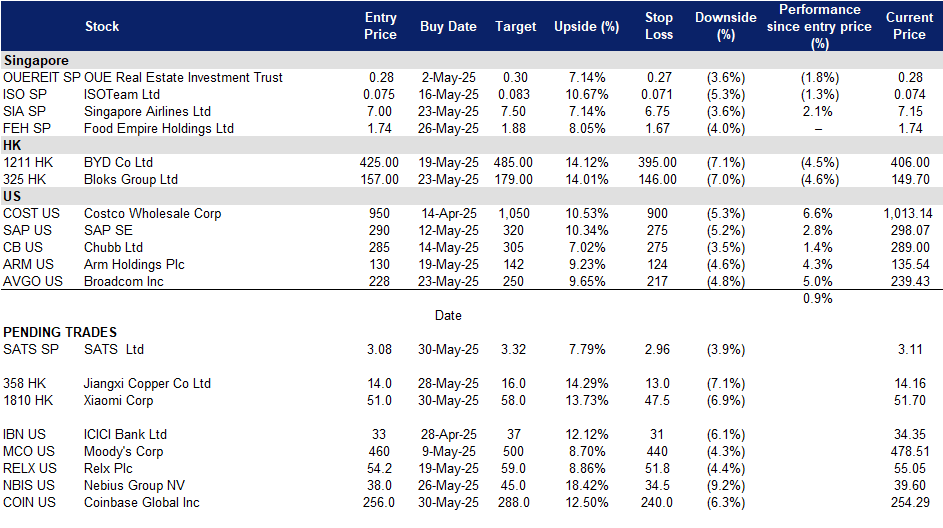

SATS Ltd (SATS SP): Rising business volume and higher rates to accelerate growth

BUY Entry – 3.08 Target – 3.32 Stop Loss – 2.96

SATS Ltd. provides air cargo handling services and food solutions. The Company offers airfreight and ground handling services including passenger, ramp and baggage handling, aviation security, aircraft cleaning and aviation laundry, and food distribution and logistics. SATS serves clients worldwide.

Outperformance driving momentum. SATS posted a robust FY25 performance, with profit surging more than three-fold to S$243.8 million on the back of a 13% YoY revenue increase to S$5.8 billion. Gateway Services revenue grew 10.6% driven by strong air cargo demand, while Food Solutions revenue jumped 22% amid a rebound in aviation travel. Operating profit nearly doubled to S$475.7 million, lifting margins from 4.7% to 8.2%. Total equity rose to S$2.77 billion, and free cash flow turned positive at S$228.3 million, reflecting enhanced cash generation. SATS remains focused on debt reduction and reinvesting in operations to drive shareholder value.

Strategic expansion to capture future growth. SATS plans to invest over S$250 million to modernize and expand its ground support and cargo handling capabilities at Changi Airport, positioning itself ahead of Terminal 5’s expected opening in the mid-2030s. This includes more than S$150 million to renew and electrify over 40% of its ground support fleet within five years, and S$100 million to enhance cargo operations, boosting peak handling capacity by over 50%. SATS will also upskill its 7,800-strong workforce and adopt technologies such as autonomous vehicles and AI to meet rising air traffic and maintain Singapore’s status as a top global air hub. Looking ahead, we believe these initiatives will fortify SATS’ competitive position, support robust passenger and cargo growth and ensure long-term value creation as Singapore Changi Airport expands.

4Q25 Business Updates. SATS Ltd reported 10.4% YoY revenue growth to S$1,476.7mn from S$1,337.7mn in the corresponding year-ago period, driven by increased business volume and rate improvements. Its net profit rose 18.3% YoY to S$38.7mn from S$32.7mn in 4Q24, delivering EPS of S$0.026 for the quarter. After shareholder approval, its proposed final dividend of S$0.035 per share will be distributed on 15 August, higher than the final dividend of S$0.015 per share in 4Q24.

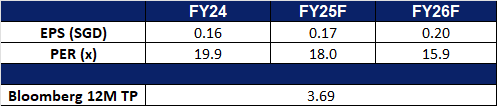

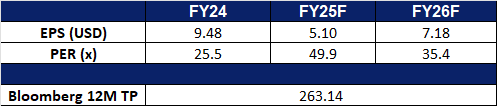

Market consensus

(Source: Bloomberg)

Food Empire Holdings Ltd (FEH SP): Brewing a growth recipe in Asia

Food Empire Holdings Limited operates as a food and beverage manufacturing and distribution company. The Company offers beverages and snacks including classic and flavoured coffee mixes and cappuccinos, chocolate drinks, fruit-flavoured and bubble teas, cereal blends, and crispy potato snacks. Food Empire Holdings serves customers worldwide.

