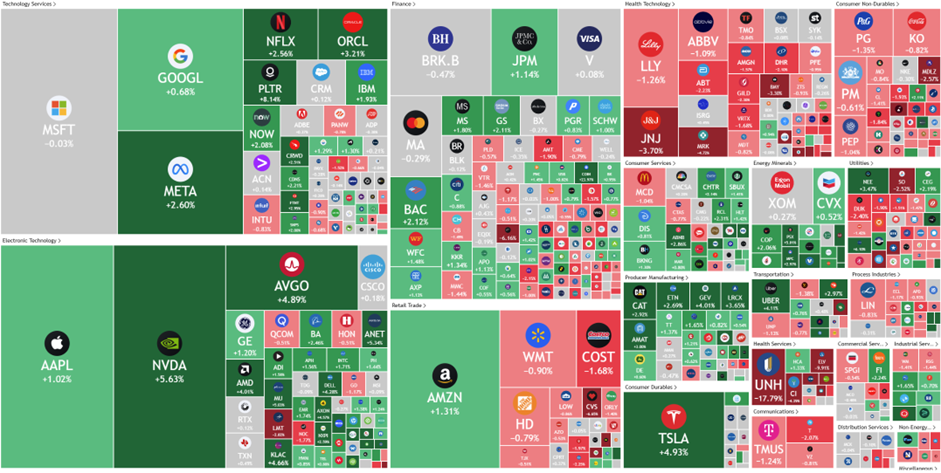

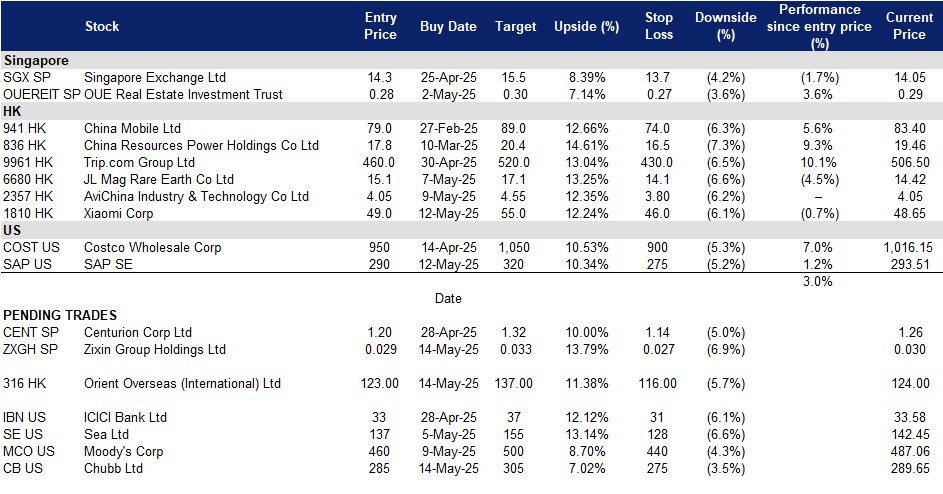

Zixin Group Holdings Ltd (ZXGH SP): Plenty of growth potential

BUY Entry – 0.029 Target– 0.033 Stop Loss – 0.027

Zixin Group Holdings Limited is a holding company. The Company, through its subsidiaries, operates sweet potato biotech-focused value chain focuses on cultivation and supply, product innovation and snacks production, brand building, marketing, and distribution.

Further expansion into Hainan. Zixin Group is expanding its sweet potato value chain from Liancheng County, Fujian, to Lingao County, Hainan, through a Revitalisation Project covering 8,961.33 hectares across 12 villages. This new land in Hainan is significantly larger than their original area in Fujian, offering substantial replication potential. Although currently in the initial stages, the group anticipates realizing profits from this expansion starting in FY2027. This strategic move marks Zixin’s first replication of its model outside Fujian, demonstrating its growth ambitions in the agricultural sector.

Breakthrough in new snack products. Zixin Group recently announced that it has achieved a breakthrough in the production of sweet potato chips and fries snack products. The company has begun to deliver the substantial orders received in February 2025 for these new products from its network of distributors. These products have also received significant demand, and Zixin has ramped up its production capacity at its existing snack manufacturing facility.

