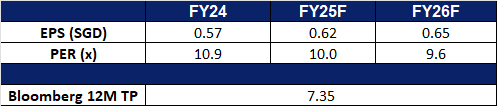

Raffles Medical Group Ltd (RFMD SP): Boosted by expansion opportunities

BUY Entry – 0.94 Target– 1.02 Stop Loss – 0.90

Raffles Medical Group Limited is a health care provider. The Company operates medical clinics, imaging centers, and medical laboratories. Raffles provides general and specialized medical, medical evacuation, medical advisory, and dental treatment services.

Establishing stronger ties. Singapore-linked firms are making major strides in China’s healthcare sector despite economic headwinds, with Raffles Medical Group recently partnering with Shanghai’s renowned Renji Hospital. This collaboration aims to create a “dual circulation” system, allowing Raffles patients access to top Chinese specialists while offering Renji exposure to affluent patients across Asia. Raffles, which already operates hospitals and clinics in several Chinese cities, sees strong demand from patients willing to spend on quality healthcare despite a broader economic slowdown. As China encourages domestic medical consumption and tourism, Singapore’s healthcare firms are well-positioned to expand their footprint.

Improved confidence and optimistic growth outlook. Raffles Medical Group has demonstrated increased shareholder confidence by revising its dividend policy to distribute at least 50% of its sustainable earnings annually and announcing plans to repurchase up to 100 million shares over the next two years. The company reported a 4.3% increase in net profit to S$31.6 million in the second half of 2024, alongside a 14.8% growth in revenue to S$385.9 million. Despite a 31% decline in full-year net profit due to the cessation of Covid-19 services and reduced government grants, Raffles Medical remains optimistic about its profitability in 2025. The company anticipates continued expansion into new markets and meeting the rising demand for personalized healthcare, supported by its hospitals in Beijing, Shanghai, and Chongqing, which are positioned to drive future growth. Regional revenue in 2024 grew 10.1% to S$65.3 million, bolstered by the growing recognition of the Raffles Hospital brand in China. This demonstrates the company’s resilience and long-term potential in the rapidly expanding healthcare market.

Advantage from China’s policy support. China’s recent policy shift, allowing foreign healthcare providers to fully own hospitals in key regions like Beijing, Shanghai, and Guangzhou, presents a significant opportunity for Raffles Medical Group. This policy change aligns with Raffles Medical’s strategy to expand its footprint in China, capitalizing on its expertise to provide high-quality, personalized healthcare services tailored to both local and expatriate populations. By establishing wholly-owned facilities in China’s growing economic zones, Raffles Medical can strengthen its position in a competitive market, addressing the increasing demand for advanced medical services. However, the group must also navigate regulatory requirements, such as the mandate that at least 50% of healthcare professionals in these hospitals must be from mainland China. By ensuring compliance and integrating international care standards, Raffles Medical can continue its expansion while maintaining high levels of service and reinforcing its brand presence in the Chinese healthcare sector.

Partnership with AIA. Raffles Hospital and AIA Singapore recently signed a memorandum of understanding (MoU) to improve access to healthcare services. Through this collaboration, more than 90 Raffles Hospital specialists will join the AIA Quality Healthcare Partners panel, expanding the network to nearly 700 specialists for AIA HealthShield Gold Max customers. Additionally, both organizations will share quality indicators and patient outcomes to support a value-based healthcare model. The partnership also includes joint management of hospitalization bills for AIA policyholders, ensuring alignment with the Ministry of Health’s fee benchmarks. This initiative is expected to enhance healthcare quality, improve patient access, and provide Raffles Medical with a larger base of AIA HealthShield Gold Max customers, driving higher patient volume.

2H24 results review. Revenue increased by 14.8% YoY to S$385.9 million, primarily driven by strong performance from its hospital services division. Net profit rose 4.3% to S$31.6 million. The hospital services division saw a 4.6% revenue increase to S$345.7 million, while the healthcare services division grew 4.1% to S$295.1 million, though profitability declined. The board proposed a final dividend of 2.5 cents per share, up from 2.4 cents for the year-ago period.

