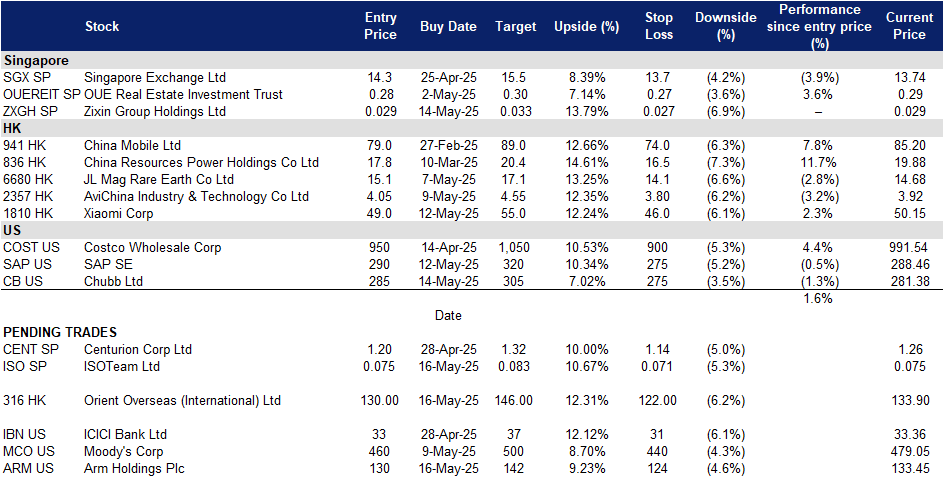

ISOTeam Ltd (ISO SP): Leveraging public sector demand and sustainability tailwinds

BUY Entry – 0.075 Target– 0.083 Stop Loss – 0.071

ISOTeam Ltd. is a building maintenance and estate upgrading company experienced in implementing eco-driven solutions through R&R and A&A services to the public and private sector. The Company has extensive experience in upgrading, retrofitting and maintenance of buildings and facilities in Singapore, and reshapes and rejuvenates public housing landscape, amenities, and environment.

Robust and diversified order book. As of February 2025, ISOTeam’s outstanding order book stood at S$188.7mn, providing clear revenue visibility through FY29. The Group is well positioned to capture recurring demand from upgrading, sustainability retrofits, and infrastructure enhancement projects.

Technology driven productivity gains. ISOTeam is on track to commercialise autonomous facade cleaning and painting drones by end-2025 via ISOTeam BuildTech. With 18 drones targeted and Civil Aviation Authority of Singapore (CAAS) permits pending, this first-mover advantage is set to enhance efficiency and reduce labour reliance in maintenance works.

Structural tailwinds underpin multi-year growth visibility. ISOTeam is well-positioned to capitalise on Singapore’s sustained public sector upgrading and green initiatives. Its core Repairs & Redecoration (R&R) and Addition & Alteration (A&A) services align with recurring programmes like the Home Improvement Programme (HIP), Neighbourhood Renewal Programme (NRP) and the planned launch of over 50,000 BTO flats from 2025-2027. These works, typically recurring every five to ten years, underpin long-term revenue visibility. ISOTeam has also expanded into sustainability-linked projects, such as solar installations with Singapore’s 2 GWp by 2030 target. Its Coating & Painting (C&P) segment also supports HDB initiatives to mitigate the Urban Heat Island (UHI) effect through heat-reflective coatings. The Group’s early adoption of robotics, drones, and AI-powered painting solutions enhances productivity and mitigates labour constraints. Backed by its robust order book, ISOTeam offers clear earnings visibility and sustained multiyear growth potential.

1H25 financial results. ISOTeam delivered a strong performance in 1H25, with revenue rising by 4.2% YoY to S$65.4mn, up from S$62.7mn in 1H24. This growth was driven by higher contributions from its Addition & Alteration (A&A) segment, which saw a 61.6% YoY jump in revenue to S$30.3mn in 1H25, up from S$18.7mn in 1H24. Gross profit rose 18.4% YoY to S$9.9mn in 1H25, reflecting improved margins from projects secured post-COVID-19. Additionally, the company reported a net profit attributable to shareholders of S$1.9mn, a 36.5% increase compared to S$1.4mn in 1H24.

We have fundamental coverage with a BUY recommendation and a TP of S$0.100. Please read the full report here.

