Centurion Corporation Limited provides purpose-built workers and student accommodation services. Centurion owns, develops, and manages quality and purpose-built workers accommodation assets. Centurion serves customers worldwide.

REIT listing exploration. Centurion is exploring a potential REIT structure comprising stabilized PBWA and PBSA assets in mature markets like Singapore, Malaysia, and the UK. This could unlock asset value, enhance capital recycling, and deliver stable income for shareholders via a potential dividend-in-specie.

Stronger than anticipated revenue growth. Total revenue rose 22% YoY to S$253.6 million, while net profit after tax surged 118% to S$382.6 million, driven by high financial occupancy and rental rate uplifts across all key markets.

Expanding global footprint. As of 31 December 2024, Centurion operated 69,929 beds across 37 assets with AUM of S$2.5 billion. It added 2,552 new beds and has 7,662 beds under development for 2025-2026, including a new PBSA in Macquarie Park, Australia.

2H24 results review. Revenue increased 18% YoY to S$129.2 million from S$109.3 million in 2H23, while gross profit grew 27% to S$101.5 million, underpinned by sustained high occupancy and positive rental revisions. Despite a slight dip in PBWA occupancy in Malaysia, attributable to short-term foreign worker caps, strong rental performance and high occupancy in key markets like Singapore, the UK, and Australia offset this temporary weakness. Centurion declared a final dividend of 3.5 Scents per share for FY24, representing a 28.6% increase from the 2.5 Scents distributed in FY23.

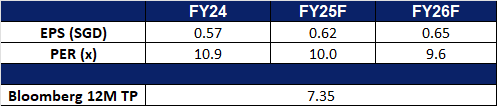

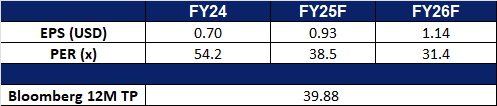

We have fundamental coverage with a BUY recommendation and a TP of S$1.38. Please read the full report here.

Market consensus

(Source: Bloomberg)

Sembcorp Industries Ltd (SCI SP): Risk off and rate cut expectations

Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

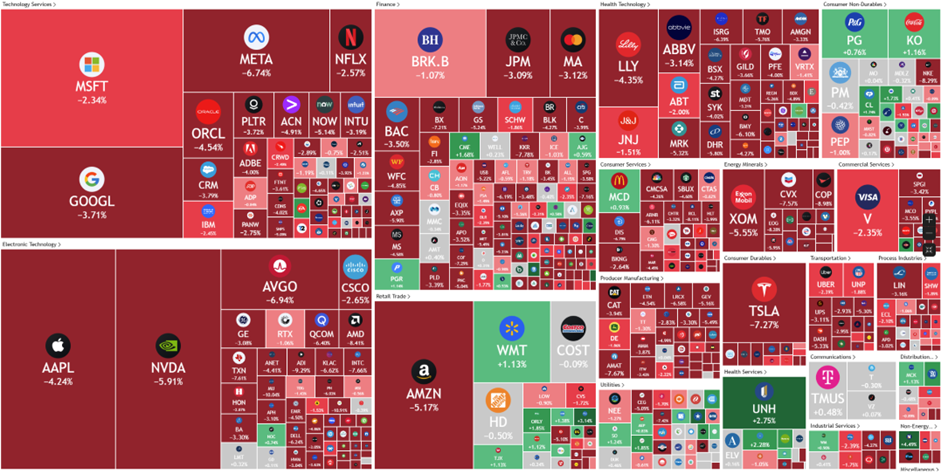

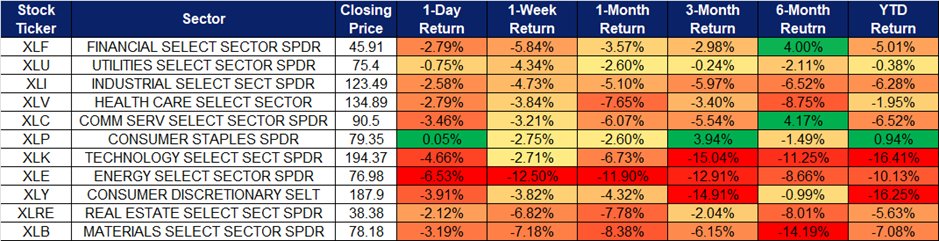

Rotation to defensive sectors and rising rate cut expectations. Escalating global trade tensions, driven by the broad tariff policies of the US, will gradually reshape global supply chains. World economic growth, especially in Asia, is expected to slow down substantially in the near term. Amidst macro headwinds, the utility sector is expected to outperform others. Meanwhile, expectations of rate cut are reviving. Lower interest rates would benefit Sembcorp by reducing financing costs, enhancing project viability, and potentially boosting demand for its energy and urban solutions. In a nutshell, investors favour assets with stability and visibility moving forward.