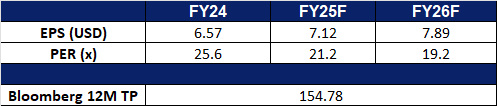

Market consensus

(Source: Bloomberg)

Sembcorp Industries Ltd (SCI SP): Risk off and rate cut expectations

BUY Entry – 6.00 Target– 6.52 Stop Loss – 5.74

Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

Rotation to defensive sectors and rising rate cut expectations. Escalating global trade tensions, driven by the broad tariff policies of the US, will gradually reshape global supply chains. World economic growth, especially in Asia, is expected to slow down substantially in the near term. Amidst macro headwinds, the utility sector is expected to outperform others. Meanwhile, expectations of rate cut are reviving. Lower interest rates would benefit Sembcorp by reducing financing costs, enhancing project viability, and potentially boosting demand for its energy and urban solutions. In a nutshell, investors favour assets with stability and visibility moving forward.

Proposed acquisition. Sembcorp Industries plans to increase its stake in Senoko Energy from 30% to a maximum of 70%, expanding its role in Singapore’s energy sector. The acquisition agreement, signed with KPIC Netherlands, Kyuden International, and Japan Bank for International Cooperation (JBIC), involves purchasing up to a 57.1% stake in Lion Power, which owns 70% of Senoko. The deal, valued at up to S$144mn, will be funded through internal cash and/or external borrowings and is expected to close in 2Q25. The Energy Market Authority has approved the acquisition, with Sembcorp committing to measures that ensure fair market competition. The acquisition is projected to be earnings accretive but will not significantly impact net tangible assets per share for FY25. This strategic move strengthens Sembcorp’s position in Singapore’s energy market and supports its commitment to the energy transition. With a larger stake in Senoko, Sembcorp can enhance operational synergies and contribute more effectively to sustainable and reliable energy solutions, aligning with its long-term growth strategy.

Increased dividend payout. Sembcorp raised its dividend to S$0.23 per share, from its previous S$0.13 in FY23, reflecting a higher payout ratio, signaling confidence in sustained profitability. The company’s net profit before exceptional items remained above S$1bn for a second consecutive year. Sembcorp’s gas and related services segment saw a 10% decline in profit to S$727mn, impacted by a 34% drop in Singapore’s wholesale electricity prices. However, the company solidified its position as the leading power provider for data centers and acquired a 30% stake in Senoko Energy. Additionally, it fully exited coal-fired power assets with the divestment of its 49% stake in Chongqing Songzao. Sembcorp’s renewable energy portfolio grew to 13.1 GW in 2024, progressing toward its 2028 goal of 25 GW. The company remains focused on executing its 2024-2028 strategic plan to meet Asia’s evolving energy needs. With a stronger commitment to dividends and an expanding clean energy portfolio, the company is poised to capitalize on Asia’s transition to sustainable energy while maintaining financial stability.

FY24 financial results. Sembcorp Industries Ltd reported net profit of S$1,011mn for FY24, a 7% incline YoY, compared to S$942mn in FY23. Due to the Group’s strong performance, the Board of Directors approved a total dividend of S$0.23 per ordinary share for FY24, an increase from the S$0.13 distributed for FY23.

Market consensus

(Source: Bloomberg)

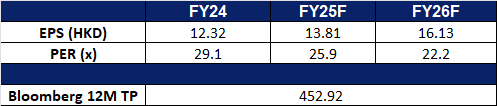

Mixue Bingcheng Co Ltd. (2097 HK): An insulation against the ongoing trade war

BUY Entry – 370 Target – 410 Stop Loss – 350

Mixue Bingcheng Co Ltd is a China-based company principally engaged in the provision of ice cream and tea. The Company is a national chain brand, and its main products include ice cream, tea, milk tea, real fruit tea, coffee and others. The Company mainly operates its businesses in the domestic market.

