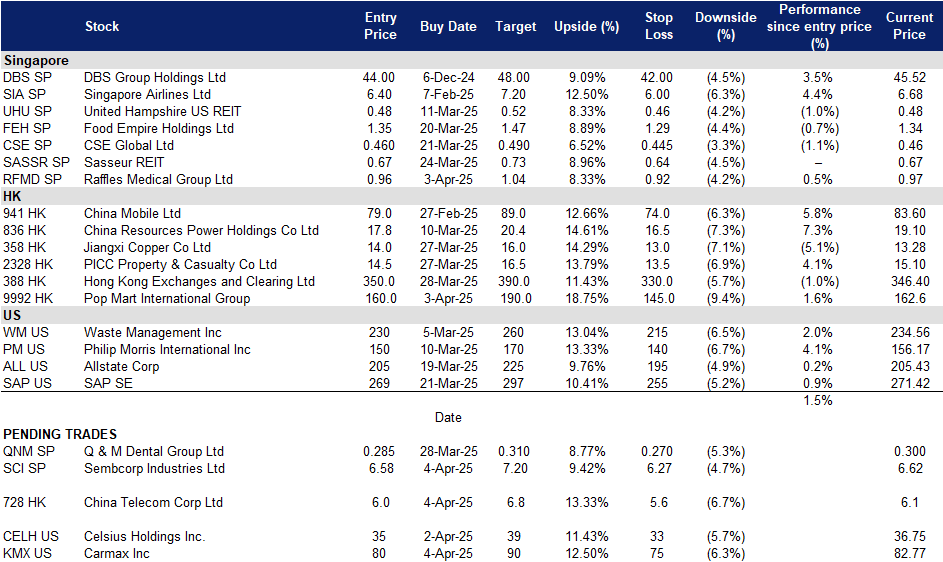

Sembcorp Industries Ltd (SCI SP): Risk off and rate cut expectations

BUY Entry – 6.58 Target– 7.20 Stop Loss – 6.27

Sembcorp Industries Ltd provides utilities and integrated services for industrial sites such as power, gas, steam, water, wastewater treatment and other on-site services. Sembcorp Industries serves industrial parks, business, commercial, and residential spaces.

Rotation to defensive sectors and rising rate cut expectations. Escalating global trade tensions, driven by the broad tariff policies of the US, will gradually reshape global supply chains. World economic growth, especially in Asia, is expected to slow down substantially in the near term. Amidst macro headwinds, the utility sector is expected to outperform others. Meanwhile, expectations of rate cut are reviving. Lower interest rates would benefit Sembcorp by reducing financing costs, enhancing project viability, and potentially boosting demand for its energy and urban solutions. In a nutshell, investors favour assets with stability and visibility moving forward.

Proposed acquisition. Sembcorp Industries plans to increase its stake in Senoko Energy from 30% to a maximum of 70%, expanding its role in Singapore’s energy sector. The acquisition agreement, signed with KPIC Netherlands, Kyuden International, and Japan Bank for International Cooperation (JBIC), involves purchasing up to a 57.1% stake in Lion Power, which owns 70% of Senoko. The deal, valued at up to S$144mn, will be funded through internal cash and/or external borrowings and is expected to close in 2Q25. The Energy Market Authority has approved the acquisition, with Sembcorp committing to measures that ensure fair market competition. The acquisition is projected to be earnings accretive but will not significantly impact net tangible assets per share for FY25. This strategic move strengthens Sembcorp’s position in Singapore’s energy market and supports its commitment to the energy transition. With a larger stake in Senoko, Sembcorp can enhance operational synergies and contribute more effectively to sustainable and reliable energy solutions, aligning with its long-term growth strategy.

Increased dividend payout. Sembcorp raised its dividend to S$0.23 per share, from its previous S$0.13 in FY23, reflecting a higher payout ratio, signaling confidence in sustained profitability. The company’s net profit before exceptional items remained above S$1bn for a second consecutive year. Sembcorp’s gas and related services segment saw a 10% decline in profit to S$727mn, impacted by a 34% drop in Singapore’s wholesale electricity prices. However, the company solidified its position as the leading power provider for data centers and acquired a 30% stake in Senoko Energy. Additionally, it fully exited coal-fired power assets with the divestment of its 49% stake in Chongqing Songzao. Sembcorp’s renewable energy portfolio grew to 13.1 GW in 2024, progressing toward its 2028 goal of 25 GW. The company remains focused on executing its 2024-2028 strategic plan to meet Asia’s evolving energy needs. With a stronger commitment to dividends and an expanding clean energy portfolio, the company is poised to capitalize on Asia’s transition to sustainable energy while maintaining financial stability.

FY24 financial results. Sembcorp Industries Ltd reported net profit of S$1,011mn for FY24, a 7% incline YoY, compared to S$942mn in FY23. Due to the Group’s strong performance, the Board of Directors approved a total dividend of S$0.23 per ordinary share for FY24, an increase from the S$0.13 distributed for FY23.

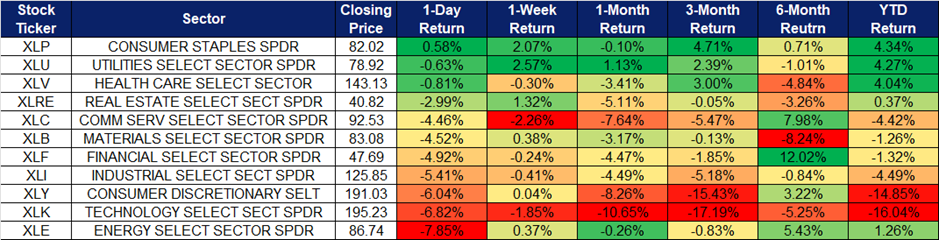

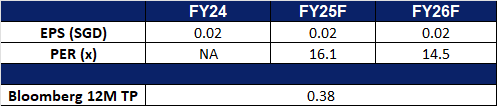

Market consensus

(Source: Bloomberg)

Q&M Dental Group Ltd (QNM SP): Streamlining business operations

Q & M Dental Group (Singapore) Limited operates dental clinics. The Company offers aesthetic, children’s and general dentistry; fits crowns, dentures and braces; and offers bleeding gum treatment, gum surgery and oral surgery; and treats snoring and teeth grinding.

Increased Profitability Outlook. The company reported a strong improvement in profitability, with net profit margin (NPM) rising by 18.0% to S$13.1 million in FY24. This was driven by cost-cutting initiatives, including the closure of underperforming clinics and the winding down of its medical laboratory business in September 2024 following the decline of COVID-related operations. Several expense categories declined year-over-year, reflecting the company’s effective streamlining efforts. We expect these efficiency gains to sustain profitability into the next financial year.

Expansion into New Markets with Additional AI Licenses. EM2AI has obtained regulatory licenses to sell and distribute its dental AI solutions in Thailand, the Philippines, Vietnam, and Indonesia, expanding beyond its existing presence in Singapore and Malaysia. These approvals enable EM2AI to broaden its market reach and capitalize on the growing demand for AI-driven dental solutions across Southeast Asia.

Strategic Partnership to Scale Regional Presence. Following its recent licensing approvals, EM2AI has actively pursued partnerships to accelerate market expansion. The company has signed a Memorandum of Understanding (MoU) with an established regional dental solutions provider, granting the partner a license to integrate EM2AI’s technology into its platform. This collaboration aligns with the company’s strategy to expand its business network and solidify its footprint in key regional markets. As a result, EM2AI is now set to provide its dental AI solutions to over 1,100 clinics across Singapore, Malaysia, Thailand, and Vietnam, reinforcing its growth trajectory and long-term value creation for shareholders.

FY24 financial results. Q & M Dental Group reported revenue of S$180.7mn for FY24, a 1.1% decline YoY, compared to S$182.7mn in FY23, mainly due to the cessation of the Group’s medical laboratory business. PATMI rose by 27.1% YoY to S$14.6mn in FY24, compared with S$11.5mn in FY23. EPS rose to 1.55 Singapore cents in FY24, compared to 1.22 Singapore cents in FY23. The Group also announced plans to carry out a share buyback of up to 50mn ordinary shares.

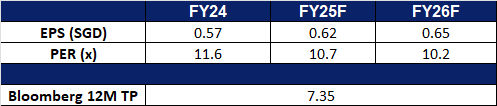

We have fundamental coverage with a BUY recommendation and a TP of S$0.35. Please read the full report here.

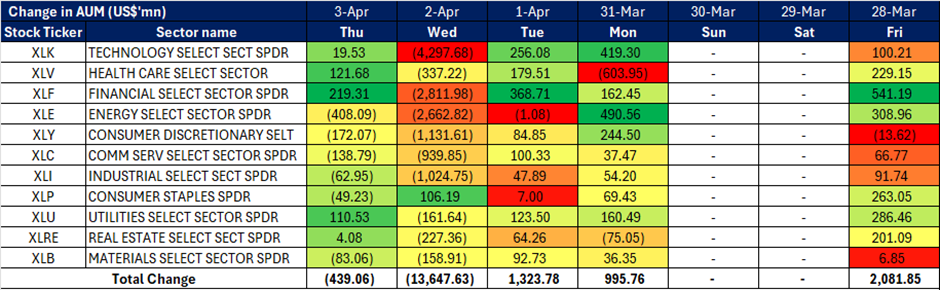

Market consensus

(Source: Bloomberg)

China Telecom Corp Ltd. (728 HK): Smartphone market recovery

BUY Entry – 6.00 Target – 6.80 Stop Loss – 5.60

China Telecom Corp Ltd is a China-based company mainly engaged in telecommunications and related businesses. The Company’s main business includes mobile telecommunications services, wireline and smart family services, industrial digital services, and commodity sales. The Company’s mobile telecommunications services business mainly includes mobile voice, handset Internet access, and mobile value-added services. The Company’s Wireline and smart family services business mainly include fixed-line telephone, wireline broadband and smart home services. The Company’s industrial digital business mainly includes industry cloud, Internet data center (IDC), digital platform, network dedicated line, Internet of Things and other businesses. The Company’s commodity sales business refers to the company’s sales of mobile terminal equipment and wireline communication equipment to users. The Company distributes its products within the domestic market.

Another step to 6G technologies. A China Telecom subsidiary has been granted a national invention patent for a critical 6G satellite-terrestrial integration technology, marking a major step toward technological self-sufficiency in next-generation wireless communications. The patent, titled “A Method for 6G-Based Integrated Space-Air-Ground Transmission Optimization and Topographic Mapping,” establishes a core technical foundation for a fully connected “space-air-ground-sea” network. As the lead entity in the national 6G Satellite Communication Access and Networking Technology project, China Telecom promotes a backward-compatible approach that harnesses ground network technology to drive satellite communication advancements. This milestone comes at a crucial time as the global telecom industry works to define key technologies and standards for 6G.

Subsidies driving smartphone sales. China’s smartphone market saw a significant boost in February, driven largely by government subsidies aimed at stimulating consumer demand. Effective January 20, 2025, the subsidy program offers a 15% discount on smartphones priced below 6,000 RMB, with a maximum rebate of 500 RMB. While domestic brands have been the primary beneficiaries, foreign brands like Apple also saw stronger-than-expected sales, defying the usual seasonal decline. According to the China Academy of Information and Communications Technology (CAICT), February smartphone shipments reached 18.6 million units, marking a 33% year-over-year increase despite a 24% decline from January. This market rebound is expected to have a positive impact on China Telecom in the long run.

AI integration. Earlier this year, China Telecom, along with other major Chinese telecom companies, announced the integration of DeepSeek’s artificial intelligence (AI) models into their services and products. The move follows a broader trend among the country’s top tech firms, including Alibaba Group, Tencent Holdings and Baidu Inc, which have ramped up support for DeepSeek’s latest AI models on their respective platforms. While these telecom giants have been developing their own large language models (LLMs) over the past two years amid a global AI boom spurred by OpenAI, they primarily leverage DeepSeek’s models for cloud-based applications. China Telecom was the first of the big telcos to adopt DeepSeek with the early February launch of a full-stack DeepSeek-R1/V3 inferencing on its Xiran intelligent computing platform.

FY24 results review. Revenue increased by 3.1% YoY to RMB529.4bn in FY24, compared with RMB513.6bn in FY23. Net profit rose by 8.4% to RMB33.0bn in FY24, compared to RMB30.4bn in FY23. Basic EPS increased to RMB0.36 in FY24, compared to RMB0.33 in FY23.

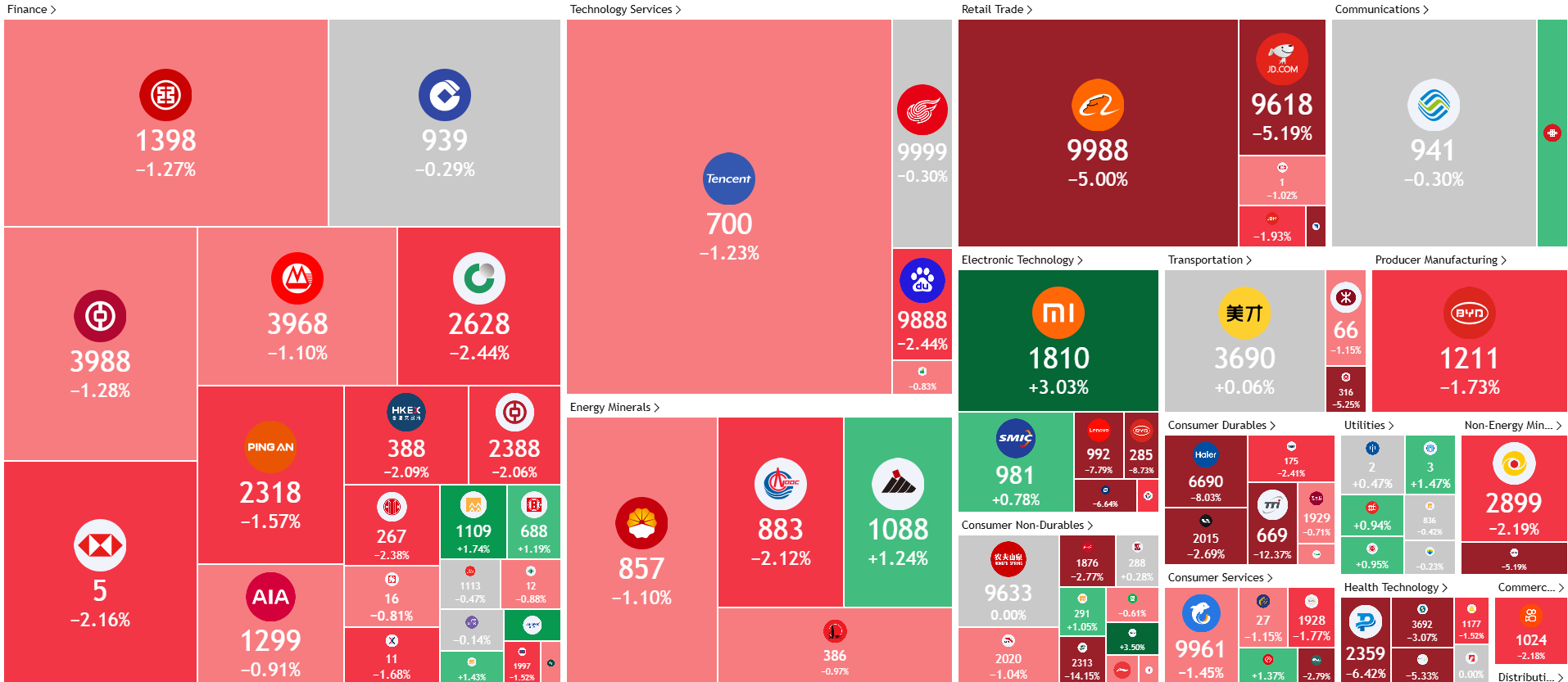

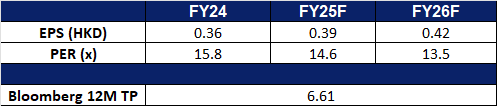

Market consensus.