Proposed acquisition. Sembcorp Industries plans to increase its stake in Senoko Energy from 30% to a maximum of 70%, expanding its role in Singapore’s energy sector. The acquisition agreement, signed with KPIC Netherlands, Kyuden International, and Japan Bank for International Cooperation (JBIC), involves purchasing up to a 57.1% stake in Lion Power, which owns 70% of Senoko. The deal, valued at up to S$144mn, will be funded through internal cash and/or external borrowings and is expected to close in 2Q25. The Energy Market Authority has approved the acquisition, with Sembcorp committing to measures that ensure fair market competition. The acquisition is projected to be earnings accretive but will not significantly impact net tangible assets per share for FY25. This strategic move strengthens Sembcorp’s position in Singapore’s energy market and supports its commitment to the energy transition. With a larger stake in Senoko, Sembcorp can enhance operational synergies and contribute more effectively to sustainable and reliable energy solutions, aligning with its long-term growth strategy.

Increased dividend payout. Sembcorp raised its dividend to S$0.23 per share, from its previous S$0.13 in FY23, reflecting a higher payout ratio, signaling confidence in sustained profitability. The company’s net profit before exceptional items remained above S$1bn for a second consecutive year. Sembcorp’s gas and related services segment saw a 10% decline in profit to S$727mn, impacted by a 34% drop in Singapore’s wholesale electricity prices. However, the company solidified its position as the leading power provider for data centers and acquired a 30% stake in Senoko Energy. Additionally, it fully exited coal-fired power assets with the divestment of its 49% stake in Chongqing Songzao. Sembcorp’s renewable energy portfolio grew to 13.1 GW in 2024, progressing toward its 2028 goal of 25 GW. The company remains focused on executing its 2024-2028 strategic plan to meet Asia’s evolving energy needs. With a stronger commitment to dividends and an expanding clean energy portfolio, the company is poised to capitalize on Asia’s transition to sustainable energy while maintaining financial stability.

FY24 financial results. Sembcorp Industries Ltd reported net profit of S$1,011mn for FY24, a 7% incline YoY, compared to S$942mn in FY23. Due to the Group’s strong performance, the Board of Directors approved a total dividend of S$0.23 per ordinary share for FY24, an increase from the S$0.13 distributed for FY23.

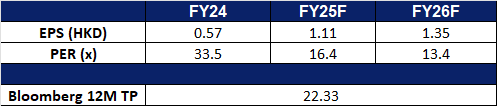

Market consensus

(Source: Bloomberg)

Shandong Gold Mining Ltd. (1787 HK): The strength of Gold amidst economic uncertainties

BUY Entry – 18.8 Target – 20.8 Stop Loss – 17.8

Shandong Gold Mining Co., Ltd. is a China-based company principally engaged in the mining, processing and sales of gold. The Company operates two segments. The Gold Mining segment is engaged in the mining of gold ore. The Gold Refining segment is engaged in the production and sales of gold. The Company is also engaged in the distribution of other metals extracted during the gold ore smelting process, such as silver, copper, iron, lead and zinc. The Company conducts its businesses in domestic and overseas markets.

Gold Prices Near All-Time High. Gold continues its upward trajectory, nearing record highs as investors seek refuge in safe-haven assets amid mounting global economic uncertainties. The precious metal, often viewed as a hedge against inflation and geopolitical instability, has surged over 18% year-to-date in 2025. Key drivers include escalating geopolitical tensions in the Middle East and Ukraine, heightened central bank gold purchases, robust inflows into gold-backed ETFs, and growing market expectations of U.S. interest rate cuts. Additionally, renewed trade tensions between the U.S. and China—marked by tit-for-tat tariff hikes, with U.S. duties on Chinese imports rising to 125% and China’s retaliatory tariffs climbing to 84%—have further fueled investor anxiety. The ongoing trade war between the world’s two largest economies is likely to sustain upward pressure on gold prices in the near term.

Gold price

(Source: Bloomberg)

Record Gold ETF Inflows in China. Chinese investors are increasingly turning to gold-backed ETFs as a safe-haven play amid intensifying trade hostilities. Last week, inflows into four major onshore gold ETFs, including the Huaan Yifu Gold ETF, reached a record 7.6 billion yuan, according to Bloomberg. Strong inflows have continued this week, reflecting growing demand for gold exposure as global market volatility rises. This surge in investor interest is expected to support the performance of Chinese gold miners such as Shandong Gold.