Improving margins. Zixin Group saw an improvement in margins YoY in FY2024. The company’s gross profit margin (GPM) rose to 32.0% in FY24, largely attributed to higher sales and lowered costs due to economies of scale. The company also recorded an operating profit margin (OPM) of 6.9% and a net profit margin (NPM) of 4.2%, highest in over 5 years, largely attributed to lower costs relative to revenue. These improving margins showcased the initial results of Zixin Group’s integrated industrial value chain, which includes the supporting industry of cold storage warehousing services, enabling the company to recover from the post-Covid crisis and return to profitability.

1H25 financial results. Zixin Group Holdings reported total revenue of RMB156.7mn in 1H25, representing a 33.1% YoY increase, compared with a revenue of RMB117.8mn in 1H24. The company continues to make strong progress on its integrated circular economy industrial value chain across business operations, driving significant and organic growth in financial performance. Net profit after tax increased to RMB7.73mn in 1H25, compared to a net loss after tax of RMB3.40mn in 1H24. The group’s basic EPS was 0.54 RMB cents in 1H25, compared to a loss per share of 0.25 RMB cents in 1H24.

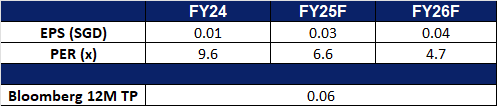

We have fundamental coverage with a BUY recommendation and a TP of S$0.060. Please read the full report here.

Market Consensus.

(Source: Bloomberg)

OUE Real Estate Investment Trust (OUEREIT SP): Refocused, resilient and ready for growth

OUE Real Estate Investment Trust (OUE REIT) provides real estate investment services. The Company invests in income-producing real estate used primarily for retail, hospitality, and office purposes in financial and business hubs, as well as real estate-related assets. OUE REIT serves customers in Singapore and China.

Softer quarter on divestment and hospitality pullback. OUE REIT reported a YoY decline in revenue and NPI of 11.9% and 12.1% respectively for 1Q25. The lower figures reflect the absence of contributions from Lippo Plaza, following its divestment in December 2024, as well as a softer hospitality performance amid a more subdued trading environment compared to the previous year.

Strategic divestment. As of 27 December 2024, OUE REIT successfully completed the divestment of Lippo Plaza in Shanghai for a sale consideration of RMB1,917.0mn (S$357.4mn). This divestment will enhance portfolio resilience and provide financial flexibility for future growth.

Tourism-led tailwinds. The Singapore Tourism Board projects international visitor arrivals to reach between 17 and 18.5 million in 2025, with tourism receipts forecasted at S$29.0bn – S$30.5bn. A robust line-up of leisure events, including Lady Gaga’s four-night concert in May and the Formula 1 Grand Prix, alongside other performances are expected to boost inbound travel, supporting demand for OUE REIT’s centrally located hotels and retail assets.

Proactive debt management. Financing costs declined 11.3% YoY to S$22.6mn in 1Q25, supported by active refinancing and interest rate hedging. The weighted average cost of debt fell to 4.2% per annum, down from 4.7% in the prior quarter. A 25-basis-point drop in interest rates could further boost DPU by an estimated 0.03 Scents, offering additional upside.

1Q25 results review. Revenue and net property income (NPI) declining by 11.9% and 12.1% YoY to S$66.0mn and S$53.2mn, respectively. These declines were largely due to the divestment of Lippo Plaza and lower contributions from the hospitality segment. On a like-for-like basis, revenue and NPI fell by a more modest 3.9% and 4.1% YoY, underscoring the resilience of its Singapore portfolio.

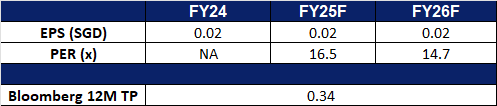

We have fundamental coverage with a BUY recommendation and a TP of S$0.318. Please read the full report here.