(Source: Bloomberg)

Pop Mart International Group Ltd. (9992 HK): Labubu craze still strong

Pop Mart International Group Ltd is a China-based company mainly engaged in the provision of pop toy. intellectual property (IP) is at the core of its business. It has established an integrated platform covering the entire industry chain of pop toys, including artists development, IP operation, consumer access and pop toy culture promotion. The Company develops a broad array of pop toy products based on its IPs. Its Pop Mart brand products are primarily categorized into blind boxes, action figures, ball-jointed doll (BJDs) and accessories. The Company conducts its businesses within the China market and to overseas markets.

Record-Breaking Growth and Strong Financial Performance. Pop Mart International delivered an exceptional financial performance in 2024, with revenue soaring by 106.9% to 13bn.0 yuan and net profit surging 185.9% to 3.4 billion yuan. This explosive growth was primarily driven by the company’s plush toy category, which saw an unprecedented 1,289% increase in sales to 2.83 billion yuan. The popularity of its flagship IP, LABUBU, played a crucial role, with plush toy production capacity expanding from 300,000 units in early 2024 to 10 million units by year-end. In response to soaring demand, Pop Mart has prioritized strengthening its supply chain and investing in design, craftsmanship, and materials to sustain growth. As it looks ahead to 2025, the company targets a 50% year-on-year revenue increase to 20 billion yuan, further solidifying its position as a dominant player in the global trendy toy market.

Aggressive Global Expansion and Strategic Growth Plans. Pop Mart is aggressively expanding its international footprint, with overseas revenue skyrocketing 375.2% to 5.07 billion yuan in 2024. Southeast Asia and North America were key growth regions, experiencing revenue surges of 619% and nearly sixfold, respectively. The company expects its North American revenue alone to reach 2.513 billion yuan in 2025, a milestone equivalent to its total global revenue in 2020. The US market, in particular, has demonstrated remarkable momentum, exceeding its 2024 full-year revenue within the first quarter of 2025. To support its expansion, Pop Mart plans to open approximately 100 new overseas stores this year, including flagship locations in the US, Thailand, France, and Australia. Additionally, the company is diversifying its offerings by exploring new categories such as jewelry and investing in animation content featuring its most popular IPs, reinforcing its vision to become a world-class cultural and consumer brand.

China’s Pro-Consumption Policies. China’s newly unveiled 30-point policy package aims to boost consumer spending by increasing household incomes, reducing financial burdens, and stabilizing key markets like property and stocks. This initiative, which integrates fiscal and financial tools, seeks to enhance consumer confidence by addressing livelihood concerns such as childcare, education, and healthcare while also expanding domestic demand through trade-in subsidies for consumer goods. With China doubling its funding for consumer incentives to 300 billion yuan in 2025, the policy is expected to stimulate discretionary spending, benefiting brands like Pop Mart. As a leading cultural and consumer brand, Pop Mart stands to gain from increased disposable income and consumer confidence, particularly in categories like collectible toys and lifestyle products. The emphasis on stabilizing financial markets may also encourage investor sentiment, supporting Pop Mart’s stock performance and expansion plans. With strong government backing for consumption-driven growth, Pop Mart is well-positioned to capitalize on rising demand in both its core Chinese market and international expansion efforts.

FY24 results review. Revenue increased by 106.9% YoY to RMB13.0bn in FY24, compared with RMB6.30bn in FY23. Net profit rose by 203.9% to RMB3.31bn in FY24, compared to RMB1.09bn in FY23. Basic EPS increased to RMB2.36 in FY24, compared to RMB0.81 in FY23.

Market consensus.

(Source: Bloomberg)

Celsius Holdings Inc. (CELH US): Fuelling female consumer expansion

Celsius Holdings, Inc. operates as a holding company. The Company, through its subsidiaries, provides thermogenic calorie-burning beverages. The Company markets its beverages multiple channels including grocery, drug, convenience stores, gyms, and nutrition stores. Celsius Holdings serves clients in the United States.

Low beta stock. The beverage industry is a relatively defensive sector with low correlation to the overall market. The company’s product market positioning is in the niche market of functional beverages, with 94.7% of its revenue coming from the North American market, making it less affected by tariff policies.

