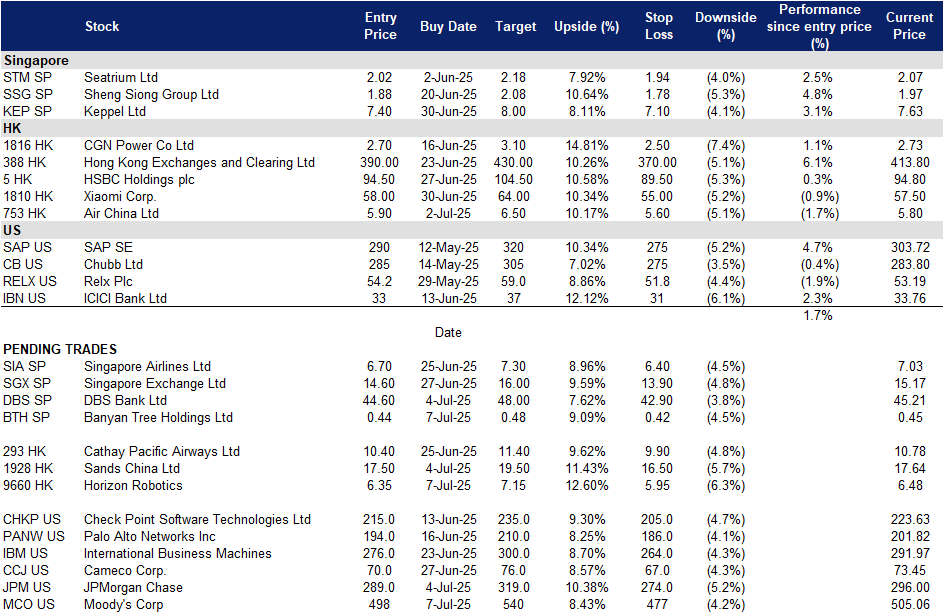

Banyan Tree Holdings Ltd (BTH SP): Potential to improve margins

BUY Entry – 0.44 Target – 0.48 Stop Loss – 0.42

Banyan Tree Holdings Limited operates as a holding company. The Company, through its subsidiaries, owns and manages hotel groups. The Company focuses on hotels, resorts, spas, galleries, golf courses, and residences, as well as provides investments, design, construction, and project management services. Banyan Tree Holdings serves customers worldwide.

Favorable macroeconomic backdrop supports expansion. Amid ongoing market volatility and continued USD depreciation, investor expectations for a U.S. Federal Reserve rate cut in September are rising. A potential decline in interest rates would benefit Banyan Tree by lowering borrowing costs, thereby enhancing its ability to finance expansion plans more efficiently. With a growing pipeline in key tourism markets like Japan and a strategic focus on experiential luxury, improved financing conditions could significantly boost margins and accelerate the group’s international growth trajectory.

Surging regional travel demand. According to Mastercard Economics Institute’s Travel Trends 2025 report, Asia-Pacific continues to lead global summer travel, with eight of the top 15 trending destinations, including Tokyo, Osaka, and emerging favorite Nha Trang. This momentum is underpinned by favorable exchange rates, enhanced air connectivity, and rising demand for wellness-driven, nature-based, and culinary travel. With China and India at the forefront of outbound tourism growth, travelers are seeking high-value, immersive experiences. These consumer shifts align directly with Banyan Tree Group’s brand ethos and product offerings, reinforcing the Group’s positioning within Asia-Pacific’s thriving travel ecosystem.

Strategic global expansion. In 2025, Banyan Tree Group is accelerating its growth with the launch of 15 new hotels and five branded residences across diverse geographies. The recent opening of Mandai Rainforest Resort in Singapore marked the Group’s 100th property and its debut in its home market. Other key developments include Ubuyu, its first African safari lodge in Tanzania, and an integrated lifestyle hub in Bangkok. Expansion in the Caribbean and across Asia, China, Korea, Thailand, and the Philippines, underscores the Group’s multi-brand strategy and its focus on delivering authentic, locally inspired hospitality. This global pipeline positions Banyan Tree to meet rising demand for meaningful, destination-driven travel.