Expecting more consumption measures. President Xi Jinping recently emphasized the need to “fully unleash” China’s consumption potential as a key driver of economic growth amid ongoing trade tensions with the United States. According to media, Xi underscored that revitalizing consumer demand, expanding domestic markets, and improving investment efficiency are now national priorities. He added that strengthening consumption is essential to accelerating the domestic economic cycle and sustaining momentum in the world’s second-largest economy. Furthermore, China also recently unveiled a “Special Action Plan to Boost Consumption”, reinforcing its commitment to stimulating domestic demand. The expectations of more consumption stimulus in the near term will likely positively benefit consumer groups like Mixue.

Insulation from the trade war. As of FY24, Mixue Bingcheng operated a total of 46,479 stores globally, with approximately 90%—or around 41,584 outlets—located in China. The company has established a broad footprint across all 31 provinces, autonomous regions, and municipalities, covering over 300 cities across all tiers. The remaining 10%, or roughly 4,895 stores, are situated in 11 overseas markets, primarily within the Asia-Pacific region, including Indonesia, Vietnam, and Malaysia. Given Mixue’s predominantly China-centric operations, with limited exposure to the U.S. market, the company remains largely shielded from the direct impacts of the U.S.-China trade war—offering a degree of geopolitical insulation for investors.

Increasing presence. As of late 2024, Mixue Bingcheng emerged as the world’s largest food and beverage chain by store count, operating over 46,000 stores globally—surpassing McDonald’s and Starbucks, which have approximately 43,000 and 40,000 outlets respectively. This strong expansion strategy highlights Mixue’s rapid scalability, driven by its highly efficient, low-cost franchise model and strong brand resonance across both urban centers and lower-tier cities. The company also recently went public on the Hong Kong Stock Exchange, raising about $444 million and achieving a valuation exceeding $10 billion. This also allows the company more opportunities to further expand their presence globally.

FY24 earnings. Revenue increased by 22.3% YoY to RMB24.8bn in FY24, compared to RMB20.3bn in FY23. Profit increased by 39.8% to RMB4.45bn in FY24, compared to RMB3.19bn in FY23. Basic earnings per share was RMB12.32 in FY24, compared to a basic earnings per share of RMB8.71 in FY23, representing an increase by 41.4% YoY.

Market consensus.

(Source: Bloomberg)

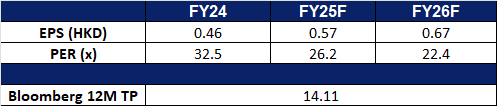

Weilong Delicious Global Holdings Ltd. (9985 HK): Plans to boost consumption levels

BUY Entry – 15.0 Target – 17.0 Stop Loss – 14.0

Weilong Delicious Global Holdings Ltd is a China-based holding company principally engaged in the production and sales of spicy snack foods. The Company operates in three segments: Seasoned Flour Products segment, Vegetable Products segment and Bean-based and Other Products segment. The Seasoned Flour Products segment mainly includes Big Latiao, Mini Latiao, Spicy Hot Stick, Mini Hot Stick and Kiss Burn. The Vegetable Products segment mainly includes Konjac Shuang and Fengchi Kelp. The Bean-based and Other Products segment mainly includes Soft Tofu Skin, 78° Braised egg and meat products.

Plans to Boost Consumption. China recently unveiled a “Special Action Plan to Boost Consumption”, reinforcing its commitment to stimulating domestic demand. The plan aims to drive consumption growth, expand household spending power, and enhance purchasing capacity by raising incomes and reducing financial burdens. This follows Premier Li Qiang’s recent government work report, which identified consumption growth as the country’s top economic priority for the year. Key measures include employment support initiatives, enhanced unemployment benefits, and targeted income-boosting efforts for both urban and rural residents, including farmers. Beyond short-term stimulus, the plan signals China’s resolve to tackle structural challenges such as stagnant wage growth, negative wealth effects from property and stock market downturns, and an inadequate social safety net. Furthermore, China will also place greater emphasis on domestic consumption as a key driver of economic growth this year, aiming to counterbalance the effects of softer external demand resulting from higher tariffs imposed by the Trump administration. The expected rise in consumption level could have a positive impact on Weilong Delicious Global Holdings, as stronger domestic demand may support the company’s growth.

