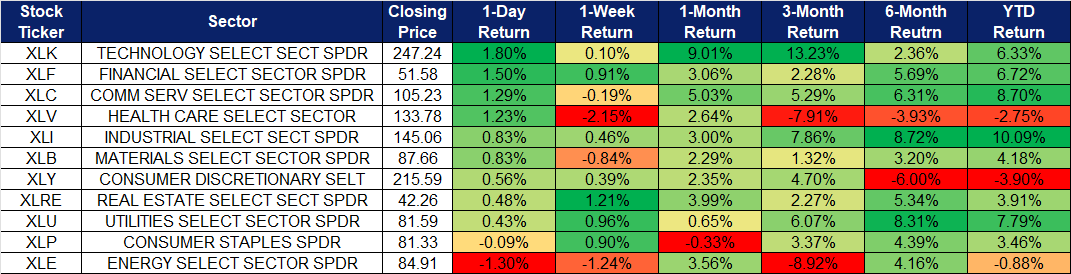

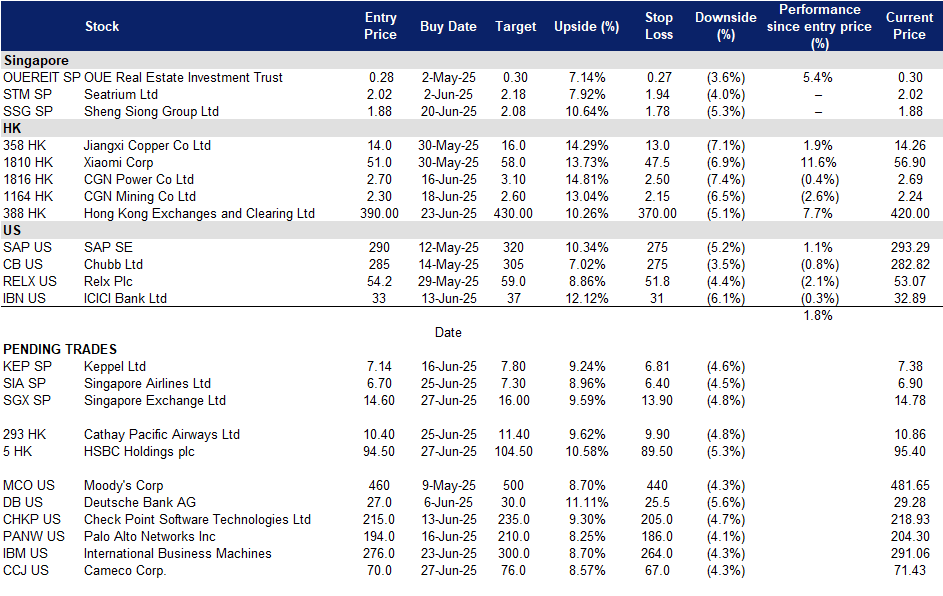

Singapore Exchange Ltd (SGX SP): Improving trading volume and fee income potential

BUY Entry – 14.6 Target– 16.0 Stop Loss – 13.9

Singapore Exchange Limited owns and operates Singapore’s Securities and derivatives exchange and their related clearing houses. The Company also provides ancillary securities processing and information technology services to participants in the financial sector.

Growing SDR market. The Singapore Exchange (SGX) is seeing strong growth in its Singapore Depository Receipts (SDR) platform, which simplifies access to foreign-listed blue-chip stocks by allowing local investors to trade them in Singapore dollars. With six new SDRs added on 23 June, three from Hong Kong and three from Thailand, the total shelf now covers 21 securities, representing about 50% of the Hang Seng Index and SET50 by weight. Retail interest has surged, with daily turnover hitting a record S$5.4mn in May and total assets under management surpassing S$100mn, over 60% of which is held by more than 7,000 retail investors. The low entry cost and ease of access continue to drive adoption, positioning SGX to benefit from increased trading activity, custody fees and platform engagement, especially among the retail segment. The SDR initiative strengthens SGX’s strategic positioning and enables it to diversify its revenue streams in a scalable way.

Supportive government policies driving growth. The Singapore government, through the Monetary Authority of Singapore (MAS), introduced a series of initiatives to enhance the attractiveness and competitiveness of the local stock market. These include the $5bn Equity Market Development Programme (EQDP), which will partner with fund managers to invest in Singapore equities and streamlined regulations to make the listing process more efficient. Additionally, tax incentives and expanded research grants under the Grant for Equity Market Singapore (GEMS) aim to attract quality IPOs and boost liquidity. These comprehensive measures, coupled with a focus on fostering innovation and sustainability sectors, position the Singapore Exchange as a prime destination for both retail and institutional investors, fostering long-term growth and resilience.

