SATS Ltd. provides air cargo handling services and food solutions. The Company offers airfreight and ground handling services including passenger, ramp and baggage handling, aviation security, aircraft cleaning and aviation laundry, and food distribution and logistics. SATS serves clients worldwide.

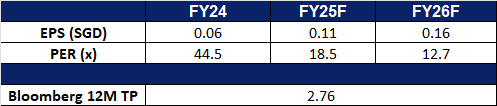

Outperformance driving momentum. SATS posted a robust FY25 performance, with profit surging more than three-fold to S$243.8 million on the back of a 13% YoY revenue increase to S$5.8 billion. Gateway Services revenue grew 10.6% driven by strong air cargo demand, while Food Solutions revenue jumped 22% amid a rebound in aviation travel. Operating profit nearly doubled to S$475.7 million, lifting margins from 4.7% to 8.2%. Total equity rose to S$2.77 billion, and free cash flow turned positive at S$228.3 million, reflecting enhanced cash generation. SATS remains focused on debt reduction and reinvesting in operations to drive shareholder value.

Strategic expansion to capture future growth. SATS plans to invest over S$250 million to modernize and expand its ground support and cargo handling capabilities at Changi Airport, positioning itself ahead of Terminal 5’s expected opening in the mid-2030s. This includes more than S$150 million to renew and electrify over 40% of its ground support fleet within five years, and S$100 million to enhance cargo operations, boosting peak handling capacity by over 50%. SATS will also upskill its 7,800-strong workforce and adopt technologies such as autonomous vehicles and AI to meet rising air traffic and maintain Singapore’s status as a top global air hub. Looking ahead, we believe these initiatives will fortify SATS’ competitive position, support robust passenger and cargo growth and ensure long-term value creation as Singapore Changi Airport expands.

4Q25 Business Updates. SATS Ltd reported 10.4% YoY revenue growth to S$1,476.7mn from S$1,337.7mn in the corresponding year-ago period, driven by increased business volume and rate improvements. Its net profit rose 18.3% YoY to S$38.7mn from S$32.7mn in 4Q24, delivering EPS of S$0.026 for the quarter. After shareholder approval, its proposed final dividend of S$0.035 per share will be distributed on 15 August, higher than the final dividend of S$0.015 per share in 4Q24.

Market consensus

(Source: Bloomberg)

Seatrium Ltd (STM SP): Growth from cross-border cooperation

BUY Entry – 2.02 Target – 2.18 Stop Loss – 1.94

Seatrium Ltd offers engineering solutions for the offshore, marine, and energy industries. The Company provides rigs and floaters, repairs and upgrades, offshore platforms, and specialized shipbuilding. Seatrium serves customers worldwide.

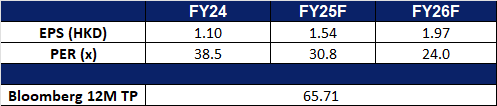

Strong order book. Seatrium reported a net order book of $21.3 billion as of March 31, spanning 26 projects with deliveries up to 2031, of which $7.1 billion are linked to renewables and green solutions. Despite global uncertainties, Seatrium maintains a steady pipeline of oil and gas projects, with significant progress in FPSO construction for South America and Petrobras. The company is also expanding into offshore renewables, with projects in Europe, Asia, and Taiwan. Offshore wind remains strong in Europe and Asia Pacific, despite challenges in the US. Its CEO noted minimal supply chain issues and said the company’s diversification in energy transition positions it well. Seatrium also reported completing 45 repair and upgrade projects in Q1, including cruise ship retrofits and carbon capture upgrades. The company returned to profitability in 2024, posting a net profit of $157 million.

Continued offshore milestones and strategic growth. Seatrium has strengthened its leadership in offshore engineering with the successful delivery of its 18th FPSO to BW Offshore, the BW Opal, which will serve Australia’s Barossa Field while significantly cutting emissions. Further cementing its market dominance, Seatrium secured a major FSRU conversion contract with Höegh Evi for the LNG carrier Hoegh Gandria, set for deployment in Egypt. These achievements reinforce Seatrium’s proven capabilities and trusted partnerships in the energy sector, driving continued growth in complex FPSO and FSRU projects.

Asean-GCC-China collaboration driving future opportunities. At the Asean-GCC Summit, Singapore Prime Minister Lawrence Wong called for deeper economic, energy, and digital cooperation among Asean, the GCC, and China, highlighting potential trade and investment deals like a region-to-region free trade agreement and collaboration on green energy and the digital economy. These initiatives can potentially benefit Seatrium by opening new markets and fostering opportunities in energy transition projects, digitalisation in shipyard operations, and clean energy infrastructure—especially with the GCC’s backing for the Asean Power Grid and the digital economy frameworks. As these regions work on cross-border energy grids, infrastructure financing, and digital governance, Seatrium could find itself well-positioned to leverage its engineering and offshore expertise, particularly in clean energy and digital solutions, to tap into these emerging opportunities.