Partnership with KFC. Earlier this year, Weilong Delicious has partnered with KFC to launch a co-branded “Spicy Strip Flavor Large Chicken Strips,” capitalizing on the fast-food chain’s popular “Crazy Four” promotion to engage young consumers. This collaboration follows previous partnerships with Pizza Hut and Xiaolongkan Hotpot, reinforcing Weilong’s strategy of leveraging fast-food platforms to enhance brand visibility and product appeal. By prioritizing genuine product innovation and aligning with fast-food consumption trends, Weilong aims to translate marketing buzz into sustained consumer engagement. This approach reflects shifting dynamics in China’s consumer market, where brands must focus on core customer segments and product differentiation rather than broad, awareness-driven marketing campaigns to drive long-term growth.

FY24 results review. Revenue increased by 8.6% YoY to RMB6.27bn in FY24, compared with RMB4.87bn in FY23. Net profit increased by 21.3% to RMB1,068.5bn in FY24, compared to RMB880.3mn in FY23. EPS rose to RMB0.46 in FY24 compared with RMB0.38 in FY23. The company also announced a final dividend of RMB0.11 per share and a special dividend of RMB0.18 per share for FY24.

Market consensus.

(Source: Bloomberg)

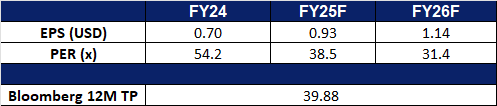

Carmax Inc (KMX US): Benefitting from implementation of tariffs

CarMax, Inc. retails automobiles. The Company offers used cars, vans, electric vehicles, and light trucks, as well as provides rental, maintenance, post warranty repairs, mechanical and painting work, diagnosis insurance, valuation, and security services. CarMax serves customers in the United States.

Auto tariffs benefit. Trump’s 25% auto tariffs, set to take effect on April 2nd, are prompting consumers to accelerate vehicle purchases to avoid price increases. Dealerships are reporting increased customer traffic, with used car inquiries up 16% on Dealer.com and new car demand surging 54%. This surge in demand benefits CarMax, as more consumers turn to the used car market to navigate new car price uncertainties. Higher demand will boost CarMax’s sales volume, profit margins, and profitability, further solidifying its market position in a rising cost environment.

3Q25 performance. Net sales increased by 1.1% YoY to US$6.22bn, exceeding expectations by US$170mn. GAAP earnings per share were US$0.81, beating estimates of US$0.60. This was primarily driven by a 5.4% increase in retail used vehicle unit sales and a 6.3% growth in wholesale unit sales. CarMax Auto Finance revenue also increased by 7.6%, and the company repurchased US$114.8mn worth of shares. Despite a decrease in average retail prices, the increase in sales volume successfully offset the impact. CarMax’s focus on digital expansion and cost management, coupled with expected continued improvement in sales volume, will help drive revenue growth.

3Q25 results. Revenue increased by 1.1% YoY to US$6.22bn, exceeding expectations by US$170mn. GAAP earnings per share were US$0.81, exceeding expectations by US$0.20.

Market consensus

(Source: Bloomberg)

Philip Morris International Inc (PM US): Zyn-ergy in action

Philip Morris International Inc. operates as a tobacco company working to deliver a smoke-free future and evolving its portfolio for the long term to include products outside of the tobacco and nicotine sector. The Company offers cigarettes, e-vapor, and oral smoke-less products. Philip Morris International serves customers worldwide.

Signs of recession benefitting defensive stocks. Recent U.S. macroeconomic data shows that inflation remains high, while the labour market is beginning to cool, and consumer spending and confidence are declining. Trump’s tariff policy has triggered a global trade. With the concentration of negative factors, the market is averse to uncertainty, so major growth sectors have seen significant corrections, and funds have rotated to stronger defensive sectors.

