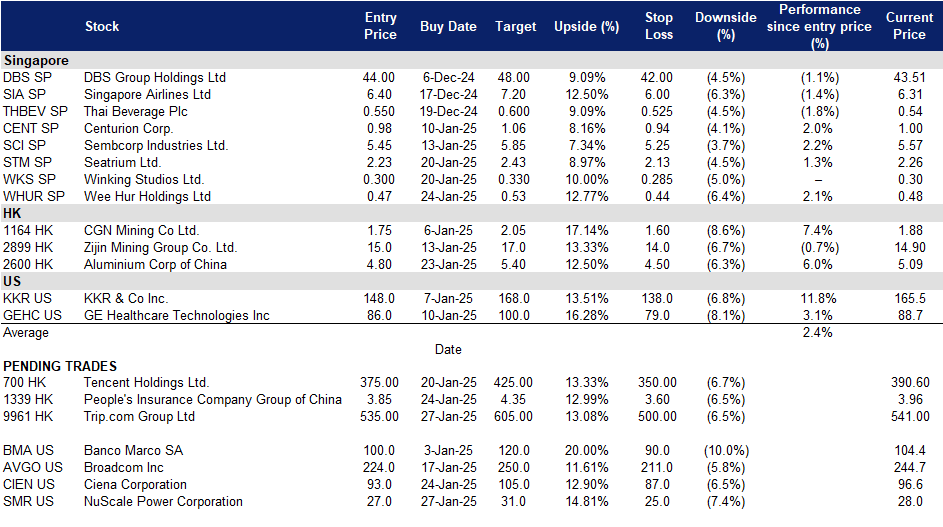

27 January 2025 : Wee Hur Holdings Ltd (WHUR SP), Trip.com Group Ltd. (9961 HK), NuScale Power Corp (SMR US)

Sector Performance | Hong Kong Trading Ideas |United States Trading Ideas | Singapore Trading Ideas| Trading Dashboard

United States

Hong Kong

Wee Hur Holdings Ltd (WHUR SP): Strategic repositioning

- RE-ITERATE BUY Entry – 0.47 Target– 0.53 Stop Loss – 0.44

- Wee Hur Holdings Ltd provides building construction services and acts as the management or main contractor in construction projects for both private and public sectors. The Company’s clients from the private sector include property owners and developers, and those from the public sector comprise government bodies and statutory boards.

- Increased construction demand in Singapore. Wee Hur Holdings showcased robust performance in the first half of 2024, underpinned by its strong dormitory segment and increased contributions from investments in associates and joint ventures. A key strength lies in its Tuas View Dormitory, which saw higher revenue as rising construction demand in Singapore drove the need for worker accommodation. As a BCA-registered A1-grade contractor, Wee Hur is well-positioned to tender for public projects of unlimited value, spanning residential, commercial, industrial, and conservation projects, further solidifying its expertise in the construction sector. The recent sale of its Australian PBSA portfolio has provided the company with additional capital flexibility, enabling it to focus on core segments like construction and dormitories. With Singapore’s construction demand projected to reach S$47bn to S$53bn in 2025, fuelled by major projects such as Changi Airport Terminal 5 and public housing developments, Wee Hur is poised to capitalize on these opportunities. Its diversified capabilities, including expertise in new constructions, refurbishments, and heritage restoration, further enhance its versatility and competitive edge in the market. These strengths position Wee Hur to thrive amid Singapore’s growing infrastructure and construction needs.

- Capitalising on sale of assets. Wee Hur Holdings sold its Australian student accommodation assets for A$1.6bn to Greystar, generating S$320mn in cash and retaining a 13% stake worth A$200mn in the new venture. The portfolio, comprising over 5,500 beds, has benefited from high occupancy rates and rising rental income. Wee Hur intends to allocate the proceeds toward expanding its construction and engineering business and exploring alternative investment opportunities. The sale also enabled the company to clear associated debt, strengthening its financial position. Additionally, Wee Hur continues to advance other key projects, including the development of new worker dormitories and student accommodations. Looking ahead, investors are optimistic about the potential for special dividends once the company receives the net proceeds from the transaction, further enhancing shareholder value.

