Centurion Corporation Limited provides purpose-built workers and student accommodation services. Centurion owns, develops, and manages quality and purpose-built workers accommodation assets. Centurion serves customers worldwide.

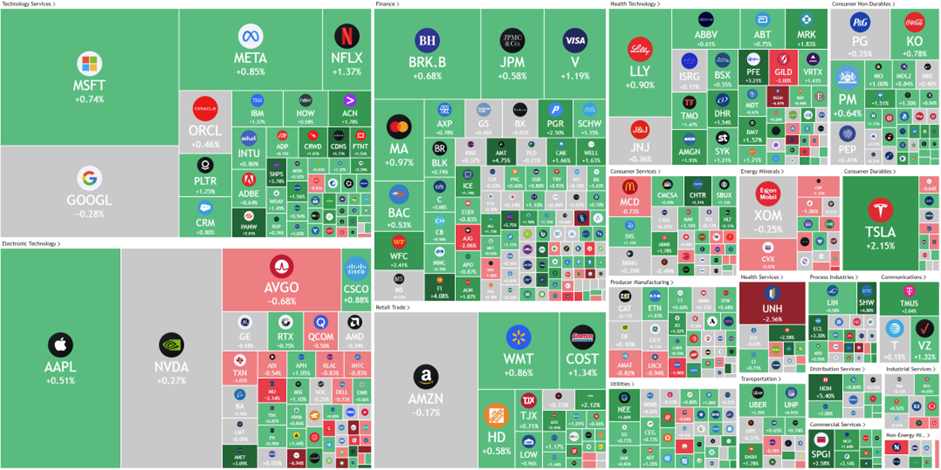

Rising rate cut expectations. US weekly jobless claims rose by 6,000 to 222,000, signalling mounting economic risks driven by President Trump’s volatile tariff policies. Economists expect job losses to accelerate later this year in tariff-sensitive sectors such as retail and manufacturing, amid weakening business investment and growing employer caution. Broader economic momentum is also slowing, as reflected in the sharp decline in home sales, driven by rising concerns over inflation, employment prospects, and high mortgage rates. These signs of economic strain are reinforcing market expectations for Federal Reserve easing, with the CME FedWatch tool now pricing in a 61.3% probability of a rate cut by June. A potential rate cut would benefit Centurion by lowering financing costs for its expansion plans, improve funding conditions for future developments, and enhance property valuations.

REIT listing exploration. Centurion is exploring a potential REIT structure comprising stabilized PBWA and PBSA assets in mature markets like Singapore, Malaysia, and the UK. This could unlock asset value, enhance capital recycling, and deliver stable income for shareholders via a potential dividend-in-specie.

Stronger than anticipated revenue growth. Total revenue rose 22% YoY to S$253.6 million, while net profit after tax surged 118% to S$382.6 million, driven by high financial occupancy and rental rate uplifts across all key markets.

Expanding global footprint. As of 31 December 2024, Centurion operated 69,929 beds across 37 assets with AUM of S$2.5 billion. It added 2,552 new beds and has 7,662 beds under development for 2025-2026, including a new PBSA in Macquarie Park, Australia.

2H24 results review. Revenue increased 18% YoY to S$129.2 million from S$109.3 million in 2H23, while gross profit grew 27% to S$101.5 million, underpinned by sustained high occupancy and positive rental revisions. Despite a slight dip in PBWA occupancy in Malaysia, attributable to short-term foreign worker caps, strong rental performance and high occupancy in key markets like Singapore, the UK, and Australia offset this temporary weakness. Centurion declared a final dividend of 3.5 Scents per share for FY24, representing a 28.6% increase from the 2.5 Scents distributed in FY23.

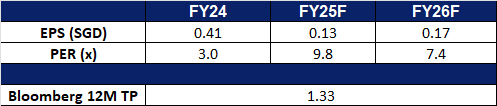

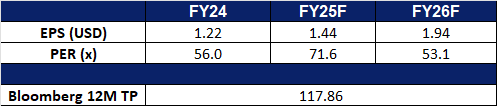

We have fundamental coverage with a BUY recommendation and a TP of S$1.38. Please read the full report here.