Safe-haven for investors. The weakening of the USD, coupled with tensions in the middle east and global trade uncertainty, has triggered capital inflow to emerging markets like Singapore.Positioned as a safe-haven financial hub, Singapore offers a unique combination of high dividend yields, economic resilience, and a robust regulatory framework. Its ability to weather global economic instability makes the Singapore Exchange a sweet spot for investors looking for stability and capital preservation amidst current market volatility.

1H25 results review. Singapore Exchange Ltd reported 1H25 revenue of S$682.2mn a 15.2% increase from S$592.2mn in the previous period. Its net profit of S$340mn for 1H25, a 20.7% incline YoY, compared to S$281.6mn in 1H24. Earnings per share (EPS) stood at S$0.318, up from S$0.263 in the year-ago period. Due to the Group’s strong performance, the Board of Directors declared an interim quarterly dividend of S$0.09 per share, up from the S$0.085-per-share payout in the previous corresponding period, bringing total dividends for 1H25 to S$0.18 per share.

Singapore Airlines Limited provides air transportation, engineering, pilot training, air charter, and tour wholesaling services. The Company’s airline operation covers Asia, Europe, the Americas, South West Pacific, and Africa.

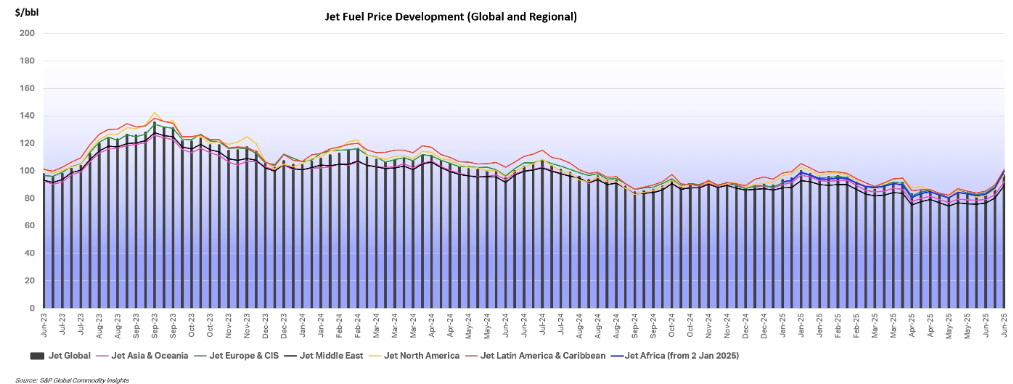

Jet fuel prices expected to gradually decline. Recent tensions between Israel and Iran have pushed jet fuel prices to their highest levels in 15 months. However, this spike is expected to ease as geopolitical risks subside. Saudi Arabia and the United Arab Emirates can quickly ramp up production, with a combined spare capacity of approximately 3.5 million barrels per day (bpd), which could offset any temporary supply disruptions from Iran, which currently produces around 3.3 million bpd and exports over 2 million bpd. According to the International Air Transport Association (IATA), the average jet fuel price in 2025 is projected at US$86 per barrel, with total airline fuel expenditures expected to fall to US$236 billion—nearly 9% lower than in 2024. While short-term price fluctuations may occur due to geopolitical or refinery disruptions, overall fuel price stability is anticipated, with minimal impact from ongoing trade tensions. Fuel costs are forecast to account for 25.8% of total airline operating expenses, supporting improved airline profitability. As of the week ending June 20, 2025, the global average jet fuel price stood at US$96.97 per barrel, up 12.9% from the previous week.

Record US$1 trillion in 2025 airline revenue. According to the IATA, in 2025, global airline revenues are projected to reach a record US$979 billion, with net profits improving to US$36 billion, despite falling short of earlier forecasts due to US tariffs, trade tensions, and softer-than-expected growth in passenger and cargo volumes. The Asia-Pacific region is expected to lead industry expansion, driven by economic growth and eased visa policies, contributing over half of global air travel growth. Lower jet fuel prices will support airline profitability by reducing operating costs, though supply chain disruptions, aircraft delivery delays, and ongoing engine and parts shortages continue to constrain capacity. While the industry remains on a positive trajectory with stable margins, structural challenges such as thin profitability, geopolitical risks, and the slow progress in scaling sustainable aviation fuel production present headwinds to long-term growth.