Brand expansion. In February 2025, Celsius announced the acquisition of its competitor Alani Nu for US$1.8bn in cash and stock. Alani Nu, founded by fitness influencer Katy Hearn in 2018, has quickly gained popularity among young women through social media marketing and low-calorie, health-oriented products. This acquisition is expected to expand Celsius’s market reach, particularly among female consumers, and is expected to significantly drive the company’s growth. According to its 2024 financial report, the company’s market share slightly increased by 1.6%, reaching 11.8%.

4Q24 results. Revenue decreased by 4.3% YoY to US$332mn, exceeding expectations by US$5.18mn. Non-GAAP earnings per share were US$0.14, exceeding expectations by US$0.04.

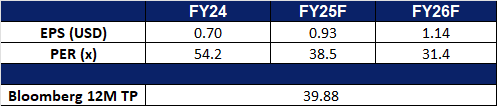

Market consensus

(Source: Bloomberg)

Allstate Corp (ALL US): Active management amid tariff impact

The Allstate Corporation provides property-liability insurance solutions. The Company sells private passenger automobile and homeowners insurance through independent and specialized brokers, as well as life insurance, annuity, and group pension products through agents. Allstate serves customers in the United States and Canada.

Tariffs to benefit. Allstate Protection Auto Insurance continues to strengthen margins, with earned premiums rising 9.1% YoY, driven by rate increases. The auto combined ratio improved to 93.5 in 4Q24, reflecting higher premiums and better loss performance. Trump’s 25% auto tariffs, effective 2 April, and auto parts tariffs by 3 May, alongside existing steel and aluminium tariffs, could further benefit Allstate by raising vehicle prices, leading to higher insured values and premiums. With insurance costs already up 11% YoY in February and projected to rise 19%, Allstate is well-positioned for further profitability. Additionally, as consumers hold onto older vehicles longer, insurers will adjust rates to cover rising repair costs, further contributing to Allstate’s profitability in the auto insurance sector.

Increased concerns about a U.S. recession benefiting defensive sectors. Recent U.S. macroeconomic data shows that inflation remains high, while the labour market is beginning to cool, and consumer spending and confidence are declining. Trump’s tariff policy has triggered a global trade war, and the U.S. stance on the Russia-Ukraine issue has been questioned by its allies. With the concentration of negative factors, the market is averse to uncertainty, so major growth sectors have seen significant corrections, and funds have rotated to stronger defensive sectors.

Unlocking value. Allstate continues to optimize its portfolio by divesting non-core businesses and adjusting insurance pricing. The company announced estimated catastrophe losses of US$1.08bn for January, largely due to California wildfires. To streamline operations, Allstate has agreed to sell its Group Health business to Nationwide for US$1.25bn, marking another step in its plan to exit non-core segments. Combined with the earlier sale of Employer Voluntary Benefits, total expected proceeds from these divestitures will reach US$3.25bn, generating an estimated US$1bn financial book gain in 2025. Meanwhile, Allstate is actively adjusting insurance pricing to mitigate risk exposure and improve profitability. In California, homeowners insurance rates rose by an average of 34% in November, with another 30% increase for condo insurance planned in April. Similarly, Illinois homeowners saw about a 14% premium hike in February. These rate adjustments will help Allstate navigate increasing claims costs while bolstering its financial position.

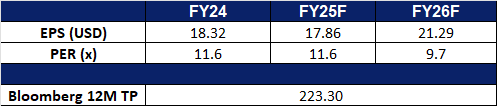

4Q24 results. Revenue rose 11.3% YoY to US$16.51 billion, beating expectations by US$280 million. Non-GAAP earnings per share were US$7.67, beating expectations by US$1.39. The board of directors approved a quarterly common stock dividend of US$1.00, an increase of US$0.08 or 8.7% per share compared to the previous quarter. Additionally, they also authorised a US$1.5bn share repurchase program of outstanding common stock, which will remain in effect through 30 September 2026.

Trading Dashboard Update: Add Raffles Medical Group Ltd (RFMD SP) at S$0.96 and Pop Mart International Group (9992 HK) at HK$160. Cut loss on GE Healthcare Technologies Inc (GEHC US) at US$79 and Alibaba Group Holding Ltd (9988 HK) at HK$127.