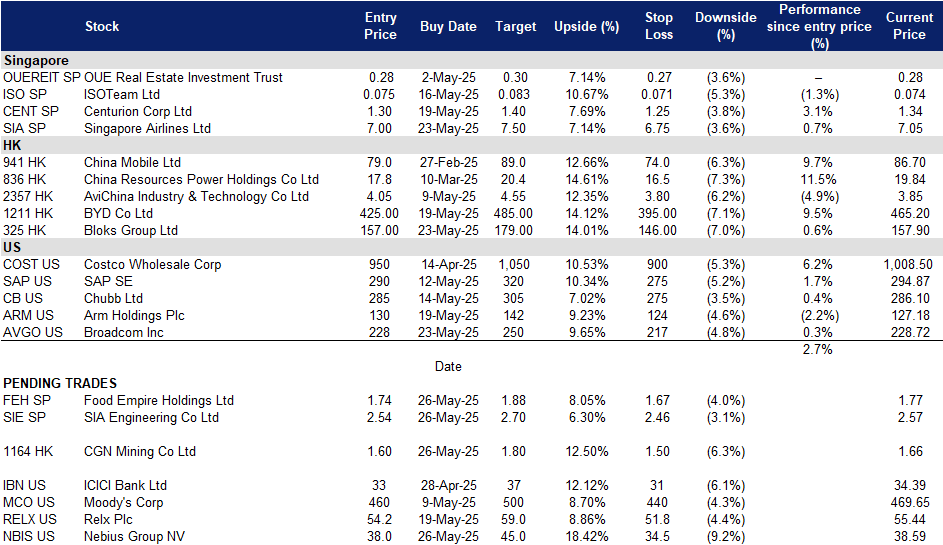

Food Empire Holdings Ltd (FEH SP): Brewing a growth recipe in Asia

BUY Entry – 1.74 Target – 1.88 Stop Loss – 1.67

Food Empire Holdings Limited operates as a food and beverage manufacturing and distribution company. The Company offers beverages and snacks including classic and flavoured coffee mixes and cappuccinos, chocolate drinks, fruit-flavoured and bubble teas, cereal blends, and crispy potato snacks. Food Empire Holdings serves customers worldwide.

Continued strong growth in Asia. Food Empire experienced a sustained increase in sales across its core markets in 1Q24, showcasing continued strong consumer demand for the company’s products, especially in the Southeast Asia and South Asia regions, which continued to see growth of over 30% in 1Q25. The group continues to reap the benefits of its brand-building efforts in Vietnam, increasing its market share across the Vietnamese market, with revenue growing 44.6% YoY. This has significantly boosted Food Empire’s Southeast Asia revenue contribution, taking the top spot and contributing to 29.2% of the group’s total sales in 1Q25. Demand for the group’s products in South Asia also remains strong amidst a coffee consumption boom in the region.

Expanding production capabilities across Asia. Food Empire is significantly expanding its production capabilities across Asia to meet growing demand. In Vietnam, a new freeze-dried soluble coffee facility is set to begin construction by late 2025 and become operational by 2028, bolstering its ingredients business. Meanwhile, its Malaysian snack manufacturing facility will increase output by about 50% by the third quarter of 2025 after an expansion is completed in the first half. Outside Southeast Asia, Food Empire’s first coffee-mix plant in Kazakhstan is expected to be finished by the end of 2025, boosting overall coffee-mix capacity by approximately 15% and extending its reach into Central Asia. These strategic expansions are set to drive continued top-line growth across its key Asian markets.

Capturing market growth and demand in Vietnam. Vietnam remains a strategic growth focus for Food Empire, underpinned by its position as the company’s fastest-growing market. In 1Q25, Vietnam’s GDP expanded by 6.93% YoY, marking the highest first-quarter growth since 2020 despite a quarter-on-quarter slowdown. The World Bank forecasts 5.8% GDP growth for 2025, while the Vietnamese Parliament maintains a more optimistic target of 8%. This strong economic outlook bodes well for Food Empire’s continued expansion in the country. The Group’s investments in marketing, consumer engagement, and production capacity are expected to reinforce its brand presence and position it to capture long-term growth opportunities in Vietnam’s rapidly developing economy.