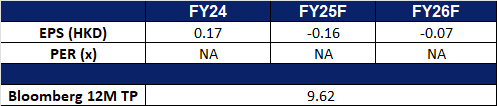

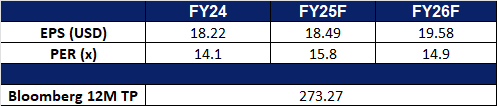

FY24 business updates. Banyan Tree Holdings reported a 16% increase in revenue to S$380.6 million, mainly due to robust growth across all business segments. Operating Profit increased by S$13.1 million to S$103.2 million, attributable to higher contributions from the Hotel Investments and Residences segments due to higher revenue. PATMI rose to S$42.1 million from the previous S$31.7 million in FY23 and earnings per share rose to S$0.049 compared to S$0.037 in FY23. As of FY24, the Group recorded a total of 91 hotels and resorts, 73 spas, 68 galleries and 22 branded residences in 22 countries. During the year, the group reported 17 new hotel and resort openings, with six in Japan and South Korea, and eight in China as part of the Group’s multi-brand expansion strategy across Asia.

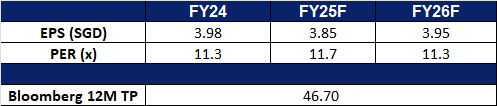

Market consensus

(Source: Bloomberg)

DBS Group Holdings Ltd (DBS SP): Boosting customer growth, one cashback at a time

DBS Group Holdings Limited and its subsidiaries provide a variety of financial services. The Company offers services including mortgage financing, lease and hire purchase financing, nominee and trustee, funds management, corporate advisory and brokerage. DBS Group also acts as the primary dealer in Singapore government securities.

Safe-haven appeal and market volatility driving growth. DBS stands to benefit from Singapore’s growing status as a financial haven amid global uncertainties, including U.S. economic concerns, trade tensions and a weakening USD. The strengthening SGD, combined with an inverse correlation to the STI, makes Singaporean assets more attractive to international investors. DBS, with its dominant local presence, saw market trading activity more than double in Q1, its highest in 12 quarters, driven by FX, interest rate and equity derivatives. Ongoing macro volatility and capital inflows into Singapore will likely boost DBS’s trading and wealth management income.

Strengthening digital ecosystem and brand loyalty. Through its SG60 campaign, DBS/POSB is driving increased engagement and transaction volume with initiatives like the weekly S$3 cashback, S$0.60 and S$6 meal deals, and eVoucher rewards via PayLah! and POSB cards. Running from July to September, these offers aim to ease cost-of-living pressures and encourage digital payments at over 22,000 heartland merchants. This initiative not only reinforces DBS’s community presence but also deepens user adoption of its digital platforms and payment products, supporting fee-based income and customer retention.

1Q25 Business Updates. Total income for 1Q25 rose 6% YoY to a record of S$5.91bn from broad-based business growth, while net profit fell 2% YoY to S$2.90bn, due to the impact of the 15% global minimum tax, with return on equity at 17.3%. The board declared a total dividend of S$0.75 per share for the first quarter.

Market consensus

(Source: Bloomberg)

Horizon Robotics (9660 HK): An edge in smart driving in China

BUY Entry – 6.35 Target – 7.15 Stop Loss – 5.95

Horizon Robotics is an investment holding company principally engaged in the provision of advanced driver assistance systems (ADAS) and autonomous driving (AD) solutions for passenger cars. The Company operates primarily through two segments. The Automotive Solutions segment is principally engaged in the provision of product solutions and license and services. The Company’s solutions mainly include Horizon Mono, Horizon Pilot, Horizon SuperDrive, and automotive in-cabin solution for the passenger vehicle. The Non-Automotive Solutions segment enables device manufacturers to design and manufacture devices and appliances, such as lawn mowers, fitness mirrors, and air purifiers. The Company mainly conducts its businesses in the domestic market.

Momentum in China’s Autonomous Driving Sector. Chinese regulators are finalizing new safety standards for driver-assistance systems, aiming to strike a balance between innovation and oversight. The objective is to prevent carmakers from overstating system capabilities while maintaining global competitiveness. By establishing clear guidelines without stifling progress, China’s autonomous driving industry could gain an edge over U.S. and European peers. Authorities are encouraging domestic automakers to accelerate deployment of Level 3 assisted-driving systems, which allow drivers to take their eyes off the road under specific conditions. Several OEMs showcased advancements in this area at the Shanghai Auto Show in April. This regulatory clarity and industry momentum stand to benefit Horizon Robotics, a key player in smart driving technologies.

Horizon SuperDrive (HSD) Enters Mass Production on new Chery models in September. Horizon Robotics recently introduced its Horizon SuperDrive (HSD) urban driving assistance system in Shanghai, with mass production set to begin in September on new Chery models. Powered by the company’s Journey 6 chip and developed through its proprietary software-hardware co-optimization approach, HSD replicates human driving behavior to deliver a safer, more efficient, and comfortable driving experience. As one of China’s leading smart driving chip and software providers, Horizon Robotics is well-positioned to see increased adoption and sales with the HSD rollout.