Orient Overseas (International) Limited is an investment holding company principally engaged in container transport and logistics businesses. Along with subsidiaries, the Company operates its business through two segments: the Container Transport and Logistics segment, as well as the Others segment. The Container Transport and Logistics segment is engaged in the provision of global containerised shipping services in major trade lanes, covering Trans-Pacific, Trans-Atlantic, Asia/Europe, Asia/Australia and Intra-Asia trades. In addition, it also provides integrated services over the management and control of effective storage and flow of goods. The Others segment is involved in the commercial properties.

Expected surge in shipping demand. Transpacific container traffic is poised for a significant surge in the coming weeks, as businesses accelerate shipments to capitalize on a temporary easing of trade tariffs between the United States and China. The uptick follows a 90-day truce announced by both countries on Monday, which is expected to drive immediate demand for container shipping services. The agreement, reached during trade discussions in Switzerland over the weekend, includes a U.S. commitment to lower recently imposed tariffs on Chinese goods—from 145% to 30%—by eliminating 91 percentage points and suspending an additional 24 percentage points for the 90-day period. In response, China will reduce its retaliatory tariffs on U.S. imports from 125% to 10%. The tariff reductions are set to take effect on Wednesday. This anticipated spike in shipping volumes is expected to benefit carriers with strong transpacific exposure, including Orient Overseas (International) Ltd.

More routes. Orient Overseas Container Line (OOCL) has launched a direct shipping service to Quanzhou via its KTX2 route, strengthening connectivity to one of Fujian Province’s key economic centers, according to a company announcement. The new service establishes a direct Japan–Quanzhou link, offering competitive transit times and enhanced efficiency for regional trade flows. In addition to calling major ports, OOCL’s domestic feeder network allows cargo to be accepted from a wide range of regional Japanese ports, further expanding accessibility. This development is expected to support increased export volumes to Fujian Province and could contribute positively to OOCL’s revenue growth.

Expansion of fleet. Orient Overseas (International) Ltd. has announced that its subsidiaries have placed orders for 14 new container vessels with China COSCO Shipping Corporation, in a deal valued at approximately US$3.08 billion. The vessels will be equipped with methanol dual-fuel engines, a move the company says will enhance operational efficiency, reduce emissions, and strengthen its competitive positioning across both established and emerging markets. To finance the newbuild program, Orient Overseas plans to fund 60% of each vessel’s cost through a combination of bank loans and external debt, with the remaining 40% to be covered by internal resources. Deliveries are scheduled to take place between the third quarter of 2028 and the third quarter of 2029.

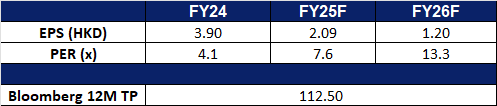

FY24 results review. Revenue increased by 28.3% YoY to US$10.7bn in FY24, compared with US$8.34bn in FY23. Net profit increased by 88.4% to US$2.58bn in FY24, compared to US$1.37bn in FY23. Basic EPS rose to US$3.90 in FY24, compared to US$2.07 in FY23.

Market consensus.

(Source: Bloomberg)