1Q25 Business Updates. Food Empire Holdings reported higher revenue of US$136.6mn for 1Q25, up 16.3% YoY, compared to US$117.5mn in 1Q24, led by strong growth in its Southeast Asia and South Asia markets, which saw a growth of 33.8% and 31.7% respectively. The company’s markets in Ukraine, Kazakhstan and CIS experienced growth of 14.6% YoY, while the Russian market saw a slight increase in revenue of 0.5% YoY. The company experienced revenue growth across all key markets, demonstrating robust consumer demand despite increased prices due to higher raw material costs and ongoing global geopolitical tensions.

We have fundamental coverage with a BUY recommendation and a TP of S$1.95. Please read the full report here.

Market consensus

(Source: Bloomberg)

SIA Engineering Co Ltd (SIE SP): Continued strength in flight activities

BUY Entry – 2.54 Target– 2.70 Stop Loss – 2.46

SIA Engineering Co Ltd provides airframe and component overhaul services, line maintenance and technical ground handling services. The Company also manufactures aircraft cabin equipment, refurbishes aircraft galleys, repairs and overhauls hydromechanical aircraft equipment.

Flight recovery nearing pre-Covid levels. SIAEC reported that total flights handled by the company’s line maintenance business reached 97% of pre-COVID level at the end of FY24/25. Flights handled in the 4Q25 caught up to 99% of pre-COVID volume. Increased flight activities contributed to a higher demand for aircraft maintenance, repair, and overhaul (MRO) services. This uptrend is expected to continue as more airlines ramp up flight schedules, alongside the arrival of the summer travel season.

More upcoming revenue sources. The company recently incorporated TIA Engineering Services Co. Ltd to provide line maintenance services at Cambodia’s new Techo International Airport. Operations are currently expected to commence in July 2025, extending the company’s line maintenance network to 36 airports in 9 countries. Operations at the group’s Base Maintenance Malaysia Sdn. Bhd. (BMM), a wholly owned subsidiary under SIAEC, are also expected to begin in 2H25, with one hangar operational in 2H25, and another in 1H26. These activities are likely to positively contribute to the company’s topline.

Ongoing flight recovery. Flight activities in Singapore have continued to show improvement since 2022, with commercial aircraft movements in Changi Airport improving to 366 thousand flights in 2024, reaching 95.8% of pre-pandemic levels at 382 thousand in 2019. Based on figures from March 2024, Changi Airport has recorded 94 thousand flights, 25.7% of FY24 levels. Airfreight movement also reached 1,995 thousand in FY24, representing 99.3% of pre-pandemic levels at 2,010 thousand in 2019. Going forward, flight activities in Singapore are likely to remain strong as travel demand continues to remain resilient amidst economic uncertainties. With the release of more flight routes and frequencies to and from Singapore, Changi Airport is bound to record higher flight activities for the rest of 2025. The upcoming summer peak travel season is expected to boost flight demand and volume as well. This, in turn, will translate to higher demand for MRO services for SIAEC.

FY25 results review. SIAEC reported revenue of S$1,245.1mn for FY24/25, up 13.8% YoY, compared to S$1,094.2mn in FY23/24, as the company continues to benefit from the recovery of demand for aircraft MRO services. The company also reported a FY24/25 operating profit of S$14.6mn, compared to an operating profit of S$2.3mn in FY23/24. Group profit after tax came in at S$141.6mn in FY24/25, up 16.0% YoY, compared to S$97.1mn in FY23/24, largely attributed to a higher share of profits of JVs and Associated companies.

We have fundamental coverage with a BUY recommendation and a TP of S$2.83. Please read the full report here.

Market consensus

(Source: Bloomberg)

CGN Mining Co Ltd. (1164 HK): More demand tailwinds upcoming

BUY Entry – 1.60 Target – 1.80 Stop Loss – 1.50

CGN Mining Co Ltd is a company mainly engaged in the trading of natural uranium. The Company operates its business through three segments. The Natural Uranium Trading segment is engaged in the trading of natural uranium. The Property Investment segment is engaged in leasing business. The Other Investments segment is engaged in investment activities.

