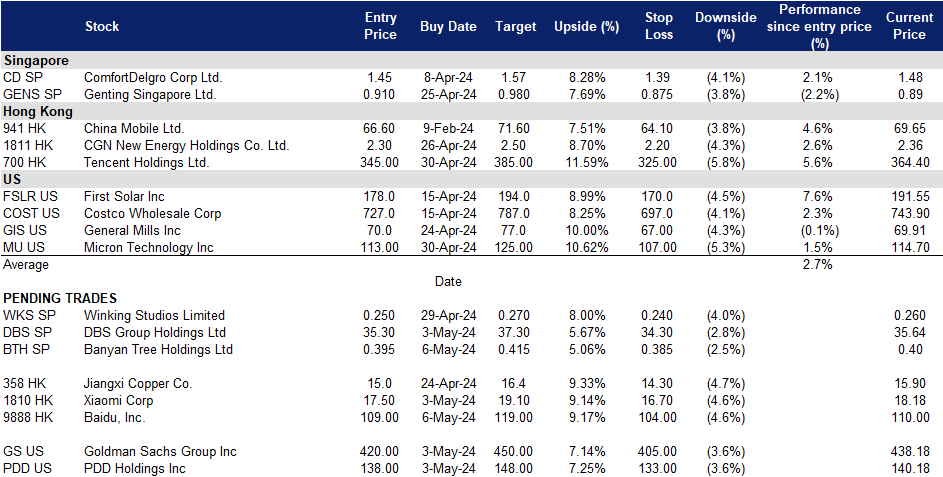

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

Hong Kong

Banyan Tree Holdings Ltd (BTH SP): Growth in sustainability efforts

- BUY Entry – 0.395 Target– 0.415 Stop Loss – 0.385

- Banyan Tree Holdings Limited operates as a holding company. The Company, through its subsidiaries, owns and manages hotel groups. The Company focuses on hotels, resorts, spas, galleries, golf courses, and residences, as well as provides investments, design, construction, and project management services. Banyan Tree Holdings serves customers worldwide.

- Secured new sustainable loan. Banyan Tree secured its first sustainability-linked loan worth S$70 million, led by Maybank, with support from the Bank of India and Hua Nan Commercial Bank. The loan reflects Banyan Tree’s commitment to responsible tourism and decarbonization, following its financial recovery from the pandemic. In FY23, the group saw a 23% increase in property sales from branded residences and extended-stay segments. Maybank emphasizes the need for timely and flexible financial solutions amid changing market conditions, highlighting its substantial mobilization in sustainable finance.

- Success in joint venture. Banyan Tree Residences Creston Hill, the inaugural luxury branded residences near Khao Yai National Park, celebrated the success of its presales phase valued at THB17bn. Managed by Banyan Tree in partnership with Creston Holding Ltd., the venture reflects a rising demand for upscale residences in Thailand. With presales surpassing THB1bn, its Managing Director anticipates increased interest with the unveiling of fully furnished display units. The project caters to the growing trend of luxury living amidst nature, appealing to permanent residents and holidaymakers. The strategic location, near the upcoming Motorway 6, enhances accessibility. The development offers 21 pool villas and 16 condominium buildings, designed to blend seamlessly with the serene landscape. Future phases will introduce additional villas and condominiums. Buyers benefit from Banyan Tree’s exclusive owner programme, “The Sanctuary Club,” granting privileges across global properties. Situated just 200km from Bangkok, Khao Yai offers diverse activities, making Creston Hill an ideal second home. The on-site sales gallery welcomes prospective buyers with exclusive promotions during the presales period.

- 30th anniversary new launches. Banyan Tree announced a robust pipeline of 19 new property openings. Under the new corporate brand umbrella, Banyan Group, the company expanded beyond its luxury offerings with brands like Angsana, Cassia, and Dhawa. New destinations include Japan, Saudi Arabia, Vietnam, and South Korea. Sustainability commitments include a 2030 Sustainability Roadmap aligned with UN targets. Laguna Lakelands in Phuket promises immersive living with nature-integrated development. New initiatives include Beyond, a digital companion for holistic experiences, and withBanyan, an experiential members program.

- Segmental split. Banyan Group previously announced plans to split its hotel and property development segments into separate companies to boost investor confidence. Chairman Ho Kwon Ping revealed the restructuring plan, aiming to simplify the company’s complex business model and unlock value. The move comes as the company’s stock performance lags, down 85% from its peak in 2007. The pandemic accelerated the need for restructuring, with a focus on selectively developing properties in Thailand and expanding hotel management globally. Despite recent losses due to COVID-19, the company anticipates growth, with plans to reach 100 hotels by year-end. The property development arm remains a unique strength, offering quicker returns compared to hotel ownership. Banyan’s residential projects aim to tap into strong demand for homes, positioning the company for future growth while maintaining a focus on its home market.

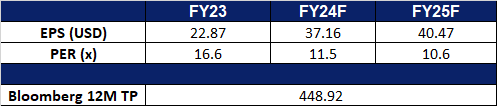

- FY23 results review. FY23 revenue inclined by 21% to S$327.9mn. Net profit rose significantly to S$31.7mn, compared to S$767,000 in FY22. FY23 operating profit more than doubled to S$90.1mn. It declared a final dividend of S$0.012 for FY23.

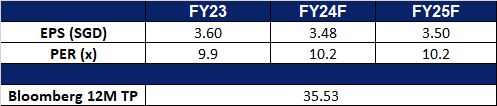

- Market Consensus

(Source: Bloomberg)

DBS Group Holdings Ltd. (DBS SP): Increase shareholders returns

- RE-ITERATE BUY Entry – 35.30 Target– 37.30 Stop Loss – 34.30

- DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

- Increasing business momentum. DBS just announced its results exceeding the market expectations. Loans grew and both fee income and treasury customer sales reached new highs, showcasing the strength and momentum of the company’s business. ROE reached a record high of 19.4% compared to 18.6% a year ago, and the net interest margin edged up to 2.14%, compared to 2.12% a year ago.The company remains optimistic that total income and earnings will be better than previously guided and the company would be able to deliver another year of strong shareholder returns.

- Bonus share issuance. DBS paid out its Q4 final dividend amounting to 54 Singapore cents per share on 19 April. DBS also issued one bonus share for every 10 shares held on 30 April and these shares will qualify for dividends from 1Q24. The increase in dividend payout and issuance of bonus shares is to increase capital returns to its shareholders.

- Expectations of monetary policy to remain unchanged. The Monetary Authority of Singapore (MAS) is expected to maintain its current monetary policy in the upcoming review. Despite inflation showing some volatility, core inflation remains above the central bank’s target. MAS may consider easing monetary settings in the second half of the year if inflation stabilizes. While inflation in Singapore remains elevated, forecasts suggest moderation throughout the year. Global central banks are cautiously adjusting interest rates, and MAS is likely to follow suit gradually, balancing growth and inflation concerns. Analysts suggest MAS may not rush to relax policy, considering Singapore’s role as a bellwether for global growth and the ongoing export-driven economic recovery. Policy easing, if any, is anticipated in October at the earliest, with MAS managing monetary policy through adjustments to the Singapore dollar’s exchange rate against its main trading partners. With the monetary policy expected to remain unchanged, DBS will continue to benefit from the high net interest margins for the coming quarters, allowing it to maintain its FY23 net interest income levels.

- New sustainability initiative. On 3 April, DBS Bank and Enterprise Singapore launched a program to support local companies in becoming more sustainable. The initiative offers training, guidance, and financing options to SMEs and mid-cap companies, with around 100 expected to join the first cohort. Companies will receive support from sustainability specialists and can choose basic or intermediate training levels. By the end of the program, participating firms should have a clear sustainability action plan. Enterprise Singapore will finance 70% of eligible activities per company until March 2026. The initiative aims to help businesses future-proof themselves, cut costs, and meet the growing demand for sustainability.

- 1Q24 results review. 1Q24 total income rose by 12.6% YoY to S$5.56bn, compared to S$4.94bn in 1Q23. Net profit increased 15.0% YoY to S$2.96bn in 1Q24, compared to S$2.57bn in 1Q23. Basic EPS rose to S$4.57 in 1Q24 compared to S$3.65 in 1Q23.

- Market Consensus

(Source: Bloomberg)

Baidu, Inc. (9888 HK): To benefit from deal with Tesla

- BUY Entry – 109 Target –119 Stop Loss – 104

- Baidu Inc is a Chinese language Internet search provider. The Company offers a Chinese language search platform on its Baidu.com Website that enables users to find information online, including Webpages, news, images, documents and multimedia files, through links provided on its Website. The Company operates through two segments, Baidu Core segment and iQIYI segment. Baidu Core mainly provides search-based, feed-based, and other online marketing services, as well as products and services from the Company’s new artificial intelligence (AI) initiatives. Within Baidu Core, the Company’s product and services offerings are categorized as Mobile Ecosystem, Baidu AI Cloud and Intelligent Driving & Other Growth Initiatives. iQIYI is an online entertainment service provider that offers original, professionally produced and partner-generated content on its platform.

- Partnership with Tesla. Baidu has recently finalized an agreement with Tesla, granting the car manufacturer access to its mapping license for data collection on China’s public roads. This agreement marks the resolution of a key regulatory requirement for Tesla’s driver assistance system, known as Full Self Driving (FSD), to be introduced in China. Under the terms of the deal, Baidu will also supply its lane-level navigation system to Tesla. With the mapping service license in place, Tesla gains the legal authorization to deploy its FSD software on Chinese roads, allowing its vehicle fleets to collect data on road configurations, traffic signals, and surrounding infrastructure.

- 1st in AI patent application. Baidu maintains its top position in national rankings for artificial intelligence patent applications and authorizations, demonstrating its commitment to fostering technological innovation and advancing new productive forces. By the end of 2023, the company had submitted 19,308 AI-related patent applications and received 9,260 patents, securing its leading position among domestic tech firms for six consecutive years, as reported. Additionally, Baidu leads in patents for AI-powered large language models, with 869 applications and 317 patents granted in this field.

- Release of new AI tools. Baidu recently unveiled user-friendly AI tools enabling individuals without coding expertise to develop specialized generative AI-driven chatbots tailored for specific purposes. These chatbots can seamlessly integrate into websites, Baidu search results, and various online platforms. The basic Baidu tools are accessible for experimentation at no cost, subject to a usage threshold. Additionally, Baidu introduced three new iterations of its Ernie AI model – dubbed “Speed,” “Lite,” and “Tiny” – providing developers with selective access based on the complexity of their projects. These supplementary AI tools are poised to draw in a broader audience for Baidu. The company’s “Ernie bot,” has also amassed over 200mn users, with its application programming interface (API) being utilized 200mn times daily. Additionally, the chatbot has garnered 85,000 enterprise clients. In 4Q2023, Baidu generated significant revenue, totaling several hundred million yuan, by leveraging AI to enhance its advertising services and assist other companies in constructing their own models.

- FY23 earnings. Revenue increased by 8.8% YoY to RMB134.6bn in FY23, compared to RMB123.7bn in FY22. Non-GAAP Net income rose by 39.0% to RMB28.7bn in FY23, compared to RMB20.7bn in FY22. Non-GAAP diluted earnings per share rose to RMB80.85 in FY23, compared to RMB58.93 in FY22.

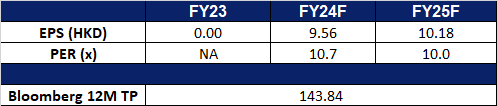

- Market consensus.

(Source: Bloomberg)

Xiaomi Corp. (1810 HK): Strengthening market position

- RE-ITERATE BUY Entry – 17.5 Target –19.1 Stop Loss – 16.7

- Xiaomi Corp is a China-based investment holding company principally engaged in the research, development and sales of smartphones, Internet of things (IoTs) and lifestyle products, the provision of Internet services, and investment business. The Company mainly conducts its businesses through four segments. The Smartphone segment is engaged in the sales of smartphones. The IoT and Lifestyle product segment is engaged in the sales of other in-house products, including smart televisions (TVs), laptops, artificial intelligence (AI) speakers and smart routers; ecosystem products, including IoT and other smart hardware products, as well as certain lifestyle products. The Internet service segment is engaged in the provision of advertising services and Internet value-added services. The Others segment is engaged in the provision of repair services for its hardware products. The Company distributes its products in domestic market and to overseas markets.

- Strong Smartphone sales. In 1Q24, Xiaomi maintained its position as the world’s third-largest smartphone vendor by shipments. With 40.7 million smartphone units shipped, Xiaomi held a 14% market share, trailing behind Samsung, which shipped 60 million units (20% market share), and Apple, which shipped 48.7 million units (16% market share). Xiaomi’s impressive performance was propelled by robust shipments of its latest models in the Middle East, Africa, and Latin America markets. Additionally, the company’s strategic focus on technological advancements, such as its HyperOS technology aimed at integrating multiple systems into a single ecosystem, has contributed to its strong market performance and efforts to capture a larger market share.

- Better turnarounds on EV business. Xiaomi has ventured into the electric vehicle (EV) market with the launch of its new EV car. The sales of the new EV SU7 surpassed expectations, bringing the company closer to breaking even, despite offering it at a lower price point compared to Tesla’s Model 3. Xiaomi now aims to deliver 100,000 units of its new EV this year, targeting an estimated gross profit margin of approximately 5% to 10% for its auto business. This outlook is reinforced by cost reductions from suppliers. Moreover, Xiaomi is currently engaging in discussions with supply chain partners to explore ways to increase production capacity and further streamline costs to support its EV venture.

- Further Integration of new operating system. Xiaomi has been focusing on extending its new operating system, the Xiaomi HyperOS to more Xiaomi and Redmi devices and products. HyperOS is expected to power not only smartphones but also smart home devices and even electric vehicles like the new Xiaomi SU7. With the launch of the new Xiaomi SU7 EV, customers can expects to gain a seamless experience in a new smart ecosystem between the EV and their phones. Under the new HyperOS operating system, the company has also been releasing several products, such as a ceiling fan as well as clothes dryer. This shift into a new operating system also marks a strategic move of the company’s vision into creating a seamless smart ecosystem, “Human x Car x Home”. This ecosystem is bound to entice consumers to purchase Xiaomi’s other products as well.

- FY23 earnings. Revenue fell by 3.2% YoY to RMB271.0bn in FY23, compared to RMB280.0bn in FY22. Net profit rose by 598.2% to RMB7.5bn in FY23, compared to RMB2.50bn in FY22. Basic earnings per share rose to RMB0.70 in FY23, compared RMB0.10 in FY22.

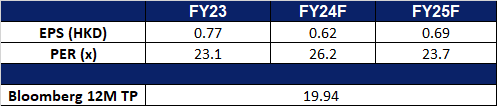

- Market consensus.

(Source: Bloomberg)

PDD Holdings Inc (PDD US): Temu staying on top

- Entry – 138 Target – 148 Stop Loss – 133

- PDD Holdings Inc. is a multinational commerce group that owns and operates a portfolio of businesses. The Company focuses on the digital economy so that local communities and small businesses can benefit from the increased productivity and new opportunities. PDD Holdings has built a network of sourcing, logistics, and fulfilment capabilities for its underlying businesses.

- Government to increase support. The Communist Party’s Politburo announced plans to enhance support for China’s economy through prudent monetary and proactive fiscal policies, including adjustments to interest rates and bank reserve requirement ratios (RRR). While the economy showed faster-than-expected growth in the first quarter, it still faces challenges. The Politburo highlighted structural issues such as insufficient demand and risks in key sectors, emphasizing the need for flexible policy tools. China aims for around 5% economic growth in 2024, necessitating additional stimulus measures. The government plans to issue ultra-long-term special treasury bonds and accelerate the issuance of local government special bonds to maintain fiscal expenditure intensity. Additionally, reforms will be a focal point, aiming to address economic imbalances and promote a pro-market environment. Efforts to stabilize the housing market and optimize policy measures for new housing are also underway. The emphasis on developing “new productive forces” underscores the importance of innovation in driving economic growth. Investors will continue to be influenced by how the Chinese government implements policies to address its underlying economic issues, with the recently announced economic reforms and stimulus measures seen improving investor sentiment.

- Change in consumer patterns. Amidst rising inflation, American consumers are increasingly favoring the Chinese e-commerce platform Temu, which boasts a 17% market share in the US market. Temu, owned by PDD Holdings offers a wide range of products at competitive prices and is the top shopping app on Apple’s app store, surpassing giants like Amazon and Walmart. With orders shipped from China, Temu is now expanding its presence in the US by opening its marketplace to local warehouses, aiming to compete with Amazon’s fast delivery. This disruption in the US market from changing consumer preferences and economic challenges has ultimately benefitted Temu.

- Continued global growth. In the first quarter of 2024, Korean consumers’ direct purchases from China reached a new quarterly high of 938.4bn won (US$677mn), driven by the popularity of Chinese e-commerce platforms like Temu and AliExpress. This marked a 54% YoY increase and accounted for 57% of total direct purchases. Overall, online cross-border shopping reached 1.65tn won, with the United States and the European Union also significant contributors. Additionally, online shopping transactions within Korea reached a record high of 59.68tn won in the first quarter, driven by increased demand for travel, transportation services, and food items during the Lunar New Year holiday. Purchases made through mobile devices also saw a significant increase. Amid shifting global consumer preferences towards e-commerce and a preference for affordable goods, Temu has effectively expanded its customer base and is poised to capitalize on this persistent trend.