Continued strong growth in Asia. Food Empire experienced a sustained increase in sales across its core markets in 1Q24, showcasing continued strong consumer demand for the company’s products, especially in the Southeast Asia and South Asia regions, which continued to see growth of over 30% in 1Q25. The group continues to reap the benefits of its brand-building efforts in Vietnam, increasing its market share across the Vietnamese market, with revenue growing 44.6% YoY. This has significantly boosted Food Empire’s Southeast Asia revenue contribution, taking the top spot and contributing to 29.2% of the group’s total sales in 1Q25. Demand for the group’s products in South Asia also remains strong amidst a coffee consumption boom in the region.

Expanding production capabilities across Asia. Food Empire is significantly expanding its production capabilities across Asia to meet growing demand. In Vietnam, a new freeze-dried soluble coffee facility is set to begin construction by late 2025 and become operational by 2028, bolstering its ingredients business. Meanwhile, its Malaysian snack manufacturing facility will increase output by about 50% by the third quarter of 2025 after an expansion is completed in the first half. Outside Southeast Asia, Food Empire’s first coffee-mix plant in Kazakhstan is expected to be finished by the end of 2025, boosting overall coffee-mix capacity by approximately 15% and extending its reach into Central Asia. These strategic expansions are set to drive continued top-line growth across its key Asian markets.

Capturing market growth and demand in Vietnam. Vietnam remains a strategic growth focus for Food Empire, underpinned by its position as the company’s fastest-growing market. In 1Q25, Vietnam’s GDP expanded by 6.93% YoY, marking the highest first-quarter growth since 2020 despite a quarter-on-quarter slowdown. The World Bank forecasts 5.8% GDP growth for 2025, while the Vietnamese Parliament maintains a more optimistic target of 8%. This strong economic outlook bodes well for Food Empire’s continued expansion in the country. The Group’s investments in marketing, consumer engagement, and production capacity are expected to reinforce its brand presence and position it to capture long-term growth opportunities in Vietnam’s rapidly developing economy.

1Q25 Business Updates. Food Empire Holdings reported higher revenue of US$136.6mn for 1Q25, up 16.3% YoY, compared to US$117.5mn in 1Q24, led by strong growth in its Southeast Asia and South Asia markets, which saw a growth of 33.8% and 31.7% respectively. The company’s markets in Ukraine, Kazakhstan and CIS experienced growth of 14.6% YoY, while the Russian market saw a slight increase in revenue of 0.5% YoY. The company experienced revenue growth across all key markets, demonstrating robust consumer demand despite increased prices due to higher raw material costs and ongoing global geopolitical tensions.

We have fundamental coverage with a BUY recommendation and a TP of S$1.95. Please read the full report here.

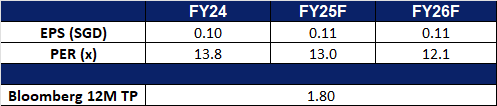

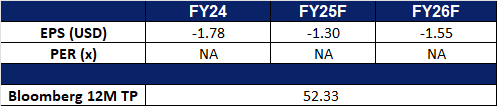

Market consensus

(Source: Bloomberg)

Xiaomi Corp. (358 HK): Strength across different markets

BUY Entry – 51.0 Target – 58.0 Stop Loss – 47.5

Xiaomi Corp is an investment holding company primarily engaged in the research and development and sales of smartphones, the Internet of Things (IoT) and consumer products. The Company conducts its businesses primarily through four segments. The Smartphone segment is primarily engaged in the sales of smartphones. The IoT and lifestyle products segment primarily sells other in-house products (including smart TVs, laptops, artificial intelligence (AI) speakers and smart routers), ecological chain products (including IoT and other smart hardware products) and some consumer products. The Internet Services segment provides advertising services and Internet value-added services such as online games and fintech businesses. The Other segment provides hardware product repair services. The Company is also engaged in smart electric vehicles and other related businesses.

Upcoming Launch of YU7 SUV in July. Xiaomi has announced the upcoming launch of its highly anticipated YU7 SUV, set for official release in July. Static displays of the YU7 began on May 29 across 13 Xiaomi stores in Beijing, with a broader rollout to 92 cities nationwide throughout June. The company will also showcase the YU7—alongside its SU7 sedan and SU7 Ultra—at the 2025 Guangdong-Hong Kong-Macao Greater Bay Area Auto Show, taking place from May 31 to June 8 at the Shenzhen World Exhibition & Convention Centre. The YU7 aims to expand Xiaomi’s EV lineup and directly challenge competitors such as Tesla’s Model Y in China’s fast-evolving electric vehicle market.