FY24 results review. Revenue rose by 26.6% YoY to S$9.23bn in FY24, compared to S$7.29bn in FY23. Net profit was S$155.9mn in FY24, compared to a net loss of S$2.03bn in FY23. Basic EPS per share was 4.61 S cents in FY24, compared to net loss per share of 64.77 S cents in FY23.

Market consensus

(Source: Bloomberg)

Trip.com Group Ltd. (9961 HK): Upcoming favourable seasonalities

BUY Entry – 490 Target – 550 Stop Loss – 460

Trip.com Group Ltd is a China-based company mainly engaged in the operation of one-stop travel platform. The Company’s platform integrates a comprehensive suite of travel products and services and differentiated travel content. Its platform aggregates its product and service offerings, reviews and other content shared by its users based on their real travel experiences, and original content from its ecosystem partners to enable leisure and business travelers to have access to travel experiences and make informed and cost-effective bookings. Users come to its platform for any type of trip, from in-destination activities, weekend getaways, and short-haul trips, to cross-border vacations and business trips.

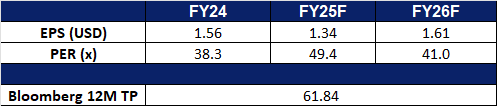

Favourable seasonalities ahead. China’s National Immigration Administration (NIA) expects an average of 2.15 million cross-border trips per day during the Dragon Boat Festival holiday, marking a 12.2% increase from the same period last year. The holiday, which runs from May 31 to June 2, is anticipated to drive a notable rise in travel activity. Major transportation hubs, such as Shanghai Pudong International Airport, are preparing for heightened passenger traffic, with the airport forecasting 100,000 daily border crossings. Dragon boat races and cultural events in Guangdong, Hong Kong, and Macao are also expected to draw both domestic and international visitors, further boosting travel demand. Looking ahead, the summer peak travel season from late June through August is likely to sustain this momentum. Trip.com stands to benefit from the continued recovery and seasonal increase in travel demand.

Deepening expansion in Vietnam. In a strategic push to expand its footprint in Southeast Asia, Trip.com Group has announced plans to deepen its presence in Vietnam, positioning the country as a key growth market alongside Indonesia and the Philippines. Over the past year, the company has established an office in Hanoi and is exploring the possibility of opening a second location in Da Nang. As part of its expansion strategy, Trip.com is scaling up its local workforce and broadening its service offerings in Vietnam. The company has also made several strategic moves in the market, including a $10 million investment in co-living startup M Village, a partnership with Vietjet, and a strategic alliance with hospitality group Vinpearl. According to Trip.com, demand for travel to Vietnam has surged, with growth approaching triple digits. As travel momentum continues to build, the company is well-positioned to capitalize on increased tourism activity and further strengthen its market presence in Vietnam.

Initiatives to drive growth. Trip.com Group has launched a 1 billion yuan (approximately US$140 million) Tourism Innovation Fund to support forward-thinking initiatives and talent in the travel sector. Announced during the company’s Global Partner Summit on May 26 in Shanghai, the fund is designed to drive innovation in travel services and customer experiences, with a focus on product development, digital transformation, and cross-border collaboration. As part of its broader strategic agenda, Trip.com also revealed new partnerships with hotel groups in Thailand, Malaysia, and Indonesia. These collaborations aim to elevate hospitality standards across Southeast Asia through joint marketing efforts and service enhancements. In addition, to boost inbound tourism to China, Trip.com is establishing “two-way service hubs” in 10 domestic cities and with five overseas tour operators. These hubs are intended to improve connectivity between Chinese destinations and global travel agencies, streamlining the travel experience for both inbound and outbound tourists.

1Q25 earnings. NetRevenue increased by 15.9% YoY to RMB13.8bn in 1Q25, compared to RMB11.9bn in 1Q24. Net profit remained flat YoY at RMB4.3bn in 1Q25, same as a year ago period. Diluted EPS fell to RMB6.09 in 1Q25, compared to RMB6.38 in 1Q24.

Market consensus.