Expanded Strategic Partnership with Volkswagen. Horizon Robotics has deepened its collaboration with Volkswagen Group to advance intelligent driving technologies, centered on the HSD platform. The system will be deployed through CARIZON, the joint venture between Horizon Robotics and Volkswagen’s software unit, CARIAD. Supporting Volkswagen’s “In China, for China” strategy, this partnership will accelerate the integration of smart driving features across its Chinese lineup and further solidify its position in the local smart mobility landscape.

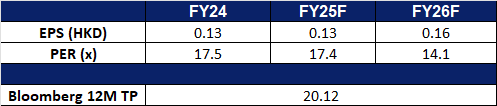

FY24 results review. FY24 revenue rose by 53.6% to RMB2.38bn, compared to RMB1.55bn in FY23. Net profit was RMB2.35bn in FY24, compared to a net loss of RMB6.74bn in FY23. Basic EPS rose to RMB0.51 in FY24, compared to RMB(2.50) in FY23.

Market consensus.

(Source: Bloomberg)

Sands China Ltd. (1928 HK): Summer and concert crowd

Sands China Ltd is an investment holding company principally engaged in the development and operation of resorts. The Company operates its business through six segments. The Venetian Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Londoner Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Parisian Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Plaza Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering services and others. The Sands Macao segment is engaged in the operation of casinos, hotels and shopping malls as well as provision of catering and others. The Ferry and Other Operations segment is engaged in the provision of ferry, shuttle bus and other services.

Anticipated Surge in Macau Tourism. China is gearing up for a record-breaking summer travel season, with over 900 million railway journeys expected between July and August. Macau is well-positioned to benefit from this surge, as June casino revenues rose 19% year-over-year amid robust visitor traffic. This momentum is likely to continue through the summer, supported by a strong lineup of premium entertainment events, including Jacky Cheung’s concert in July and G-Dragon’s performance in early August. Increased visitor traffic, particularly in the premium segment, is expected to positively impact Sands China.

Enhanced Brand Visibility Through Strategic Marketing. Sands China is leveraging its multi-year partnership with the NBA to bolster brand presence. As part of the agreement, two preseason NBA games will be held annually at the Venetian Arena in Macau over the next five years. The company will host the 2025 games in October and has launched the “2025 NBA China Games Experience Package,” offering five accommodation tiers at The Londoner Macao. The top-tier packages include exclusive backstage access and dining experiences with NBA Legends. These initiatives are designed to drive traffic and elevate Sands China’s hotel and retail offerings through the global appeal of the NBA brand.

Strategic Partnership to Develop Health Tourism. Sands China has signed a memorandum of understanding with Guangdong-Macau Traditional Chinese Medicine Technology Industrial Park Development Co. Ltd. to position Macau and Hengqin as a leading destination for health tourism. The partnership aims to integrate tourism, traditional Chinese medicine (TCM), and MICE (meetings, incentives, conferences, and exhibitions), in line with the Macau SAR government’s “1+4” economic diversification strategy. This collaboration is expected to support long-term growth in visitor numbers and broaden Macau’s tourism appeal beyond gaming.

FY24 results review. FY24 revenue rose by 8.36% to US$7.08bn, compared to US$6.53bn in FY23. Net profit rose by 51.0% to US$1.05bn in FY24, compared to US$692mn in FY23. Basic EPS rose to 12.91 US cents in FY24, compared to 8.56 US cents in FY23.

Market consensus.

(Source: Bloomberg)

Moody’s Corp (MCO US): Stable, scalable and diversified

BUY Entry – 498 Target – 540 Stop Loss – 477

Moody’s Corporation is a credit rating, research, and risk analysis firm. The Company provides credit ratings and related research, data and analytical tools, quantitative credit risk measures, risk scoring software, and credit portfolio management solutions and securities pricing software and valuation models.

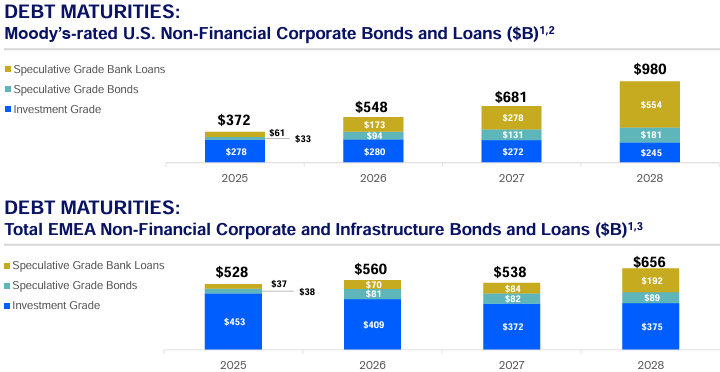

Strong prospects for bond issuance. From 2025 to 2028, over US$4 trillion in debt is expected to mature across the United States, Europe, the Middle East, and Africa. This large-scale wave of debt maturities is expected to drive refinancing and new debt issuance activities, providing Moody’s with a stable and predictable source of business, which is likely to support the continued growth of its credit rating and financial analysis services.