- 1H24 results review. Total revenue for 1H24 increased by 10% YoY to S$109.12mn from S$99.21mn driven by higher contributions from Tuas View Dormitory, the Group’s first Purpose-Built Dormitory in Singapore, which operated at nearly full occupancy throughout 1H24. Gross profit for 1H24 surged to S$44.73mn, an increase of 144% YoY from S$18.30mn in 1H23. Profit from continuing operations for 1H24 was S$75.07mn, an increase of 488% from S$12.77mn the year before, this was mainly attributable to improved performance at Tuas View Dormitory and higher profits from investments in associates and joint ventures.

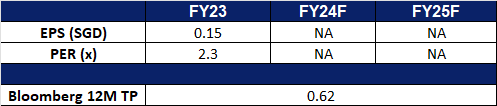

- Market Consensus.

(Source: Bloomberg)

Winking Studios Ltd (WKS SP): Continued momentum from M&A strategy

- RE-ITERATE BUY Entry – 0.300 Target– 0.330 Stop Loss – 0.285

- Winking Studios Limited operates as a game art outsourcing studio. The Company provides complete end-to-end art outsourcing and game development services across various platforms for the video games industry. Winking Studios serves customers worldwide.

- New acquisition. On 17 January, Winking Studios announced plans to acquire Shanghai Mineloader Digital Technology, a leading Asian game art outsourcing and development studio, for approximately RMB 146mn (S$27.2mn). Mineloader, with 466 employees and a strong focus on console platform games, generates 90% of its revenue from game art outsourcing. For the financial year ending 31 December 2023, Mineloader delivered EBITDA of approximately S$3.6mn. This deal aims to expand Winking Studios’ scale in Asia, access Western clients, and support global ambitions. Completion of the proposed acquisition is expected by 2Q25, with Mineloader’s leadership continuing under Winking Studios’ resources and expertise.

- M&A focused. Winking Studios’ largest peer Keywords Studios was previously listed on AIM in 2013, valued at £49mn. It was then acquired for £2.1bn, rewarding investors as the business grew 40-fold by providing services like music, art, and translation for video games. Winking Studios leverages key industry trends like art outsourcing and mobile gaming, attracting major clients like Ubisoft and EA. With a focus on high-quality, cost-effective services and a strong foundation with Acer as a major shareholder, Winking aims to replicate Keyword’s success. This includes organic growth, strategic acquisitions, and leveraging AI to enhance its offerings. As Winking Studios continues to execute its growth strategy and demonstrates increasing value, we anticipate its SGX share price to follow suit and expect continued strong performance and attractive returns for investors.

- Joint AI development project. Winking Studios entered a supplementary agreement with Acer for the second phase of their joint AI project to develop GenMotion.AI, a 3D animation generation tool. Acer will contribute US$200,000, with Winking providing resources. Both companies will share intellectual property 50/50 for any new inventions. GenMotion.AI converts text input into detailed 3D animations, enhancing efficiency and creativity for animators. GenMotion.AI leverages Winking’s proprietary, traceable training data, aiming to lead the way in AI adoption for digital art. The tool is expected to revolutionize workflows by improving visual quality, production speed, and ultimately, revenue per worker. This collaboration strengthens Winking’s position to handle more projects with tighter deadlines or larger projects, without the need for more manpower, unlocking significant growth potential.

- 1H24 results review. Total revenue for 1H24 increased by 7.1% YoY to US$15.23mn driven by strong growth in the Art Outsourcing Segment and Game Development segment, which saw a 6.6% and 8.1% rise respectively.

- We have fundamental coverage with a BUY recommendation and a TP of S$0.35. Please read the full report here.

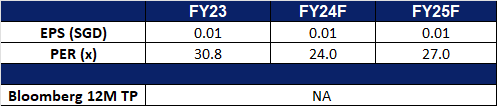

- Market Consensus.

(Source: Bloomberg)

Trip.com Group Ltd. (9961 HK): Surge in Chinese New Year Travellers

- BUY Entry – 535 Target – 605 Stop Loss – 500

- Trip.com Group Ltd is a China-based company mainly engaged in the operation of one-stop travel platform. The Company’s platform integrates a comprehensive suite of travel products and services and differentiated travel content. Its platform aggregates its product and service offerings, reviews and other content shared by its users based on their real travel experiences, and original content from its ecosystem partners to enable leisure and business travelers to have access to travel experiences and make informed and cost-effective bookings. Users come to its platform for any type of trip, from in-destination activities, weekend getaways, and short-haul trips, to cross-border vacations and business trips.

