23 October 2024: Tianjin Pharmaceutical Da Re Tang Group Corp Ltd (TIAN SP), Goldwind Science & Technology Co Ltd. (2208 HK), Affirm Holdings Inc (AFRM US)

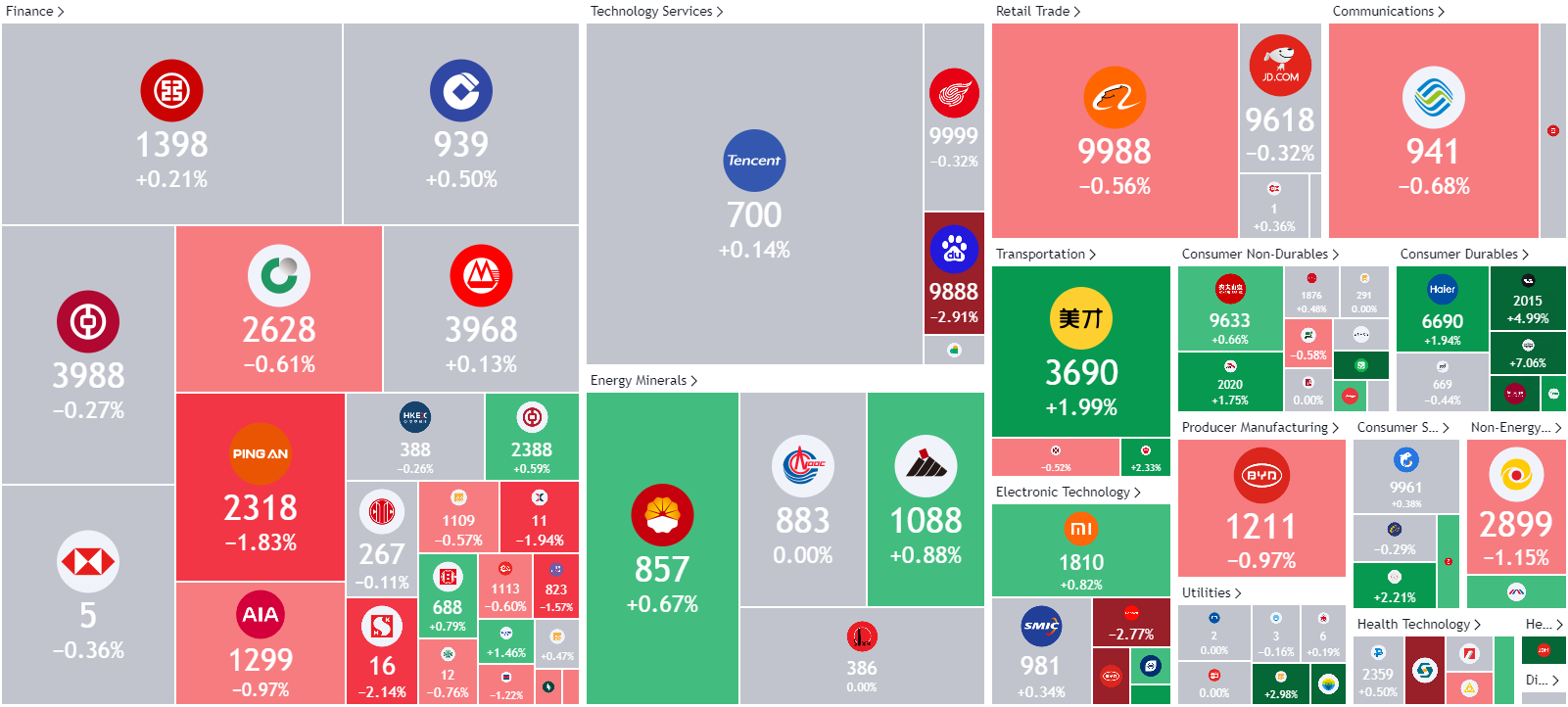

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

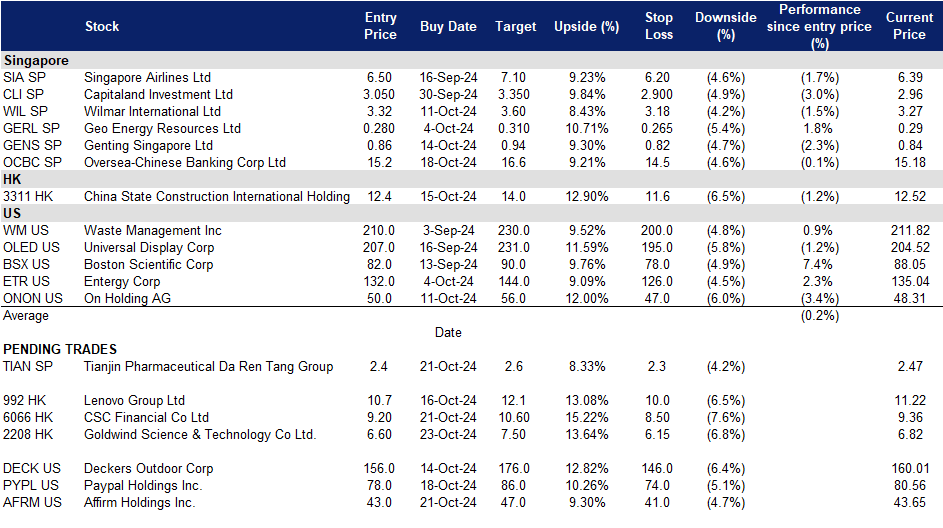

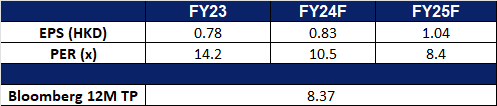

Tianjin Pharmaceutical Da Re Tang Group Corp Ltd (TIAN SP): Enhancing the world’s second-largest pharmaceutical market

- RE-ITERATE BUY Entry – 2.4 Target– 2.6 Stop Loss – 2.3

- Tianjin Pharmaceutical Da Ren Tang Group Corporation Limited produces and sells traditional Chinese medicine, western medicine, health products, and healthcare instruments. The Company also manufactures gene-related biopharmaceutical products. Tianjin Pharmaceutical Da Ren Tang Group markets its products under the Great Wall, Cypress, and Health brand names.

- Policy support. China’s government is accelerating the development of its pharmaceutical market by implementing policies that emphasize innovation and R&D. The Government Work Report, passed in 2024, outlines measures to modernize the country’s industrial system, including financial incentives, subsidies, and the creation of high-tech science parks. These initiatives aim to boost the domestic biotech industry, enhance innovation, and support the development of new drugs. Additionally, China