Technical Analysis – 3 September 2024

United States | Singapore | Hong Kong | Earnings

Clorox Co (CLX US)

- Shares closed at a 52-week high above the 5dEMA with rising volume.

- MACD is constructive, while RSI is at an overbought level.

- Long – Entry 158 Target 170, Stop 152

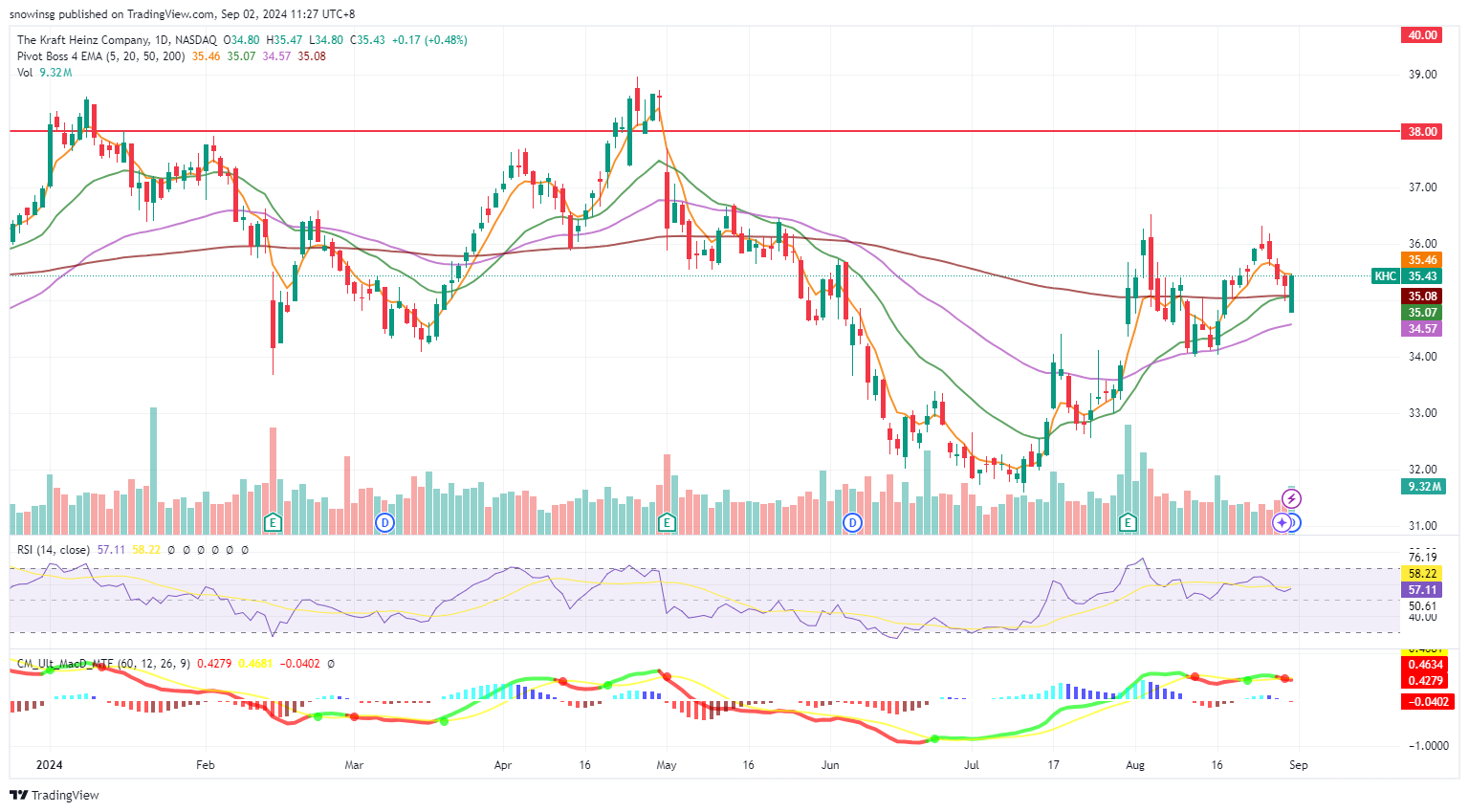

Kraft Heinz Co (KHC US)

- Shares closed above the 200dEMA with rising volume. The 20dEMA crossed the 200dEMA.