- Surge in Chinese New Year travelers. Train stations and airports across China experienced a surge in travelers on January 25, as millions returned home ahead of Chinese New Year. This annual migration, anticipated to break records, marks a significant cultural tradition as families reunite to celebrate. The holiday season officially begins on January 29, 2025, with eight consecutive public holidays offering opportunities to share festive meals, attend traditional performances, and enjoy firecrackers and fireworks. During the traditional 40-day travel period surrounding the holidays, an estimated nine billion interprovincial passenger trips are expected across all modes of transport. The Ministry of Transport projects approximately 510 million train journeys and 90 million air trips during this time. This massive travel wave presents a significant opportunity for Trip.com, which stands to benefit from the heightened demand for transportation bookings and travel-related services, solidifying its position as a key player in facilitating seamless travel experiences during peak seasons.

- New experiences. Zhangjiajie, one of China’s most iconic and breathtaking natural destinations, has partnered with Trip.com Group to offer international travelers captivating experiences in 2025. Announced during the “Fairyland Zhangjiajie, Enchanting the World” event in early January, this strategic collaboration marks a significant step in advancing the region’s tourism development. Co-hosted by the Zhangjiajie Municipal Bureau of Culture, Sports, Tourism, Radio & Television and Trip.com Group, the event welcomed global travel influencers from 12 countries and regions, including the UK, South Korea, Japan, Spain, Australia, Canada, Belarus, South Africa, Colombia, Nepal, Ukraine, and Hong Kong. These influencers experienced Zhangjiajie’s breathtaking landscapes, vibrant culture, and unique offerings firsthand. By showcasing its natural beauty and cultural richness to an international audience, Zhangjiajie aims to establish itself as a must-visit destination for 2025, driving an anticipated surge in inbound travel to China.

- Free layover tour to attract more travelers. Trip.com Group has introduced a complimentary half-day tour of Beijing for international transit passengers with layovers of eight hours or more. This initiative aims to attract and serve global travelers by showcasing Beijing’s beauty and offering a glimpse into Chinese culture. The tour includes free shuttle services, multilingual guides, attraction tickets, and complimentary internet access, ensuring a seamless and enjoyable experience for passengers. The service is available at the designated gathering point in Terminal 3 of Beijing Capital International Airport and has already been embraced by travelers from nearly 50 countries, including Australia, the United Kingdom, Germany, France, and Singapore. This initiative not only enhances the travel experience for transit passengers but also strengthens Trip.com Group’s brand as a leader in customer-centric travel solutions. By introducing travelers to Beijing’s attractions, the company builds goodwill, fosters brand loyalty, and positions itself to convert transit passengers into future customers, potentially increasing bookings for more extended stays or broader travel itineraries across China.

- 3Q24 results review. Revenue increased 15.6% YoY to RMB15.9bn in 3Q24, compared with RMB13.8bn in 3Q23. Net profit rose by 47.1% to RMB6.82bn in 3Q24, compared to RMB4.63bn in 3Q23. Basic earnings per share increased to RMB10.37 in 3Q24, compared to RMB7.05in 3Q23.

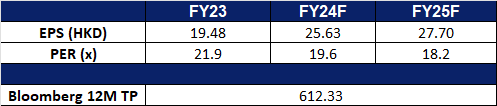

- Market consensus.

(Source: Bloomberg)

People’s Insurance Company Group of China Ltd. (1339 HK): New stimulus measures

- RE-ITERATE BUY Entry – 3.85 Target – 4.35 Stop Loss – 3.60

- People’s Insurance Company Group of China Ltd is a holding company that mainly provides insurance products. The Company and its subsidiaries are mainly engaged in property insurance, health insurance, life insurance, reinsurance, Hong Kong insurance, pension insurance and operating insurance business. The property insurance business mainly includes providing property insurance products for companies and individuals, including motor vehicle insurance, agricultural insurance, property insurance and liability insurance. The health insurance business mainly includes health and medical insurance products. The life insurance business mainly includes life insurance products, including dividends, whole life, annuities and universal life insurance products. The Hong Kong insurance business includes property insurance business in Hong Kong, China. The pension insurance business includes business such as enterprise annuities and occupational annuities.

