KGI DAILY TRADING IDEAS – 3 May 2021

IPO WATCH

The Honest Company (HNST US): Will celebrity IPOs storm up the market, or stay invisible?

- HNST is a household products company targeted at ethical consumerism, marketing their products as safe, eco-friendly and affordable. HNST currently generates the bulk of their sales from childcare products such as diapers and baby wipes, followed by other personal care and household products.

- HNST’s journey to the public market was a tumultuous one, and we recommend reading this blogpost for further understanding on HNST’s background, where the company was valued at US$1.7bn at its peak before a series of setbacks.

- HNST boasts a unique growth profile, with 28% sales gain in 2020 despite the pandemic through strong marketing reach amongst Gen Z.

- Initial IPO price of US$14-17 is 5.2x Price/Sales at the midpoint at a market cap of around US$1.6bn. While we see potential for a 100% gain given that Lululemon and Farfetch trades at 10x P/S, HNST currently lacks the brand strength of Lululemon and the growth numbers of Farfetch to justify the valuation. We thus see 5-6x P/S as fairly priced.

UNITED STATES

The Trade Desk Inc (TTD US): Ad spending is back

- BUY Entry – 720 Target – 870 Stop Loss – 652

- TTD is a high-growth ad-tech company, boasting over 40% sales growth, no long-term debt, a high customer retention rate of over 95% and substantial profitability at 29% net profit margin.

- We see the recent downtrend to be caused by Apple and Alphabet increasing user control over ad personalization. However, TTD has been working around the issue of internet cookies and individual identity protection with its Unified ID Solution 2.0.

- With ad spending back in 2021, we see strong potential for a results beat for TTD, not dissimilar to Facebook and Alphabet. We set entry at the 20 EMA.

Atlassian Corporation (TEAM US): At the top of a wedge

- BUY Entry – 207.5 Target – 236 Stop Loss – 198.5

- TEAM is an enterprise software company with over 51,000 customers, offering project management, issue tracking, integration, deployment and support services, helping both developer and non-developer teams collaborate for software innovation.

- During Fiscal 3Q results, the company beat sales and earnings estimates by 7% and 76% respectively, and guided for a fairly strong Fiscal 4Q.

- TEAM is currently trading at the high end of a wedge. We recommend accumulation at the lower end if the stock pulls back.

SINGAPORE

Uni-Asia Group (UAG SP): Opportunities in the high seas

- BUY Entry – 0.65 Target – 0.80 Stop Loss – 0.58

- UAG is an alternative investment company which owns and manages bulk carriers, invests in Hong Kong commercial offices and develops residential properties in Japan.

- The group derives around 65% of its revenues from charter income generated by its fleet of bulk carriers, and the remainder of revenue is from its property projects in HK and Japan. While its shipping business performed poorly in FY2020 due to poor charter rates and impairments, it is turning around in FY2021.

- The Baltic Dry Index (BDI) has finally crossed the elusive 3,000 point mark, the highest in more than 10 years. The surge in the main sea freight index comes amid strong demand across all vessel segments. Order book for bulk carriers is at a record low of 6% of fleet capacity, while demand side is driven by increase in Chinese dry bulk imports from the Atlantic and also fueled by port congestion.

- The company will be going ex-div on 19 May 2021, and will be paying out a S$0.01 dividend.

Baltic Dry Index Handysize Index (2010-2021 YTD)

Keppel Corp (KEP SP): Healthy start to the year

- BUY Entry – 5.35 Target – 6.00 Stop Loss – 5.05

- KEP operates four key business segments, with urban development (commercial and residential property development) its largest earnings contributor. Its other businesses include Energy & Environment (Offshore & Marine, Keppel Infrastructure), Connectivity (Keppel Data Centres, M1, Keppel Logistics) and Asset Management (Keppel Capital, REITs & Trust, Private Funds).

- The company is off to a positive start as it posted a higher YoY growth in both top line and net profit. In its business update last week, management remains upbeat for the year ahead despite the challenging macro environment.

- Keppel Offshore & Marine (KOM) finally returned to positive EBITDA due to improving margins as it continues its organic transformation. Property development continued its positive momentum, with new home sales in 1Q2021 tripling YoY to 1,360 units, underpinned by strong performance in China, Vietnam and Singapore.

- Overall street consensus is positive, with 11 BUYS, 2 HOLDS, 2 SELLS and an overall 12-month target price of S$6.23. Dividend yield is forecasted to improve to 3% in FY2021, 4% in FY2022 and FY2023.

HONG KONG

Aluminum Corporation of China Limited (2600 HK): Another metal play in the upward cycle

- Buy Entry – 3.8 Target – 4.8 Stop Loss – 3.4

- Aluminum Corporation of China Limited (Chalco) is an aluminum producer with operations in bauxite and coal mining, alumina refining and primary aluminum smelting. The company operates through alumina segment, including the mining and purchasing of bauxite and other raw materials, and production and sale of alumina, as well as alumina-related products; primary aluminum segment includes the procurement of alumina, other raw materials, supplemental materials and electricity power, the production and sale of primary aluminum and aluminum-related products; trading segment is engaged in the trading of alumina, primary aluminum, other non-ferrous metal products, and crude fuels; energy segment includes coal mining and power generation, including conventional coal-fired power generation and renewable energy generation, such as wind power and photovoltaic power, and corporate and other operating segment includes corporate and other aluminum-related research, development, and other activities.