- RSI is constructive, while MACD is negative.

- Long – Entry 35.0, Target 38.0, Stop 33.5

Oversea-Chinese Banking Corp Ltd (OCBC SP)

- Shares closed at a one-month high above the 5dEMA.

- MACD is positive, RSI is constructive.

- Long – Entry 14.60, Target 15.38, Stop 14.21

United Overseas Bank Ltd (UOB SP)

- Shares closed at a one-month high above the 5dEMA.

- Both RSI and MACD are constructive.

- Long – Entry 31.46 Target 33.26, Stop 30.56

China Merchants Port Holdings Co Ltd (144 HK)

- Shares closed at a 1-month high above the 5dEMA with rising volume.

- RSI and MACD are constructive.

- Long – Entry 12.0, Target 13.2, Stop 11.4

China Coal Energy Co Ltd (1898 HK)

- Shares closed at a 2-month high above the 5dEMA with rising volume.

- MACD is constructive, while RSI is at an overbought level.

- Long – Entry 9.40, Target 10.04, Stop 9.08

Best Buy Co Inc (BBY)

- 2Q25 Revenue: $9.29B, -3.0% YoY, beat estimates by $40M

- 2Q25 Non-GAAP EPS: $1.34, beat estimates by $0.18

- 2Q25 Dividend: Best Buy declares $0.94/share quarterly dividend, in line with the previous; Forward yield 3.69%; Payable Oct 10; for shareholders of record Sept 19; ex-div Sep 19.

- FY25 Guidance: Expect revenue of $41.3bn to $41.9bn, compared to $41.3bn to $42.6bn previously; Expect comparable sales of -1.5% to -3.0%, compared to 0% to -3.0% previously; Expect Non-GAAP diluted EPS of $6.10 to $6.35, compared to $5.75 to $6.20 previously.

- Comment: Best Buy delivered strong results and raised its FY25 guidance. Despite a 2.3% decline in comparable sales for the quarter, the domestic tablet and computing categories showed robust performance, with 6% year-over-year growth in comparable sales. The company anticipates increasing stabilization within the industry and a return to growth. Management remains optimistic about Best Buy’s strategic position, which is expected to benefit from this growth trend. Additionally, the company expects the long-awaited replacement cycle for pandemic-era tech purchases to gradually begin, prompting plans to increase marketing and operational investments to capitalize on the anticipated sales boost. Upcoming product launches, including Apple’s new iPads and Microsoft’s AI-enabled laptops, are also expected to drive sales. Furthermore, an improved outlook on rate cuts is likely to enhance consumer spending, benefiting Best Buy’s performance. 3Q25 recommended trading range: $90 to $110. Positive Outlook.

百思买 (BBY)

- 25财年第二季营收:92.9亿美元,同比下跌3.0%,超预期4,000万美元

- 25财年第二季Non-GAAP每股盈利:1.34美元,超预期0.18美元

- 25财年第二季股息:百思买宣布每股0.94美元的季度股息,与之前一致;远期股息率为3.69%;10月10日为付息日;9月19日为股东登记日及除息日。

- 25财年指引:预计营收为413亿至419亿美元,高于此前的413亿至426亿美元;预计可比销售额为-1.5%至-3.0%,此前为0%至-3.0%;预计Non-GAAP摊薄每股收益为6.10美元至6.35美元,而此前为5.75美元至6.20美元。

- 短评:百思买发布了强劲的业绩,并上调了25财年的指引。尽管本季度的可比销售额下降了2.3%,但国内平板电脑和电脑类产品表现强劲,可比销售额同比增长了6%。该公司预计该行业将越来越稳定,并恢复增长。管理层对百思买的战略地位保持乐观,预计百思买将从这一增长趋势中受益。此外,该公司预计,人们期待已久的大流行时代科技产品购买的更新周期将逐步开始,这促使公司计划增加营销和运营投资,以利用预期的销售增长。即将推出的产品,包括苹果的新款iPad和微软的人工智能笔记本电脑,预计也将推动销售。此外,降息前景的改善可能会提振消费者支出,有利于百思买的业绩。25年第三季度建议交易区间:90至110美元。积极前景。

Campbell Soup Co (CPB)

