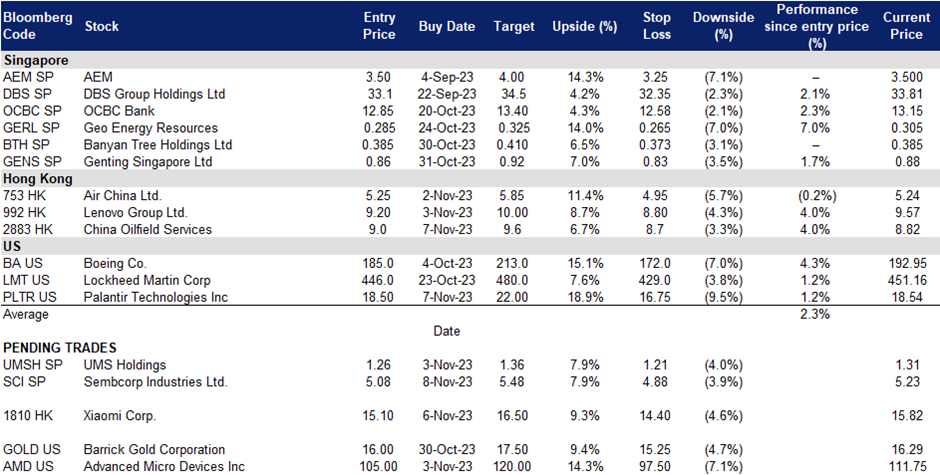

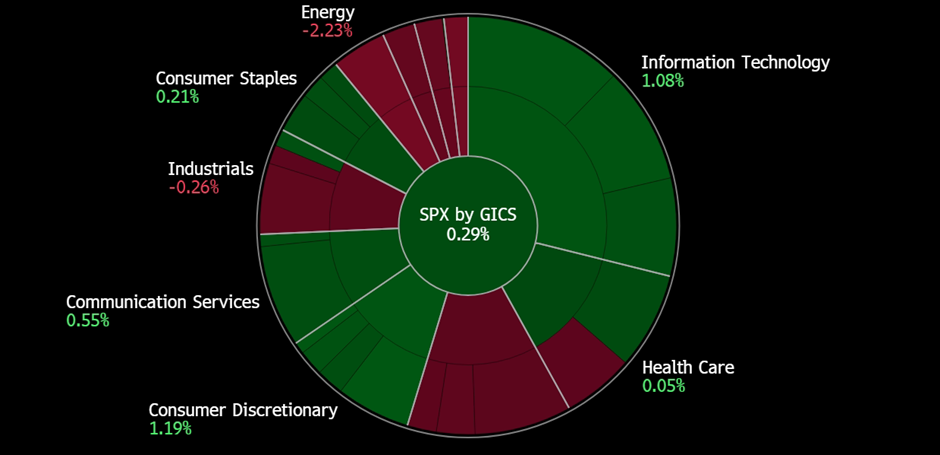

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

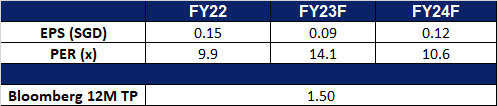

UMS Holdings (UMSH SP): Expect better 3Q23 earnings

- RE-ITERATE BUY Entry 1.26 – Target – 1.36 Stop Loss –1.21

- UMS Holdings Limited provides equipment manufacturing and engineering services to Original Equipment Manufacturers (OEMs) of semiconductors and related products. The Company manufactures high precision components and complex electromechanical assembly and final testing services. UMS supports the electronic, machine tools and oil and gas industries.

- Semiconductor sector is bottoming out. The milestone development of artificial intelligence (AI) in 1H23 not only buffers the downcycle of the semiconductor sector but also kickstarts a new growth engine. The AI hype shadows the fall in demand for mobile/PC chips due to the normalisation of life and the drop in capex due to geopolitical factors. However, several market leaders projected that the sector will bottom out in 2H23 or 1H24 as both orders and capex will gradually recover. In the UMS’s 2Q23 press release, according to SEMI, global 300mm fab equipment spending for front-end facilities next year is expected to begin a growth streak to hit a US$119 billion record high in 2026 following a decline in 2023.

- Upbeat 2024 outlook from the upstream. Advanced Micro Devices’s 3Q23 results topped market estimates. Meanwhile, it predicted that the data center GPU revenue would exceed US$2bn in 2024. Samsung Electronics reported its 3Q23 as most profitable quarter in 2023, and it mentioned that smartphone and PC demand is poised to rebound amid the coming replacement cycle. AI theme will remain a key investment thesis in 2024, driving related segments to grow.

- Applied Materials 3Q23 review. Applied Materials (AMAT US) is a key customer to UMS. Its 3Q23 revenue dropped 1.4% YoY to US$6.3bn, beating estimates by US$250mn. 3Q23 Non-GAAP EPS was US$1.9, beating estimates by US$0.15. It expects 4Q23 net sales to be approximately US$6.51bn, plus or minus US$400 mn, compared to a consensus of US$5.87bn. 4Q23 Non-GAAP adjusted diluted EPS is expected to be in the range of US$1.82 to US$2.18, compared to a consensus of US$1.60. AMAT will be releasing its 4Q23 earnings on 16 November.

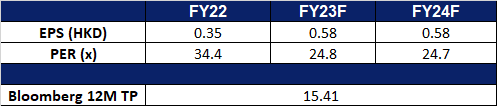

- 2Q23 results review. Revenue fell 14% YoY to S$74.4mn. Gross material margin decreased to 46.3% from 51.7%. PATMI plugged 42% YoY to S$11.6mn. Net margin fell to 15.4% from 23.2%. The new plant in Penang is expected to contribute at least US$30mn for FY24. The company declared an interim dividend of 1.2 SG cents. UMS will be releasing its 3Q23 earnings on 14 November.

- Market Concensus.

(Source: Bloomberg)

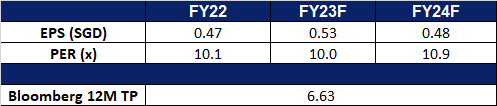

Sembcorp Industries Ltd. (SCI SP): The green transition

- BUY Entry 5.08 – Target – 5.48 Stop Loss – 4.88

- Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

- Investing in renewables. Sembcorp Industries recently announced plans to invest about S$10.5bn in renewables as part of its 2023-2028 strategic plan. This substantial investment will account for 75% of the company’s total investments from 2024 to 2028. Sembcorp aims to grow its installed renewable capacity to 25 gigawatts (GW) by 2028, building upon its current 12 GW capacity, which represents 61% of its energy portfolio. The company also targets a 50% reduction in emission intensity and intends to focus on hydrogen assets, decarbonisation solutions, and integrated urban solutions for the remaining investment allocation. Sembcorp will continue to use gas as a transitional fuel to support its renewable growth and invest in low-carbon energy and hydrogen technologies. Its comprehensive 5-year plan will help to achieve its goal of halving its emission intensity by 2028.

- Retrofit Sakra cogen plant. Sembcorp Industries is collaborating with IHI Corporation and GE Vernova’s Gas Power business to retrofit its Sakra power plant in Singapore with ammonia-firing capabilities. This initiative aims to decarbonise the power plant operations and potentially generate low-carbon energy. This project builds upon a separate cooperation between IHI and GE Vernova to develop a retrofittable, 100% ammonia-capable combustion system, compatible with specific GE Vernova turbine models. This effort supports the transition to carbon-free combustion fuels like ammonia, aligning with the growing interest in sustainable alternatives in the energy sector, such as ammonia and hydrogen. It also facilitates the retrofitting of existing power generation facilities for reduced carbon emissions.

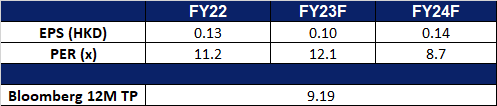

- 1H23 results review. Revenue fell 6% YoY to S$3.7bn. Net profit rose 56% YoY to S$608mn, due to contributions from a deferred payment note arising from the sale of its Indian unit and its Conventional Energy and Renewables segments. Its renewables segment’s revenue grew 71% YoY to S$379mn.

- Market Consensus.

(Source: Bloomberg)

Xiaomi Corp. (1810 HK): More new products to boost sales

- BUY Entry – 15.1 Target – 16.5 Stop Loss – 14.4

- XIAOMI CORPORATION is a China-based investment holding company principally engaged in the research, development and sales of smartphones, Internet of things (IoTs) and lifestyle products, the provision of Internet services, and investment business. The Company mainly conducts its businesses through four segments. The Smartphone segment is engaged in the sales of smartphones. The IoT and Lifestyle product segment is engaged in the sales of other in-house products, including smart televisions (TVs), laptops, artificial intelligence (AI) speakers and smart routers; ecosystem products, including IoT and other smart hardware products, as well as certain lifestyle products. The Internet service segment is engaged in the provision of advertising services and Internet value-added services. The Others segment is engaged in the provision of repair services for its hardware products. The Company distributes its products in domestic market and to overseas markets.

- Surging sales of Xiaomi 14 and 14Pro. Xiaomi just released it Xiaomi 14 and 14Pro last week, marking them as the world’s first smartphones powered by the Snapdragon 8 Gen 3 chipset. The Xiaomi 14 series broke the company’s previous year’s record on all its major Chinese online retail platforms, selling out within the first four hours of its initial sales. Consumers were attracted to the series 14 impressive design, the enhanced iteration of the Xiaomi 13 series, the incorporation of the Snapdragon 8 Gen 3 chipset, and the introduction of the all-new HyperOS user experience, alongside having a Leica-optimized Light Hunter 900 primary camera in addition to a unique Leica Summilux lens, providing a high-quality photography experience.

- Integration of new operating system. Xiaomi announced recently its new operating system, the Xiaomi HyperOS. This operating system is made available to consumers together with the sales of Xiaomi’s latest phone, the 14 series, as well as other latest wearables and TV sets in China on 31st Oct 23. This shift into a new operating system also marks a strategic move of the company’s vision into creating a seamless smart ecosystem, “Human x Car x Home”. This ecosystem is bound to entice consumers to purchase Xiaomi’s other products as well.

- Tapping into the EV market. As part of the company’s effort to create a seamless ecosystem, the company has engaged with several carmakers about possible partnerships to build EVs. The company has also recently secured approval from the National Development and Reform Commission (NDRC) to manufacture 100,00 vehicles annually, marking a major milestone for the company’s venture into EV manufacturing. Xiaomi’s founder, Lei Jun has also previously announced an investment of $10bn into the EV space over the next ten years, and aims to mass produce its first cars by 1H2024.

- 2Q23 earnings. Revenue fell 4.0% YoY to RMB67.4bn in 2Q23, compared with withRMB70.2bn in 2Q22. Adjusted Net profit was RMB5.14bn in 2Q23, increasing 147% YoY compared to RMB2.08bn in 2Q22. Basic earnings per share was RMB0.15 in 2Q23, compared to RMB0.06 in 2Q22.

- Market Consensus.

(Source: Bloomberg)

Lenovo Group Ltd. (992 HK): Tap intp AI

- RE-ITERATE BUY Entry – 9.20 Target – 10.00 Stop Loss – 8.80

- Lenovo Group Limited is an investment holding company principally engaged in personal computers and related businesses. The Company’s main products include Think-branded commercial personal computers and Idea-branded consumer personal computers, as well as servers, workstations and a family of mobile Internet devices, including tablets and smart phones. The Company operates its business through four geographical segments, including China, Asia Pacific (AP), Europe, the Middle East and Africa (EMEA) and Americas (AG). The Company also provides cloud service and other related services. The Company distributes its products in domestic market and to overseas markets.

- Partnership with Nvidia. Lenovo and NVIDIA have expanded their partnership to develop new hybrid AI solutions and collaborate on engineering. This partnership aims to bring the power of generative AI to every enterprise. Working closely with NVIDIA, Lenovo will deliver fully integrated systems that bring AI-powered computing to the edge and cloud, where data is created. This will make it easier for businesses to deploy tailored generative AI applications to drive innovation and transformation across all industries.

- New product on sales. Lenovo has just placed the ThinkPad X1 Fold 16” folding laptop on sales, more than a year after announcing the product. The ThinkPad X1 Fold 16” features an impressive 16.3-inch foldable Samsung OLED display, sporting a resolution of 2024 x 2560 pixels, and when folded, the device transforms into a 12-inch display, and it can be seamlessly paired with a Bluetooth keyboard, delivering a laptop-like experience. This product is bound to attract consumers to prefer a convenient yet big tablet that provides the same experience as using a laptop.

- Tapping into the India Market. Lenovo is amongst the 100 firms that are authorised by India to import electronic devices such as laptops, tablets, and personal computers under a new system aimed at monitoring shipments. Other companies include Apple, Dell, HP, Samsung etc. These companies must register the quantity and value of imports on a portal, with an authorisation valid until September 2024. This allows Lenovo to tap into the India market, possibly adding another source of revenue from India.

- 1Q24 earnings. Revenue fell 24.0% YoY to US$12.90bn in1Q24, compared with US$17.0bn in 1Q23. Net profit was US$191mn in 1Q23, dropping 66% YoY comparing to US$556mn in 1Q23. Basic earnings per share was US 1.48 cents in 1Q24, compared to US4.39 cents in 1Q23.

- Market Consensus.

(Source: Bloomberg)

Palantir Technologies Inc (PLTR US): Upbeat outlook

- BUY Entry – 18.50 Target – 22.0 Stop Loss – 16.75

- Palantir Technologies Inc. develops software to analyze information. The Company offers solutions support many kinds of data including structured, unstructured, relational, temporal, and geospatial. Palantir Technologies serves customers worldwide.

- Raised guidance. Palantir reported strong Q3 earnings, exceeding expectations, and raised its full-year revenue guidance. US commercial revenue grew 33% YoY (52% growth without specific contracts), and the customer count rose by 37% YoY, from 132 to 181. Palantir’s investment in AI Platform (AIP) is yielding quick results through boot camps, and its government products remain essential in the geopolitical landscape. The company raised its revenue guidance for Q4 and FY23. Notably, the 33% YoY growth in US commercial sector revenue to $116 million signifies a shift from relying on government contracts. These have boosted investor confidence in Palantir.

- Possible inclusion into S&P 500. This quarter’s profitability marks Palantir’s fourth consecutive profitable quarter, positioning it as a potential candidate for inclusion in the S&P 500 index. Its CEO acknowledged this milestone, highlighting the company’s commitment to profitability while maintaining its broader business growth ambitions.

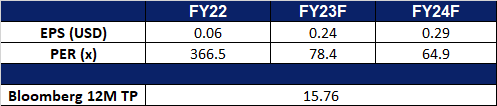

- 3Q23 earnings review. Revenue rose by 16.8% YoY to US$558mn, beating estimates by US$2.08mn. Non-GAAP EPS was US$0.07, beating estimates by US$0.01. It raised revenue guidance for FY23 to be between US$2.216bn – US$2.220bn vs. the consensus of US$2.21B.

- Market consensus.

(Source: Bloomberg)

Advanced Micro Devices Inc (AMD US): AI progression

- RE-ITERATE BUY Entry – 105.0 Target – 120.0 Stop Loss – 97.5

- Advanced Micro Devices, Inc. (AMD) produces semiconductor products and devices. The Company offers products such as microprocessors, embedded microprocessors, chipsets, graphics, video and multimedia products and supplies it to third-party foundries, as well as provides assembling, testing, and packaging services. AMD serves customers worldwide.

- Further AI developments are to be announced. AMD will be holding an Advancing AI Event on December 6, featuring its products and partnerships related to AI development. The event will be live-streamed on their website.

- Increase in AI chip sales. AMD reported strong Q3 performance with revenue growth in the server CPU and Ryzen processor segments. The company is focusing on enhancing its AI capabilities and foresees robust growth in the Data Center and Client segments, projecting Q4 revenue of around $6.1 billion. In addition, AMD is targeting the AI market with the MI300X chip to compete with Nvidia and expects $2 billion in sales from it in 2024. However, these estimates could face challenges due to recent restrictions and potentially more stringent bans enforced by the US Department of Commerce, prohibiting the sale of advanced AI chips to China. While chip manufacturers have indicated that the impact will likely be minimal, this issue remains a source of concern for certain investors.

- Acquired AI software. AMD acquired Nod.ai, an artificial intelligence startup, as part of its strategy to strengthen its software capabilities and compete with Nvidia. Nvidia has established itself as a dominant force in the AI chip market through its software and developer ecosystem. AMD aims to invest in building unified software to support its range of chips. The Nod.ai acquisition aligns with the strategy, as its technology facilitates the deployment of AI models optimised for AMD’s chips. AMD has been growing its AI group with plans for further expansion and potential future acquisitions.

- ROCm vs CUDA. AMD is emphasising its commitment to evolving its software stack, ROCm, in the competitive AI chip market, recognising that software development is a journey. The company has made ROCm a top priority and created a new organisation to consolidate its software assets. This effort includes acquiring companies like Mipsology and expanding its talent pool. AMD has also established an internal AI models group to strengthen its software expertise. It uses open-source solutions like Triton to challenge Nvidia’s CUDA and offer alternatives for developers, emphasising the importance of open-source collaboration. AMD’s ROCm stack aims to allow the community to contribute and bridge the gap in software maturity. They have MI300 and MI300X AI chips with samples currently with customers and are focused on the success of ROCm in supporting these offerings.

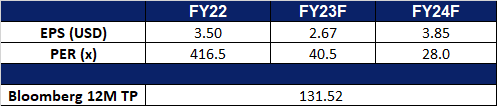

- 3Q23 earnings review. Revenue rose by 4.1% YoY to US$5.8bn, beating estimates by US$110mn. Non-GAAP EPS was US$0.70, beating estimates by US$0.02. Revenue from the data centre segment remained flat, whereas the client segment saw an increase, followed by a decline in both the embedded and gaming segments.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: Add China Oilfield Services (2883 HK) at HK$9 and Palantir Technologies Inc (PLTR US) at US$18.5. Cut loss on Shandong Gold Mining (1787 HK) at HK$14.3.