- The company announced 1Q21 results last week. Revenue grew by 32.55% YoY to RMB52.6bn. Net profit attributable to the company’s shareholders grew by 3025.7% YoY to RMB967mn.

- Shanghai aluminium futures price has surpassed the highs in 2011 and is back to the high in 2008.

- The stock has relatively high aluminium beta (regression against aluminium futures). The market estimates of aluminium prices range averages at US$2,400/tonne. Based on the regression model and the average estimate, the implied stock price is HK$4.8.

- Market consensus of net profit growth in FY21 and FY22 are 584.9% YoY and 28% YoY, which implies forward PERs of 20.2x and 17.4x. Current PER is 44.5x. Bloomberg consensus average 12-month target price is HK$4.53.

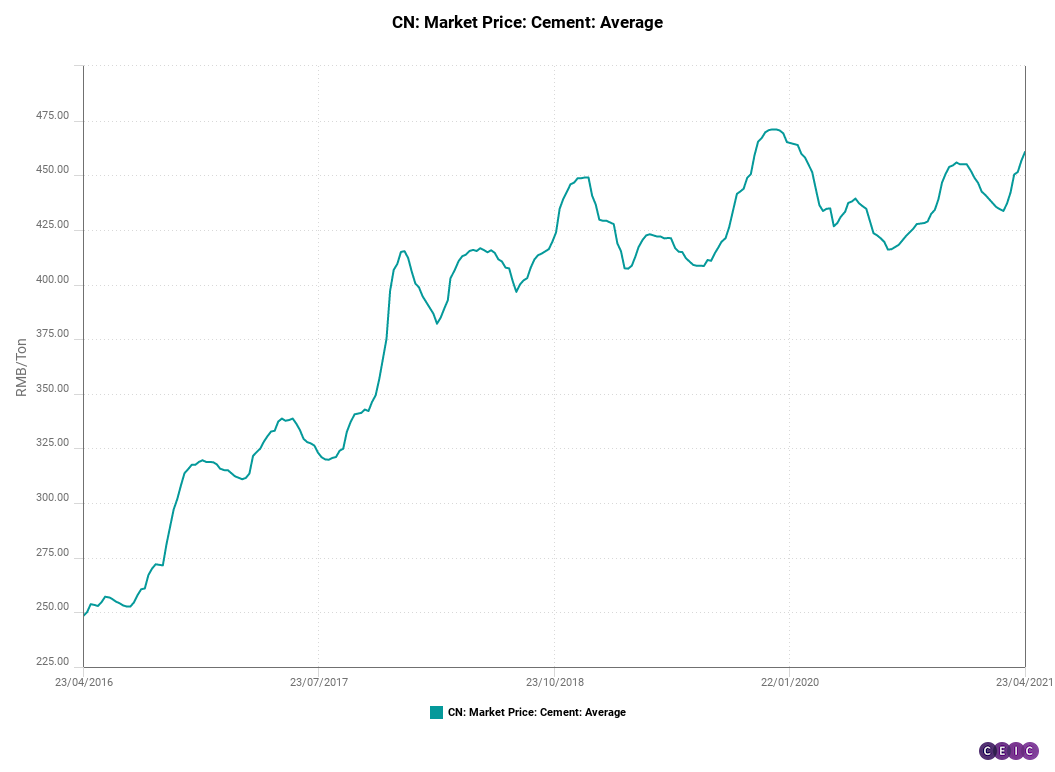

China Resources Cement Holdings Limited (1313 HK): Boring but offering a 7.4% dividend yield

- Buy Entry – 8.45 Target – 9.5 Stop Loss – 7.9

- China Resources Cement Holdings Limited is a Hong Kong-based investment holding company principally engaged in the cement and concrete businesses. The company operates through two business segments. The cement segment is engaged in the manufacture and sales of cement and related products. The Concrete segment is engaged in the manufacture and sales of concrete and related products. The Company is also involved in the trading of fly ash, mortars and shotcrete, as well as the property holding business through its subsidiaries.

- Previously, the company announced 1Q21 results. Revenue grew by 52.1% YoY to HK$8.5bn. GPM dropped to 28.4% compared to 39.2% during the same period last year. Net profit attributable to the company’s shareholders grew by 15.8% YoY to HK$1.3bn.

- This is another value stock in the cement sector. Its current PER is 6.47x and FY21F dividend yield is 7.4%.

- Updated market consensus of the estimated growth of net profit in FY21 and FY22 are 2.6% and 2.3% respectively, which translates to 6.4x and 6.3x forward PE. The current PE is 6.5x. The estimated respective dividend yield in FY21 and FY22 is around 7.4% to 7.6%. Bloomberg consensus average 12-month target price is HK$10.54.

