 HK): Accelerating nuclear expansion in China

CGN Mining Co Ltd is a company mainly engaged in the trading of natural uranium. The Company operates its business through three segments. The Natural Uranium Trading segment is engaged in the trading of natural uranium. The Property Investment segment is engaged in leasing business. The Other Investments segment is engaged in investment activities.

Rebound in Uranium Prices. Uranium prices climbed to a four-month high of $72 per pound in late May, driven by renewed optimism around political support for the nuclear sector. The rally followed an executive order by former U.S. President Donald Trump aimed at cutting regulatory hurdles and accelerating the licensing process for reactors and power plants—moves that could bolster long-term uranium demand. This marks a notable pivot in U.S. nuclear policy, which now seeks to scale up output in response to surging power needs from data centers and artificial intelligence infrastructure. However, despite the policy tailwind, new domestic uranium projects remain stalled amid weak market sentiment and limited investor appetite—challenges echoed across the sector. Adding to the uncertainty, potential tariffs on uranium imports continue to cloud the outlook. The U.S. relies heavily on imports from Kazakhstan and Canada, both of which are now under scrutiny. Kazakhstan faces a proposed 27% tariff, while Canadian imports could be hit with a 10% levy, further straining already tight supply chains.

Uranium future prices

(Source: Bloombeg)

China Accelerates Nuclear Expansion, Underpinned by Expanding Domestic Uranium Supply. In April 2025, China’s State Council approved the construction of 10 additional nuclear reactors, reaffirming its strategic commitment to nuclear energy as a cornerstone of its clean energy transition. This marks the fourth consecutive year that at least 10 new reactors have received approval. With 30 reactors currently under construction—accounting for nearly half of all global builds—China is poised to surpass the United States as the world’s largest nuclear energy producer by the end of the decade. The China Electricity Council projects national nuclear power capacity will reach 65 gigawatts by the end of this year, up from under 60 gigawatts in 2024. Further reinforcing this momentum, China recently announced a landmark discovery of 30 million tons of uranium reserves in the Ordos Desert—one of the largest known finds globally. The timing of this discovery is strategically aligned with China’s accelerating nuclear buildout, including the 11 reactors currently under construction. This vast domestic uranium resource is expected to enhance energy security by reducing reliance on imports and ensuring a long-term fuel supply for China’s expanding nuclear fleet. Energy analysts believe these reserves could meet national demand for generations, providing greater resilience in an increasingly uncertain global energy environment. As China ramps up reactor development, demand for uranium is set to rise sharply—creating long-term growth opportunities for uranium suppliers such as CGN Mining.

CGN Mining Extends Framework Agreements with Subsidiaries. CGN Mining Co. has announced the renewal of its framework agreements governing the sale of natural uranium and the provision of financial services with its subsidiaries. These agreements will be extended for an additional three years, starting January 2026. Classified as major and continuing connected transactions under the Hong Kong Listing Rules, the agreements are subject to approval by independent shareholders. They will also remain under annual disclosure and compliance review requirements. This extension supports operational continuity and reinforces CGN Mining’s integrated role in the CGN Group’s broader nuclear fuel and financial ecosystem.

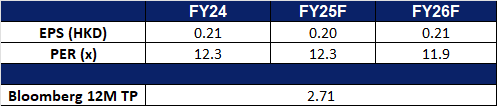

FY24 earnings. Revenue rose by 17.2% YoY to HK$8.62bn in FY24, compared to HK$7.36bn in FY23. Net profit fell to HK$342.0mn in FY24, compared to HK$497.1mn in FY23, primarily due to a loss coming from discontinued operations. Basis EPS from continuing operations and discontinued operations dropped to HK4.50cents in FY24, compared to HK$6.54cents in FY23.

Market consensus.

(Source: Bloomberg)

Palo Alto Networks Inc. (PANW US): Capitalising on cloud growth and cybersecurity demand

BUY Entry – 194 Target – 210 Stop Loss – 186

Palo Alto Networks is a multinational company focused on cybersecurity solutions, primarily providing products and services such as firewalls, cloud security, endpoint protection, and threat intelligence.

Expected rapid growth in global cloud spending in 2025. According to Gartner’s latest forecast, global end-user spending on public cloud services is expected to grow from $595.7 billion in 2024 to $723.4 billion in 2025. Spending on cybersecurity is projected to increase from $183.9 billion in 2024 to $212 billion in 2025. With the rise of artificial intelligence, more investments are flowing into the security software market, including areas such as application security, data security and privacy protection, and infrastructure protection. The cybersecurity market is expected to grow at an average annual rate of 11% before 2030.

Leader in the firewall market. The company holds about 20% of the firewall market. It has over 80,000 customers globally, covering a diverse range of industries including large enterprises, government agencies, and financial institutions. The company’s customer retention rate exceeds 90%, indicating high demand and stability for its products. Its cloud security platforms, including Prisma Cloud and Cortex XSOAR, are rapidly expanding in the market. In Q4 2024, Prisma Cloud achieved a year-over-year growth rate of 38%.

