Food Empire Holdings Limited operates as a food and beverage manufacturing and distribution company. The Company offers beverages and snacks including classic and flavoured coffee mixes and cappuccinos, chocolate drinks, fruit-flavoured and bubble teas, cereal blends, and crispy potato snacks. Food Empire Holdings serves customers worldwide.

Sustained Growth in Southeast Asia to Drive Topline Expansion. Food Empire continues to see strong revenue growth in its Southeast Asian markets, particularly in Vietnam, where demand remains robust. The region’s revenue increased 27.3% to US$129.4 million, driven by past and ongoing investments in brand development. Management expects this momentum to continue, supported by strategic commercial initiatives aimed at capturing opportunities across the region. In Vietnam, the Group is focused on strengthening brand presence and accelerating consumer acquisition to sustain its growth trajectory. The country’s coffee market is projected to grow at a CAGR of 8.13% over the next five years, reaching US$552.6 million by 2025—a trend that Food Empire is well-positioned to capitalize on. In Malaysia, the Group completed the expansion of its non-dairy creamer manufacturing facility in 2Q2024, with production capacity expected to reach full utilization within the next two to three years. Additionally, its snack manufacturing facility expansion is set for completion in 1Q2025, with commercial production beginning in 2Q2025. These initiatives will continue fueling strong growth in the Group’s Southeast Asian operations in FY25.

Expansion of Production Capabilities to Strengthen Market Leadership. As part of its regional expansion strategy, Food Empire is investing in new production facilities to enhance supply chain efficiency and market positioning. By end-2025, the Group expects to complete its first coffee-mix production facility in Kazakhstan, improving service efficiency across Central Asia. In Vietnam, Food Empire has committed to building a freeze-dried soluble coffee manufacturing facility, expected to be completed by 2028. This investment will further establish the Group as one of Asia’s leading producers of freeze-dried soluble coffee. These expansions will not only strengthen Food Empire’s supply chain but also reinforce its market leadership across key regions.

Defensive F&B industry globally. The global food and beverage industry is inherently defensive, driven by stable demand for essential consumer goods rather than discretionary spending. This resilience provides a natural hedge during economic downturns, as consumers continue to prioritize necessities. Food Empire further strengthens its position through its diversified distribution network, which helps mitigate regional economic risks and ensures a steady revenue stream. While industry challenges such as supply chain fluctuations and rising operational costs persist, the company’s strategic focus on core product categories and efficient supply chain management reinforces its stability. As a result, Food Empire remains well-positioned within the globally defensive F&B sector, offering investors a degree of protection against economic volatility.

2H24 results review. Total revenue for 2H24 increased by 10.4% YoY to US$251.1mn from US$227.5mn in 2H23, led by strong growth in its South-East Asia, South Asia, as well as Ukraine, Kazakhstan and Commonwealth of Independent States segments. Its net profit fell 3.2% to US$28.9mn for 2H24, from US$29.8mn in the same period the year before. EPS for the period stood at US$0.0549, down from US$0.0567. The group proposed a dividend per share of S$0.08, comprising a final dividend of S$0.06 and a special dividend of S$0.02.

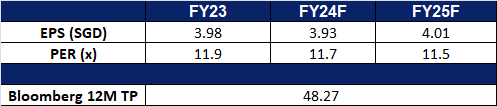

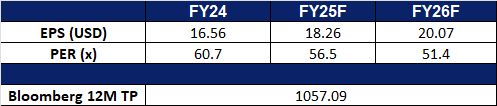

We have fundamental coverage with a BUY recommendation and a TP of S$1.35. Please read the full report here.