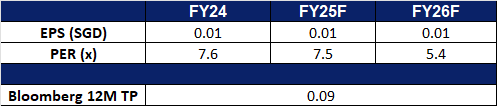

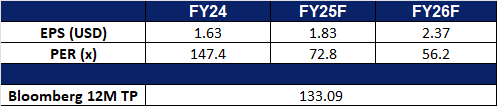

Market Consensus.

(Source: Bloomberg)

Zixin Group Holdings Ltd (ZXGH SP): Plenty of growth potential

Zixin Group Holdings Limited is a holding company. The Company, through its subsidiaries, operates sweet potato biotech-focused value chain focuses on cultivation and supply, product innovation and snacks production, brand building, marketing, and distribution.

Further expansion into Hainan. Zixin Group is expanding its sweet potato value chain from Liancheng County, Fujian, to Lingao County, Hainan, through a Revitalisation Project covering 8,961.33 hectares across 12 villages. This new land in Hainan is significantly larger than their original area in Fujian, offering substantial replication potential. Although currently in the initial stages, the group anticipates realizing profits from this expansion starting in FY2027. This strategic move marks Zixin’s first replication of its model outside Fujian, demonstrating its growth ambitions in the agricultural sector.

Breakthrough in new snack products. Zixin Group recently announced that it has achieved a breakthrough in the production of sweet potato chips and fries snack products. The company has begun to deliver the substantial orders received in February 2025 for these new products from its network of distributors. These products have also received significant demand, and Zixin has ramped up its production capacity at its existing snack manufacturing facility.

Improving margins. Zixin Group saw an improvement in margins YoY in FY2024. The company’s gross profit margin (GPM) rose to 32.0% in FY24, largely attributed to higher sales and lowered costs due to economies of scale. The company also recorded an operating profit margin (OPM) of 6.9% and a net profit margin (NPM) of 4.2%, highest in over 5 years, largely attributed to lower costs relative to revenue. These improving margins showcased the initial results of Zixin Group’s integrated industrial value chain, which includes the supporting industry of cold storage warehousing services, enabling the company to recover from the post-Covid crisis and return to profitability.

1H25 financial results. Zixin Group Holdings reported total revenue of RMB156.7mn in 1H25, representing a 33.1% YoY increase, compared with a revenue of RMB117.8mn in 1H24. The company continues to make strong progress on its integrated circular economy industrial value chain across business operations, driving significant and organic growth in financial performance. Net profit after tax increased to RMB7.73mn in 1H25, compared to a net loss after tax of RMB3.40mn in 1H24. The group’s basic EPS was 0.54 RMB cents in 1H25, compared to a loss per share of 0.25 RMB cents in 1H24.

We have fundamental coverage with a BUY recommendation and a TP of S$0.060. Please read the full report here.

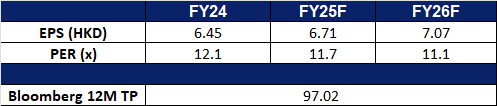

China Mobile Ltd is a company mainly engaged in the provision of communication and information services. The Company’s businesses include customer market business, home market business, business market business and new market business. The customer market business mainly provides fifth-generation mobile communication technology (5G) mobile services and brand differentiated service operations. The home market business mainly provides home wired broadband services, mobile housekeeping smart services and smart home value-added services. The business market business is engaged in the research and development and sales of cloud computers and Internet of Things card services. The new market business includes international business, equity investment, digital content and financial technology.

AI integration. Earlier this month, China Mobile, along with other major Chinese telecom companies, announced the integration of DeepSeek’s artificial intelligence (AI) models into their services and products. The move follows a broader trend among the country’s top tech firms, including Alibaba Group, Tencent Holdings and Baidu Inc, which have ramped up support for DeepSeek’s latest AI models on their respective platforms. While these telecom giants have been developing their own large language models (LLMs) over the past two years amid a global AI boom spurred by OpenAI, they primarily leverage DeepSeek’s models for cloud-based applications. China Mobile, in particular, has incorporated DeepSeek’s full suite of models—from DeepSeek-V1 to the latest DeepSeek-R1—into its computing platform. This enables businesses of all sizes to access the models, deploy application programming interfaces (APIs), and build new AI agents on its platform.