(Source: Bloomberg)

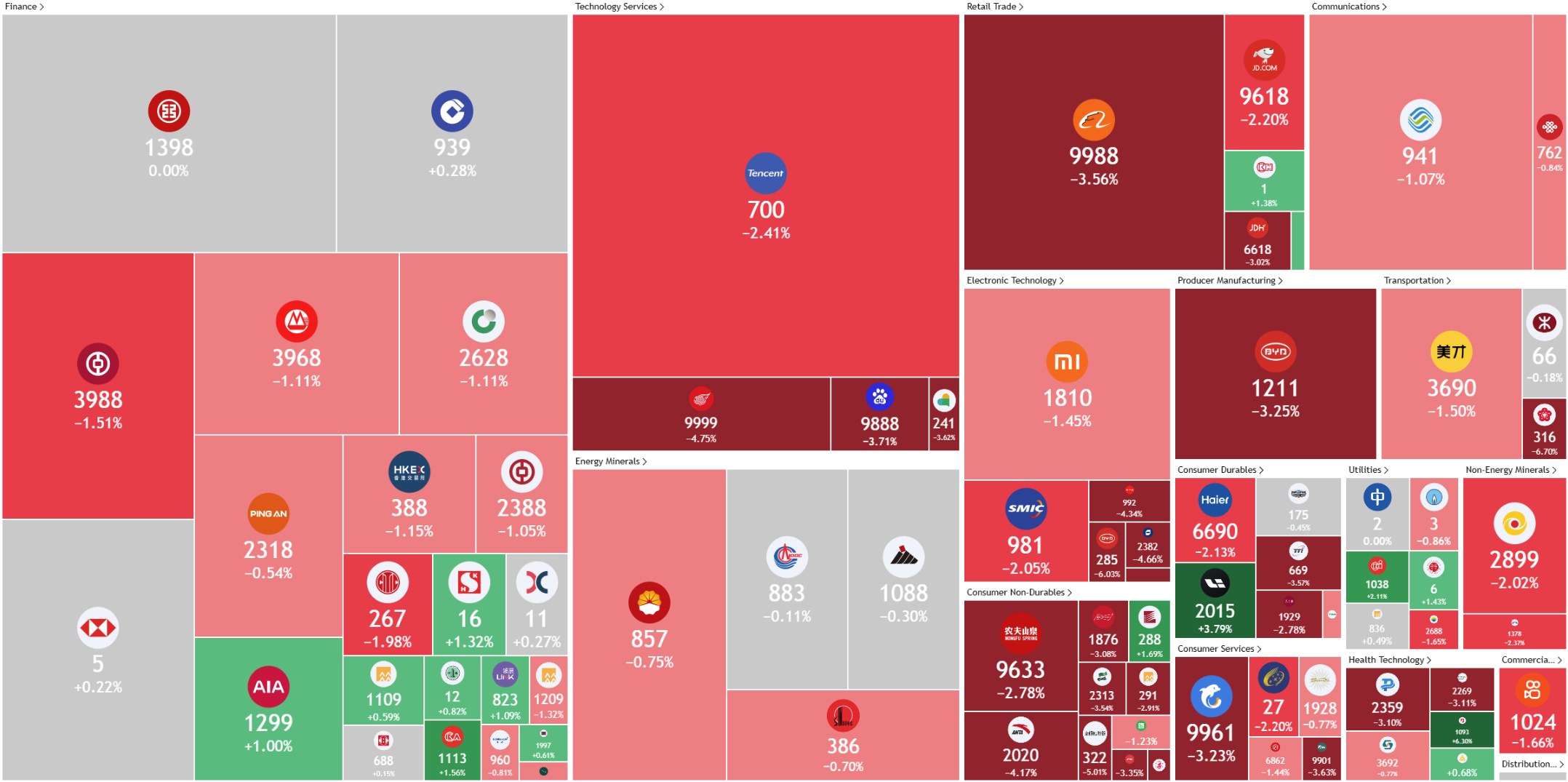

Xiaomi Corp. (1810 HK): Strength across different markets

Xiaomi Corp is an investment holding company primarily engaged in the research and development and sales of smartphones, the Internet of Things (IoT) and consumer products. The Company conducts its businesses primarily through four segments. The Smartphone segment is primarily engaged in the sales of smartphones. The IoT and lifestyle products segment primarily sells other in-house products (including smart TVs, laptops, artificial intelligence (AI) speakers and smart routers), ecological chain products (including IoT and other smart hardware products) and some consumer products. The Internet Services segment provides advertising services and Internet value-added services such as online games and fintech businesses. The Other segment provides hardware product repair services. The Company is also engaged in smart electric vehicles and other related businesses.