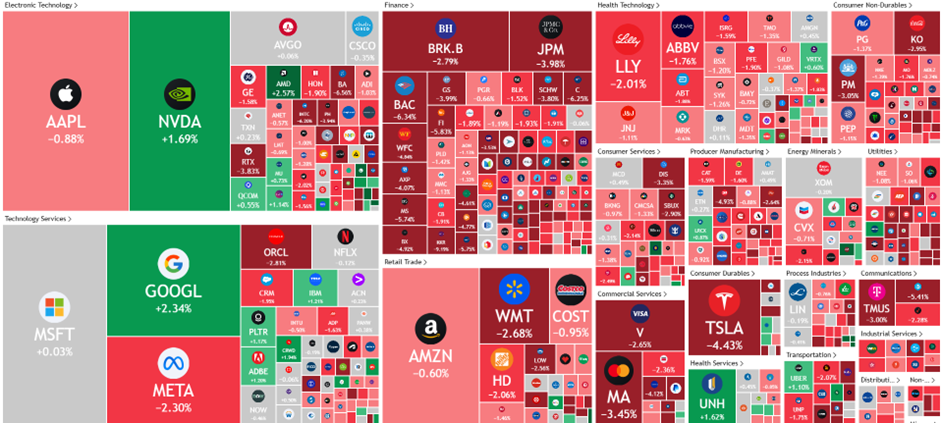

Market Consensus.

(Source: Bloomberg)

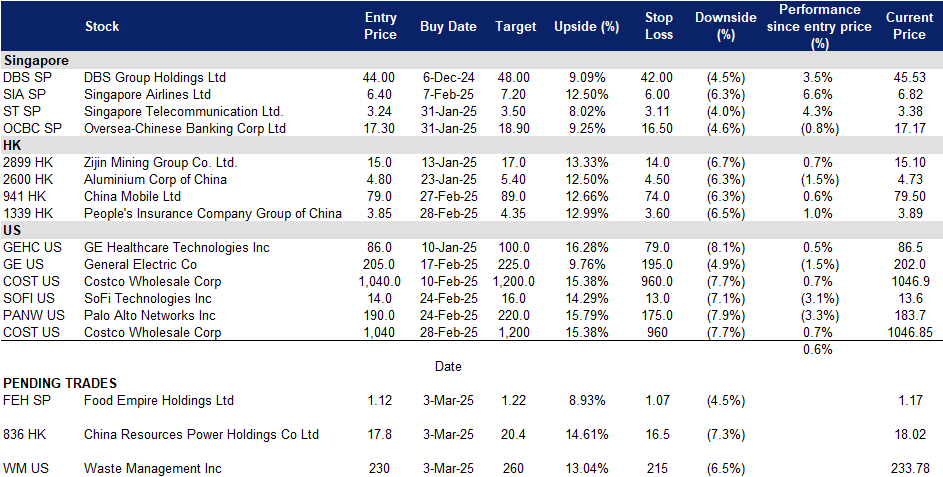

DBS Group Holdings Ltd (DBS SP): Budget’25 to boost economy

DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

Potential benefits from budget. On 18 February, Prime Minister Lawrence Wong announced a bonanza of vouchers, credits, tax rebates and enhanced wage support for Singaporeans and corporations. Singapore’s budget 2025 introduced measures that could bolster local banks by stimulating economic activity and improving credit conditions. Infrastructure investments, including top-ups to key funds, are likely to drive higher loan demand. The 50% corporate tax rebate for SMEs may ease financial pressures, reducing asset quality risks for banks. Consumer-focused initiatives could support spending while mitigating inflationary risks, lowering non-performing loans. Additionally, incentives for SGX listings and fund management may enhance capital market activity, benefiting banks through increased trading volumes and demand for financial products. Overall, the budget measures are expected to create a favourable environment for Singapore banks, driving loan growth, improving asset quality, and supporting broader financial sector activity.