has introduced national reimbursement for innovative therapies and seen a rise in FDA-approved drugs and out-licensing deals, particularly in oncology, further demonstrating the government’s commitment to advancing the pharmaceutical sector. These will help to support Tianjin Pharmaceutical’s research and development of more products and instruments.

- New joint venture. Tianjin Pharmaceutical Da Ren Tang Group Corporation Limited (formerly known as Tianjin Zhong Xin Pharmaceutical Group) is entering into an amended equity joint venture agreement regarding Tianjin TSKF Pharmaceutical Co., Ltd., alongside Haleon UK Services Limited and Haleon China Co., Ltd. This initiative includes extending the JV company’s operating period to 30 June 2025 and disposing of a 13% equity interest in the JV to Haleon China. Post-disposal, the equity structure will be adjusted, with Haleon UK holding 55%, Haleon China 33%, and Tianjin Da Ren Tang 12%.

- 1H24 results review. Revenue for 1H24 decreased by 3% YoY to RMB 3,965mn, a decrease of approximately RMB 124mn, driven mainly due to a YoY decrease in sale of goods. The profit attributable to equity holders in 1H24 was approximately RMB 658mn, a decrease of approximately RMB 65mn, or 9% from RMB 722mn of the corresponding period in 1H23. Earnings per share for 1H24 was RMB 0.85, lower than the RMB 0.94 in 1H23.