Market consensus

(Source: Bloomberg)

Singapore Exchange Ltd (SGX SP): Benefitting from macroeconomic uncertainty

Singapore Exchange Limited owns and operates Singapore’s Securities and derivatives exchange and their related clearing houses. The Company also provides ancillary securities processing and information technology services to participants in the financial sector.

Benefitting from fund outflows from the U.S. The weakening of the USD, coupled with escalating trade tensions between the U.S. and China, has triggered a capital outflow from U.S. equities to emerging markets like Singapore. Singapore’s high-yield, defensive stocks, such as telecom, industrials, and utilities, have benefitted from this trend, making the Singapore Exchange an attractive platform for institutional investors seeking stability and income.

Supportive government policies driving growth. The Singapore government, through the Monetary Authority of Singapore (MAS), introduced a series of initiatives to enhance the attractiveness and competitiveness of the local stock market. These include the $5bn Equity Market Development Programme (EQDP), which will partner with fund managers to invest in Singapore equities and streamlined regulations to make the listing process more efficient. Additionally, tax incentives and expanded research grants under the Grant for Equity Market Singapore (GEMS) aim to attract quality IPOs and boost liquidity. These comprehensive measures, coupled with a focus on fostering innovation and sustainability sectors, position the Singapore Exchange as a prime destination for both retail and institutional investors, fostering long-term growth and resilience.

Safe-haven for investors. Positioned as a safe-haven financial hub, Singapore offers a unique combination of high dividend yields, economic resilience, and a robust regulatory framework. Its ability to weather global economic instability makes the Singapore Exchange a sweet spot for investors looking for reliable returns and capital preservation amidst current market volatility.

1H25 results review. Singapore Exchange Ltd reported 1H25 revenue of S$682.2mn a 15.2% increase from S$592.2mn in the previous period. Its net profit of S$340mn for 1H25, a 20.7% incline YoY, compared to S$281.6mn in 1H24. Earnings per share (EPS) stood at S$0.318, up from S$0.263 in the year-ago period. Due to the Group’s strong performance, the Board of Directors declared an interim quarterly dividend of S$0.09 per share, up from the S$0.085-per-share payout in the previous corresponding period, bringing total dividends for 1H25 to S$0.18 per share.

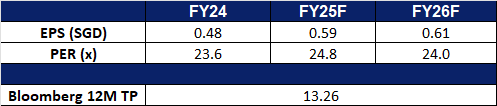

Market consensus

(Source: Bloomberg)

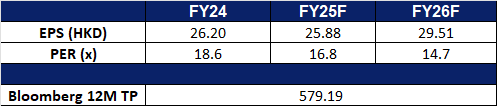

Hong Kong Exchanges and Clearing Ltd. (388 HK): Expecting increased trading activities

Hong Kong Exchanges and Clearing Limited (HKEX) is principally engaged in the operation of stock exchanges. The Company operates through five business segments. The Cash segment includes various equity products traded on the Cash Market platforms, the Shanghai Stock Exchange and the Shenzhen Stock Exchange. The Equity and Financial Derivatives segment includes derivatives products traded on Hong Kong Futures Exchange Limited (HKFE) and the Stock Exchange of Hong Kong Limited (SEHK) and other related activities. The Commodities segment includes the operations of the London Metal Exchange (LME). The Clearing segment includes the operations of various clearing houses, such as Hong Kong Securities Clearing Company Limited, the SEHK Options Clearing House Limited, HKFE Clearing Corporation Limited, over the counter (OTC) Clearing Hong Kong Limited and LME Clear Limited. The Platform and Infrastructure segment provides users with access to the platform and infrastructure of the Company.