Market Movers

United States

- Twitter’s (TWTR US) daily loss extended from 12% pre-market to 15% during Friday’s trading after missing user growth estimates mildly in 1Q21 and guiding for sales forecast below analyst averages in the next quarter.

- Domino’s Pizza (DPZ US) rallied 6% for the week above the US$400 mark after announcing 1Q21 results, with US same store sales growth (SSSG) of 13.4% vs expectations of 9.7%, while international SSSG was 11.8% vs 6.0% consensus.

- Nucor (NUE US) closed at a record high as steel futures continue climbing and forming new record highs. At 1Q21 results 2 weeks ago, management guided for 2Q21 to set “a new record for quarterly earnings.”

- Aon Plc (AON US) climbed to a record high share price after 1Q21 results beat analyst estimates. The company expects to grow revenue in the mid-single digits this year, and hopes to finish their mega-merger with Willis Towers Watson by 1H21 after obtaining the relevant regulatory approvals.

- Vaxart (VXRT US) almost doubled for the week after announcing plans to host a webinar this Monday that will include progress updates on their vaccine candidate, which is an oral tablet to combat COVID-19. Vaxart also released a study 2 weeks prior that indicated almost 19 million more American adults will take the COVID-19 vaccine if it is by pill form rather than by needle.

- Trading Dashboard: Take profit on Aptiv at US$143.89. Include Green Brick Partners at US$25.9.

Earnings Watch: Berkshire Hathaway posted earnings over the weekend. Others worth watching include Estee Lauder, On Semiconductor, and Transocean.

Singapore

- Raffles Education Corp (RLS SP). Earlier last week, Oei Hong Leong and his firm Hong Leong Art Museum, who are the second largest shareholder with a 10% take in Raffles Education, requested to convene an EGM to remove founder Chew Hua Seng from his official appointments in the company.

- Hanwell (HANW SP). Sam Goi, who has a 23% stake in the company, has won board control after ousting two other directors. Sam Goi told The Business Times that he believes the company has a strong set of brand assets and the potential to expand the scale of its business and to grow regionally.

- DBS (DBS SP). Shares of DBS rose to its highest level since May 2018 after a strong 1Q2021 performance, and now trading near its all-time high of S$30.84. The bank’s latest quarterly earnings beat analysts estimates, surging 72% YoY to S$2bn. The latest results mark the first time in the bank’s history that its quarterly net profit crossed the S$2bn level. DBS declared an interim dividend of 18 Sing cents.

- Nanofilm Technologies (NANO SP). Shares of NANO are under selling pressure and are now trading close to the 50-day moving average after the company said that it could defer selected projects due to the global chip shortage. The company noted that the global semiconductor market has “experienced significant tightening in Q1 due to the continued strong demand for semiconductors across multiple industries”. Bloomberg Consensus still has 6 BUYS and an average 12-month TP of S$5.84.

- Yangzijiang (YZJSGDP SP). Shares declined on broad-based market weakness and profit taking after the company announced an 89% YoY jump in 1Q2021 net profit. Yanyzijiang’s shares have gained 50% year-to-date, outperforming the main STI index, after it secured around S$4bn worth of new orders. The strong order wins so far this year is on pace to surpass its previous record order win of S$5bn set in the last shipbuilding supercycle in 2007.

Hong Kong

- Shanghai Fosun Pharmaceutical (Group) Co., Ltd. (2196 HK) shares were trading higher and closed at a 52-week high. Investors continued to trade up on the COVID-19 vaccine sentiment. Credit Suisse raised the TP to HK$52 from HK$44 and maintained an OVERWEIGHT rating.

- Jinke Smart Services Group Co Ltd (9666 HK). The property management sector was holding up well. The stock caught up with peers who rallied over the past few days.

- Fosun Tourism Group (1992 HK) share prices corrected as investors took profit before the golden week of Labour Day holiday in China.

- Yanzhou Coal Mining Company Limited (1171 HK). Even though Shanghai thermal coal futures continued to break new highs, shares were sold off. The company announced 1Q21 results. Revenue dropped by 35.3% YoY to RMB31bn. Net profit attributable to the company’s shareholders grew by 30.2% YoY to RMB2.3bn. Coal production volume dropped by 6.6% YoY to 26.3mn tonnes; Chemical production volume grew by 44.6% YoY to1.5mn tonnes; Electricity generation volume dropped by 42% YoY to 1,874 GWh.

- Xinte Energy Co Ltd (1799 HK). The company announced 1Q21 results. Revenue grew by 113.1% YoY to RMB2.9bn. Net profit attributable to the company’s shareholders grew by 376.8% YoY to RMB242mn. The company announced it would issue no more than 177.3mn domestic shares to fund the 100,000 tonnes polysilicon project. The public float of H-shares will be diluted to 22.67% from 26.02%.

TRADING DASHBOARD

Related Posts: