Singapore Airlines Limited provides air transportation, engineering, pilot training, air charter, and tour wholesaling services. The Company’s airline operation covers Asia, Europe, the Americas, South West Pacific, and Africa.

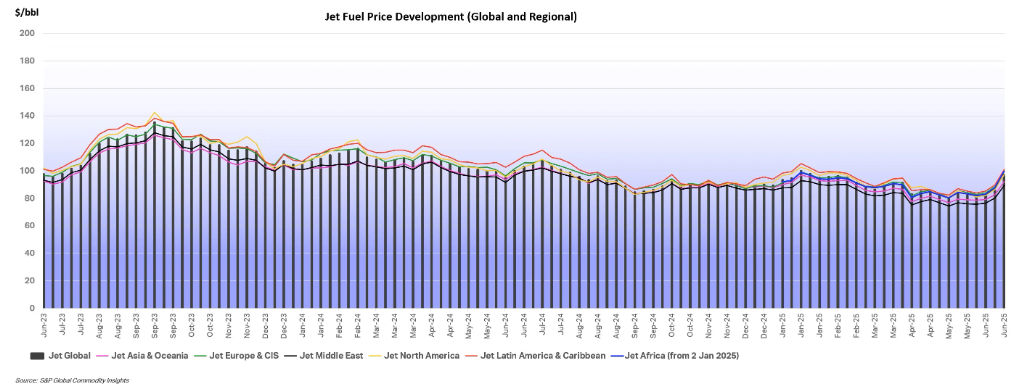

Jet fuel prices expected to gradually decline. Recent tensions between Israel and Iran have pushed jet fuel prices to their highest levels in 15 months. However, this spike is expected to ease as geopolitical risks subside. Saudi Arabia and the United Arab Emirates can quickly ramp up production, with a combined spare capacity of approximately 3.5 million barrels per day (bpd), which could offset any temporary supply disruptions from Iran, which currently produces around 3.3 million bpd and exports over 2 million bpd. According to the International Air Transport Association (IATA), the average jet fuel price in 2025 is projected at US$86 per barrel, with total airline fuel expenditures expected to fall to US$236 billion—nearly 9% lower than in 2024. While short-term price fluctuations may occur due to geopolitical or refinery disruptions, overall fuel price stability is anticipated, with minimal impact from ongoing trade tensions. Fuel costs are forecast to account for 25.8% of total airline operating expenses, supporting improved airline profitability. As of the week ending June 20, 2025, the global average jet fuel price stood at US$96.97 per barrel, up 12.9% from the previous week.

Record US$1 trillion in 2025 airline revenue. According to the IATA, in 2025, global airline revenues are projected to reach a record US$979 billion, with net profits improving to US$36 billion, despite falling short of earlier forecasts due to US tariffs, trade tensions, and softer-than-expected growth in passenger and cargo volumes. The Asia-Pacific region is expected to lead industry expansion, driven by economic growth and eased visa policies, contributing over half of global air travel growth. Lower jet fuel prices will support airline profitability by reducing operating costs, though supply chain disruptions, aircraft delivery delays, and ongoing engine and parts shortages continue to constrain capacity. While the industry remains on a positive trajectory with stable margins, structural challenges such as thin profitability, geopolitical risks, and the slow progress in scaling sustainable aviation fuel production present headwinds to long-term growth.

Seasonality chart – SIA

(Source: Bloomberg)

Seasonal rise in travel. In the first five months of 2025, Singapore attracted over seven million international tourists, driven by strong demand from China, Indonesia, and India. With the ongoing summer holidays, both inbound and outbound travel demand is anticipated to rise. This seasonal uptick in travel is likely to benefit Singapore Airlines by increasing passenger traffic, contributing to higher flight bookings and demand for its services during peak travel periods. The airline is well-positioned to capitalize on this increased travel activity, boosting its revenue and enhancing its global connectivity.

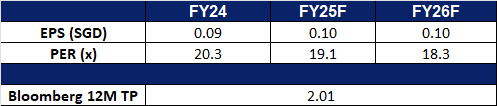

FY24 results review. Revenue increased 2.8% YoY to S$19.5bn, driven by resilient demand for air travel and cargo uplift during the year. It delivered record S$2.8bn in net profit, boosted by the one-off non-cash accounting gain of S$1.1bn from the Air India-Vistara merger. Proposed final dividend of S$0.30 per share for FY2024/25, resulting in a total dividend of S$0.40 per share for the year.