Seasonality chart – SIA

(Source: Bloomberg)

Seasonal rise in travel. In the first five months of 2025, Singapore attracted over seven million international tourists, driven by strong demand from China, Indonesia, and India. With the ongoing summer holidays, both inbound and outbound travel demand is anticipated to rise. This seasonal uptick in travel is likely to benefit Singapore Airlines by increasing passenger traffic, contributing to higher flight bookings and demand for its services during peak travel periods. The airline is well-positioned to capitalize on this increased travel activity, boosting its revenue and enhancing its global connectivity.

FY24 results review. Revenue increased 2.8% YoY to S$19.5bn, driven by resilient demand for air travel and cargo uplift during the year. It delivered record S$2.8bn in net profit, boosted by the one-off non-cash accounting gain of S$1.1bn from the Air India-Vistara merger. Proposed final dividend of S$0.30 per share for FY2024/25, resulting in a total dividend of S$0.40 per share for the year.

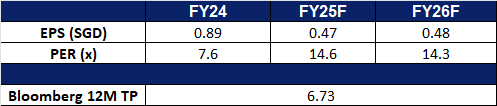

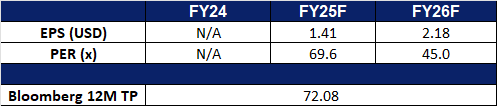

Market consensus

(Source: Bloomberg)

HSBC Holdings Plc. (5 HK): Digital asset to increase fund flow

BUY Entry – 94.5 Target – 104.5Stop Loss – 89.5

HSBC Holdings plc (HSBC) is a banking and financial services company. Its business segments include Hong Kong, UK, Corporate and Institutional Banking (CIB), and International Wealth and Premier Banking (IWPB). Its Hong Kong business comprises retail banking and wealth and commercial banking of HSBC Hong Kong and Hang Seng Bank. Its UK business comprises UK retail banking and wealth (including first direct and M&S Bank) and UK commercial banking, including HSBC Innovation Bank. The CIB segment is formed from the integration of its commercial banking business (outside the UK and Hong Kong) with its global banking and markets business. The IWPB segment comprises premier banking outside of Hong Kong and the UK, its global private bank, and its asset management, insurance and investment distribution businesses. Its customers worldwide through a network covering 58 countries and territories. Its customers range from individual savers and investors to companies, governments and others.

Hong Kong’s Push to Become a Global Digital Asset Hub to Attract Fund Inflows. The Hong Kong government has recently released Policy Statement 2.0 on the Development of Digital Assets in Hong Kong, reaffirming its commitment to positioning the city as a global hub for digital asset (DA) innovation. The updated policy outlines a clear vision for building a trusted and forward-looking DA ecosystem that emphasizes risk management and investor protection, while supporting the growth of the real economy and financial markets. With greater regulatory clarity and confidence in the digital asset space, this initiative is expected to attract increased investor interest and capital inflows into Hong Kong—potentially boosting assets under management (AUM) for institutions like HSBC.

Expertise in Tokenization Supports Strategic Advantage. As part of its digital asset roadmap, the Hong Kong government plans to institutionalize the issuance of tokenized government bonds and promote the tokenization of real-world assets (RWAs) to improve liquidity and accessibility. Initiatives include clarifying stamp duty treatment for tokenized exchange-traded funds (ETFs) and supporting secondary market trading of these ETFs on licensed digital asset platforms or through alternative channels. The government also aims to broaden tokenization across various asset classes, such as precious and non-ferrous metals, and renewable energy instruments. HSBC, with its established track record in digital asset innovation—including initiatives like the HSBC Gold Token and tokenized deposits—is well-positioned to support this transformation. The bank can leverage its infrastructure, advisory capabilities, and custodial services to facilitate the adoption and growth of tokenized financial instruments in Hong Kong.

Strategic Restructuring to Drive Efficiency and Focus. In a move to streamline its investment banking operations, HSBC recently laid off more than two dozen analysts as part of a broader restructuring initiative. As part of these changes, the bank is consolidating its macro strategy functions across asset classes, including foreign exchange and fixed income, to create a more integrated and efficient approach. This latest restructuring effort reflects CEO Georges Elhedery’s ongoing push to enhance operational efficiency and sharpen strategic focus. Additionally, HSBC has merged its capital markets and corporate advisory teams into a newly formed unit aimed at capitalizing on opportunities in the rapidly growing private credit market. These structural changes are expected to strengthen the bank’s competitive positioning and deliver long-term value.

