Zixin Group Holdings Limited is a holding company. The Company, through its subsidiaries, operates sweet potato biotech-focused value chain focuses on cultivation and supply, product innovation and snacks production, brand building, marketing, and distribution.

Replicating value chain into Hainan. Expansion into Hainan is underway. Zixin Group is actively extending its sweet potato value chain beyond Liancheng County, Fujian, into Lingao County, Hainan, through a revitalisation project spanning 8,961.33 hectares across 12 villages. The Hainan site is significantly larger than the Group’s original operations in Fujian, offering considerable potential for replication and scale. While the project remains in its early stages, Zixin anticipates majority of profit contributions beginning in late FY26 or early FY27. This marks the company’s first attempt to replicate its agricultural model outside Fujian, signalling its broader growth ambitions in the sector.

Diversifying revenue streams. Zixin continues to strengthen its presence across the sweet potato industrial value chain, resulting in a growing number of revenue streams. Recent expansion efforts have driven top-line growth, including the launch of its feedstock business with two initial orders. In addition, the development of new sweet potato-based snacks has introduced another source of income. Looking ahead, the company plans to produce and sell sweet potato flour, further expanding its processed food portfolio. The Hainan project is also expected to contribute positively to revenue over time.

Improving margins. Zixin Group saw an improvement in margins YoY in FY25. The company’s gross profit margin (GPM) rose to 34.0% in FY25, largely attributed to higher sales and lowered costs due to economies of scale. The company also recorded an operating profit margin (OPM) of 13.2% and a net profit margin (NPM) of 10.1%, the highest in over five years, largely attributed to lower costs relative to revenue. These improving margins showcased the results of Zixin Group’s integrated industrial value chain, as the company continues to expand across its value chain to optimise business processes and increase efficiencies.

FY25 financial results. Zixin Group Holdings reported FY25 revenue of RMB424.7mn, up 33.1% YoY from RMB319.0mn in FY24. The strong top-line growth was driven by higher sales volumes of both fresh and processed sweet potatoes, which increased by 72.1% and 24.1% respectively. The company also benefited from a favourable pricing environment, with local sweet potato prices increasing by an average of approximately 30% in FY24. Net profit after tax surged 220.0% to RMB42.7mn in FY25, up from RMB13.4mn in FY24, as the company continued to benefit from economies of scale and business optimisation. Basic EPS rose to 2.75 RMB cents, compared to 0.97 RMB cents a year earlier.

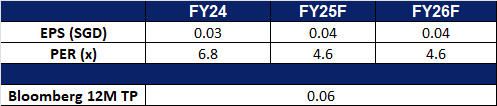

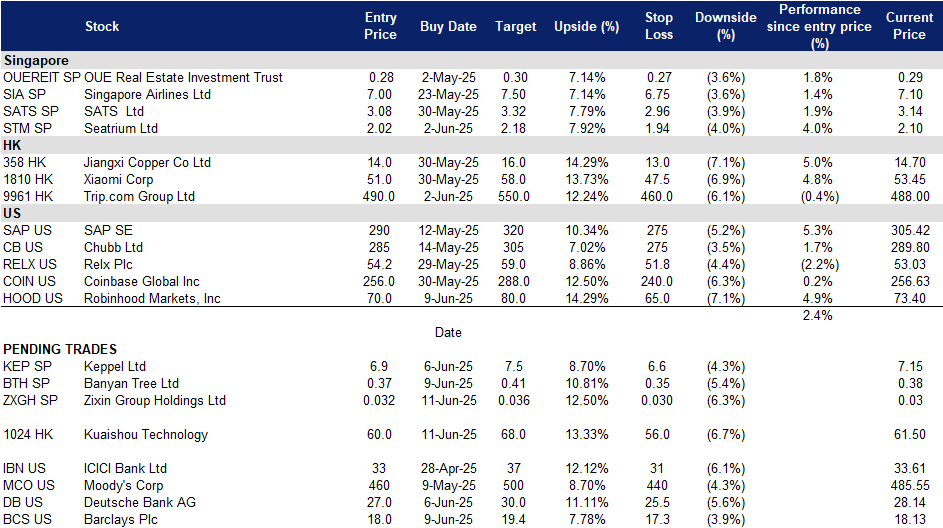

We have fundamental coverage with a BUY recommendation and a TP of S$0.060. Please read the full report here.