- Market Consensus.

(Source: Bloomberg)

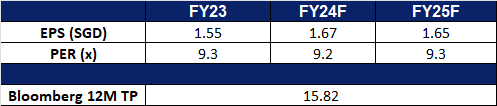

Oversea-Chinese Banking Corp Ltd (OCBC SP): Increased banking activity

- RE-ITERATE BUY Entry – 15.2 Target– 16.6 Stop Loss – 14.5

- Oversea-Chinese Banking Corporation Limited offers a comprehensive range of financial services. The Company’s services include deposit-taking, corporate, enterprise and personal lending, international trade financing, investment banking, private banking, treasury, stockbroking, insurance, credit cards, cash management, asset management and other financial and related services.

- Positive sentiment from the US banks. Despite declining interest rates impacting net interest income, US banks delivered strong third-quarter results, fuelled by increased deal-making and corporate debt issuance. There is growing optimism that the upcoming interest rate cuts will continue to boost deal activity as borrowing costs decline. Furthermore, with the strong stock market and expectations of a soft economic landing in the US are also boosting dealmakers’ confidence. This positive sentiment in the US banking sector has also extended to the banking market in Singapore.

- Collaboration with Disney. OCBC and Disney have announced a five-year strategic partnership across Singapore, Malaysia, and Indonesia, aimed at significantly increasing OCBC’s new customer base in Southeast Asia by 2029. The collaboration includes the launch of the OCBC MyOwn Account for children aged 7-15, allowing them to manage their own accounts under parental supervision via the OCBC app. The partnership will also feature Disney-themed bank cards, financial literacy materials with Disney characters, and related merchandise by mid-2025. OCBC highlighted that the partnership will help attract new customers by offering unique, non-price-based products and services.

- Increase in SME transactions. The OCBC SME Index saw gains for the second consecutive quarter, reaching 50.8 in 3Q24, up from 50.2 in 2Q24. This improvement reflects a slight increase in collections and payments by SMEs, supported by cooling inflation and stronger external demand. In a survey of 1,100 SMEs, 40% reported better business performance, up from 35% in the previous quarter. Looking ahead, 48% of SME owners expect further improvement over the next six months, while 40% foresee stable conditions. Singapore’s GDP growth for 3Q24 is estimated at over 3.5%, surpassing earlier forecasts. Despite, potential risks from geopolitical tensions and economic uncertainties, OCBC anticipates continued expansion in the fourth quarter and relative stability in the year ahead.

- 1H24 results review. Total income for 1H24 increased by 7% YoY to S$7.26bn, net interest income and non-interest income rose 3% and 15% YoY respectively. Net profit increase by 9% YoY to S$3.93bn in 1H24, compared to S$3.59bn in 1H23, mainly due to record total income and lower allowances. The Board declared an interim dividend of S$0.44, up 10% or S$0.04 from a year ago, representing a payout ratio of 50% of the Group’s 1H24 net profit.

- Market Consensus.

(Source: Bloomberg)

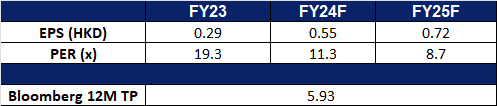

Goldwind Science & Technology Co Ltd. (2208 HK): Spurring investments into renewable energy

- BUY Entry – 6.60 Target 7.50 Stop Loss – 6.15

- Goldwind Science & Technology Co Ltd, formerly Xinjiang Goldwind Science & Technology Co Ltd, is a China-based company that provides overall solutions for wind turbines, wind power services and wind farm development. The Company operates its businesses through four segments. The Wind Turbine Manufacturing and Sales segment is mainly engaged in the research and development, manufacturing and sales of wind turbines and their parts. The Wind Power Service segment mainly provides wind power-related consultants, wind farm construction and maintenance and transportation services. The Wind Farm Development segment is mainly engaged in the development and operation of wind farms. Other segment is mainly engaged in financial leasing and water treatment development and operation business. The Company conducts its businesses both in the domestic market and overseas markets.