Commissioning of Major Gold Mine in Ghana. At the end of 2024, Ghana officially commissioned its largest single gold stream mine, located in the Talensi District of the Upper East Region. The project, developed by Cardinal Namdini Gold Limited (a subsidiary of Shandong Gold Limited), is an open-pit mine with an initial lifespan of 15 years. It is projected to process approximately 150 million tonnes of ore, yielding an estimated five million ounces of gold. The commencement of operations is expected to enhance Shandong Gold’s production profile and contribute positively to its long-term growth.

FY24 earnings. Revenue increased by 39.2% YoY to RMB82.5bn in FY24, compared to RMB59.3bn in FY23. Profit increased by 55.4% to RMB4.39bn in FY24, compared to RMB2.82bn in FY23. Basic earnings per share was RMB0.56 in FY24, compared to a basic earnings per share of RMB0.40 in FY23, representing an increase by 40.0% YoY.

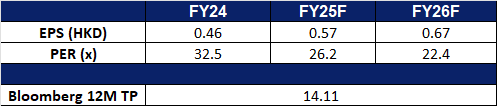

Market consensus.

(Source: Bloomberg)

Weilong Delicious Global Holdings Ltd. (9985 HK): Plans to boost consumption levels

Weilong Delicious Global Holdings Ltd is a China-based holding company principally engaged in the production and sales of spicy snack foods. The Company operates in three segments: Seasoned Flour Products segment, Vegetable Products segment and Bean-based and Other Products segment. The Seasoned Flour Products segment mainly includes Big Latiao, Mini Latiao, Spicy Hot Stick, Mini Hot Stick and Kiss Burn. The Vegetable Products segment mainly includes Konjac Shuang and Fengchi Kelp. The Bean-based and Other Products segment mainly includes Soft Tofu Skin, 78° Braised egg and meat products.

Plans to Boost Consumption. China recently unveiled a “Special Action Plan to Boost Consumption”, reinforcing its commitment to stimulating domestic demand. The plan aims to drive consumption growth, expand household spending power, and enhance purchasing capacity by raising incomes and reducing financial burdens. This follows Premier Li Qiang’s recent government work report, which identified consumption growth as the country’s top economic priority for the year. Key measures include employment support initiatives, enhanced unemployment benefits, and targeted income-boosting efforts for both urban and rural residents, including farmers. Beyond short-term stimulus, the plan signals China’s resolve to tackle structural challenges such as stagnant wage growth, negative wealth effects from property and stock market downturns, and an inadequate social safety net. Furthermore, China will also place greater emphasis on domestic consumption as a key driver of economic growth this year, aiming to counterbalance the effects of softer external demand resulting from higher tariffs imposed by the Trump administration. The expected rise in consumption level could have a positive impact on Weilong Delicious Global Holdings, as stronger domestic demand may support the company’s growth.

Partnership with KFC. Earlier this year, Weilong Delicious has partnered with KFC to launch a co-branded “Spicy Strip Flavor Large Chicken Strips,” capitalizing on the fast-food chain’s popular “Crazy Four” promotion to engage young consumers. This collaboration follows previous partnerships with Pizza Hut and Xiaolongkan Hotpot, reinforcing Weilong’s strategy of leveraging fast-food platforms to enhance brand visibility and product appeal. By prioritizing genuine product innovation and aligning with fast-food consumption trends, Weilong aims to translate marketing buzz into sustained consumer engagement. This approach reflects shifting dynamics in China’s consumer market, where brands must focus on core customer segments and product differentiation rather than broad, awareness-driven marketing campaigns to drive long-term growth.

FY24 results review. Revenue increased by 8.6% YoY to RMB6.27bn in FY24, compared with RMB4.87bn in FY23. Net profit increased by 21.3% to RMB1,068.5bn in FY24, compared to RMB880.3mn in FY23. EPS rose to RMB0.46 in FY24 compared with RMB0.38 in FY23. The company also announced a final dividend of RMB0.11 per share and a special dividend of RMB0.18 per share for FY24.

Market consensus.

(Source: Bloomberg)

UnitedHealth Group Inc (UNH US): Favourable Medicare rate decision

BUY Entry – 560 Target – 620 Stop Loss – 530

UnitedHealth Group Incorporated owns and manages organized health systems. The Company provides employers products and resources to plan and administer employee benefit programs. UnitedHealth serves customers worldwide.