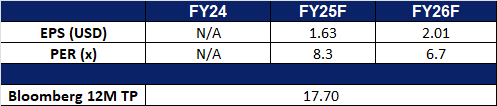

Market consensus

(Source: Bloomberg)

Banyan Tree Holdings Ltd (BTH SP): Leading Asia Pacific’s evolving travel landscape

Banyan Tree Holdings Limited operates as a holding company. The Company, through its subsidiaries, owns and manages hotel groups. The Company focuses on hotels, resorts, spas, galleries, golf courses, and residences, as well as provides investments, design, construction, and project management services. Banyan Tree Holdings serves customers worldwide.

Surging regional travel demand. According to Mastercard Economics Institute’s Travel Trends 2025 report, Asia-Pacific continues to lead global summer travel, with eight of the top 15 trending destinations, including Tokyo, Osaka, and emerging favorite Nha Trang. This momentum is underpinned by favorable exchange rates, enhanced air connectivity, and rising demand for wellness-driven, nature-based, and culinary travel. With China and India at the forefront of outbound tourism growth, travelers are seeking high-value, immersive experiences. These consumer shifts align directly with Banyan Tree Group’s brand ethos and product offerings, reinforcing the Group’s positioning within Asia-Pacific’s thriving travel ecosystem.

Resilient regional mobility. The Association of Asia Pacific Airlines (AAPA) reports robust growth in April 2025, with a 10.5% year-on-year increase in international passengers and a 12.6% rise in revenue passenger kilometres (RPK), signalling strong long-haul travel demand. Air cargo traffic also rose 4.9% despite persistent global trade headwinds. These indicators highlight sustained regional connectivity and tourism demand, which will continue to support Banyan Tree Group’s regional expansion. As international arrivals rise, Banyan Tree is well-positioned to benefit from increasing mobility and consumer interest in experience-led luxury accommodations across key Asia-Pacific markets.

Strategic global expansion. In 2025, Banyan Tree Group is accelerating its growth with the launch of 15 new hotels and five branded residences across diverse geographies. The recent opening of Mandai Rainforest Resort in Singapore marked the Group’s 100th property and its debut in its home market. Other key developments include Ubuyu, its first African safari lodge in Tanzania, and an integrated lifestyle hub in Bangkok. Expansion in the Caribbean and across Asia, China, Korea, Thailand, and the Philippines, underscores the Group’s multi-brand strategy and its focus on delivering authentic, locally inspired hospitality. This global pipeline positions Banyan Tree to meet rising demand for meaningful, destination-driven travel.

FY24 business updates. Banyan Tree Holdings reported a 16% increase in revenue to S$380.6 million, mainly due to robust growth across all business segments. Operating Profit increased by S$13.1 million to S$103.2 million, attributable to higher contributions from the Hotel Investments and Residences segments due to higher revenue. PATMI rose to S$42.1 million from the previous S$31.7 million in FY23 and earnings per share rose to S$0.049 compared to S$0.037 in FY23. As of FY24, the Group recorded a total of 91 hotels and resorts, 73 spas, 68 galleries and 22 branded residences in 22 countries. During the year, the group reported 17 new hotel and resort openings, with six in Japan and South Korea, and eight in China as part of the Group’s multi-brand expansion strategy across Asia.

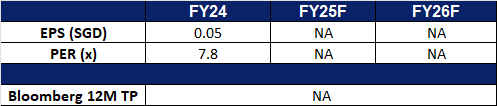

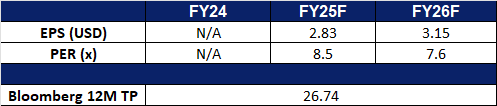

Market consensus

(Source: Bloomberg)

Kuaishou Technology (1024 HK): Reaping the success of its AI investment

BUY Entry – 60.0 Target – 68.0 Stop Loss – 56.0

Kuaishou Technology is an investment holding company mainly engaged in the operation of content communities and social platforms. The Company mainly provides live streaming services, online marketing services and other services. The online marketing solutions include advertising services, Kuaishou fans headline services and other marketing services. Other services include e-commerce, online games and other value-added services. The Company also develops new businesses, such as local services, Kwai Hire and Ideal Housing. The Company operates its business in domestic market and overseas markets.