- New stimulus measures. China recently unveiled a series of measures designed to bolster the domestic stock market. Among these initiatives, the Chinese government plans to roll out the second phase of a pilot program in the first half of 2025, enabling insurance funds to make long-term equity investments. This phase will have a minimum scale of 100bn yuan ($13.7bn). The program permits insurance companies to establish securities investment funds dedicated to long-term stock market investments, with 50 bn yuan set to be approved before the Spring Festival to inject additional capital into the market. The program’s scope is expected to expand gradually over time. During the initial phase, which involved 50bn yuan, the funds achieved solid returns. These measures are poised to deliver sustained benefits to insurance companies in the long term.

- Expanding presence through partnerships. China People’s Property and Casualty Insurance Company (PICC P&C), a subsidiary of the People’s Insurance Company (Group) of China, has recently formed a strategic partnership with AXA Hong Kong & Macau and AXA Tianping P&C Insurance. This collaboration is centered on driving the growth of Hong Kong’s auto insurance market, with a particular focus on new energy vehicles (NEVs). By leveraging shared market insights, distribution channels, and technical expertise, the partnership aims to enhance insurance services for electric and other NEVs in the region. Key initiatives include expanding service offerings, developing innovative insurance products, and strengthening the companies’ market presence. Together, the three entities seek to combine their strengths to deliver superior solutions and support the evolving needs of Hong Kong’s auto insurance sector.

- 3Q24 results review. Revenue increased 28.5% YoY to RMB177.3bn in 3Q24, compared with RMB138.0bn in 3Q23. Net profit rose significantly to RMB13.6bn in 3Q24, compared to RMB622mn in 3Q23. Basic earnings per share significantly increased to RMB0.31 in 3Q24, compared to RMB0.01in 3Q23.

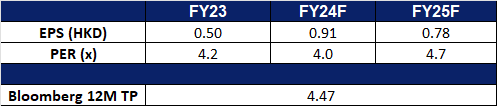

- Market consensus

(Source: Bloomberg)

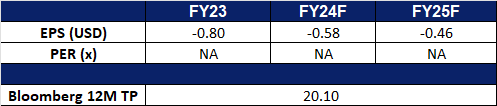

NuScale Power Corp (SMR US): Meeting energy demands

- BUY Entry – 27 Target – 31 Stop Loss – 25

- NuScale Power Corporation operates as a small modular reactor (SMR) technology company. The Company provides scalable advanced nuclear technology for the production of electricity, heat, and clean water. NuScale Power serves customers worldwide.

- Surging electricity demand. The International Energy Agency (IEA) expects a significant rise in electricity demand driven by advancements such as electric vehicles, data centers, and artificial intelligence (AI). To meet this demand it necessitates a shift toward low-emission energy sources, with nuclear power taking center stage. NuScale Power Corporation is well-positioned to meet this growing need. Its VOYGR™ SMR power plants, with modular configurations generating up to 924 MWe, provide scalable solutions for diverse energy requirements. Factory-based construction of these reactors enables faster deployment and reduced costs compared to traditional large-scale reactors, aligning with the IEA’s call for cost-effective nuclear expansion. NuScale’s global presence is expanding, evidenced by its agreement to build a VOYGR-12 SMR in Ghana. This project highlights the growing demand for innovative nuclear technology to support both rising energy needs and decarbonization efforts worldwide. With governments and industries seeking reliable, sustainable energy sources, NuScale’s cutting-edge SMR systems are poised to play a pivotal role in reshaping the energy landscape.