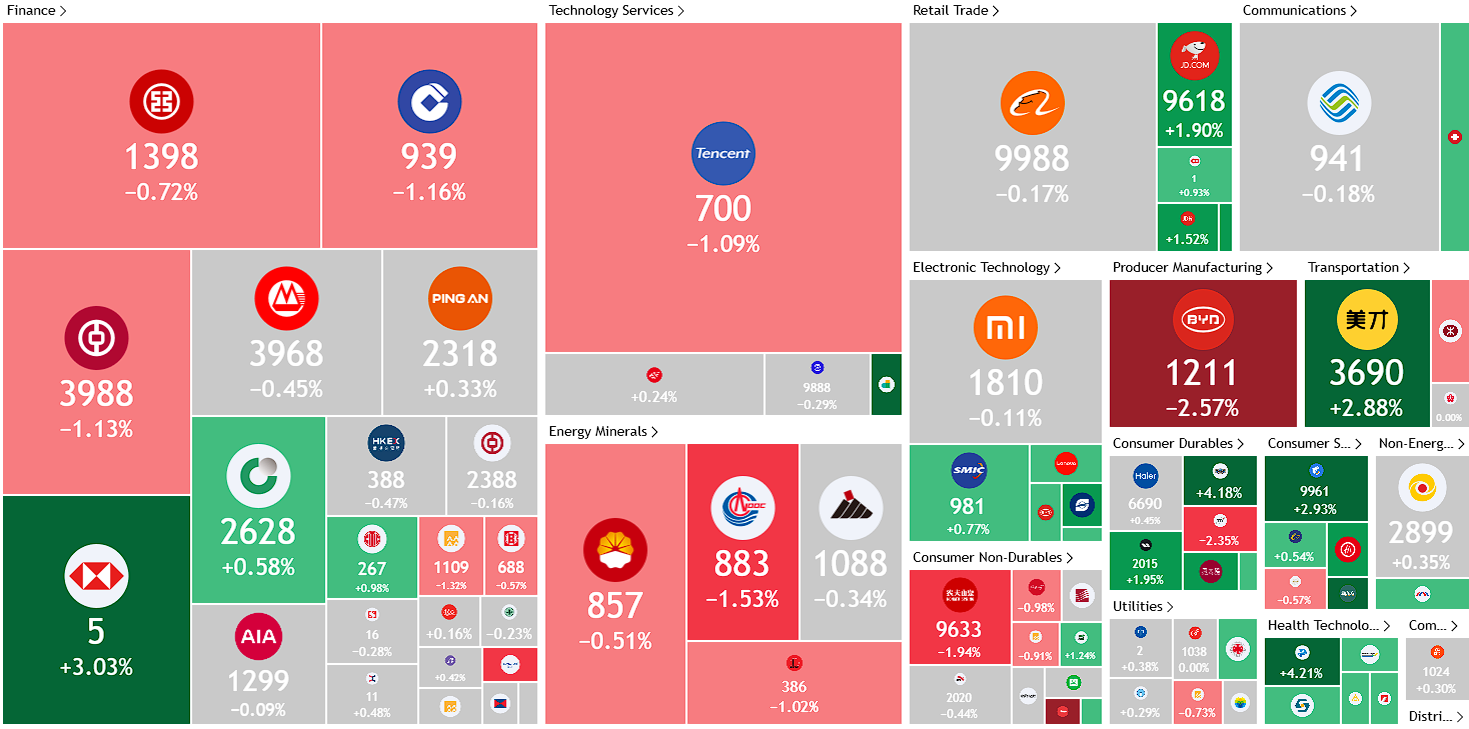

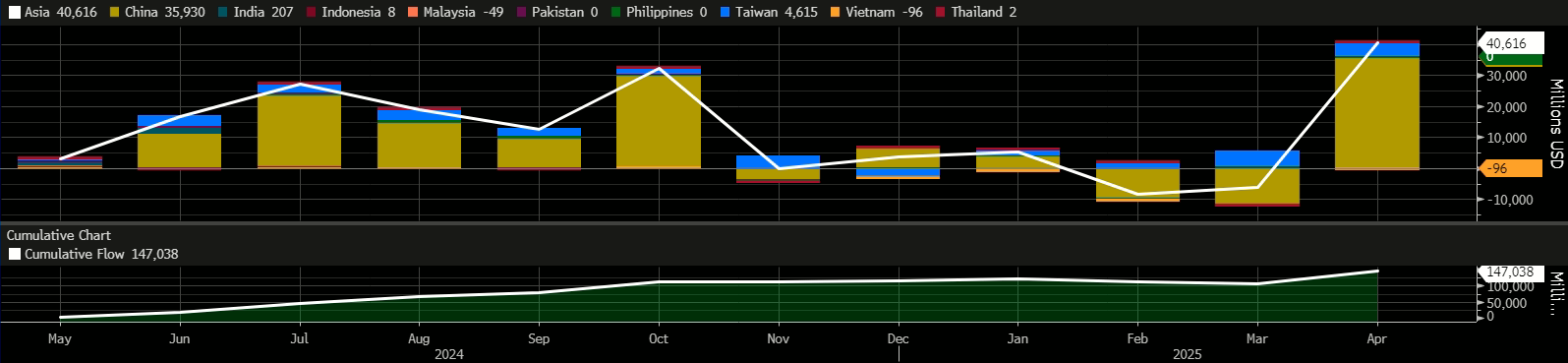

Fund reallocation to emerging markets. The continued depreciation of the U.S. dollar, driven by U.S. policy instability and heightened trade tensions, has prompted investors to reduce their exposure to the U.S. market. This loss of confidence in the dollar has increased investment in emerging markets. The Hong Kong stock market continued its recovery, with Hang Seng Index regaining over half of the losses incurred after the 7 April tariff announcement. Positive sentiment is supported by capital outflows from the U.S. and growing interest in undervalued Hong Kong stocks, especially amid AI innovation progress. This recovery and renewed investor confidence signal a stronger outlook for the Hong Kong market, enhancing its appeal as a global investment destination. In April, Asia recorded the highest positive net inflows YTD, signalling increased investor confidence.

Fund flow – Asia

(Source: Bloomberg)

Supportive Monetary Policy. People’s Bank of China (PBOC) Deputy Governor Zou Lan recently reaffirmed that China’s monetary policy remains accommodative and relatively loose. With potential interest rate and reserve requirement ratio (RRR) cuts on the horizon, liquidity conditions are expected to improve. A supportive monetary environment would benefit HKEX by lowering financing costs, stimulating economic activity, and strengthening investor confidence, all of which could lead to higher trading volumes and an uptick in new listings.