Smartphone Leadership and Premiumization Strategy. In Q1 2025, Xiaomi reclaimed the No. 1 position in China’s smartphone market for the first time in a decade, with shipments rising to 13.3 million units—up from 9.5 million a year earlier—boosting market share from 14% to 19%. This growth was driven by strong synergies across Xiaomi’s smartphone, AIoT, and smart mobility ecosystems, along with support from national subsidy programs. Looking ahead, the company is intensifying its smartphone premiumization strategy, focusing on higher-margin mid- to high-end models over volume expansion. While broader market growth is expected to moderate, Xiaomi is positioning itself for long-term profitability through a refined product mix and continued innovation in AI and hardware integration.

Introduction of MiMo, Xiaomi’s First Open-Source LLM. Xiaomi has unveiled MiMo, its first open-source large language model (LLM), specifically designed for complex reasoning tasks. Despite its relatively compact 7-billion-parameter architecture, MiMo has outperformed significantly larger models—such as OpenAI’s o1-mini and Alibaba’s Qwen-32B-Preview—on key public benchmarks like AIME24-25 (math reasoning) and LiveCodeBench v5 (code generation). Developed by Xiaomi’s specialized AI division, Core, the model leverages advanced pretraining and post-training techniques to enhance its reasoning capabilities. The launch of MiMo marks a strategic move to embed generative AI more deeply across Xiaomi’s hardware ecosystem—including smartphones and its growing electric vehicle (EV) portfolio—potentially enabling more seamless user experiences and strengthening its competitive edge.

1Q25 earnings. Revenue increased by 47.4% YoY to RMB111.3bn in 1Q25, compared to RMB75.5bn in 1Q24. Net profit increased by 161.0% to RMB10.9bn in 1Q25, compared to RMB4.17bn in 1Q24. Basis EPS rose to RMB0.44 in 1Q25, compared to RMB0.17 in 1Q24.

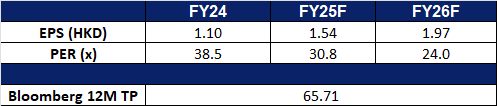

Market consensus.

(Source: Bloomberg)

Jiangxi Copper Co Ltd. (358 HK): Optimism in the economy

Jiangxi Copper Co Ltd is a China-based company mainly engaged in the mining, smelting and processing of copper and gold. The Company mainly conducts businesses through two segments. The Copper-related Industry segment is mainly engaged in the production and sales of copper and copper-related products. The Gold-related Industry segment is mainly engaged in the production and sales of gold and gold-related products. The Company’s products mainly include cathode copper, gold, silver, sulfuric acid, copper rods, copper tubes, copper foil, selenium, tellurium, rhenium and bismuth. The Company’s products are mainly used in electrical, electronic, light industry, machinery manufacturing, construction, transportation, military industry and other industries. The Company principally conducts its businesses in the domestic market.

Optimism towards tariff negotiations between US, Japan and EU. Tariff developments remain a key driver of market sentiment. This month, markets largely responded to the recent trade agreements reached between the U.S. and China, as well as between the U.S. and the U.K. The resolution of these negotiations has eased concerns that the broad tariffs announced in recent months would be implemented at their most severe levels, renewing optimism about the global economic outlook. Further reinforcing this sentiment, the European Union’s chief trade negotiator noted that “good calls” were held with Trump administration officials on Monday, as key trading partners advanced talks amidst the administration’s tariff-driven efforts to reshape global trade. This renewed confidence in economic growth is likely to support higher copper prices.

Copper demand is set to outpace supply over the long term. According to the International Energy Agency (IEA), copper demand, critical to the global transition to a low-carbon economy, is projected to exceed supply within the next decade. The IEA estimates that by 2035, copper supply could fall short by as much as 30% relative to demand. As a key component in virtually all electrical energy systems, this supply-demand imbalance is expected to put upward pressure on copper prices over the long term. Additionally, with China processing over 70% of the world’s top 20 energy transition minerals—including copper—producers such as Jiangxi Copper are well-positioned to benefit from rising demand and higher copper prices.

Copper Prices

(Source: Bloomberg)

More stake in SolGold and potential access to strategic assets. Earlier this year,Jiangxi Copper acquired about 157mn shares in SolGold. Following the investment, Jiangxi Copper, through its subsidiary Jiangxi Copper (Hong Kong) Investment Company Limited, would increase its holding in SolGold from 6.95% to 12.19% of the company’s total issued share capital.By increasing its stake in SolGold, Jiangxi Copper gains a larger ownership share and consequently, more influence over SolGold’s decisions. This is particularly important concerning the Cascabel project, a major copper/gold asset. This strategic increase in ownership aligns with JCC’s objective of securing access to vital copper resources.