Market consensus

(Source: Bloomberg)

Sheng Siong Group Ltd (SSG SP): Value driven growth potential

Sheng Siong Group Ltd is a retailer in Singapore. The Company operates a groceries chain across Singapore. Sheng Siong’s stores provide fresh and chilled produce, seafood, meat and vegetables, processed, packaged and preserved food products as well as general merchandise such as toiletries and essential household items.

Government vouchers to support near-term growth. Singapore’s FY25 voucher disbursement program, including S$800 in CDC Vouchers for households and up to S$800 in SG60 Vouchers for all Singapore Citizens, is expected to directly boost supermarket sales, with half the amount allocated for spend at participating supermarkets like Sheng Siong. These voucher schemes, alongside ongoing government support measures, will help sustain consumer spending momentum despite a cautious economic backdrop, providing a visible near-term revenue tailwind for Sheng Siong.

Value shopping to drive demand. Singapore’s core inflation rose to 0.7% in April 2025, ending six consecutive months of decline, mainly driven by rising food and services costs. However, the Monetary Authority of Singapore (MAS) and economists project inflation to remain modest for the rest of the year, with downside risks from weak global demand, persistent supply chain disruptions, and escalating tariff uncertainties. In this environment, Singaporean consumers are expected to remain price-conscious, driving sustained demand for affordable essentials and value-for-money house brand products. Sheng Siong, with its strong house brand offerings priced 5% to 20% below national brands, robust supply chain diversification, and disciplined cost management, is well-positioned to capture this structural shift towards value-driven consumption and defend margins amid inflationary and import cost pressures.

Strategic expansion partially linked to new HDB pipeline. Sheng Siong’s store network expansion is strategically tied to the Housing Development Board’s (HDB) pipeline, with over 50,000 new flats scheduled to be launched from 2025 to 2027 across growth areas. The Group is actively bidding for new supermarket sites within upcoming housing estates, having recently secured multiple tenders and two private retail spaces at KINEX and CATHAY. As HDB continues to roll out new developments, Sheng Siong is well-positioned to grow its footprint in high-density residential areas, supporting long-term revenue expansion.

1Q25 financial results. Sheng Siong reported 7.1% YoY growth in revenue for 1Q25, to S$403.0mn from S$376.2mn in 1Q24, mainly driven by the eight new stores opened compared to the same period last year alongside the festive sales for Hari Raya. Net profit for the period increased by 6.1% to S$38.5mn from the previous S$36.3mn. Comparable same store revenue in Singapore for 1Q25 increased marginally by 0.1%. China’s revenue increased marginally by 0.7%.

Cathay Pacific Airways Ltd is a company mainly engaged in the provision of international passenger and cargo air transportation. Together with its subsidiaries, the Company operates business through its four operating segments. The Cathay Pacific and Cathay Dragon segment provides full service international passenger and cargo air transportation under the Cathay Pacific and Cathay Dragon brands. The Air Hong Kong segment provides express cargo air transportation offering scheduled services within Asia. The HK Express segment provides a low-cost passenger air transportation offering scheduled services within Asia. The Airline Services segment provides supporting airline operations services include catering, cargo terminal operations, ground handling services and commercial laundry operations.

Lowered crude oil prices. Brent crude oil futures fell over 1% to around $69 per barrel on Tuesday, hitting a more than one-week low, following news of a ceasefire between Israel and Iran. The Israeli government confirmed the agreement early Tuesday, with Iranian state media later reporting Tehran’s acceptance, raising hopes for an end to the 12-day conflict. The truce eased fears of potential supply disruptions in the Middle East, particularly concerns over a possible blockade of the Strait of Hormuz, a key passage for about 20% of global oil flows. The resulting decline in crude prices is expected to benefit airlines, for whom jet fuel represents a significant portion of operating costs.

Brent Crude Oil Price

(Source: Bloomberg)

China’s summer holidays.Chinese airlines are stepping up efforts to expand their international networks ahead of the upcoming summer travel season, driven by strong demand, particularly to destinations along the Belt and Road Initiative (BRI), which are emerging as key markets for Chinese carriers. According to data from travel industry platform Umetrip, as of June 16, inbound and outbound flight bookings for July 1–31 surpassed 3.8mn, marking an 8% increase YoY. Cathay Pacific, recently ranked among the world’s top three airlines in the 2025 Skytrax World Airline Awards, reported a 36.1% YoY increase in passengers for May 2025, with available seat kilometres up 31.2%. For the first five months of the year, passenger volume rose by 28.4% compared with the same period in 2024. With strong forward bookings and rising travel momentum, the upcoming summer holidays are expected to bring further growth in travel demand, likely benefiting Cathay Pacific’s operational and financial performance.