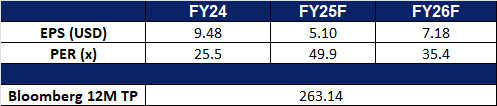

Upcoming Launch of YU7 SUV in July. Xiaomi has announced the upcoming launch of its highly anticipated YU7 SUV, set for official release in July. Static displays of the YU7 began on May 29 across 13 Xiaomi stores in Beijing, with a broader rollout to 92 cities nationwide throughout June. The company will also showcase the YU7—alongside its SU7 sedan and SU7 Ultra—at the 2025 Guangdong-Hong Kong-Macao Greater Bay Area Auto Show, taking place from May 31 to June 8 at the Shenzhen World Exhibition & Convention Centre. The YU7 aims to expand Xiaomi’s EV lineup and directly challenge competitors such as Tesla’s Model Y in China’s fast-evolving electric vehicle market.

Smartphone Leadership and Premiumization Strategy. In Q1 2025, Xiaomi reclaimed the No. 1 position in China’s smartphone market for the first time in a decade, with shipments rising to 13.3 million units—up from 9.5 million a year earlier—boosting market share from 14% to 19%. This growth was driven by strong synergies across Xiaomi’s smartphone, AIoT, and smart mobility ecosystems, along with support from national subsidy programs. Looking ahead, the company is intensifying its smartphone premiumization strategy, focusing on higher-margin mid- to high-end models over volume expansion. While broader market growth is expected to moderate, Xiaomi is positioning itself for long-term profitability through a refined product mix and continued innovation in AI and hardware integration.

Introduction of MiMo, Xiaomi’s First Open-Source LLM. Xiaomi has unveiled MiMo, its first open-source large language model (LLM), specifically designed for complex reasoning tasks. Despite its relatively compact 7-billion-parameter architecture, MiMo has outperformed significantly larger models—such as OpenAI’s o1-mini and Alibaba’s Qwen-32B-Preview—on key public benchmarks like AIME24-25 (math reasoning) and LiveCodeBench v5 (code generation). Developed by Xiaomi’s specialized AI division, Core, the model leverages advanced pretraining and post-training techniques to enhance its reasoning capabilities. The launch of MiMo marks a strategic move to embed generative AI more deeply across Xiaomi’s hardware ecosystem—including smartphones and its growing electric vehicle (EV) portfolio—potentially enabling more seamless user experiences and strengthening its competitive edge.

1Q25 earnings. Revenue increased by 47.4% YoY to RMB111.3bn in 1Q25, compared to RMB75.5bn in 1Q24. Net profit increased by 161.0% to RMB10.9bn in 1Q25, compared to RMB4.17bn in 1Q24. Basis EPS rose to RMB0.44 in 1Q25, compared to RMB0.17 in 1Q24.

Market consensus.

(Source: Bloomberg)

Robinhood Markets, Inc. (HOOD US): Crypto and market volatility spurring volume

BUY Entry – 64 Target – 72 Stop Loss – 60

Robinhood Markets, Inc. operates a financial services platform. The Company offers brokerage and cash management applications such as stocks, exchange-traded funds, options, and cryptocurrency. Robinhood Markets serves clients in the United States.

Expanding cryptocurrency business. Robinhood recently announced the acquisition of Canadian cryptocurrency company WonderFi for CA$250 million (approximately US$178 million) in cash, further strengthening its crypto operations. WonderFi owns two of Canada’s largest regulated crypto platforms, Bitbuy and Coinsquare, which will be integrated into Robinhood Crypto, expanding the company’s presence in Canada. WonderFi reported over CA$3.57 billion in trading volume in fiscal year 2024, a 28% year-over-year increase, with approximately 1.6 million users. This acquisition is expected to close in the second half of 2025 and follows Robinhood’s acquisition of Bitstamp in 2024, demonstrating its ambition to become a key player in the global crypto market. With the launch of the first U.S. XRP futures ETF, Robinhood is preparing to capture more market share.

Market volatility boosts trading volume. Robinhood reported an 84% YoY surge in first-quarter equity trading volume, while options trading volume hit a new high, further driving performance growth. Interest-earning assets and securities lending activities also expanded, offsetting the impact of short-term interest rates, while Robinhood Gold subscriptions reached a new peak. Amid current market volatility, a significant return of retail investors has fueled increased trading volume, further boosting revenue. In the short term, ongoing market turbulence is expected to continue attracting retail participation, further driving Robinhood’s revenue growth and enhancing its short-term upside potential.