Rule of 40. The Rule of 40 is a key metric for measuring the profitability and growth of Software-as-a-Service (SaaS) companies. The company’s latest quarterly revenue growth and EBITDA margin combined reached 48.6, indicating strong performance.

3Q25 results. Revenue increased by 15.7% YoY to US$2.29bn, exceeding expectations by US$10mn. Non-GAAP earnings per share were US$0.80, surpassing estimates by US$0.03. The company raised its full-year revenue forecast for FY25 to between US$9.17bn and US$9.19bn, up from the previous forecast of US$9.14bn to US$9.19bn.

Market consensus

(Source: Bloomberg)

Check Point Software Technologies Ltd. (CHKP US): Fortifying cybersecurity through expansion and innovation

Check Point Software Technologies Ltd. develops, markets and supports a range of software and hardware products and services for information technology (IT) security and offers its customers a network and gateway security solutions, data and endpoint security solutions and management solutions.

Strategic acquisition enhancing exposure management. Check Point’s acquisition of Veriti significantly enhances its Infinity Platform by expanding real-time, automated threat exposure management across complex, multi-vendor environments. Veriti’s fully automated platform continuously identifies, prioritizes, and remediates cyber risks without disrupting business operations, offering key benefits such as automated virtual patching, seamless integration with over 70 security vendors, and real-time threat intelligence enforcement. This acquisition deepens Check Point’s partnerships with cloud-native platforms like Wiz and strengthens its prevention-first strategy by providing comprehensive, proactive security across both internal and external attack surfaces in today’s AI-driven threat landscape. By integrating Veriti, Check Point is well-positioned to streamline multi-vendor protection, accelerate cyber risk reduction, and improve operational efficiency for enterprise security teams.

Next-generation security innovation. Check Point made major advancements to its family of Quantum Force Security Gateways designed to provide enterprise-level firewall security with up to a 4x increase in threat prevention performance from previous models. Additionally, it also launched its next generation Quantum Smart-1 Management appliances, delivering 2X increase in managed gateways and up to 70% higher log rate, with AI-powered security tools designed to meet the demands of hybrid enterprises.

Strong growth efficiency. The Rule of 40 is a key metric for measuring the profitability and growth of Software-as-a-Service (SaaS) companies. Check Point Software remains slightly below the SaaS Rule of 40 benchmark with a combined revenue growth and EBITDA margin of 39.2, reflecting both strong scalability and profitability.

1Q25 results. Revenue increased by 7% year-on-year to $638 million. Products & licenses revenue and security subscriptions revenue grew by 14% and 10% year-on-year to $114 million and $ 291 million respectively. Non-GAAP earnings per share rose by 9% year-on-year to $2.21 above estimates by $0.02.

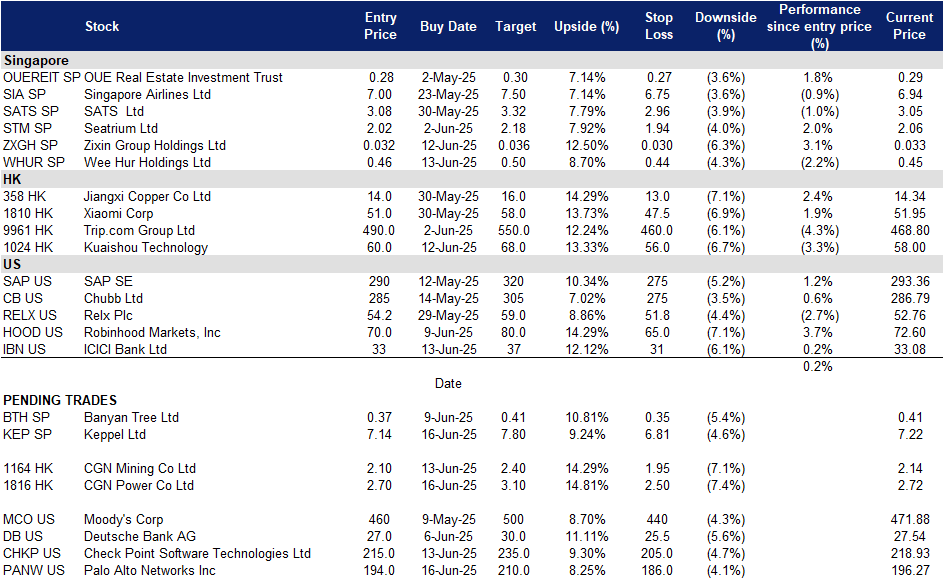

Trading Dashboard Update: Add ICICI Bank Ltd (IBN US) at US$33 and Wee Hur Holdings Ltd (WHUR SP) at S$0.46.Cut loss on Barclays Plc (BCS US) at US$17.3 and Coinbase Global Inc (COIN US) at US$240.