- New Renewable Energy Consumption Benchmarks. China’s National Development and Reform Commission (NDRC) and National Energy Administration (NEA) have jointly released updated requirements for the percentage of energy that provinces must source from renewable generators in 2024 and 2025. These requirements are part of China’s renewable energy consumption guarantee mechanism, mandating a significant increase in the share of renewable energy in several provinces. The document also outlines tentative renewable energy consumption targets for 2025. Current data reveals that six provinces experienced increases exceeding 6 percentage points in their renewable energy consumption mandate between 2023 and 2024. China remains on track to achieve its renewable energy goals, aiming for renewable energy, including hydropower, to account for 40 percent of total national energy consumption by 2030. This benchmarks are likely to spur on more investment into renewable energy as well.

- Increasing use of renewable energy in China. China’s renewable energy utilization has reached or exceeded advanced international levels, demonstrating rapid progress in sustainable energy. The country has maintained strong momentum in renewable energy adoption, with a utilization rate of 97.6%, surpassing 95% for six consecutive years since 2018. Last year, newly installed renewable energy capacity rose to 290 million kW, 2.4 times that of 2022, accounting for 79% of the total new power generation capacity nationwide, making it the primary source of new power generation. This surge in capacity has spurred significant investments in solar, wind, and hydropower projects across the country. These efforts are part of China’s broader strategy to peak carbon emissions before 2030 and achieve carbon neutrality before 2060. Furthermore, China’s National Energy Administration also recently reported that 486 million Green Electricity Certificates (GECs) were issued during the first half of 2024– a 13-fold increase compared to the same period last year, further signalling progress towards the decarbonisation and reform of the power sector. Goldwind is likely to benefit from the increased investment and spending in renewable energy.

- Expanding presence. Goldwind Science & Technology has officially opened its first overseas wind turbine manufacturing plant in Brazil. The facility has begun production with a capacity to produce up to 150 turbines annually. Valued at approximately $18.2 million, this investment aims to strengthen local supply chains and leverage the region’s rich wind resources. While the plant will primarily serve the Brazilian market, it is also positioned to export equipment across South America via the port of Bahia. With this new facility, Goldwind is expected to secure a 24% to 30% share of the Brazilian wind turbine market.

- 1H24 earnings. The company’s revenue rose to RMB20.1bn in 1H24, +6.53% YoY, compared to RMB18.9bn in 1H23. The company’s net profit rose by 6.74% YoY to RMB1.44bn in 1H24, compared to RMB1.35bn in 1H23. Basic earnings per share rose to RMB0.32 in 1H24, compared to RMB0.28 in 1H23.

- Market consensus.

(Source: Bloomberg)

CSC Financial Co Ltd (6066 HK): Resuscitating the economy

- RE-ITERATE Entry – 9.20 Target 10.60 Stop Loss – 8.50

- China Securities Co., Ltd. is mainly engaged in securities brokerage, securities investment consulting, financial advisers related to securities trading and securities investment activities, securities underwriting and sponsor, securities self-management, securities asset management, securities investment fund agent distribution, providing futures companies with medium introduction services, margin financing, financial products agent distribution, insurances facultative agent, stock options market making, securities investment fund trusteeship and precious metal products sales businesses.

- More stimulus to boost economy. In response to the largest stimulus package announced in late September, China introduced a second round of economic stimulus and policy measures in early October to further bolster its economy. The government has pledged to “significantly increase” debt in an effort to revitalize its sluggish economy. These initiatives aim to assist local governments in managing their debt, provide subsidies to low-income individuals, support the property market, and strengthen state banks’ capital, among other objectives. Markets are currently awaiting further details on the scale of the package and a more comprehensive plan to stabilize the economy for long-term growth, which is expected to be announced by the end of October. China’s economy grew at a slower pace in 3Q24, with GDP expanding by 4.6%, slightly down from 4.7% in 2Q24. The ongoing weakness in the property sector continues to be a concern, and further stimulus measures are expected to support economic recovery.