- 4Q24 Revenue: $2.3B, +11.1% YoY, miss estimates by $10M

- 4Q24 Non-GAAP EPS: $0.63, beat estimates by $0.01

- FY25 Guidance: Expect the addition of the 53rd week is expected to add approximately 2 points of growth to both reported and organic net sales and adjusted EBIT, along with $0.06 of adjusted EPS. Expect net sales growth of 9% to 11% vs estimated growth of 8.96%; Expect organic net sales flat to up 2% reflecting modestly positive volume compared to FY24; Expect adjusted EBIT growth of 9% to 11%; Expects adjusted EPS growth of 1% to 4% vs. $3.23 consensus.

- Comment: Campbell Soup reported mixed results and issued an FY25 profit forecast below expectations, citing ongoing high raw material costs and planned investments in promotions. The company saw sequential volume improvements and year-over-year margin growth during the quarter, making significant strides toward its long-term strategic goals despite a shifting consumer landscape. Notably, the Meals & Beverages segment, particularly Soup, showed a strong recovery, and the integration of Sovos exceeded expectations, signaling a positive shift in the segment’s growth trajectory. An improved rate outlook is also expected to boost consumer spending, which could drive higher volumes for the company. However, Campbell, like many other packaged food companies, continues to face elevated costs for inputs such as olive oil, cocoa, packaging, labor, and warehousing. These pressures have led to several rounds of price increases over the past year to support margins. 1Q25 recommended trading range: $45 to $53. Neutral Outlook.

金宝汤 (CPB)

- 24财年第四季营收:23亿美元,同比增幅11.1%,逊预期1,000万美元

- 24财年第四季Non-GAAP每股盈利:0.63美元,超预期0.01美元

- 25财年指引:预计第53周的增加预计将为报告和有机净销售额以及调整后息税前利润增加约2个百分点,调整后每股收益增长0.06美元。预计净销售额将增长9%至11%,而此前的预期增长率为8.96%;与24财年相比,预计有机净销售额将持平,增长2%,反映出适度的正增长;预计调整后息税前利润增长9%至11%;预期调整后每股收益增长1%至4%,市场预期为3.23美元。

- 短评:金宝汤公布了好坏参半的业绩,并发布了低于预期的25财年利润预测,原因是原材料成本持续高企,以及计划在促销方面的投资。该公司在本季度实现了连续销量增长和同比利润率增长,尽管消费者环境发生了变化,但在实现其长期战略目标方面取得了重大进展。值得注意的是,餐饮部门,特别是汤,表现出强劲的复苏,Sovos的整合超出了预期,标志着该部门增长轨迹的积极转变。利率前景的改善预计也将提振消费者支出,这可能会推动该公司的销量增长。然而,像许多其他包装食品公司一样,坎贝尔继续面临橄榄油、可可、包装、劳动力和仓储等投入成本上升的问题。这些压力导致了过去一年的几轮涨价,以支撑利润率。25年第一季度建议交易区间:45至53美元。中性前景。

Dell Technologies Inc (DELL)

- 2Q25 Revenue: $25.03B, +9.2% YoY, beat estimates by $910M

- 2Q25 Non-GAAP EPS: $1.89, beat estimates by $0.18

- FY25 Guidance: Expect FY25 revenue outlook to be between $95.5bn and $98.5bn, up from $93.5bn and $97.5bn previously; Raised FY25 adjusted EPS forecast to $7.80, plus or minus 25 cents.

- Comment: Dell reported strong results and raised its annual revenue and profit forecasts, driven by robust demand for its AI-optimized servers powered by Nvidia’s advanced chips. The company’s Infrastructure Solutions Group, which includes these Nvidia-powered servers, saw a 38% surge in revenue, reaching a record $11.65bn in 2Q25. Dell sees significant opportunities ahead, as many enterprises are still in the early stages of AI adoption. Additionally, Dell is exploring emerging opportunities in “sovereign AI” by leveraging its strong relationships with governments worldwide. Demand for its AI-optimized servers rose approximately 23% sequentially to $3.2bn in 2Q25, with a backlog for these servers valued at $3.8bn. However, while AI server demand soared, Dell’s PC business faced challenges, losing market share to competitors. A strong refresh cycle for AI PCs is anticipated next year, driven by the end of Microsoft’s support for Windows 10. 3Q25 recommended trading range: $100 to $150. Positive Outlook.