- Exceptional performance. PDD Holdings delivered better-than-expected earnings for the fourth quarter, driven by overseas expansion. Revenue reached 88.88bn yuan (US$12.4bn), up 123% YoY and surpassing analyst forecasts. Its Chairman and co-CEO highlighted 2023 as a pivotal year for the company’s development towards high-quality growth, with a commitment to improving consumer experiences and technology innovation in 2024. The company’s full-year revenue increased by 90% YoY to 247.64bn yuan, with plans to focus on supporting high-quality supply and enhancing service delivery. Despite challenges in China’s economy, PDD’s overseas platform Temu gained popularity among American consumers for its affordable products. While facing scrutiny from American authorities regarding supply chain practices, PDD continues to expand its logistics capabilities and increase spending on advertising and promotions. PDD’s executives emphasized the importance of rational consumption upgrades and announced plans to invest in technology and agriculture to continue to drive growth in 2024.

- 4Q23 earnings review. Revenue rose by 113.26% YoY to US$12.35bn, beating estimates by US$1.50bn. EPS was US$2.41, beating estimates by US$0.75. In 2024, the company will continue to ramp up its support for high-quality supply and enhance its ability to deliver good value and excellent service.

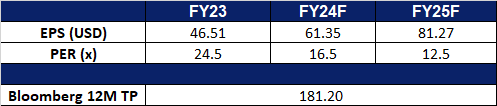

- Market consensus.

(Source: Bloomberg)

Goldman Sachs Group Inc (GS US): Net interest margins to remain elevated

- RE-ITERATE Entry – 420 Target – 450 Stop Loss – 405

- The Goldman Sachs Group, Inc., a bank holding company, is a global investment banking and securities firm specializing in investment banking, trading and principal investments, asset management and securities services. The Company provides services to corporations, financial institutions, governments, and high-net worth individuals.

- Rates unchanged. In May, the US Federal Reserve maintained interest rates and hinted at potential future reductions, but expressed concern over recent disappointing inflation readings, suggesting that rate cuts might be delayed. Fed Chair Jerome Powell emphasized the need for sustained progress in inflation towards the 2% target, indicating a cautious approach to rate adjustments. While Powell’s remarks were less hawkish than expected, investors remained uncertain about the timing of rate cuts, with some speculation that cuts could begin in September. The Fed also announced a reduction in the pace of balance sheet shrinking to ensure adequate reserves in the financial system. Despite relatively weak GDP growth in the first quarter, Powell highlighted strong job gains and low unemployment, dismissing concerns of stagflation. With interest rates expected to remain unchanged, banks like Goldman Sachs will benefit from continued high net interest margin.

- Lead private credit debt deal. Goldman Sachs spearheaded a significant private credit debt deal, raising €1.5bn for SumUp, a leading global FinTech firm. This financing will be utilized to restructure existing debt and drive SumUp’s international growth initiatives, particularly in bolstering support for merchants and expanding product offerings. The oversubscribed round underscores investor faith in SumUp’s established business model and highlights the prowess of Goldman Sachs’ deal team. Notable new investors AllianceBernstein, Apollo Global Management, and Deutsche Bank AG joined existing backers such as BlackRock and Temasek in supporting SumUp’s mission.

- Success in going back to its roots. Goldman Sachs exceeded Wall Street expectations with a 28% rise in profit in the first quarter, driven by a resurgence in underwriting, deals, and bond trading. The bank’s earnings showed strong performance in investment banking, indicating a rebound after recent challenges. Its CEO expressed optimism about the reopening of capital markets and highlighted the growing interest in initial public offerings and debt underwriting. The bank’s focus on AI-related advisory services and a shift away from consumer banking garnered investor confidence. Additionally, robust investment banking fees and record revenue from asset and wealth management contributed to the positive outcome. Goldman Sachs remains committed to its strategic shifts, prioritizing its core businesses and anticipates continued growth as it bolsters its position in capital markets.

- 1Q24 earnings review. Revenue rose by 16.3% YoY to US$14.21bn, beating estimates by US$1.28bn. GAAP EPS was US$11.58, beating estimates by US$2.90. The company declared a quarterly dividend of US$2.75 per share, in line with the previous dividend.

- Market consensus.

(Source: Bloomberg)

Trading Dashboard Update: No stock additions/deletions.