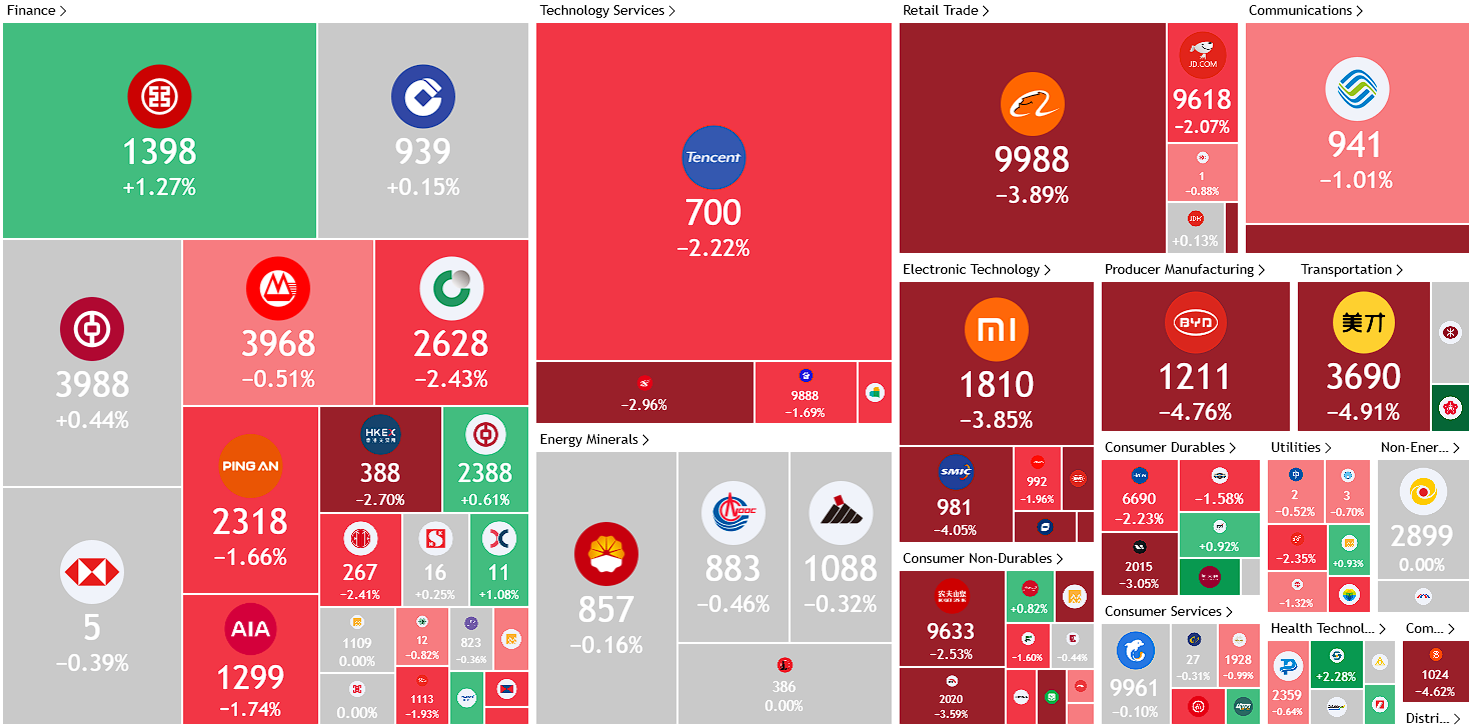

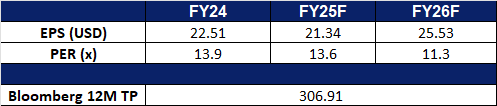

AviChina Industry & Technology Co Ltd. (2357 HK): Credibility in China’s defense technology

AviChina Industry & Technology Co Ltd is a China-based company principally engaged in the research, development, manufacture and sale of aviation products and relevant engineering services. The Company operates its businesses through three segments. The Aviation Entire Aircraft segment mainly includes providing helicopters, trainer aircraft, general-purpose aircraft and regional jets for domestic and overseas customers. The Aviation Ancillary System and Related Business segment mainly includes avionics products, mechanical electronics, connectors and its accessories. The Aviation Engineering Services segment mainly includes providing planning, design, consultation, construction, operation and other services. The Company mainly operates its businesses in the domestic market.

Increasing conflicts between Pakistan and India. Pakistan and India recently saw an increase in conflicts after a terrorist attack near Pahalgam, Kashmir. This has resulted in an Indian airstrike, followed by a clash between the countries’ fighter jets. The confrontation marks the latest escalation of a decadeslong conflict over Kashmir, which is wedged between the two nuclear-armed nations. This conflict would increase both countries’ defense spending, benefiting aerospace and defense companies in the region, which include China based’s AviChina Industry & Technology.

Strength of China’s aerospace and defense technology. Pakistan’s Deputy Prime Minister Ishaq Dar confirmed that J-10C fighter jets, acquired from China, were deployed in response to recent Indian airstrikes. His remarks follow speculation about the involvement of Chinese-made military hardware in the clashes, during which Pakistan claimed to have downed five Indian aircraft. The reported operational use of the J-10C in active combat marks a significant milestone, enhancing the aircraft’s appeal in the global defense market. A “battle-tested” designation is a notable advantage for military exports, lending credibility and boosting demand. This development also enhances the reputation of China’s defense industry. AviChina, a key player within the broader AVIC (Aviation Industry Corporation of China) ecosystem, stands to benefit indirectly from heightened international interest and improved perceptions surrounding Chinese military aviation technologies.