More flights to cater to growing demand. Cathay Pacific has announced it will introduce double daily flights between Hong Kong and Perth, adding more than 43,000 extra inbound seats to Western Australia annually. This expanded service is supported by the Western Australian Government, through Tourism WA, in collaboration with Perth Airport. With this addition, Cathay Pacific’s total annual seat capacity into WA will exceed 200,000. This marks the second increase in flight frequency to Perth within a year, reflecting strong and growing demand for Western Australia among travellers from China and Hong Kong (Greater China). As a major global transit hub, Hong Kong also facilitates broader connectivity, and the increased frequency will enhance one-stop travel options for key visitor markets such as the United Kingdom, the United States, and Japan. The expansion is expected to contribute positively to Cathay Pacific’s top-line growth in the long term.

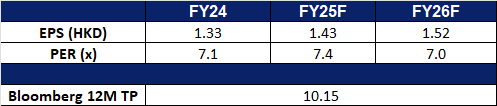

FY24 results review. FY24 revenue rose by 10.5% to HK$104.4bn, compared to HK$94.5bn in FY23. Profit attributable to shareholders was HK$9.89bn in FY24, up 1.0% YoY, compared to HK$9.79bn in FY23. Basic EPS increased to HK$1.49 in FY24 from HK$1.41 the same period last year.

Market consensus.

(Source: Bloomberg)

Hong Kong Exchanges and Clearing Ltd. (388 HK): Hottest IPO market

Hong Kong Exchanges and Clearing Limited (HKEX) is principally engaged in the operation of stock exchanges. The Company operates through five business segments. The Cash segment includes various equity products traded on the Cash Market platforms, the Shanghai Stock Exchange and the Shenzhen Stock Exchange. The Equity and Financial Derivatives segment includes derivatives products traded on Hong Kong Futures Exchange Limited (HKFE) and the Stock Exchange of Hong Kong Limited (SEHK) and other related activities. The Commodities segment includes the operations of the London Metal Exchange (LME). The Clearing segment includes the operations of various clearing houses, such as Hong Kong Securities Clearing Company Limited, the SEHK Options Clearing House Limited, HKFE Clearing Corporation Limited, over the counter (OTC) Clearing Hong Kong Limited and LME Clear Limited. The Platform and Infrastructure segment provides users with access to the platform and infrastructure of the Company.

Hong Kong regained global IPO leadership. Deloitte has upgraded its forecast for Hong Kong’s IPO market, projecting over HK$200 billion from 80 listings in 2025, as the city reclaimed its position as the world’s top fundraising venue in the first half, outpacing both Nasdaq and the New York Stock Exchange. This resurgence, driven by a 33% YoY increase in IPO deals and several mega A+H listings, highlights renewed investor confidence and robust global capital inflows. With nearly 200 IPO applications in the pipeline, including several large-cap names, and ongoing exchange reforms aimed at enhancing liquidity and attracting international investors, HKEX is well-positioned to sustain its strong IPO momentum and reinforce its role as a leading global financial hub.

Expansion of secondary listing market. HKEX is accelerating its global expansion by targeting secondary listings from Southeast Asia, the Middle East, and beyond. The exchange plans to open a representative office in Riyadh to deepen ties with the Saudi market and has already seen successful listings from Singaporean and Thai companies. Growing interest from mainland Chinese firms seeking offshore capital and rising participation from U.S. investors further strengthen HKEX’s competitive position. The IPO pipeline has more than doubled since December 2024 and the exchange has reclaimed its spot as the world’s largest listing venue by volume in 2025. HKEX’s proactive outreach and increasing cross-border listings underscore its transformation into a premier international fundraising platform.

Supportive monetary policy. The People’s Bank of China’s decision to maintain stable benchmark interest rates reflects confidence in the resilience of China’s economic recovery and creates a supportive backdrop for corporate capital raising. Stable rates reduce financial market uncertainty, support corporate valuations, and encourage both IPO and secondary listing activity. Recent signs of improving consumer demand, resilient export performance, and policy stability in China further underpin the capital markets environment. This is expected to drive sustained interest from mainland Chinese companies seeking offshore funding, as well as continued investor appetite for equity issuance, supporting the Hong Kong Stock Exchange’s long-term growth prospects.

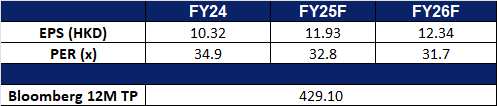

1Q25 results review. Q1 revenue and other income of HK$6,857mn was 32% higher than 1Q24. Profit attributable to shareholders was HK$4,077mn, 37% higher than 1Q24. Basic EPS increased to HK$3.23 from HK$2.35 the same period last year.