1Q25 performance exceeds expectations. For 1Q25, revenue increased 50% year-over-year to US$927 million, surpassing expectations by US$9.84 million. GAAP EPS was US$0.37, exceeding expectations by US$0.04. Transaction-based revenue increased 77% year-over-year to US$583 million, primarily contributed by cryptocurrency trading (US$252 million). Average revenue per user increased 39% year-over-year to US$145.

Coinbase Global, Inc. provides financial solutions. The Company offers platform to buy and sell cryptocurrencies. Coinbase Global serves clients worldwide.

GENIUS ACT helps expand stablecoin scale. The U.S. Senate recently passed the “Guidance and Establishment of American Stablecoin Innovation Act” (GENIUS ACT), which requires institutions issuing stablecoins to hold reserves on a 1:1 basis. The reserve assets include U.S. dollars, time deposits, short-term U.S. Treasury bonds, repurchase agreements, and other highly liquid assets. The current stablecoin market size has reached $232 billion, and with the implementation of this act, large financial institutions or companies are expected to enter the stablecoin market..

Rapid growth of stablecoin business. In the first quarter, Coinbase reported a record USDC market capitalization of $60 billion, with the average USDC balance on its platform growing 49% quarter-over-quarter to $12 billion. Revenue related to stablecoins increased 32% quarter-over-quarter to $298 million, driven by Coinbase’s strong partnership with Circle and its expanding stablecoin products, including B2B payment features targeted at startups and SMEs. As Coinbase prioritizes the adoption of USDC and expands its role in stablecoin payments, the company is expected to profit in this growing market, especially as enhanced regulation increases trust and usage of stablecoins. This accelerated adoption will directly translate to higher trading volumes and stable revenue sources, supporting a short-term rise in Coinbase’s stock price.

Results exceeded expectations. In the first quarter of FY25, revenue reached US$2.03bn, a 23.8% YoY increase, missing estimates by US$60mn. Non-GAAP earnings per share were US$1.94, missing estimates by US$0.04. First-quarter trading revenue was US$1.26bn, a 16.7% YoY increase; subscription and service revenue was US$698mn, a 36.6% YoY increase.

1Q25 results. Revenue rose 23.8% YoY to US$2.03bn, missing estimates by US$60mn. Non-GAAP earnings per share were US$1.94, missing estimates by US$0.04. For Q2, it expects subscription and services revenue to be between US$600mn and US$680mn, technology and development and general and administrative expenses to be in the range of US$700mn to US$750mn and sales and marketing to be in the range of US$215mn to US$315mn.

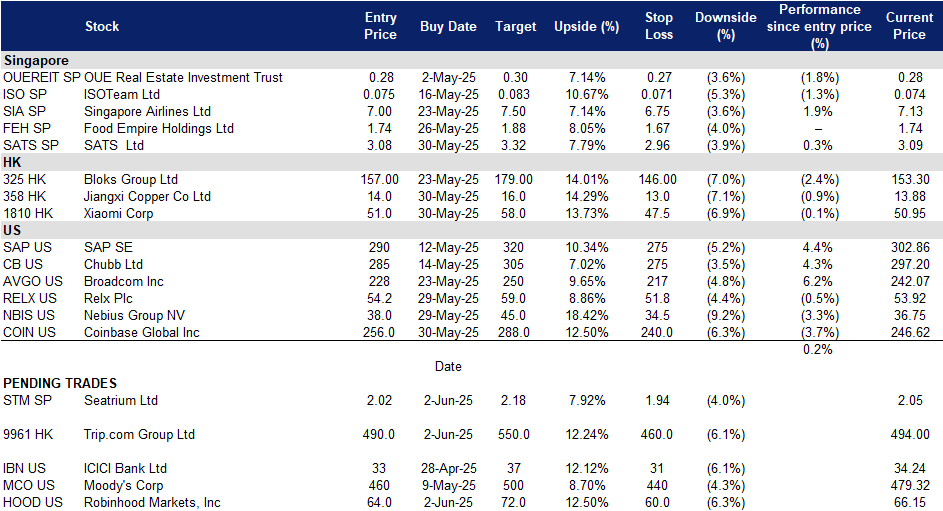

Trading Dashboard Update: Take profit on Costco Wholesale Corp (COST US) at US$1,050. Add SATS Ltd (SATS SP) at S$3.08, Jiangxi Copper Co Ltd (358 HK) at HK$14, Xiaomi Corp (1810 HK) at HK$51, Relx Plc (RELX US) at US$54.2, Coinbase Global Inc (COIN US) at US$256 and Nebius Group NV (NBIS US) at US$38. Cut loss on BYD Co Ltd (1211 HK) at HK$425 and Arm Holdings Plc (ARM US) at US$124.