Growth in smart devices and 5G adoption. China’s mobile phone market experienced robust growth in 2024, with total shipments increasing by 8.7% to 314 million units. Notably, December 2024 saw a significant YoY surge of 22.1%, reaching 34.53 million units. 5G smartphones dominated the market, accounting for 88.1% of December shipments and 86.6% of total annual shipments. This trend is supported by China’s rapidly expanding 5G infrastructure, which now includes over 4.25 million 5G base stations and serves more than 1 billion 5G users. The rise in smart device adoption, particularly 5G-enabled phones, is expected to drive an expansion of China Mobile’s customer base, as more users seek high-speed connectivity and advanced mobile services.

Strategic cooperation agreement to deepen AI development. China Mobile recently announced a strategic cooperation agreement with Chengdu City to deepen collaboration across multiple sectors. Under this agreement, the two parties will enhance infrastructure development in AI, 5G-A, and next-generation networks, drive technological innovation and commercialization, and strengthen partnerships in areas such as supply chains, industrial investment, and intelligent hardware. They will also explore opportunities in smart cities, the data industry, 5G-powered industrial internet applications, and the low-altitude economy, fostering high-quality growth in Chengdu’s electronic information and audio-entertainment industries. This initiative is expected to further position China Mobile to capitalize on China’s expanding AI landscape.

9M24 earnings. Revenue rose by 2.0% YoY to RMB791.5bn in 9M24, compared to RMB775.6bn in 9M23. Profit attributable to equity shareholders was RMB110.9bn, up by 5.1% YoY from RMB105.5bn. Basic earnings per share was RMB5.18 in 9M24, compared to a basic earnings per share of RMB4.94 in 9M23.

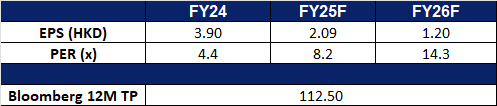

Orient Overseas (International) Limited is an investment holding company principally engaged in container transport and logistics businesses. Along with subsidiaries, the Company operates its business through two segments: the Container Transport and Logistics segment, as well as the Others segment. The Container Transport and Logistics segment is engaged in the provision of global containerised shipping services in major trade lanes, covering Trans-Pacific, Trans-Atlantic, Asia/Europe, Asia/Australia and Intra-Asia trades. In addition, it also provides integrated services over the management and control of effective storage and flow of goods. The Others segment is involved in the commercial properties.

Expected surge in shipping demand. Transpacific container traffic is poised for a significant surge in the coming weeks, as businesses accelerate shipments to capitalize on a temporary easing of trade tariffs between the United States and China. The uptick follows a 90-day truce announced by both countries on Monday, which is expected to drive immediate demand for container shipping services. The agreement, reached during trade discussions in Switzerland over the weekend, includes a U.S. commitment to lower recently imposed tariffs on Chinese goods—from 145% to 30%—by eliminating 91 percentage points and suspending an additional 24 percentage points for the 90-day period. In response, China will reduce its retaliatory tariffs on U.S. imports from 125% to 10%. The tariff reductions are set to take effect on Wednesday. This anticipated spike in shipping volumes is expected to benefit carriers with strong transpacific exposure, including Orient Overseas (International) Ltd.

More routes. Orient Overseas Container Line (OOCL) has launched a direct shipping service to Quanzhou via its KTX2 route, strengthening connectivity to one of Fujian Province’s key economic centers, according to a company announcement. The new service establishes a direct Japan–Quanzhou link, offering competitive transit times and enhanced efficiency for regional trade flows. In addition to calling major ports, OOCL’s domestic feeder network allows cargo to be accepted from a wide range of regional Japanese ports, further expanding accessibility. This development is expected to support increased export volumes to Fujian Province and could contribute positively to OOCL’s revenue growth.

Expansion of fleet. Orient Overseas (International) Ltd. has announced that its subsidiaries have placed orders for 14 new container vessels with China COSCO Shipping Corporation, in a deal valued at approximately US$3.08 billion. The vessels will be equipped with methanol dual-fuel engines, a move the company says will enhance operational efficiency, reduce emissions, and strengthen its competitive positioning across both established and emerging markets. To finance the newbuild program, Orient Overseas plans to fund 60% of each vessel’s cost through a combination of bank loans and external debt, with the remaining 40% to be covered by internal resources. Deliveries are scheduled to take place between the third quarter of 2028 and the third quarter of 2029.