Potential sale of business. Philip Morris (PM) International’s decision to explore the sale of its U.S. cigar business aligns with its broader strategy to transition away from traditional tobacco products. By divesting this asset, the company can reallocate resources toward its growing smoke-free product portfolio, such as Zyn nicotine pouches and IQOS heated tobacco devices. This shift not only supports long-term revenue growth but also enhances PM’s positioning in the evolving nicotine market. The expected US$1bn sale proceeds could fund further innovation and expansion, accelerating its goal of achieving two-thirds of sales from smoke-free products by 2030.

Decline in smoking rates. With global smoking rates continuing to fall due to health concerns and regulatory pressures, PM’s pivot toward alternative nicotine products is a crucial move. Traditional cigarettes face declining demand, but the company’s strong performance in Zyn and IQOS demonstrates its ability to adapt to changing consumer preferences. By focusing on harm-reduction alternatives, PM ensures revenue stability despite a shrinking cigarette market. This proactive approach not only mitigates risks associated with declining smoking trends but also strengthens the company’s position as an industry leader.

FDA approved. The FDA’s authorization of Zyn nicotine pouches marks a major milestone for PM, validating its harm-reduction strategy and providing a competitive edge in the U.S. market. With official regulatory backing, PM can further promote Zyn as a safer alternative to traditional tobacco, attracting more adult smokers looking to switch. This approval also opens doors for expansion into other regions where similar regulatory acceptance could drive growth. As health-conscious consumers seek alternatives, PM is well-positioned to capitalize on the increasing demand for smokeless nicotine products.

4Q24 results. Revenue grew 7.3% YoY to US$9.71bn, beating estimates by US$270mn. Non-GAAP EPS was US$1.55, beating expectations by US$0.05. The company projected FY25 adjusted annual earnings per share in the range of US$7.04 to US$7.17, above analysts’ estimate of US$7.03. It also forecast ZYN shipments to the U.S. would rise by between 34% and 41% in 2025, while IQOS shipments would also see between 10% and 12% growth.

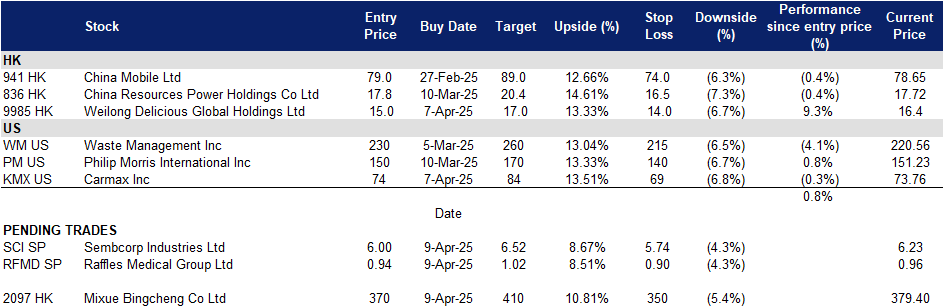

Trading Dashboard Update: Add Q&M Dental Group Ltd (QNM SP) at S$0.285, China Telecom Corp Ltd (728 HK) at HK$6, Weilong Delicious Global Holdings Ltd (9985 HK) at HK$15 and Carmax Inc (KMX US) at US$74. Cut loss on DBS Group Holdings Ltd (DBS SP) at S$42, Food Empire Holdings Ltd (FEH SP) at S$1.29, Sasseur REIT (SASSR SP) at S$0.64, Raffles Medical Group Ltd (RFMD SP) at S$0.92, Sembcorp Industries Ltd (SCI SP) at S$6.27, Jiangxi Copper Co Ltd (358 HK) at HK$13, PICC Property & Casualty Co Ltd (2328 HK) at HK$13.5, Hong Kong Exchanges and Clearing Ltd (388 HK) at HK$330, Pop Mart International Group (9992 HK) at HK$145, Q&M Dental Group Ltd (QNM SP) at S$0.27, China Telecom Corp Ltd (728 HK) at HK$5.6, Celsius Holding Inc (CELH US) at US$33 and Singapore Airlines Ltd (SIA SP) at S$6.