Bracing for headwinds. China’s central bank, the People’s Bank of China (PBOC), is ramping up monetary support by injecting 600 billion yuan through its medium-term lending facility (MLF) to cushion the economy from the impact of aggressive US tariffs. This would result in a net injection of 500 billion yuan for April, the largest since December 2023. The move signals a supportive policy stance aimed at maintaining liquidity as government bond issuance picks up and demand for cash rises due to upcoming holidays. Despite previously downplaying the MLF tool, the PBOC is now using it to help offset pressure from maturing reverse repo agreements and to ease monetary conditions without immediately resorting to cutting banks’ reserve requirements. This increased liquidity and policy easing stance boosts investor confidence and market sentiment, providing a positive catalyst for companies listed on the HKEX.

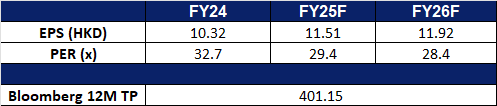

FY24 results review. Revenue increased by 12.3% YoY to HK$17.3bn in FY24, compared with HK$15.4bn in FY23. Net profit increased by 9.8% to HK$13.2bn in FY24, compared to HK$12.0bn in FY23. Basic EPS increased to HK$10.32 in Fy24, compared to HK$9.37 in FY23.

Market consensus.

(Source: Bloomberg)