- More liquidity injected into the stock market. China has also previously announced a reduction in the reserve requirement ratio (RRR), which determines the amount of cash banks must hold in reserve. This move is expected to inject approximately one trillion yuan of “long-term liquidity” into the financial market. Additionally, the government will introduce a “swap program,” allowing companies to obtain liquidity directly from the central bank. This initiative, with an initial scale of 500 billion yuan and potential future expansions, is expected to significantly improve firms’ access to capital for stock purchases. The anticipated increase in market liquidity is likely to boost investor sentiment, benefiting firms like CSC Financials.

- Benefitting from a lower interest rates. The lowering of Hong Kong’s interest rate by 50 basis points to 5.25% recently, mirroring the U.S. Federal Reserve’s move. This rate cut is expected to boost business confidence and stimulate consumer spending in Hong Kong. Lower rates are also likely to encourage a shift of funds from safe assets into the stock market, enhancing market liquidity and trading volumes. The recent recovery of the Hang Seng Index, which is now trading at a 52-week high, around the 20,000 level is bound to improve investor sentiments, further driving fund flows in the Hong Kong stock market. CSC Financial is well-positioned to benefit from the increased liquidity and volume of the stock market.

- 1H24 earnings. Total revenue fell by 20.5% YoY to RMB14.8bn in 1H24, compared to RMB18.7bn in 1H23. Net profit fell by 33.6% YoY to RMB2.86bn in 1H24, compared to RMB4.32bn in 1H23. Basic earnings per share was RMB0.30 in 1H24, compared to RMB0.49 in 1H23.

- Market consensus.

(Source: Bloomberg)

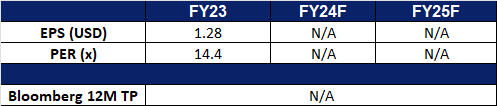

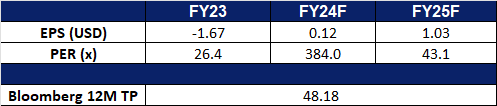

Affirm Holdings Inc (AFRM US): Growth of BNPL services

- RE-ITERATE BUY Entry – 43 Target – 47 Stop Loss – 41

- Affirm Holdings, Inc. is a financial technology company. The Company builds platform for digital and mobile-first commerce. Affirm Holdings offers financial services tool that allows consumers to purchase goods and services. Affirm Holdings serves customers worldwide.

- Small and medium-cap stocks lags behind. The three major indexes have all reached record highs, but the Russell Index is still in a volatile upward trend, and there is still about 7.5% room to rise from the historical high in 2021. Small and mid-cap stocks are more sensitive to expectations of interest rate changes; under the interest rate cut cycle, the valuations of small and mid-cap stocks are expected to gradually recover upwards.

- Favoured by the younger generation. Buy Now Pay Later (BNPL) is similar to a personal installment loan. If paid in full and on time, it is usually interest-free. If the payment is late, additional interest will be paid. According to Emarketer, the total amount of buy-now-pay-later consumption in the United States will increase by 12.3%/20.4% respectively in 2024/25 to US$80.77 billion/97.25 billion. Among them, 33.6 million and 26.4 million Millennials and Generation Z use buy now and pay later respectively. This group will be the main consumption force in the future, so the market growth prospects are optimistic.

- Looking forward to the upcoming shopping peak season. European and American countries will enter the year-end shopping season. Black Friday and Christmas holiday consumption will further stimulate buy now, pay later growth. Affirm is a strategic partner with Amazon and Shopify. The two major platforms should choose Affirm as a payment method. In addition, Apple has withdrawn from the buy now, pay later business, which has increased the market penetration of buy now, pay later providers and credit card institutions. Apple users prefer Affirm’s buy now, pay later.