Rebound in Uranium Prices. Uranium futures climbed above $71 per pound, extending their recovery after bottoming at an 18-month low of $64 in March and April. The rally reflects improving demand expectations and persistent stress on U.S. domestic mining capacity. Market sentiment was further supported by the U.S. government’s decision to pause tariffs on key trading partners and seek to reestablish trade ties with China, easing concerns over broader power demand. However, uncertainty around future tariffs on uranium imports from Canada and Kazakhstan continues to strain the limited domestic supply. The U.S. remains heavily reliant on imports—particularly from Kazakhstan, which currently faces a 27% reciprocal tariff, while Canadian imports are subject to a 10% levy.

Uranium future prices

(Source: Bloombeg)

Executive Orders to Support the Nuclear Sector. Sources indicate that U.S. President Donald Trump is set to sign a series of executive orders aimed at revitalizing the nuclear energy industry. The measures are expected to streamline regulatory approvals for new reactors and strengthen domestic nuclear fuel supply chains. A draft summary reveals plans to invoke the Cold War-era Defense Production Act, declaring a national emergency over U.S. reliance on Russia and China for enriched uranium, fuel processing, and advanced reactor components. The orders would also direct federal agencies to expedite siting and permitting of new nuclear facilities and instruct the Departments of Energy and Defense to identify federal lands for nuclear deployment. These actions are likely to boost demand for uranium, directly benefiting producers like CGN Mining.

China Accelerates Nuclear Expansion. In April 2025, China’s State Council approved the construction of 10 new nuclear reactors, reinforcing its commitment to nuclear power as a core component of its clean energy transition. This marks the fourth consecutive year China has approved at least 10 reactors. With 30 reactors currently under construction—nearly half of the global total—China is on track to surpass the U.S. as the world’s largest nuclear energy producer by the end of the decade. The China Electricity Council projects that the country’s nuclear capacity will reach 65 gigawatts by year-end, up from under 60 gigawatts last year. This rapid expansion is expected to significantly boost demand for uranium, positively impacting suppliers like CGN Mining.

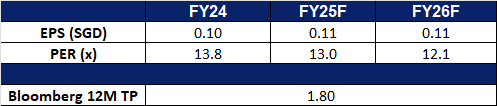

FY24 earnings. Revenue rose by 17.2% YoY to HK$8.62bn in FY24, compared to HK$7.36bn in FY23. Net profit fell to HK$342.0mn in FY24, compared to HK$497.1mn in FY23, primarily due to a loss coming from discontinued operations. Basis EPS from continuing operations and discontinued operations dropped to HK4.50cents in FY24, compared to HK$6.54cents in FY23.

Bloks Group Ltd is an investment holding company primarily engaged in the design, development and sales of assembly toys. The Company’s main products include assembly character toys and brick-based toys. The Company’s self-developed intellectual properties (IPs) include Magic Blocks and Hero Infinity. The Company’s licensed IPs include Ultraman, TRANSFORMERS, Naruto, Marvel: Infinity Saga and Spidey and His Amazing Friends, Minions, Pokemon and others. The Company mainly conducts its business in the domestic market.

Rise of China’s “Goods Economy”. Bloks Group is well-positioned to capture the momentum of China’s expanding “Goods Economy” (Guzi Economy), driven by Gen Z and Millennials’ emotional and identity-driven consumption habits. Demand is surging for ACGNC (anime, comics, games, novels, cosplay)-themed collectibles, such as blind boxes, as younger consumers increasingly view these goods as expressions of self and lifestyle. By aligning its product development and branding with culturally resonant trends, and through further investments in R&D, Bloks is poised to grow in the trillion-yuan industry both domestically and globally, alongside peers like Pop Mart.

Scalable SKU driven growth strategy. Bloks Group’s FY24 sales surged 155.6% YoY to RMB 2,240.9mn from RMB 876.7mn, supported by a robust IP portfolio and SKU (stock keeping unit) expansion. With over 50 licensed IPs and strong in-house development, the company aims to launch 800 new SKUs in 2025. Its strategy centers on broadening demographic appeal, from children to adult collectors, while growing its international presence through an omnichannel distribution model and content-driven marketing. Bloks will continue to enhance R&D and manufacturing capabilities to deliver high-quality, culturally resonant, and competitively priced assembly character toys that appeal across age groups and geographies.