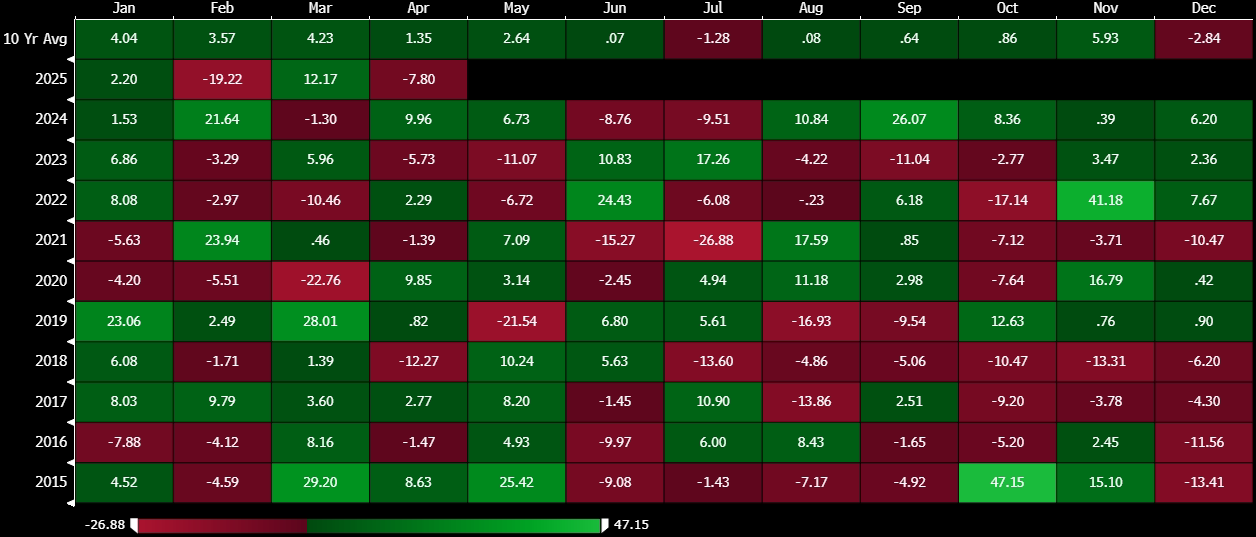

Trip.com Group Ltd. (9961 HK): Upcoming seasonality play

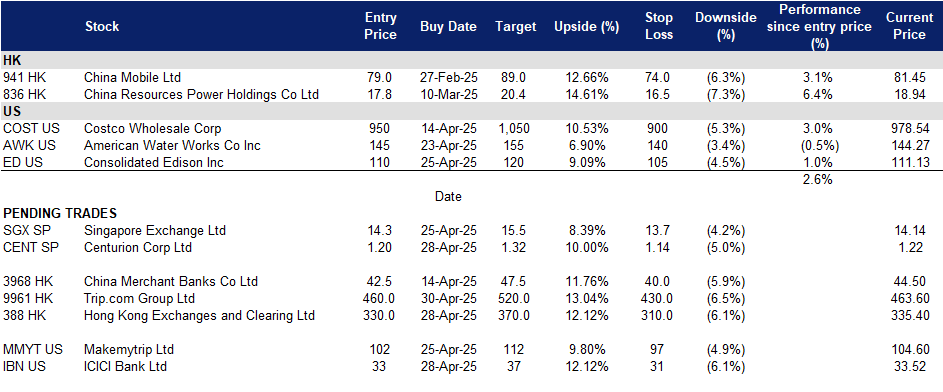

BUY Entry – 460 Target – 520 Stop Loss – 430

Trip.com Group Ltd is a China-based company mainly engaged in the operation of one-stop travel platform. The Company’s platform integrates a comprehensive suite of travel products and services and differentiated travel content. Its platform aggregates its product and service offerings, reviews and other content shared by its users based on their real travel experiences, and original content from its ecosystem partners to enable leisure and business travelers to have access to travel experiences and make informed and cost-effective bookings. Users come to its platform for any type of trip, from in-destination activities, weekend getaways, and short-haul trips, to cross-border vacations and business trips.

Upcoming May Day Holidays. The May Day holidays in China, officially observed from May 1 to May 5, are expected to drive a significant uptick in travel activity. The holiday travel rush is anticipated to span from April 29 to May 6, with peak passenger flow projected on May 1. Short-haul outbound travel is showing strong momentum, supported by rising demand for both group tours and independent travel. Market data reveals a 60% year-over-year increase in group tour bookings and a 29% rise in independent travel among mainland Chinese tourists. Additionally, flight bookings for the holiday period have exceeded 750,000 for both outbound and inbound routes. This surge in travel demand is likely to benefit Trip.com Group Ltd. positively.