戴尔科技 (DELL)

- 25财年第二季营收:250.3亿美元,同比增幅9.2%,超预期9.1亿美元

- 25财年第二季Non-GAAP每股盈利:1.89美元,超预期0.18美元

- 25财年指引:预计25财年营收前景将在955亿美元至985亿美元之间,高于此前的935亿美元至975亿美元;上调全年调整后每股收益预测至7.80美元,上下浮动25美分。

- 短评:戴尔公布了强劲的业绩,并上调了年度收入和利润预期,这得益于市场对其采用英伟达先进芯片的人工智能优化服务器的强劲需求。该公司的基础设施解决方案集团(包括这些英伟达服务器)的收入激增38%,在25年第二季度达到创纪录的116.5亿美元。戴尔看到了未来的巨大机遇,因为许多企业仍处于采用人工智能的早期阶段。此外,戴尔正在利用其与全球各国政府的牢固关系,探索“主权人工智能”领域的新兴机会。对其人工智能优化服务器的需求在25年第二季度环比增长约23%,达到32亿美元,这些服务器的积压价值为38亿美元。然而,在人工智能服务器需求激增的同时,戴尔的个人电脑业务面临挑战,市场份额被竞争对手抢走。受微软结束对Windows 10的支持推动,预计明年人工智能个人电脑将迎来一个强劲的更新周期。25财年第三季度建议交易区间:100至150美元。积极前景。

Ulta Beauty Inc (ULTA)

- 2Q24 Revenue: $2.6B, +4.0% YoY, miss estimates by $10M

- 2Q24 GAAP EPS: $5.30, miss estimates by $0.15

- FY24 Guidance: Lower FY24 outlook. Expect net sales to be between $11.0bn to $11.2bn, compared to $11.5bn to $11.6bn previously; Expect comparable sales growth between -2% to 0%, compared to 2% to 3% previously; Expect operating margin to be between 12.7% to 13.0%, compared to 13.7% to 14.0% previously; Expect diluted EPS to fall in the range of $22.60 to $23.50, compared to $25.20 to $26.0 previously.

- Comment: Ulta Beauty reported disappointing results and significantly lowered its FY24 outlook. Comparable sales for Q2 FY24 declined by 1.2%, a sharp contrast to the 8% increase from the previous year and falling short of the expected 1.2% growth. Management attributed the weaker sales performance to four main factors, including an “unanticipated operational disruption” related to a change in store systems and underwhelming results from promotions. The company also noted that consumers are becoming increasingly cautious with their spending and that competition in the beauty industry has intensified. Ulta Beauty expects to continue facing challenges in driving topline growth, with stores in areas impacted by multiple competitive openings likely to remain under pressure. 3Q24 recommended trading range: $300 to $380. Negative Outlook.

Ulta美容 (ULTA)

- 24财年第二季营收:26亿美元,同比增幅4.0%,逊预期1,000万美元

- 24财年第二季GAAP每股盈利:5.3美元,逊预期0.15美元

- 24财年指引:下调24财年前景。预计净销售额将在110亿美元至112亿美元之间,而此前为115亿美元至116亿美元;预计同店销售额增幅将从之前的2%至3%降至-2%至0%;预计营业利润率将在12.7%至13.0%之间,此前为13.7%至14.0%;预计稀释后每股收益将在22.60美元至23.50美元之间,而此前为25.20美元至26.0美元。

- 短评:Ulta美容公布了令人失望的业绩,并大幅下调了其24财年的预期。24财年第二季度的可比销售额下降了1.2%,与上年同期8%的增幅形成鲜明对比,也低于1.2%的预期增幅。管理层将较弱的销售业绩归因于四个主要因素,包括与门店系统变化相关的“意外运营中断”,以及促销活动带来的不尽如人意的结果。该公司还指出,消费者在消费方面变得越来越谨慎,美容行业的竞争也在加剧。公司预计在推动营收增长方面将继续面临挑战,受多个竞争性开业影响的地区的门店可能仍将面临压力。24财年第三季度建议交易区间:300至380美元。负面前景。

Marvell Technology Inc (MRVL)

- 2Q25 Revenue: $1.273B, -5.2% YoY, beat estimates by $20M

- 2Q25 Non-GAAP EPS: $0.30, beat estimates by $0.01

- 3Q25 Guidance: Expect revenue is expected to be $1.45B +/- 5% vs $1.41B consensus. GAAP and Non-GAAP gross margin is expected to be approximately 47.2% and 61% respectively. GAAP diluted loss per share is expected to be $0.09 +/- $0.05 and Non-GAAP diluted income per share is expected to be $0.40 +/-$0.05 per share vs consensus of $0.38.