FY24 earnings. Revenue fell by 8.90% YoY to RMB111.6bn in 1Q25, compared to RMB122.5bn in 1Q24. Net profit increased by 37.1% to RMB2.48bn in 1Q25, compared to RMB1.81bn in 1Q24. Basis EPS rose to RMB0.57 in 1Q25, compared to RMB0.50 in 1Q24.

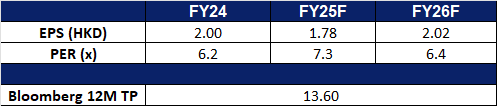

Market consensus.

(Source: Bloomberg)

Coinbase Global Inc (COIN US): A stroke of GENIUS

BUY Entry – 256 Target – 288 Stop Loss – 240

Coinbase Global, Inc. provides financial solutions. The Company offers platform to buy and sell cryptocurrencies. Coinbase Global serves clients worldwide.

GENIUS ACT helps expand stablecoin scale. The U.S. Senate recently passed the “Guidance and Establishment of American Stablecoin Innovation Act” (GENIUS ACT), which requires institutions issuing stablecoins to hold reserves on a 1:1 basis. The reserve assets include U.S. dollars, time deposits, short-term U.S. Treasury bonds, repurchase agreements, and other highly liquid assets. The current stablecoin market size has reached $232 billion, and with the implementation of this act, large financial institutions or companies are expected to enter the stablecoin market..

Rapid growth of stablecoin business. In the first quarter, Coinbase reported a record USDC market capitalization of $60 billion, with the average USDC balance on its platform growing 49% quarter-over-quarter to $12 billion. Revenue related to stablecoins increased 32% quarter-over-quarter to $298 million, driven by Coinbase’s strong partnership with Circle and its expanding stablecoin products, including B2B payment features targeted at startups and SMEs. As Coinbase prioritizes the adoption of USDC and expands its role in stablecoin payments, the company is expected to profit in this growing market, especially as enhanced regulation increases trust and usage of stablecoins. This accelerated adoption will directly translate to higher trading volumes and stable revenue sources, supporting a short-term rise in Coinbase’s stock price.

Results exceeded expectations. In the first quarter of FY25, revenue reached US$2.03bn, a 23.8% YoY increase, missing estimates by US$60mn. Non-GAAP earnings per share were US$1.94, missing estimates by US$0.04. First-quarter trading revenue was US$1.26bn, a 16.7% YoY increase; subscription and service revenue was US$698mn, a 36.6% YoY increase.

1Q25 results. Revenue rose 23.8% YoY to US$2.03bn, missing estimates by US$60mn. Non-GAAP earnings per share were US$1.94, missing estimates by US$0.04. For Q2, it expects subscription and services revenue to be between US$600mn and US$680mn, technology and development and general and administrative expenses to be in the range of US$700mn to US$750mn and sales and marketing to be in the range of US$215mn to US$315mn.

Nebius Group is a technology company providing infrastructure and services to AI builders globally. The group’s core business, Nebius, is an AI-centric cloud platform built for AI workloads. Nebius Group serves customers worldwide.

Strong market outlook for AI factories and infrastructure. Nvidia CEO Jensen Huang stated at Computex 2025 that AI data centers are essentially AI factories, and the market for AI factories and related infrastructure is expected to reach a trillion-dollar scale.

Expansion in Europe and the U.S. Nebius currently operates data center facilities in Finland and France, with a new site opening soon in Iceland. The company plans to invest $1 billion in Europe and recently launched an Nvidia H200 GPU cluster in Paris. It also plans to triple its computing capacity in Finland, potentially scaling to 60,000 GPUs—this alone could generate up to $1 billion in revenue at full capacity. Nebius has just opened a data center in Kansas City and plans to build a hyperscale facility in New Jersey with a projected power capacity of up to 300 megawatts. For fiscal year 2024, the company reported $117.5 million in revenue and expects that to grow to between $750 million and $1 billion in fiscal year 2025.

Outperformance. In Q1 of fiscal 2025, revenue surged 385% YoY to US$55.3mn, with an adjusted net loss of US$92.5mn. The company’s AI infrastructure platform, which offers full-stack solutions to AI firms, reached an annual recurring revenue (ARR) of US$249mn in March, driven by expanded computing capacity and strong sales execution. CEO Arkady Volozh reaffirmed in a shareholder letter that the company remains on track to achieve US$750mn to US$1bn in ARR by year-end. Full-year revenue guidance remains between US$500mn and US$700mn. Adjusted EBITDA is expected to turn positive in the second half of 2025, although the full-year EBITDA will remain negative.

1Q25 results. Revenue rose 385.1% YoY to US$55.3mn and an adjusted net loss of US$92.5mn.