Market consensus.

(Source: Bloomberg)

International Business Machines (IBM US): Capitalizing on mainframe expansion and quantum computing

International Business Machines is a global technology company focused on software, cloud services, artificial intelligence, and consulting services.

Steady growth in the global mainframe market. The global mainframe market is driven by the increasing demand for high-performance computing and robust data processing and cybersecurity solutions. It is expected to grow from $3.5 billion in 2024 to $6.8 billion by 2033, with a compound annual growth rate of 8.4%. IBM’s Z series mainframes hold a significant market share and maintain leadership in the mainframe market. The newly launched z17 mainframe is designed to meet the high computational demands of generative AI and the security needs of critical workloads for large enterprises, particularly in the financial services sector. As global demand for high-performance and highly secure infrastructure continues to rise, the company has strong growth momentum in this area.

Investment in quantum computing. Since the end of last year, quantum computing has gained market attention and is seen as another major technological revolution outside of artificial intelligence, with related company stocks soaring. IBM is actively developing quantum computing, planning to invest $30 billion over the next five years in research and development of quantum computing and mainframe technology, as part of its commitment to a total investment plan of $150 billion in the U.S. The company aims to launch practical quantum computers by 2029 and achieve a more advanced “Starling” system with approximately 200 logical qubits by 2033.

Business less affected by geopolitical risks. The company’s global operations cover both software and hardware, as well as consulting services, providing a higher level of risk resilience. Its core businesses, such as mainframe manufacturing and cloud services, have strong demand, resulting in relatively stable revenue growth during volatile economic cycles.

1Q25 results. Revenue grew 0.6% to US$14.54bn, exceeding expectations by US$150mn. Non-GAAP earnings per share were US$1.60, surpassing estimates by US$0.17. The company expects full-year revenue growth of 5% (fixed rate).

GE Electric Co (doing business as GE Aerospace) operates as an aircraft engine supplier company. The Company provides jet and turboprop engines, as well as integrated systems for commercial, military, business, and general aviation aircraft. GE Aerospace serves customers worldwide.

Healthy cash position. GE Aerospace reported US$1.5 bn in cash from operating activities and US$1.4bn in free cash flow in 1Q25, with revenue rising 11% YoY to $9.0bn and operating profit reaching $2.1bn, a 23.8% profit margin, supported by a robust commercial services backlog of over US$140bn as of Q1 that underpins long-term earnings visibility.

Defense orders to bolster growth. Amid ongoing geopolitical instability, GE Aerospace stands to benefit from rising defense budgets, highlighted by its US$5bn contract win with the U.S. Air Force for F110-GE-129 engines, which will support sustained military demand alongside its sizable commercial services backlog.

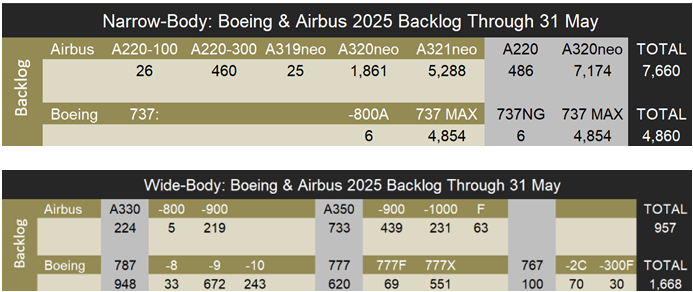

Record commercial engine deals. GE Aerospace secured a historic engine deal with Qatar Airways for over 400 engines, alongside additional commitments from ANA Holdings, Malaysia Aviation Group, and Korean Air, further building its commercial services backlog. According to Forecast International’s 2025 production estimates, as of 31 May, Airbus’s backlog represents 10.5 years of production and Boeing’s backlog approximately 11.5 years, highlighting the tight commercial aviation supply chain and potentially prolonging demand for GE’s engines, spares, and aftermarket services.

Airbus and Boeing report May 2025 commercial aircraft orders backlog:

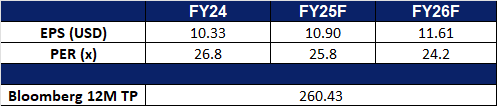

1Q25 results. Revenue increased by 11% YoY to US$9.0bn, missing expectations by US$50mn. Non-GAAP earnings per share was US$1.49, surpassing estimates by US$0.22. The company maintained its full-year revenue forecast for FY25 to in low double digit and adjusted EPS of between US$5.10 to US$5.45, with the mid-point below consensus of US$5.42. It also expects operating profit to be US$7.8bn – US$8.2bn and free cash flow to be between US$6.3bn – US$6.8bn.