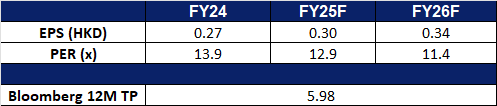

FY24 results review. Revenue increased by 2.62% YoY to RMB87.0bn in FY24, compared with RMB84.8bn in FY23. Net profit declined by 10.6% to RMB2.19bn in FY24, compared to RMB2.45bn in FY23. Basic EPS fell to RMB0.274 in FY24, compared to RMB0.311 in FY23.

Market consensus.

(Source: Bloomberg)

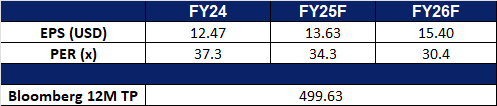

Chubb Ltd. (CB US): Higher premiums

BUY Entry – 285 Target – 305 Stop Loss – 275

Chubb Limited operates as a property and casualty insurance company. The Company provides commercial and personal property, casualty, and personal accident and supplemental health insurance, reinsurance, and life insurance to a diverse group of clients.

Expected premium increases. Higher raw material costs due to tariffs, coupled with the increased risk of claims from frequent natural disasters in North America since the beginning of the year, are expected to push up property replacement costs. Such inflationary pressures are expected to support the company’s premium increases in property insurance, further driving revenue growth, especially in a favorable underwriting environment.

Strategic expansion into Asian markets. The company’s acquisition of Liberty Mutual’s business in Thailand and Vietnam, which generated US$275 million in premium income in fiscal 2024, will effectively strengthen its layout in the high-growth insurance market in Asia Pacific. The expansion will help diversify its geographic revenue sources while also giving the company a better chance to tap into the growing insurance demand among the middle class in Asia’s emerging markets.

Performance exceeded expectations. Core operating earnings per share for the first quarter of fiscal year 25 were $3.68, higher than the market expectation of $3.23. Net premium income increased 3.6% year-on-year to US$12 billion, exceeding expectations by US$780 million. The annualized return on equity was 8.2%, the core operating tangible return on equity was 13%, and the core operating return on equity was 8.6%.

1Q25 results. Net income decreased by 37.9% YoY to US$1.33bn in 1Q25, compared with US$2.14bn in 1Q24. Core operating income, net of tax declined by 31.1% to US$1.49bn in 1Q25, compared to US$2.16bn in 1Q24.

Market consensus

(Source: Bloomberg)

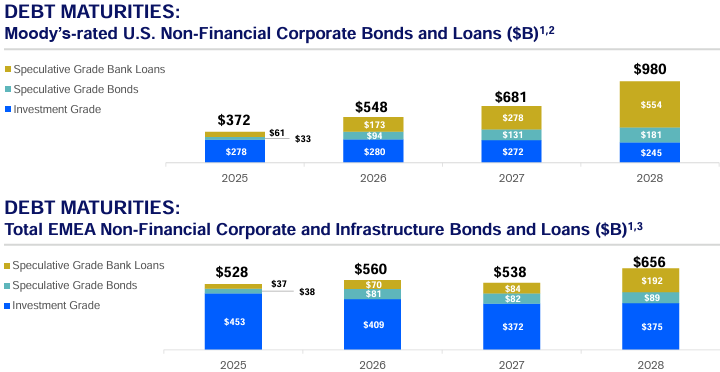

Moody’s Corp (MCO US): Stable, scalable and diversified

Moody’s Corporation is a credit rating, research, and risk analysis firm. The Company provides credit ratings and related research, data and analytical tools, quantitative credit risk measures, risk scoring software, and credit portfolio management solutions and securities pricing software and valuation models.

Robust issuance pipeline. More than US$4 trillion in debt maturities expected across the U.S. and EMEA between 2025-2028 will likely fuel refinancing and new issuance activity, providing a steady flow of business for Moody’s.