- Comment: Marvell Technology exceeded expectations for quarterly revenue and earnings, driven by high demand for its electro-optics products and custom AI programs. Increased investments in generative AI by tech giants are boosting demand for Marvell’s cloud-optimized silicon solutions. The data center segment, which includes AI chips, saw a 92% revenue increase to US$880.9mn, surpassing estimates. Marvell forecasts third-quarter revenue at approximately US$1.45bn, above Wall Street’s estimate of US$1.40bn and expects income of about US$0.40 per share compared to estimates of USS$0.38. The CEO expects growth in both enterprise networking and data center markets in the current quarter. Looking ahead, Marvell is well-positioned to benefit from the ongoing trend of increased investments in generative AI applications by big tech companies. This is driving cloud customers to build new data centers, which in turn is fueling demand for cloud-optimized silicon solutions like those offered by Marvell. 3Q25 recommended trading range: $70 to $85. Positive Outlook.

迈威尔科技 (MRVL)

- 25财年第二季营收:12.73亿美元,同比跌幅5.2%,超预期2,000万美元

- 25财年第二季Non-GAAP每股盈利:0.3美元,超预期0.01美元

- 25财年第三季指引:预计营收为14.5亿美元+/- 5%,市场预期为14.1亿美元。GAAP和Non-GAAP毛利率预计分别约为47.2%和61%。GAAP摊薄每股亏损预计为0.09美元+/- 0.05美元,Non-GAAP摊薄每股收益预计为0.40美元+/- 0.05美元,而市场预期为0.38美元。

- 短评:迈威尔科技的季度收入和收益超出预期,这得益于对其光电产品和定制人工智能程序的高需求。科技巨头加大了对生成式人工智能的投资,推动了对公司云优化芯片解决方案的需求。包括人工智能芯片在内的数据中心部门收入增长92%,达到8.890亿美元,超出预期。公司预计第三季度营收约为14.5亿美元,高于华尔街预期的14.4亿美元,每股收益约为0.40美元,高于预期的0.38美元。这位首席执行官预计,本季度企业网络和数据中心市场都将出现增长。展望未来,公司将从大型科技公司不断增加对生成式人工智能应用投资的趋势中受益。这促使云计算客户建立新的数据中心,这反过来又刺激了对像公司提供的云优化芯片解决方案的需求。25财年第三季度建议交易区间:70至85美元。积极前景。

Lululemon Athletica Inc (LULU)

- 2Q24 Revenue: $2.37B, +7.2% YoY, miss estimates by $40M

- 2Q24 GAAP EPS: $3.15, beat estimates by $0.23

- 3Q24 Guidance: Expect net revenue to be in the range of $2.340B to $2.365B, representing growth of 6% to 7%, vs consensus of $2.41B. Diluted earnings per share are expected to be in the range of $2.68 to $2.73, assumes a tax rate of approximately 30%.

- FY24 Guidance: Expect net revenue to be in the range of $10.375B to $10.475B, representing growth of 8% to 9%, or 6% to 7% excluding the 53rd week of 2024, vs consensus of $10.62B. Diluted earnings per share now expected to be in the range of $13.95 to $14.15, assumes a tax rate of approximately 30%.