Trip.com Group share price seasonality chart

(Source: Bloomberg)

New Initiatives to Attract Consumers. Trip.com Group recently launched its 2025 Word-of-Mouth Travel Rankings, offering users a fresh way to explore global destinations across its platforms. The rankings feature 16 themed global lists and “Recommended Itineraries,” combining user reviews, AI-driven insights, and curated content to streamline the travel planning process—from inspiration to booking. These itineraries link top-rated hotels, attractions, restaurants, and nightlife experiences, reflecting real user journeys and enabling personalized planning through Trip.com’s intelligent recommendation system. Travelers can explore seasonal highlights, save customized routes, and receive tailored suggestions based on their preferences and travel dates. The rankings cover 291 destinations, over 1,500 hotels, 800 attractions, 800 restaurants, and nearly 400 night tour options—enhancing the overall user experience and engagement on the platform.

Expanding Strategic Partnerships. Trip.com has also deepened its partnership with Emirates, further integrating flights, hotels, and loyalty programs to enrich travel offerings in key global markets. The next phase of this collaboration will focus on unlocking growth opportunities in new markets and customer segments. Both companies plan to expand Trip.com’s global footprint by leveraging Emirates’ extensive international network and coordinating joint promotional campaigns, particularly in Asia and Europe—strategic regions for both partners.

FY24 earnings. Revenue increased by 19.8% YoY to RMB53.4bn in FY24, compared to RMB44.6bn in FY23. Net Profit increased by 72.2% to RMB17.2bn in FY24, compared to RMB10.0bn in FY23. Basic earnings per share is RMB26.1 in FY24, compared to a basic earnings per share of RMB24.8 in FY23.

Market consensus.

(Source: Bloomberg)

ICICI Bank Ltd (IBN US): Growth expectations remain strong

ICICI Bank Limited operates as a bank. The Bank offers saving accounts, loans, debit, credit cards, insurance, investments, mortgages, and online banking services. ICICI Bank serves customers worldwide.

India’s economic growth remains robust. Although the IMF and the Reserve Bank of India (RBI) have slightly downgraded their GDP growth forecasts for India in 2025 (IMF from 6.5% to 6.2%; RBI from 6.7% to 6.5%), strong domestic demand, improving inflation (with retail inflation dropping to 3.34% in March), and ongoing policy support indicate that India’s financial system exhibits good resilience. The Industrial Credit and Investment Corporation of India is also expected to benefit from India’s long-term economic growth trends.

Reserve Bank of India has relaxed liquidity requirements. Recently, the RBI eased the regulatory requirements for the Liquidity Coverage Ratio (LCR), which is expected to increase the LCR by about 600 basis points, releasing more available capital. This will further enhance the bank’s lending capacity and help it seize credit recovery opportunities following interest rate cuts.

Financial health is strong. The bank’s deposits grew by 11.4% year-on-year to $173.9 billion in Q4 of FY25 (ending March 2024). Domestic loan growth increased by 13.9% to $153.4 billion. The net non-performing asset (NPA) ratio stands at 0.39%. The total capital adequacy ratio is at 16.55%, with a CET-1 ratio of 15.94%.

3Q25 results. ICICI Bank delivered an increase in revenue to US$3.27bn above the consensus of US$3.24bn. Earnings per share was US$0.40, beating expectations by US$0.02. Net profit increased by 14.8% YoY to US$1.4bn (₹11,792 crore) in 3Q25. Net interest income (NII) increased to US$2.4bn (₹20,371 crore), up by 9.1% YoY. Net interest margin was at 4.25% in 3Q25 compared to 4.27% in 2Q25 and 4.43% in 3Q24.

Market consensus

(Source: Bloomberg)

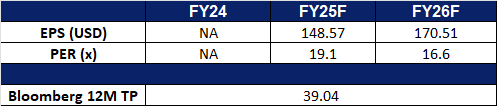

MakeMyTrip Ltd (MMYT US): Increase in travel demand

Makemytrip Ltd. offers travel services over the Internet. The Company operates websites that allow travelers to research and plan trips and book airline tickets, hotels, packages, rail tickets, bus tickets, and rental cars. Makemytrip also offers access to travel insurance.