Launch of independent risk assessments. MSCI and Moody’s have announced a strategic partnership to deliver the first large-scale, independent risk assessment solution for private credit investments. Leveraging MSCI’s extensive private capital data and Moody’s EDF-X credit risk models, will provide transparent, third-party risk assessments at both the company and facility level. As private credit markets expand, the collaboration aims to offer investors standardized tools to benchmark credit risk, inform investment decisions, and monitor portfolios more effectively, while increasing transparency and consistency in the market. The launch is well-timed to capture rising investor demand for private markets.

Resilient, diversified revenue streams. Despite a slightly lowered full-year outlook, Moody’s Q1 highlight the strength of its diversified, service-centric model. Both Moody’s Analytics’s (MA) recurring revenue, which accounts for 96% of its total revenue, grew 9% YoY, underpinned by 12% growth in Decision Solutions and 8% overall revenue growth, demonstrating the success of its strategic pivot toward subscription-based offerings. Annualized recurring revenue (ARR) rose to US$$3.3bn, reflecting continued demand for data-driven risk and decision solutions. Simultaneously, Moody’s Investors Service (MIS) posted its highest-ever quarterly revenue of US$1.1bn, driven by an 8% rise in transactional revenue and strong momentum in investment-grade corporate finance and structured finance, particularly in private credit-related transactions. As investor appetite for high-quality and private credit assets persists, Moody’s resilient revenue base, anchored by recurring subscriptions and broad market exposure, positions it well to navigate macro uncertainty and sustain long-term growth.

1Q25 results. Moody’s Corp delivered an 8% increase in revenue to US$1.92bn, beating estimates by US$40mn. Non-GAAP Earnings per share was US$3.83, beating estimates by US$0.29. The company lowered its full-year 2025 guidance with expectations of revenue growth in the mid-single digits and an adjusted operating margin between 49% and 50%. It anticipates adjusted diluted EPS for the year to range from US$13.25 to US$14.00. Moody’s also plans to repurchase at least US$1.3bn in shares and expects free cash flow between US$2.3bn and US$2.5bn.

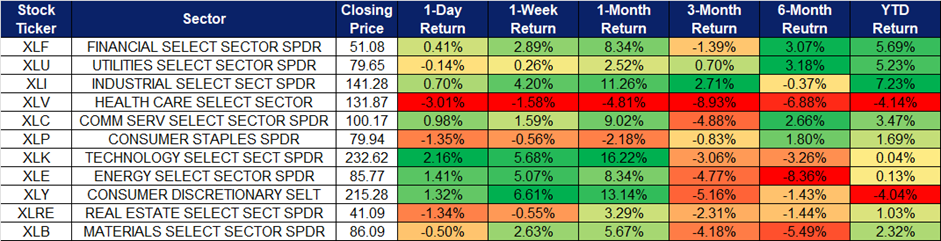

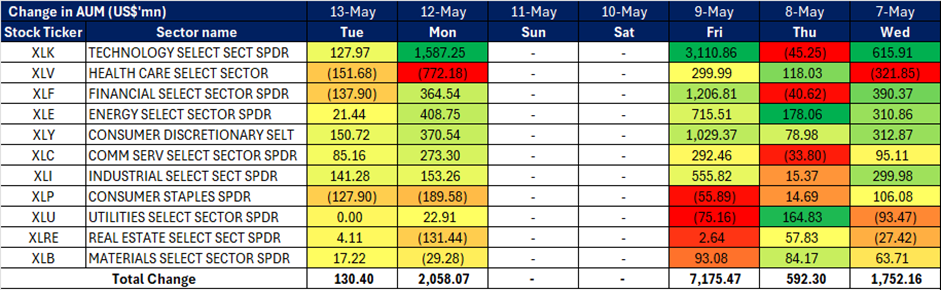

Trading Dashboard Update: Takeprofit on China Merchant Banks Co Ltd (3968 HK) at HK$47.5. Add AviChina Industry & Technology Co Ltd (2357 HK) at HK$4.05, Xiaomi Corp (1810 HK) at HK$49.0 and SAP SE (SAP US) at US$290. Cut loss on American Water Works Co Inc. (AWK US) at US$140 and Consolidated Edison Inc. (ED US) at US$105.