Leadership changes ahead of CEO transition. DBS Bank has appointed Derrick Goh as its first Group Chief Operating Officer (COO), effective 1 April, overseeing operations and transformation. He will also join the bank’s executive committee. Koh Kar Siong will take over as head of audit and join the management committee. Additionally, Jimmy Ng, current head of operations, will retire on 1 July but continue as a senior adviser for AI until year-end. These changes come as Piyush Gupta prepares to step down as CEO on 28 March, with Tan Su Shan, deputy CEO since August 2024, set to succeed him. The leadership changes at DBS Bank signal a strategic transition aimed at sustaining growth and strengthening its operational and digital transformation efforts. DBS’ leadership changes reinforce its commitment to operational efficiency, and governance, ensuring continued growth amid evolving global banking trends. The bank is well-positioned for sustained profitability and market leadership under its new executive team.

Special bonus and capital return amid record profits. DBS will distribute a one-time S$1,000 bonus to all staff except senior managers, totaling S$32 million, as a reward for their contribution to its record performance. This bonus will benefit 90-95% of employees. The bank also announced a capital return dividend of S$0.15 per share per quarter for FY25, with plans for similar distributions over the next two years. This is part of its strategy to reduce excess capital through dividends, special payouts, and share buybacks. For 4Q24, DBS reported a net profit of S$2.52 billion, 11% YoY increase, bringing its full-year net profit to a record S$11.29 billion, up 12% YoY. Despite macroeconomic uncertainty, interest rate trends and geopolitical risks, DBS managed to outperform expectations. We believe that the bank remains well-positioned for long-term growth, backed by record earnings, strong leadership succession, and continued investment in technology.

4Q24 results review. Total income for 4Q24 rose 11% to S$5.51bn and net profit rose 11% YoY to S$2.52bn, compared with S$2.27bn from the year-ago period. DBS’ full-year net profit was brought to a new record high of S$11.29bn, up 12% from the year-ago period. DBS declared Q4 dividend at S$0. 0.15 per share per quarter to be paid out over financial year 2025; it expects to pay out a similar amount of capital in the next two years.

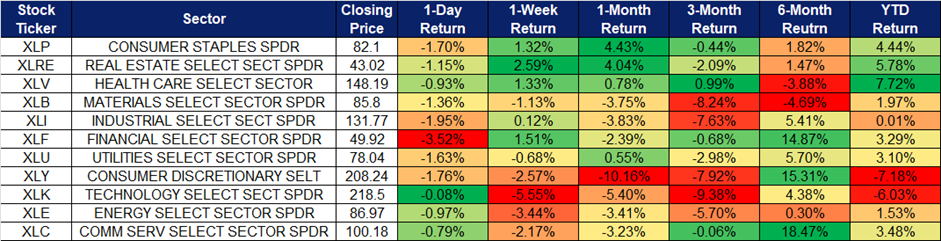

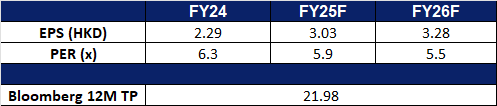

Market Consensus.

(Source: Bloomberg)

China Resources Power Holdings Co Ltd (836 HK): Continued growth in electricity demand

China Resources Power Holdings Company Limited is a Hong Kong-based investment holding company principally engaged in the investment, development and operation of power plants. The Company operates through three segments. Thermal Power segment is engaged in the investment, development, operation and management of coal-fired power plants and gas-fired power plants, as well as the sales of heat and electricity. Renewable Energy segment is engaged in wind power generation, hydroelectric power generation and photovoltaic power generation, as well as the sales of electricity. Coal Mining segment is engaged in the mining of coal mines, as well as the sales of coal. The Company mainly operates businesses in China.

Robust Electricity Demand Growth in China. According to the IEA’s Electricity 2025 report, global electricity demand is set to accelerate, with emerging and developing economies driving 85% of additional consumption over the next three years. China, in particular, has experienced electricity demand outpacing GDP growth since 2020. Consumption rose 7% in 2024 and is expected to grow at an average rate of 6% annually through 2027. This increase is largely driven by industrial demand, including energy-intensive manufacturing in sectors such as solar panels, batteries, electric vehicles, and associated materials. As China’s power consumption continues to climb, China Resources Power Holdings stands to benefit significantly from sustained demand growth.