FY24 results review. 1Q25 revenue fell by 15.0% to US$17.6bn, compared to US$20.8bn in 1Q24. Profit after tax was US$7.57bn in 1Q25, down 30.1% YoY, compared to US$10.8bn in 1Q24. Basic EPS fell to US$0.39 in 1Q25 from US$0.54 the same period last year.

Cathay Pacific Airways Ltd is a company mainly engaged in the provision of international passenger and cargo air transportation. Together with its subsidiaries, the Company operates business through its four operating segments. The Cathay Pacific and Cathay Dragon segment provides full service international passenger and cargo air transportation under the Cathay Pacific and Cathay Dragon brands. The Air Hong Kong segment provides express cargo air transportation offering scheduled services within Asia. The HK Express segment provides a low-cost passenger air transportation offering scheduled services within Asia. The Airline Services segment provides supporting airline operations services include catering, cargo terminal operations, ground handling services and commercial laundry operations.

Lowered crude oil prices. Brent crude oil futures fell over 1% to around $69 per barrel on Tuesday, hitting a more than one-week low, following news of a ceasefire between Israel and Iran. The Israeli government confirmed the agreement early Tuesday, with Iranian state media later reporting Tehran’s acceptance, raising hopes for an end to the 12-day conflict. The truce eased fears of potential supply disruptions in the Middle East, particularly concerns over a possible blockade of the Strait of Hormuz, a key passage for about 20% of global oil flows. The resulting decline in crude prices is expected to benefit airlines, for whom jet fuel represents a significant portion of operating costs.

Brent Crude Oil Price

(Source: Bloomberg)

China’s summer holidays.Chinese airlines are stepping up efforts to expand their international networks ahead of the upcoming summer travel season, driven by strong demand, particularly to destinations along the Belt and Road Initiative (BRI), which are emerging as key markets for Chinese carriers. According to data from travel industry platform Umetrip, as of June 16, inbound and outbound flight bookings for July 1–31 surpassed 3.8mn, marking an 8% increase YoY. Cathay Pacific, recently ranked among the world’s top three airlines in the 2025 Skytrax World Airline Awards, reported a 36.1% YoY increase in passengers for May 2025, with available seat kilometres up 31.2%. For the first five months of the year, passenger volume rose by 28.4% compared with the same period in 2024. With strong forward bookings and rising travel momentum, the upcoming summer holidays are expected to bring further growth in travel demand, likely benefiting Cathay Pacific’s operational and financial performance.

More flights to cater to growing demand. Cathay Pacific has announced it will introduce double daily flights between Hong Kong and Perth, adding more than 43,000 extra inbound seats to Western Australia annually. This expanded service is supported by the Western Australian Government, through Tourism WA, in collaboration with Perth Airport. With this addition, Cathay Pacific’s total annual seat capacity into WA will exceed 200,000. This marks the second increase in flight frequency to Perth within a year, reflecting strong and growing demand for Western Australia among travellers from China and Hong Kong (Greater China). As a major global transit hub, Hong Kong also facilitates broader connectivity, and the increased frequency will enhance one-stop travel options for key visitor markets such as the United Kingdom, the United States, and Japan. The expansion is expected to contribute positively to Cathay Pacific’s top-line growth in the long term.

FY24 results review. FY24 revenue rose by 10.5% to HK$104.4bn, compared to HK$94.5bn in FY23. Profit attributable to shareholders was HK$9.89bn in FY24, up 1.0% YoY, compared to HK$9.79bn in FY23. Basic EPS increased to HK$1.49 in FY24 from HK$1.41 the same period last year.

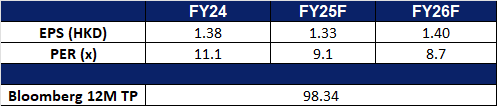

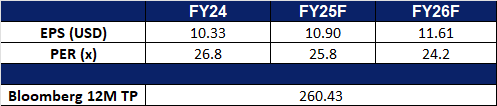

Market consensus.

(Source: Bloomberg)

Cameco Corp. (CCJ US): Long-term tailwinds for nuclear power and uranium supply

BUY Entry – 70 Target – 76 Stop Loss – 67

Cameco Corporation explores, develops, mines, refines, converts, and fabricates uranium. The Company offers uranium for sale as fuel for generating electricity in nuclear power reactors. Cameco operates worldwide.

Surging U.S. electricity demand. U.S. electricity consumption is projected to hit all-time highs in 2025 and 2026, driven by explosive demand from AI and crypto-powered data centers, as well as rising residential, commercial and industrial usage, according to the U.S. Energy Information Administration (EIA). With fossil fuels facing regulatory headwinds and renewables limited by intermittency, nuclear energy remains the only scalable, zero-emission baseload option. As the grid grows increasingly power-hungry, utilities will require long-term uranium supply to maintain reliability. This structural demand shift toward power generation and uranium production in the U.S. will benefit Cameco Corp.