(Source: Moody’s)

Rate cuts create a favorable macroeconomic environment. According to the CME FedWatch tool, the market currently anticipates a 67.8% probability that the Federal Reserve will cut interest rates by 25 basis points in September 2025, indicating a general expectation that monetary policy will begin to shift towards easing.

Resilient, diversified revenue streams. Despite a slightly lowered full-year outlook, Moody’s Q1 highlight the strength of its diversified, service-centric model. Both Moody’s Analytics’s (MA) recurring revenue, which accounts for 96% of its total revenue, grew 9% YoY, underpinned by 12% growth in Decision Solutions and 8% overall revenue growth, demonstrating the success of its strategic pivot toward subscription-based offerings. Annualized recurring revenue (ARR) rose to US$$3.3bn, reflecting continued demand for data-driven risk and decision solutions. Simultaneously, Moody’s Investors Service (MIS) posted its highest-ever quarterly revenue of US$1.1bn, driven by an 8% rise in transactional revenue and strong momentum in investment-grade corporate finance and structured finance, particularly in private credit-related transactions. As investor appetite for high-quality and private credit assets persists, Moody’s resilient revenue base, anchored by recurring subscriptions and broad market exposure, positions it well to navigate macro uncertainty and sustain long-term growth.

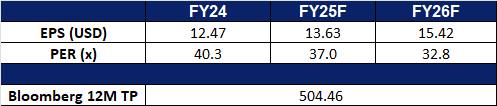

1Q25 results. Moody’s Corp delivered an 8% increase in revenue to US$1.92bn, beating estimates by US$40mn. Non-GAAP Earnings per share was US$3.83, beating estimates by US$0.29. The company lowered its full-year 2025 guidance with expectations of revenue growth in the mid-single digits and an adjusted operating margin between 49% and 50%. It anticipates adjusted diluted EPS for the year to range from US$13.25 to US$14.00. Moody’s also plans to repurchase at least US$1.3bn in shares and expects free cash flow between US$2.3bn and US$2.5bn.

JPMorgan Chase & Co. provides global financial services and retail banking. The Company provides services such as investment banking, treasury and securities services, asset management, private banking, card member services, commercial banking, and home finance. JP Morgan Chase serves business enterprises, institutions, and individuals.

Strengthened capital return program. JPMorgan Chase has announced a planned dividend increase to US$1.50 per share, up from US$1.40 and authorized a substantial US$50bn share repurchase program following its successful completion of the Federal Reserve’s 2025 stress test. This robust capital return strategy reflects JPMorgan’s strong financial position, continued regulatory compliance and ongoing commitment to returning value to shareholders. The move also reinforces investor confidence in the bank’s operational resilience and disciplined capital management amid broader macroeconomic uncertainty.

Continued resilience of large U.S. banks. Despite a less stringent stress-testing framework in 2025 due to a weaker global economy, all 22 major U.S. banks, including JPMorgan, remained well above regulatory capital thresholds, reaffirming the sector’s resilience. JPMorgan in particular stands out with a strong first quarter CET1 ratio of 15.4% and US$1.5tn in liquidity, enabling it to comfortably absorb economic shocks. While the Fed’s scenario excluded some systemic risks like private credit exposure, the results still validate JPMorgan’s financial robustness and support its continued dividend increases and share repurchases, further demonstrating its ability to navigate an uncertain economic environment.

Volatility driven trading tailwinds. Ongoing global market volatility has significantly benefited JPMorgan’s trading business, with Q1 Markets revenue surging to a record US$9.7bn, driven by exceptionally strong equities performance. As geopolitical risks escalate, particularly with the recent Middle East tensions and the U.S. set to reimpose steep tariffs on 9 July, market fluctuations are likely to persist throughout the year. This backdrop positions JPMorgan to continue capturing elevated trading activity and capital markets demand, further boosting its fee-based income and reinforcing its role as a market leader in volatile environments.

1Q25 results. Revenue increased by 9.7% YoY to US$46bn, exceeding expectations by US$1.86bn. The non-GAAP earnings per share were US$4.91 beating expectations by US$0.27. It expects net interest income for the full year 2025 to be approximately US$94.5bn.

(Source: Bloomberg)

(Source: Bloomberg)