Strong Growth in Renewable Energy Generation. Despite an overall decline in energy generation in January—primarily due to an 11.0% YoY drop in thermal power output and the impact of the Chinese New Year holiday—China Resources Power Holdings saw significant growth in its renewable energy segment. Wind power generation increased 14.1% YoY to 4,266,011 MWh, solar (photovoltaic) power generation surged 45.4% YoY to 565,676 MWh, while hydropower generation rose 18.9% YoY to 162,395 MWh. This strong performance underscores the company’s strategic shift towards renewable energy expansion, aligning with China’s clean energy transition goals. As government policies continue to support renewable energy adoption, China Resources Power Holdings is well-positioned to benefit from rising demand and favorable regulatory tailwinds.

Optimizing Capital Structure to Support Future Growth. In late 2024, China Resources Power Holdings raised HK$3.89bn through a share placement aimed at debt repayment and corporate management initiatives. The company placed 198.5mn shares (over 4% of total share capital) at HK$19.70 per share, a 5.1% discount to the last closing price of HK$20.75 on October 22. In a separate transaction, it issued 168.1mn shares to its controlling shareholder, China Resources (Holdings), under a subscription agreement for HK$3.31bn. These capital-raising efforts enhance financial flexibility, optimize the company’s capital structure, and provide resources to fuel future expansion. With a stronger balance sheet, China Resources Power Holdings is well-positioned to support its renewable energy ambitions and long-term growth strategy.

1H24 earnings. Revenue fell marginally by 0.71% YoY to HK$51.1bn in 1H24, compared to HK$51.5bn in 1H23. Net profit increased by 40.6% to HK$9.95bn in 1H24, compared to HK$7.08bn in 1H23. Basic EPS rose to HK$1.95 in 1H24, compared to a basic EPS of HK$1.40 in 1H23.

China Mobile Ltd is a company mainly engaged in the provision of communication and information services. The Company’s businesses include customer market business, home market business, business market business and new market business. The customer market business mainly provides fifth-generation mobile communication technology (5G) mobile services and brand differentiated service operations. The home market business mainly provides home wired broadband services, mobile housekeeping smart services and smart home value-added services. The business market business is engaged in the research and development and sales of cloud computers and Internet of Things card services. The new market business includes international business, equity investment, digital content and financial technology.

AI integration. Earlier this month, China Mobile, along with other major Chinese telecom companies, announced the integration of DeepSeek’s artificial intelligence (AI) models into their services and products. The move follows a broader trend among the country’s top tech firms, including Alibaba Group, Tencent Holdings and Baidu Inc, which have ramped up support for DeepSeek’s latest AI models on their respective platforms. While these telecom giants have been developing their own large language models (LLMs) over the past two years amid a global AI boom spurred by OpenAI, they primarily leverage DeepSeek’s models for cloud-based applications. China Mobile, in particular, has incorporated DeepSeek’s full suite of models—from DeepSeek-V1 to the latest DeepSeek-R1—into its computing platform. This enables businesses of all sizes to access the models, deploy application programming interfaces (APIs), and build new AI agents on its platform.

Growth in smart devices and 5G adoption. China’s mobile phone market experienced robust growth in 2024, with total shipments increasing by 8.7% to 314 million units. Notably, December 2024 saw a significant YoY surge of 22.1%, reaching 34.53 million units. 5G smartphones dominated the market, accounting for 88.1% of December shipments and 86.6% of total annual shipments. This trend is supported by China’s rapidly expanding 5G infrastructure, which now includes over 4.25 million 5G base stations and serves more than 1 billion 5G users. The rise in smart device adoption, particularly 5G-enabled phones, is expected to drive an expansion of China Mobile’s customer base, as more users seek high-speed connectivity and advanced mobile services.