FY24 results review. Revenue increased by 28.3% YoY to US$10.7bn in FY24, compared with US$8.34bn in FY23. Net profit increased by 88.4% to US$2.58bn in FY24, compared to US$1.37bn in FY23. Basic EPS rose to US$3.90 in FY24, compared to US$2.07 in FY23.

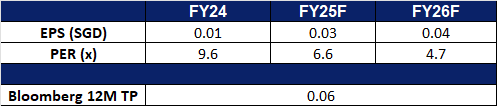

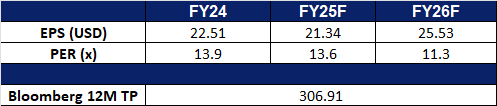

Market consensus.

(Source: Bloomberg)

Arm Holdings PLC. (ARM US): Benefitting from a big deal

BUY Entry – 130 Target – 142 Stop Loss – 124

ARM Holdings PLC operates as a holding company. The Company, through its subsidiaries, designs and manufactures semiconductor technology and other related products such as computer processors, memory controllers, internet protocol system, graphic processor, security, and storage devices. ARM Holdings serves automotive, infrastructure, and consumer technologies markets worldwide.

Tailwinds of accelerating AI demand. Arm is central to the AI and cloud computing revolution, with its energy-efficient architecture gaining adoption among hyperscalers like Google and Microsoft. By 2025, nearly half of all new server chips are expected to be Arm-based, underscoring its growing role in data centers, edge AI, and automotive systems. The recent US$600bn deal, announced during President Trump’s Middle East visit, fuelled a rally across AI infrastructure stocks. Arm stands to benefit indirectly from AI partnership initiatives with Saudi Arabia, as a key IP supplier to AI chipmakers. Combined with resilient enterprise tech demand and strong recurring revenue from partners like Nvidia and Amazon, Arm is well-positioned for multi-year growth amid rising global AI capex.

High-margin royalty and licensing expansion drive profitability. Arm’s record royalty and licensing revenue, each surpassing US$600mn last quarter, highlight the scalability of its asset-light, high-margin business model. New multi-year licensing deals, including in the automotive sector, and accelerating uptake of Armv9 CPUs and Compute Subsystems position the company to expand its market share and profitability across growth verticals like IoT, automotive, and AI.

4Q25 results. Revenue rose 33.6% YoY to US$1.24bn, above estimates by US$10mn. Its non-GAAP EPS of US$0.55 beat estimates by US$0.03. The company forecasts first quarter revenue of US$1.0bn to US$1.1bn, with a midpoint below analysts’ average estimate of US$1.1bn. Arm expects adjusted profit of US$0.30 to US$0.38 per share for the first quarter, compared with estimates of US$0.42.

Chubb Limited operates as a property and casualty insurance company. The Company provides commercial and personal property, casualty, and personal accident and supplemental health insurance, reinsurance, and life insurance to a diverse group of clients.

Expected premium increases. Higher raw material costs due to tariffs, coupled with the increased risk of claims from frequent natural disasters in North America since the beginning of the year, are expected to push up property replacement costs. Such inflationary pressures are expected to support the company’s premium increases in property insurance, further driving revenue growth, especially in a favorable underwriting environment.

Strategic expansion into Asian markets. The company’s acquisition of Liberty Mutual’s business in Thailand and Vietnam, which generated US$275 million in premium income in fiscal 2024, will effectively strengthen its layout in the high-growth insurance market in Asia Pacific. The expansion will help diversify its geographic revenue sources while also giving the company a better chance to tap into the growing insurance demand among the middle class in Asia’s emerging markets.

Performance exceeded expectations. Core operating earnings per share for the first quarter of fiscal year 25 were $3.68, higher than the market expectation of $3.23. Net premium income increased 3.6% year-on-year to US$12 billion, exceeding expectations by US$780 million. The annualized return on equity was 8.2%, the core operating tangible return on equity was 13%, and the core operating return on equity was 8.6%.

1Q25 results. Net income decreased by 37.9% YoY to US$1.33bn in 1Q25, compared with US$2.14bn in 1Q24. Core operating income, net of tax declined by 31.1% to US$1.49bn in 1Q25, compared to US$2.16bn in 1Q24.

Trading Dashboard Update: Takeprofit on Trip.com Group Ltd (9961 HK) at HK$520. Add Zixin Group Holdings Ltd (ZXGH SP) at S$0.029 and Chubb Ltd (CB US) at US$285.