- 4Q24 earnings review. Revenue increased 47.9% YoY to US$659 million, exceeding expectations by US$53.8 million. GAAP loss per share was US$0.14, beating expectations by US$0.3.

- Market consensus.

(Source: Bloomberg)

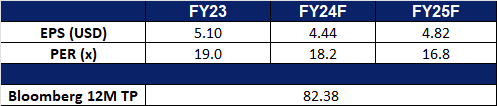

PayPal Holdings Inc (PYPL US): Spending to rise

PayPal Holdings Inc (PYPL US): Spending to rise

- RE-ITERATE BUY Entry – 78 Target – 86 Stop Loss – 74

- PayPal Holdings, Inc. operates as a holding company. The Company, through its subsidiaries, provides technology platform that enables digital and mobile payments on behalf of consumers and merchants. The Company offers online payment solutions. PayPal Holdings serves customers worldwide.

- Declining interest rates. Despite consumer sentiment declining to 68.9 in October from 70.1 in September, below forecasts of 70.8, inflationary pressures continue to affect consumers with persistently high prices. However, with 50bps rate cuts in September and another 50bps expected by year-end, the economic environment is starting to shift. The effects of these rate cuts have already begun to materialize, as seen in increased mergers and acquisitions among corporations, signalling more activity in the business sector. Inflationary pressures on consumption are expected to gradually ease, though consumers may still feel the pinch in the short term. During this period, more people may turn to PayPal’s “Buy Now, Pay Later” (BNPL) options, such as its “Pay in 4” checkout method, which allows users to make purchases in bi-weekly installments. This could incentivize higher spending as consumers look for ways to manage their cash flow while still making necessary purchases. For higher-value items, consumers may opt for monthly installment payments, where PayPal stands to benefit not only from increased transaction volumes and fees but also from the Annual Percentage Rate charged to consumers using the “Pay Monthly” option. With lowering interest rates and the upcoming holiday season, consumer spending is expected to rise, even among those who may not have the immediate funds to purchase items outright. The BNPL function will enable these consumers to buy now and pay later, boosting overall consumer spending and driving higher revenue for PayPal.

- Launch a platform in China. PayPal has launched its Complete Payments platform in China, aimed at streamlining payments and receivables for businesses of all sizes, supporting cross-border transactions. The platform offers Chinese businesses various payment options, quick fund settlements, and risk management and fraud detection tools. It connects merchants to PayPal’s global network, enabling transactions in over 100 currencies and 200 regions, reaching over 400 million active users. The platform is integrated with WooCommerce and aims to help small- to medium-sized businesses grow by offering customized checkout experiences and advanced solutions. This geographical expansion to China will help PayPal to expand its global footprint.

- Expansion of its cryptocurrency offerings. PayPal now allows US merchants to buy, hold, and sell cryptocurrency through their business accounts, expanding on its crypto services for consumers, which started in 2020. This follows the launch of its stablecoin, PayPal USD, in 2023. PayPal’s merchants had expressed interest in the same cryptocurrency features available to consumers. Businesses would be able to transfer digital currency to third-party wallets and conduct blockchain transactions, though the service would not initially be available in New York. By integrating cryptocurrencies into its US platform, PayPal gains a competitive edge in the market, offering a broader range of payment solutions compared to other platforms.

- 4Q24 earnings review. Revenue increased 8.2% YoY to US$7.9bn, exceeding expectations by US$80mn. Non-GAAP earnings per share were US$1.19, beating expectations by US$0.20. The company guided for 3Q24 revenue growth of mid-single digit and GAAP EPS of US$0.96 to US$0.98. For FY24, PayPal expects GAAP EPS of US$3.88 to US$3.98 and non-GAAP EPS growth of low to mid-teens.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add Overseas-Chinese Banking Corp Ltd (OCBC SP) at S$15.2. Cut loss on OUE REIT (OUEREIT SP) at S$0.305.