Strategic cooperation agreement to deepen AI development. China Mobile recently announced a strategic cooperation agreement with Chengdu City to deepen collaboration across multiple sectors. Under this agreement, the two parties will enhance infrastructure development in AI, 5G-A, and next-generation networks, drive technological innovation and commercialization, and strengthen partnerships in areas such as supply chains, industrial investment, and intelligent hardware. They will also explore opportunities in smart cities, the data industry, 5G-powered industrial internet applications, and the low-altitude economy, fostering high-quality growth in Chengdu’s electronic information and audio-entertainment industries. This initiative is expected to further position China Mobile to capitalize on China’s expanding AI landscape.

9M24 earnings. Revenue rose by 2.0% YoY to RMB791.5bn in 9M24, compared to RMB775.6bn in 9M23. Profit attributable to equity shareholders was RMB110.9bn, up by 5.1% YoY from RMB105.5bn. Basic earnings per share was RMB5.18 in 9M24, compared to a basic earnings per share of RMB4.94 in 9M23.

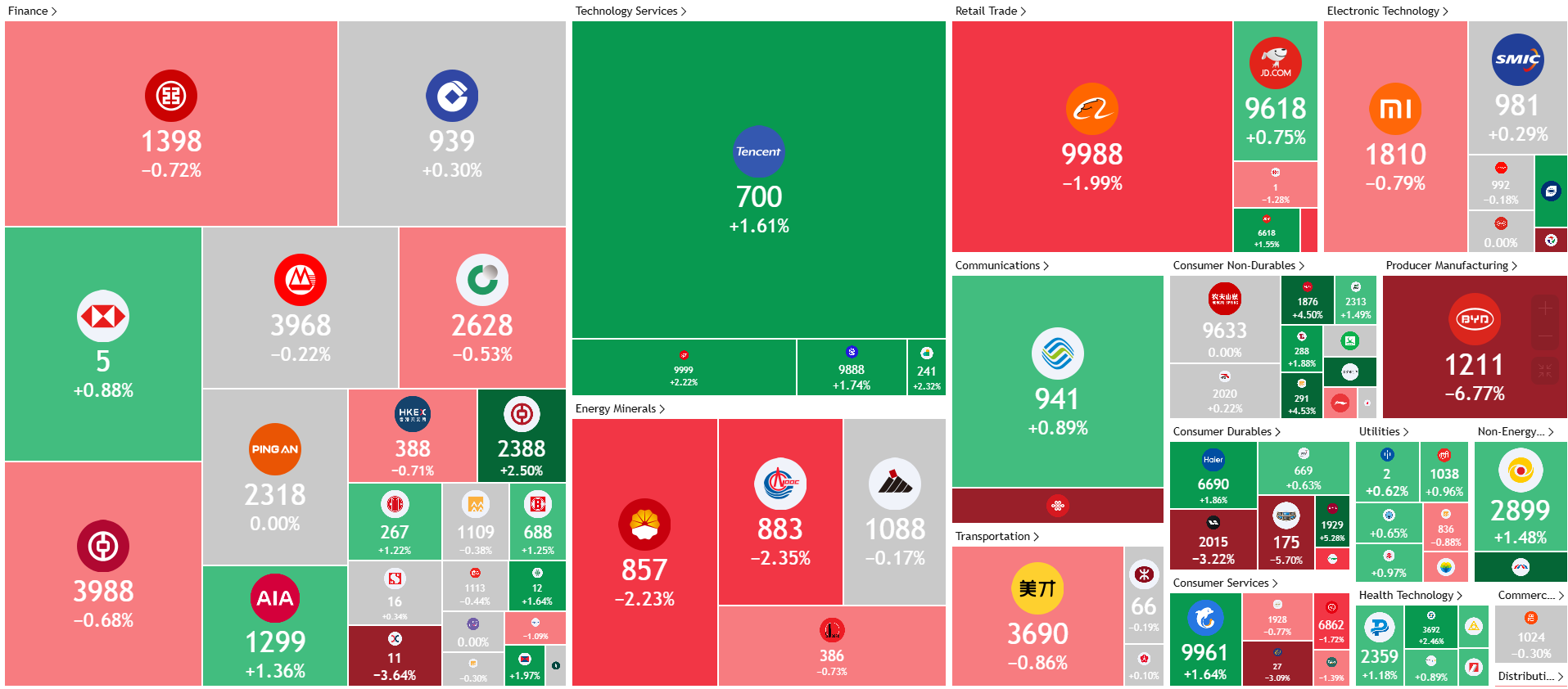

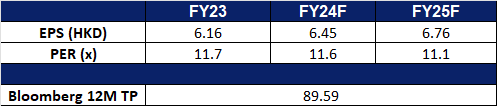

Market consensus.

(Source: Bloomberg)

Waste Management Inc (WM US): Unshaken by inflation

Waste Management Inc, through its subsidiaries, provides environmental solutions for residential, commercial, industrial, and municipal customers in the United States, Canada, Western Europe, and other international regions.

Resilient business model. The company’s operating model is similar to a public utility, providing essential waste management services that maintain consistent demand regardless of economic conditions. This allows the company to sustain stable growth even during economic uncertainty or periods of inflation. While macroeconomic fluctuations (such as tariff policies) may impact broader markets, the necessity of waste management services ensures the company’s importance and resilience.

Synergies from acquisitions. Last year, the company successfully acquired Stericycle for $7.2 billion, making it a leader in the medical waste recycling market. It expects to generate $250 million in synergies over the next three years. For fiscal year 2025, the company anticipates revenue between $25.55 billion and $25.8 billion, demonstrating confidence in its growth potential.