Favourable Medicare reimbursement outlook. The U.S. government’s decision to raise Medicare Advantage reimbursement rates by 5.06% for 2026, double the initially proposed increase, provides a significant tailwind for health insurers like UnitedHealth Group. This adjustment offers much-needed relief following a challenging 2024, helping to offset elevated medical costs and strengthening profit margins. The upward revision, based on updated claims and cost data, also signals a potentially more supportive regulatory environment for Medicare-focused insurers

Defensive strength of an essential service. As the largest U.S. provider of a critical, essential service, UnitedHealth Group benefits from stable demand across economic cycles. The necessity of healthcare, underpinned by the high cost of treatment and widespread employer-sponsored insurance, ensures a recurring revenue base through consistent premium payments. This defensive positioning makes UnitedHealth more resilient to macroeconomic headwinds, offering both income stability and long-term growth potential.

4Q25 results. Revenue increased by 6.8% YoY to US$100.8bn, missing expectations by US$930mn. Non-GAAP earnings per share were US$6.81, exceeding expectations by US$0.07. For FY25, the company expects revenue to be between US$450bn to US$455bn and adjusted EPS of US$29.5 to US$30.0.

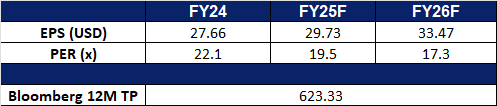

Market consensus

(Source: Bloomberg)

Carmax Inc (KMX US): Benefitting from implementation of tariffs

CarMax, Inc. retails automobiles. The Company offers used cars, vans, electric vehicles, and light trucks, as well as provides rental, maintenance, post warranty repairs, mechanical and painting work, diagnosis insurance, valuation, and security services. CarMax serves customers in the United States.

Auto tariffs benefit. Trump’s 25% auto tariffs, set to take effect on April 2nd, are prompting consumers to accelerate vehicle purchases to avoid price increases. Dealerships are reporting increased customer traffic, with used car inquiries up 16% on Dealer.com and new car demand surging 54%. This surge in demand benefits CarMax, as more consumers turn to the used car market to navigate new car price uncertainties. Higher demand will boost CarMax’s sales volume, profit margins, and profitability, further solidifying its market position in a rising cost environment.

3Q25 performance. Net sales increased by 1.1% YoY to US$6.22bn, exceeding expectations by US$170mn. GAAP earnings per share were US$0.81, beating estimates of US$0.60. This was primarily driven by a 5.4% increase in retail used vehicle unit sales and a 6.3% growth in wholesale unit sales. CarMax Auto Finance revenue also increased by 7.6%, and the company repurchased US$114.8mn worth of shares. Despite a decrease in average retail prices, the increase in sales volume successfully offset the impact. CarMax’s focus on digital expansion and cost management, coupled with expected continued improvement in sales volume, will help drive revenue growth.

3Q25 results. Revenue increased by 1.1% YoY to US$6.22bn, exceeding expectations by US$170mn. GAAP earnings per share were US$0.81, exceeding expectations by US$0.20.

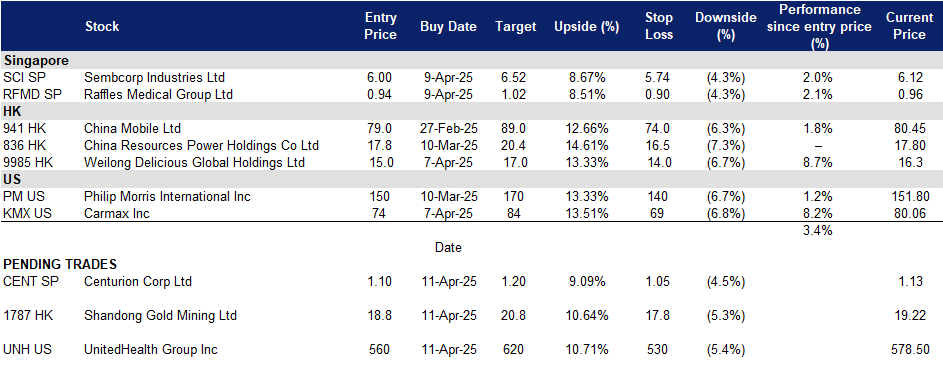

Trading Dashboard Update: Add andtake profit on Mixue Bingcheng Co Ltd (2097 HK) at HK$370 and HK$410 respectively. Add Sembcorp Industries Ltd (SCI SP) at S$6.0 and Raffles Medical Group Ltd (RFMD SP) at S$0.94. Cut loss on Waste Management Inc (WM US) at US$215.