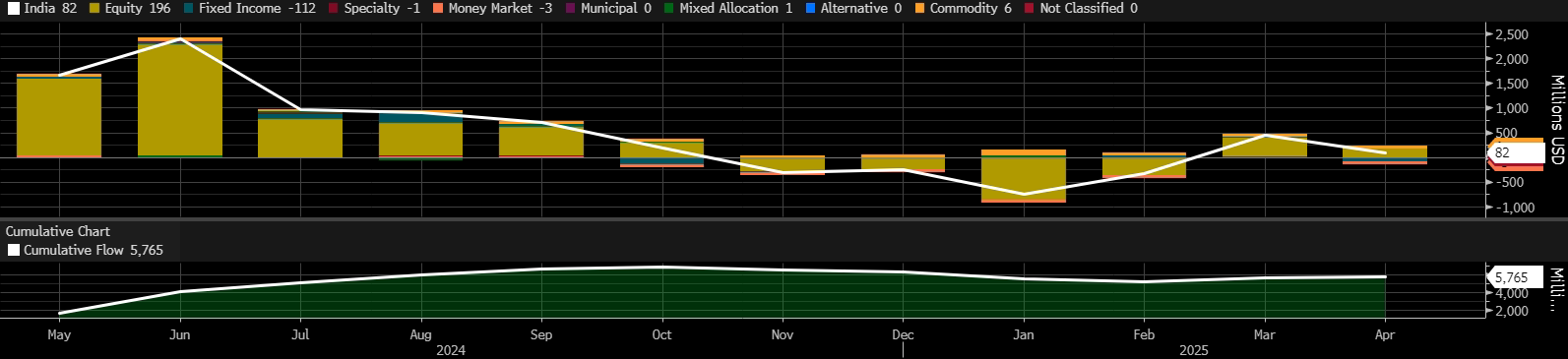

Fund reallocation to emerging markets. The continued depreciation of the U.S. dollar, driven by U.S. policy instability and heightened trade tensions, has prompted investors to reduce their exposure to the U.S. market. This loss of confidence in the dollar has increased investment in emerging markets. According to the IMF, India is a key beneficiary due to its forecasted 2025 GDP growth of 6.2%. After four months of net outflows of funds from India, India recorded positive net inflows since March, especially in its equities market, signalling increased investor confidence.

Fund flows – India

(Source: Bloomberg)

Capitalizing on growing middle class. Fuelled by India’s expanding middle class Federation of Indian Chambers of Commerce & Industry (FICCI) forecasts India’s outbound tourism market to reach US$55.4bn by 2034, with an annual compound growth rate exceeding 11%. MakeMyTrip is strategically positioned to capitalize on this surge in international travel demand, especially as global destinations increasingly target Indian travellers due to reduced Chinese outbound tourism. By 2027, India is expected to be the fifth-largest outbound market, with spending hitting US$34.2bn in 2023 and expected to surpass US$76.8bn by 2034. India is also the third-largest air passenger market and anticipates adding 960 million new passengers by 2042. The increasing purchasing power of Indians is attributed to the country’s annual economic growth of 6% to 7%, which is expanding its middle and high-income population. MakeMyTrip is strategically poised to capitalize on this growth, particularly given the increased focus on attracting Indian travellers and India’s expanding air passenger market.

IPL boosting domestic tourism. The Indian Premier League (IPL) 2025, held from 22 March to 25 May, is set to significantly boost domestic tourism. As fans travel across cities to support their favourite teams, platforms like MakeMyTrip are uniquely positioned to capitalize on this trend by meeting the growing demand for experience driven travel. IPL hosting cities have seen a surge in bookings, with the rise of community based stays and match themed packages reshaping seasonal travel behaviours, particularly among Gen Z and millennial travellers. This trend presents a strategic opportunity for MakeMyTrip to strengthen its market presence through curated offerings that integrate sport and convenience. In 2019, the IPL attracted nearly 400,000 domestic and international tourists, generating $68mn in direct hospitality revenues. Following pandemic related disruptions, IPL 2025 signifies a robust resurgence, solidifying sports tourism as a key driver of India’s domestic travel landscape. As the league continues to grow, it will continue to drive significant growth in tourism, hospitality, and local economies nationwide, benefitting MakeMyTrip domestic travel revenue.

3Q25 results. MakeMyTrip delivered a 24.8% YoY increase in revenue to US$267.36mn, surpassing estimates by US$2.24mn. GAAP earnings per share were US$0.23, beating expectations by US$0.01.