4Q24 results. Revenue grew 12.8% YoY to US$5.89bn, missing estimates by US$20mn. Non-GAAP EPS was US$1.70, missing expectations by US$0.10. The company projected FY25 revenue of between US$25.55bn to US$25.80bn.

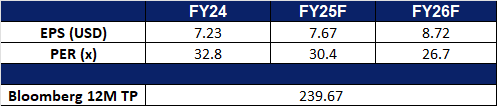

Market consensus

(Source: Bloomberg)

Costco Wholesale Corp (COST US): Counter inflationary play

Costco Wholesale Corporation is a membership-only warehouse club. The company sells a wide variety of merchandise, including groceries, automotive supplies, toys, hardware, sporting goods, jewelry, electronics, apparel, health and beauty products, and other miscellaneous items. Costco Wholesale serves consumers worldwide.

Rising inflation does not hinder good sales growth. U.S. inflation remained high in January, while U.S. retail sales fell by 0.9% month-over-month and rose by 4.2% year-over-year. The company’s U.S. comparable net sales in January rose by 9.2% year-over-year to $19.51 billion. 36% of the company’s members have an annual income exceeding $125,000, a group that is relatively less affected by inflation and has more stable spending habits. Because the company’s primary target customer base is relatively high-income, membership retention rates are high.

Defensive and growth attributes. The company’s business model differs from that of general large supermarkets, which maintain operations through low-profit, high-volume sales. Costco maintains ultra-low wholesale prices, and its main source of profit is membership fees. The growth of membership numbers and increases in membership fees are long-term growth drivers. As of December 2024, the number of paid household memberships reached 77.4 million, an increase of approximately 8% year-over-year, and the total number of cardholders reached 138.8 million. The global membership renewal rate is 90.4%. In addition, since September 1, 2024, membership fees in the United States and Canada have been increased, with the annual fee for regular memberships increasing from $60 to $65, and the annual fee for executive memberships increasing from $120 to $130. Membership fees in South Korea will increase by 7.5% to 15.2% in May 2025. The company currently operates 897 warehouses in 13 countries and plans to open 29 new warehouses in 2025, 12 of which will be outside the United States.

1Q25 results. Revenue grew 7.5% YoY to US$62.15bn, beating estimates by US$150mn. Non-GAAP EPS was US$3.82, exceeding expectations by US$0.03.