FY24 earnings. Revenue rose by 155.6% YoY to RMB2,240.9mn in FY24, compared to RMB876.7mn in FY23. Gross profit increased 184.1% from RMB414.9mn in FY23 to RMB1,178.8mn in FY24, primarily due to a 212.5% increase in gross profit from assembly character toy sales, which was partially offset by a 64.6% decrease in gross profit from brick-based toy sales. Loss for the year was RMB398.0mn in FY24, up by 91.8% YoY from the loss of RMB207.5mn in FY23.

Market consensus.

(Source: Bloomberg)

Nebius Group NV. (NBIS US): Data centre expansion

BUY Entry – 38.0 Target – 45.0 Stop Loss – 34.5

Nebius Group is a technology company providing infrastructure and services to AI builders globally. The group’s core business, Nebius, is an AI-centric cloud platform built for AI workloads. Nebius Group serves customers worldwide.

Strong market outlook for AI factories and infrastructure. Nvidia CEO Jensen Huang stated at Computex 2025 that AI data centers are essentially AI factories, and the market for AI factories and related infrastructure is expected to reach a trillion-dollar scale.

Expansion in Europe and the U.S. Nebius currently operates data center facilities in Finland and France, with a new site opening soon in Iceland. The company plans to invest $1 billion in Europe and recently launched an Nvidia H200 GPU cluster in Paris. It also plans to triple its computing capacity in Finland, potentially scaling to 60,000 GPUs—this alone could generate up to $1 billion in revenue at full capacity. Nebius has just opened a data center in Kansas City and plans to build a hyperscale facility in New Jersey with a projected power capacity of up to 300 megawatts. For fiscal year 2024, the company reported $117.5 million in revenue and expects that to grow to between $750 million and $1 billion in fiscal year 2025.

Outperformance. In Q1 of fiscal 2025, revenue surged 385% YoY to US$55.3mn, with an adjusted net loss of US$92.5mn. The company’s AI infrastructure platform, which offers full-stack solutions to AI firms, reached an annual recurring revenue (ARR) of US$249mn in March, driven by expanded computing capacity and strong sales execution. CEO Arkady Volozh reaffirmed in a shareholder letter that the company remains on track to achieve US$750mn to US$1bn in ARR by year-end. Full-year revenue guidance remains between US$500mn and US$700mn. Adjusted EBITDA is expected to turn positive in the second half of 2025, although the full-year EBITDA will remain negative.

1Q25 results. Revenue rose 385.1% YoY to US$55.3mn and an adjusted net loss of US$92.5mn.

Market consensus

(Source: Bloomberg)

Broadcom Inc. (AVGO US): Enabling scalable AI through NVLink integration

Broadcom Inc. designs, develops, and supplies semiconductor and infrastructure software solutions. The Company offers storage adapters, controllers, networking processors, motion control encoders, and optical sensors, as well as infrastructure and security software to modernize, optimize, and secure the complex hybrid environments. Broadcom serves customers worldwide.

Nvidia’s NVLink fusion opens new opportunities. Nvidia’s recent decision to open its NVLink Fusion interconnect to third parties will allow companies like Broadcom to integrate advanced chip-to-chip communication into AI systems without heavy internal R&D investment. This shift democratizes high-speed connectivity, accelerating adoption of complex multi-chip AI architectures. As a result, Broadcom stands to benefit from increased demand for its networking and interconnect solutions, reinforcing its role in enabling scalable AI infrastructure.

Breakthrough in co-packaged optics strengthens AI leadership. Broadcom’s third-generation 200G/lane co-packaged optics (CPO) platform delivers over 30% power savings and is backed by a strong ecosystem, making it a cornerstone for next-generation AI data center connectivity. With a roadmap extending to 400G/lane, Broadcom is poised to lead the transition to high-radix, power-efficient hyperscale networks, essential for meeting the exponential growth in AI workloads.

1Q25 results. Revenue rose 24.7% YoY to US$14.92bn from US$11.96bn in 1Q24. Non-GAAP EPS rose to US$1.60 from US$1.10 in 1Q24. Broadcom declared a quarterly dividend of $0.59 per share. For the second quarter it expects revenue of approximately US$14.9bn, a 19% increase from the prior year period.