Rising international demand for nuclear. As the global nuclear energy boom accelerates, Cameco is positioned to benefit not just from uranium production, but also from the international commercialization of advanced reactor technology through its 49% stake in Westinghouse. As countries reduce dependence on Russian and Chinese nuclear technology, demand is shifting to Western suppliers. Recent deals, including a Czech AP1000-based reactor project is expected to add US$170mn in Q2 adjusted EBITDA, highlight the earnings power of Cameco’s international exposure. Additional agreements, such as with Finland’s Fortum Corporation, further support long-term value creation. As global demand for clean, secure energy grows and more nations invest in long-term nuclear infrastructure, Cameco stands to realize value across both fuel supply and reactor technology, reinforcing its position in the nuclear value chain.

Renewed U.S. commitment to nuclear development. The announcement of a new 1GW nuclear plant in New York, the first in over 15 years, marks a turning point in U.S. energy policy, reinforcing recognition of nuclear’s role in grid stability and decarbonization. Federal actions to streamline nuclear permitting, paired with soaring private sector interest from technological giants like Microsoft, Amazon and Google, signal a multi-decade nuclear buildout. Cameco stands to benefit directly through rising uranium demand, backed by its strategic exposure across the fuel cycle and its ownership in Westinghouse.

Uranium price upside and supply leverage. Uranium prices have climbed to approximately US$78.5/lb, driven by resurgent demand, policy support and constrained supply. The Sprott Physical Uranium Trust’s recent US$200mn purchase, U.S. efforts to restore domestic enrichment capacity and ongoing supply shortfalls from Kazatomprom underscore a tightening market. Cameco is positioned to capture pricing upside and deliver earnings leverage as the uranium cycle strengthens.

Uranium Spot Price

(Source: Bloomberg)

1Q25 results. Revenue grew 24.4% to US$789mn. Non-GAAP earnings per share were US$0.16. For FY25, Cameco Corp plans to produce 18mn pounds (100% basis) at each of Cigar Lake and McArthur River/Key Lake, and 13mn to 14mn kgU in its fuel services segment, as well as continued work to extend the mine life at Cigar Lake. It now expects adjusted EBITDA from its equity investment in Westinghouse to increase by approximately US$170mn. Over the next five years, it expects adjusted EBITDA to grow at a compound annual growth rate of 6% to 10%.

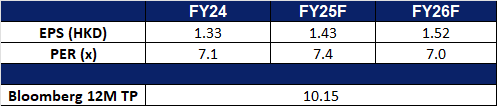

Market consensus

(Source: Bloomberg)

International Business Machines (IBM US): Capitalizing on mainframe expansion and quantum computing

International Business Machines is a global technology company focused on software, cloud services, artificial intelligence, and consulting services.

Steady growth in the global mainframe market. The global mainframe market is driven by the increasing demand for high-performance computing and robust data processing and cybersecurity solutions. It is expected to grow from $3.5 billion in 2024 to $6.8 billion by 2033, with a compound annual growth rate of 8.4%. IBM’s Z series mainframes hold a significant market share and maintain leadership in the mainframe market. The newly launched z17 mainframe is designed to meet the high computational demands of generative AI and the security needs of critical workloads for large enterprises, particularly in the financial services sector. As global demand for high-performance and highly secure infrastructure continues to rise, the company has strong growth momentum in this area.

Investment in quantum computing. Since the end of last year, quantum computing has gained market attention and is seen as another major technological revolution outside of artificial intelligence, with related company stocks soaring. IBM is actively developing quantum computing, planning to invest $30 billion over the next five years in research and development of quantum computing and mainframe technology, as part of its commitment to a total investment plan of $150 billion in the U.S. The company aims to launch practical quantum computers by 2029 and achieve a more advanced “Starling” system with approximately 200 logical qubits by 2033.

Business less affected by geopolitical risks. The company’s global operations cover both software and hardware, as well as consulting services, providing a higher level of risk resilience. Its core businesses, such as mainframe manufacturing and cloud services, have strong demand, resulting in relatively stable revenue growth during volatile economic cycles.

1Q25 results. Revenue grew 0.6% to US$14.54bn, exceeding expectations by US$150mn. Non-GAAP earnings per share were US$1.60, surpassing estimates by US$0.17. The company expects full-year revenue growth of 5% (fixed rate).