Kling AI Showing Strong Monetization Potential. Kuaishou’s Kling AI is demonstrating rapid growth and strong monetization. Less than a year after its launch, Kling achieved an annualized revenue run rate exceeding $100 million as of March. The recently released Kling AI 2.1 brings enhanced motion precision, more realistic dynamic effects, and improved cost efficiency, enabling creators and businesses to generate more compelling content and advertisements. Monthly subscription bookings surpassed RMB 100 million (approximately $13.9 million) in both April and May. With this momentum, Kling has become one of the world’s highest-grossing AI video generation tools, underscoring Kuaishou’s competitive edge in generative AI. The company expects Kling to reach $100 million in cumulative sales by February, reflecting strong user demand and commercial traction.

Continued Strategic Investment in AI. Kuaishou remains committed to AI development and recently announced plans to ramp up investment in this area. The company expects year-on-year increases in AI-related spending, primarily to attract and retain top-tier AI talent. Management noted that this will likely compress profit margins by 1 to 2 percentage points in 2025. However, the financial impact is expected to be manageable, as revenue growth and greater operating leverage help offset the cost. The success of Kling AI reinforces the strategic importance and long-term potential of continued AI investments.

618 Shopping Festival to Boost GMV. The ongoing 618 shopping festival—a major mid-year sales event in China—is expected to drive higher gross merchandise value (GMV) for Kuaishou. E-commerce platforms began promotional campaigns as early as early June, with live-streaming platforms like Kuaishou well-positioned to capitalize on the increased consumer activity. In 1Q25, Kuaishou recorded 408 million average daily active users (DAUs) and 712 million monthly active users (MAUs), representing year-over-year growth of 3.6% and 2.1%, respectively. This uptick in traffic is likely to support higher GMV and, in turn, contribute to stronger profitability.

1Q25 earnings. Revenue rose by 10.9% YoY to RMB32.6bn in 1Q25, compared to RMB29.4bn in 1Q24. Net profit fell by 3.4% to RMB3.98bn in 1Q25, compared to RMB4.12bn in 1Q24. Basis EPS fell to RMB0.93 in 1Q25, compared to RMB0.95 in 1Q24.

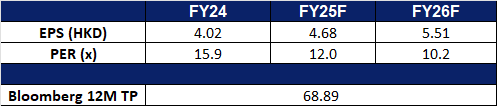

Market consensus.

(Source: Bloomberg)

Jiangxi Copper Co Ltd. (358 HK): Optimism in the economy

Jiangxi Copper Co Ltd is a China-based company mainly engaged in the mining, smelting and processing of copper and gold. The Company mainly conducts businesses through two segments. The Copper-related Industry segment is mainly engaged in the production and sales of copper and copper-related products. The Gold-related Industry segment is mainly engaged in the production and sales of gold and gold-related products. The Company’s products mainly include cathode copper, gold, silver, sulfuric acid, copper rods, copper tubes, copper foil, selenium, tellurium, rhenium and bismuth. The Company’s products are mainly used in electrical, electronic, light industry, machinery manufacturing, construction, transportation, military industry and other industries. The Company principally conducts its businesses in the domestic market.

Market optimism rises following Trump–Xi phone call. Investor sentiment improved after a phone call between U.S. President Donald Trump and Chinese President Xi Jinping last Thursday, during which both leaders agreed to resume trade negotiations in an effort to avoid a full-blown tariff war. Key concerns—such as tariffs on rare earth materials, U.S. restrictions on chip exports, and limitations on student visas—were reportedly addressed. The call, which Trump described as “very good,” helped ease fears of prolonged trade tensions and raised hopes for a near-term resolution. The renewed optimism also lifted regional equity markets and is expected to support copper prices on expectations of stronger economic activity.

Copper demand expected to outstrip supply in the long term. The International Energy Agency (IEA) projects a significant copper supply gap by 2035, estimating that supply could lag demand by as much as 30%. Global copper demand is forecast to grow around 2% in 2025, driven by the accelerating adoption of renewable energy, electric vehicles (EVs), and digital infrastructure. As a critical material in nearly all electrical systems, copper is poised to face sustained demand growth, putting upward pressure on prices. With China processing over 70% of the world’s top 20 energy transition minerals—including copper—Chinese producers such as Jiangxi Copper are well-positioned to benefit from the tightening market and rising prices.

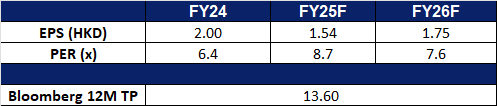

Copper Prices

(Source: Bloomberg)

More stake in SolGold and potential access to strategic assets. Earlier this year,Jiangxi Copper acquired about 157mn shares in SolGold. Following the investment, Jiangxi Copper, through its subsidiary Jiangxi Copper (Hong Kong) Investment Company Limited, would increase its holding in SolGold from 6.95% to 12.19% of the company’s total issued share capital. By increasing its stake in SolGold, Jiangxi Copper gains a larger ownership share and consequently, more influence over SolGold’s decisions. This is particularly important concerning the Cascabel project, a major copper/gold asset. This strategic increase in ownership aligns with JCC’s objective of securing access to vital copper resources.

1Q25 earnings. Revenue fell by 8.90% YoY to RMB111.6bn in 1Q25, compared to RMB122.5bn in 1Q24. Net profit increased by 37.1% to RMB2.48bn in 1Q25, compared to RMB1.81bn in 1Q24. Basis EPS rose to RMB0.57 in 1Q25, compared to RMB0.50 in 1Q24.

Barclays Bank is a global financial institution headquartered in London, UK, providing a diverse range of financial services, including retail banking, credit cards, wholesale banking, investment banking, wealth management, investment management, various lending products, and securities trading.

UK enters rate cut cycle. In May, the Bank of England cut the benchmark interest rate by 25 basis points to 4.25%, marking the fourth rate cut since August 2024. UK inflation is on a downward trend, and monetary policy is shifting towards easing. Additionally, the UK’s first-quarter growth leads the G7 nations at 0.71%.

Strong demand for mortgages in the UK. According to forecasts from the EY ITEM Club, the UK’s mortgage growth rate is expected to rise from 1.5% in 2024 to 3.1% in 2025, indicating a rebound in market activity. UK Finance predicts that total mortgage lending in 2025 will reach £260 billion, with home loans at £148 billion, and remortgaging activity is expected to grow by 30% to £76 billion.

Significant growth in mortgage loan book. Barclays’ mortgage loan book has grown rapidly over the past few quarters. In Q1 of FY25, the total loan amount reached £8.5 billion, the highest level in three years. The bank maintains a strategy of increasing mortgage credit risk, with the proportion of high loan-to-value ratios (85% or above) rising to 22% in the first quarter.

1Q25 results. In Q1 of FY25, revenue increased by 11% year-on-year to £7.71 billion. Pre-tax profit grew by 19% year-on-year to £2.7 billion, exceeding market expectations of £2.49 billion. Earnings per share rose by 26% year-on-year to 13 pence, with a return on equity of 14%.

Deutsche Bank AG is a global financial service provider delivering commercial, investment, private, and retail banking. The Bank offers debt, foreign exchange, derivatives, commodities, money markets, repo and securitization, cash equities, research, equity prime services, loans, convertibles, advice on M&A and IPO’s, trade finance, retail banking, asset management, and corporate investments.

Navigating lower rates. With Eurozone inflation easing to 1.9% in May, just below the European Central Bank’s (ECB) 2% target, the ECB initiated a rate cut, lowering its deposit facility rate by 25 basis points to 2%. As interest rates in Europe trend lower, Deutsche Bank has demonstrated its ability to adapt by growing fee-based revenue streams. This is reflected in its robust Q1 results, including strong performance in Fixed Income and Currencies revenue, as well as a €95 billion increase in assets under management across its Private Bank and Asset Management divisions over the past year. Deutsche Bank remains resilient as it strategically shifts toward a more diversified and sustainable revenue growth model in a lower-margin environment.

Mastercard partnership and open banking focus. Deutsche Bank’s strategic partnership with Mastercard leverages open banking and account-to-account (A2A) payments to enhance its Request to Pay (R2P) services. This collaboration introduces real-time, direct-from-account payment options for merchants, improving transaction transparency, reconciliation, and cost-efficiency. The move aligns with growing demand for flexible, secure digital payments and positions Deutsche Bank at the forefront of Europe’s payments modernization. As adoption of A2A and open banking accelerates, the partnership could become a cornerstone of Deutsche Bank’s long-term digital infrastructure strategy. Deutsche Bank’s strategic partnership with Mastercard strengthens its position in Europe’s evolving payments ecosystem and reinforces its push into scalable, digital-first financial infrastructure.

1Q25 results. Revenue rose 10% YoY to €8.5bn. Both profit before tax and net profit increased by 39% YoY to €2.8bn and €2.0bn respectively. It also achieved net inflows of €26bn across its Private Bank and Asset Management business. For FY25, the bank anticipates revenue of about €32bn.