- Comment: Lululemon Athletica delivered second quarter revenue of US$2.37bn which missed estimates and earnings which exceeded expectations at US$3.15 per share, driven by lower promotions and reduced costs which boosted gross margins by 80 basis points to 59.6%. The company lowered its annual sales and profit forecasts due to weakening demand for its high-priced leggings and tank tops in North America, as consumers become more selective with their spending. Despite these challenges, it pledged to improve its product mix to attract more spending. Lululemon has faced a slow start to 2024, with issues like slower innovation in women’s apparel, issues with assortment and product missteps, such as the removal of its “Breezethrough” leggings shortly after launch. While sales in China surged by 21%, sales in the Americas fell by 3%. The company now expects lower FY24 revenue in the range of US$10.38bn to US$10.48bn compared with a prior forecast of US$10.70bn to US$10.80bn and earnings of US$13.95 to US$14.15 per share compared to its previous forecast of between US$14.27 to US$14.47. The company faces increased competition and a potentially challenging consumer environment. With the slowdown in demand for women’s apparel and declining US consumer spending, Lululemon will need to execute effectively to regain market share. 3Q24 recommended trading range: $250 to $300. Neutral Outlook.

露露柠檬 (LULU)

- 24财年第二季营收:23.7亿美元,同比增幅7.2%,逊预期4,000万美元

- 24财年第二季GAAP每股盈利:3.15美元,超预期0.23美元

- 24财年第三季指引:预计净收入将在23.4亿美元至23.65亿美元之间,同比增长6%至7%,而市场预期为24.1亿美元。假设税率约为30%,摊薄后每股收益预计在2.68美元至2.73美元之间。

- 24财年指引:预计净收入将在103.75亿美元至104.75亿美元之间,增长率为8%至9%,不包括2024年第53周,增长率为6%至7%,而市场预期为106.2亿美元。假设税率约为30%,摊薄后每股收益预计在13.95美元至14.15美元之间。

- 短评:露露柠檬第二季度收入为23.7亿美元,低于预期,每股收益超过预期,为3.15美元,这是由于促销活动减少和成本降低,毛利率提高了80个基点,达到59.6%。该公司下调了年度销售和利润预期,原因是北美消费者对其高价打底裤和背心的需求减弱,因为消费者在消费方面变得更加挑剔。尽管面临这些挑战,该公司仍承诺改善其产品结构,以吸引更多的支出。露露柠檬在2024年起步缓慢,面临着女装创新缓慢、分类问题和产品失误等问题,比如“Breezethrough”打底裤在推出后不久就被撤下。虽然在中国的销量增长了21%,但在美洲的销量却下降了3%。该公司目前预计24财年收入将下降至103.8亿美元至104.8亿美元,而此前预测为107亿美元至100.8亿美元,每股收益为13.95美元至14.15美元,而此前预测为14.27美元至14.47美元。该公司面临着日益激烈的竞争和一个潜在的具有挑战性的消费环境。随着女性服装需求的放缓和美国消费者支出的下降,露露柠檬将需要有效地执行以重新获得市场份额。24财年第三季度建议交易区间:250至300美元。中性前景。

Burlington Stores Inc (BURL)

- 2Q24 Revenue: $2.46B, +13.4% YoY, beat estimates by $40M

- 2Q24 Non-GAAP EPS: $1.24, beats estimates by $0.28

- 3Q24 Guidance: Expect total sales to increase in the range of 10% to 12% vs. estimated growth of 10.44% YoY; this assumes comparable store sales will increase in the range of 0% to 2% versus the third quarter of Fiscal 2023; Adjusted EBIT margin to increase in the range of 60 to 80 basis points versus the third quarter of Fiscal 2023; Adjusted Effective Tax Rate to be approximately 25%; and adjusted EPS in the range of $1.45 to $1.55 vs. $1.37 consensus, as compared to $1.10 in Adjusted EPS last year; prior year period excludes $7M, net of tax, of expenses related to the acquired Bed Bath & Beyond leases.

- FY24 Guidance: Expect total sales to increase in the range of 9% to 10% on top of the 10% increase for the 52-weeks ended 27 January 2024, vs estimated growth of 9.04% YoY. Assumes comparable store sales will increase in the range of 2% to 3%, on top of the 4% increase for the 52-weeks ended 27 January 2024. Capital expenditures, net of landlord allowances, to be approximately $750M; To open approximately 100 net new stores; Depreciation and amortization to be approximately $350M; Adjusted EBIT margin to increase in the range of 50 to 70 basis points versus the 52 weeks ended January 27, 2024; this Adjusted EBIT margin increase excludes approximately $9M of expenses related to the acquired Bed Bath & Beyond leases in Fiscal 2024 versus $18M incurred in Fiscal 2023; Net interest expense to be approximately $40M; Adjusted Effective Tax Rate to be approximately 26%; and adjusted EPS in the range of $7.66 to $7.96 vs. $7.71 consensus (prior $7.35 to $7.75), which excludes $0.11, net of tax, of expenses, associated with the acquired Bed Bath & Beyond leases. This assumes a fully diluted share count of approximately 64 million shares.

- Comment: Burlington Stores reported strong second-quarter results, with profits more than doubling and revenue increasing by 13.4% to US$2.46bn. Its CEO attributed the strong performance to higher-than-expected sales, improved supply chain efficiency, and a significant increase in gross margin. Burlington’s net profit reached US$73.8mn, with adjusted earnings per share of US$1.24, both exceeding expectations. Despite warnings about rising ocean freight costs, Burlington raised its full-year outlook. The company achieved a 13% jump in total sales, driven by new store openings and a healthy 5% increase in comparable store sales. Additionally, Burlington expanded its operating margin by 160 basis points, primarily due to improved gross margins and supply chain efficiency. Bolstered by these positive results, Burlington increased its full-year guidance. It plans to open 100 net new stores and relocate 30 existing ones this fiscal year. The company now expects adjusted earnings per share for the full year to range between US$7.66 and US$7.96, exceeding its previous forecast. However, it acknowledges the need for cautious planning due to potential cost pressures. Despite potential headwinds, Burlington remains committed to modernizing its distribution network and prioritizing domestic growth. 3Q24 recommended trading range: $250 to $300. Positive Outlook.

伯灵顿百货 (BURL)

- 24财年第二季营收:24.6亿美元,同比增幅13.4%,超预期4,000万美元

- 24财年第二季Non-GAAP每股盈利:1.24美元,超预期0.28美元

- 24财年第三季指引:预计总销售额将增长10%至12%,而预计同比增长10.44%;这是假设可比门店销售额将比2023财年第三季度增长0%至2%;与2023财年第三季度相比,调整后息税前利润率将增加60至80个基点;调整后的有效税率约为25%;调整后每股收益为1.45美元至1.55美元,而去年调整后每股收益为1.37美元,而去年调整后每股收益为1.10美元;去年期间不包括与收购的Bed Bath & Beyond租赁相关的700万美元税后费用。

- 24财年指引:预计在截至2024年1月27日的52周内,总销售额将增长9%至10%,而预计同比增长9.04%。假设可比店面销售额将在截至2024年1月27日的52周内增长4%的基础上,增长2%至3%。资本支出(扣除业主津贴)约为7.5亿美元;净开设约100家新店;折旧和摊销约为3.5亿美元;与截至2024年1月27日的52周相比,调整后息税前利润率将增加50至70个基点;调整后息税前利润率的增长不包括与2024财年收购的Bed Bath & Beyond租赁相关的约900万美元费用,而2023财年的费用为1,800万美元;净利息支出约为4,000万美元;调整后的有效税率约为26%;调整后的每股收益为7.66美元至7.96美元,而市场预期为7.71美元(之前为7.35美元至7.75美元),其中不包括与收购Bed Bath & Beyond租赁相关的税后费用0.11美元。这假设完全稀释后的股票数量约为6,400万股。

- 短评:伯灵顿百货公司公布了强劲的第二季度业绩,利润增长了一倍多,收入增长了13.4%,达到24.6亿美元。该公司首席执行官将强劲的业绩归功于高于预期的销售额、供应链效率的提高以及毛利率的大幅增长。公司净利润达到7,380万美元,调整后每股收益为1.24美元,均超出预期。尽管有海运成本上涨的警告,公司还是上调了全年预期。在新店开业和可比店销售额健康增长5%的推动下,该公司的总销售额增长了13%。此外,公司的营业利润率提高了160个基点,这主要是由于毛利率和供应链效率的提高。在这些积极结果的支撑下,伯灵顿提高了全年指导。该公司计划在本财年净开100家新店,并搬迁30家现有门店。该公司目前预计,调整后的全年每股收益将在7.66美元至7.96美元之间,超过此前的预测。然而,它承认由于潜在的成本压力,需要谨慎规划。尽管存在潜在的阻力,伯灵顿仍致力于使其分销网络现代化,并优先考虑国内增长。24财年第三季度建议交易区间:250至300美元。积极前景。