- AI-infrastructure plans. The global demand for energy is surging, driven by advancements in artificial intelligence (AI) and other power-intensive technologies. Massive investments, such as the US$500 billion Stargate AI initiative supported by OpenAI, SoftBank, Oracle, and President Trump, highlight the immense power needed to sustain AI-driven data centers and applications across industries like healthcare, transportation, and finance. These data centers rank among the most energy-intensive infrastructures globally, with consumption expected to rise significantly as AI continues to proliferate. Traditional energy sources alone are insufficient to support this unprecedented growth, sparking renewed interest in nuclear energy as a reliable, low-emission alternative. South Carolina’s decision to revive its massive nuclear project further underscores the growing recognition of nuclear power as essential for meeting rising energy demands fuelled by AI and other emerging technologies. Beyond AI, sectors such as electric vehicles, cryptocurrency mining, and cloud computing also contribute to the escalating energy requirements, making NuScale Power Corporation’s solutions increasingly relevant. As industries and governments seek dependable power sources to fuel technological advancements and achieve sustainability goals, NuScale’s SMR systems emerge as a vital component in addressing the energy challenges of the future.

- 3Q24 results. NuScale Power Corporation’s revenue declined by 93.1% YoY to US$0.5mn in 3Q24 from US$7.0mn in 3Q23, below estimates by US$10.2mn. It delivered GAAP EPS of -US$0.18, below estimates by US$0.03. The company delivered a net loss of US$45.5mn in Q3 compared to a net loss of US$58.3mn in the prior year.

- Market consensus

(Source: Bloomberg)

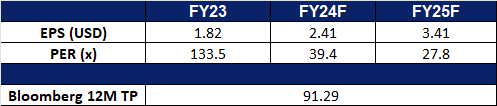

Ciena Corporation (CIEN US): Dominating the optical networking space

- RE-ITERATE BUY Entry – 93 Target – 105 Stop Loss – 87

- Ciena Corporation develops and markets communications network platforms, software, and offers professional services. The Company’s broadband access, data and optical networking platforms, software tools, and global network services support worldwide telecom and cable/MSO services providers, and enterprise, and government networks.

- Cloud and AI driven traffic. The company’s fourth-quarter earnings exceeded Wall Street expectations, with robust revenue and strong order flow highlighting the growing demand for cloud and AI-driven bandwidth across networks. As AI remains a central focus in the coming year, Ciena Corp. is well-positioned to capitalize on this trend, driving accelerated revenue growth and market share expansion. As a leading provider of networking systems and software services, Ciena stands to benefit significantly from the anticipated surge in AI-related traffic. Its expertise in optical networking, enabling high-speed data transmission over long distances, will be a key differentiator in modern telecommunications, where speed and reliability are critical. Additionally, Ciena’s advanced 1.6 Tb/s and 800G coherent Coherent-Lite pluggable solutions are designed to help cloud and data center providers manage the exponential growth in cloud, machine learning, and AI traffic. With major projects like the Stargate AI data center and other large-scale data center initiatives underway, Ciena is poised to see increased demand for its optical networking equipment and inventory management solutions, streamlining operations for its customers. Supported by substantial investments from cloud customers and telecom operators, Ciena’s growth prospects remain strong, solidifying its position as a key player in the AI and cloud infrastructure landscape.

- Secured new term loan. Ciena Corporation refinanced its existing senior secured term loan with a US$1.16bn loan maturing in October 2030. Proceeds from the new loan, along with cash, were used to fully repay the previous loan. The loan features quarterly amortization payments, a SOFR-based interest rate, and early repayment options. This refinancing aims to optimize Ciena’s capital structure and enhance financial flexibility while maintaining consistent terms with the prior agreement.

- Connectivity milestone achieved. Southern Cross Cable Limited has achieved a significant milestone by implementing the world’s first 1 Tb/s single-carrier wavelength across its 13,500 km transpacific network, utilizing Ciena’s cutting-edge WaveLogic 6 Extreme (WL6e) coherent optics. This groundbreaking achievement underscores the exceptional performance and scalability of Ciena’s technology in meeting the surging demands of today’s digital world. By leveraging WL6e, Southern Cross enhances its network capacity and efficiency, enabling it to deliver high-bandwidth services critical for AI, cloud computing, and video applications. This deployment demonstrates the power of Ciena’s technology to support the growing bandwidth needs of global connectivity.

- 4Q24 results. Ciena Corporation’s revenue declined slightly by 0.9% YoY to US$1.12bn in 4Q24 from US$1.13bn in 4Q23, above estimates by US$20mn. It delivered non-GAAP EPS of US$0.54, below estimates by US$0.11. The company repurchased approximately 2.1mn shares of common stock for the aggregate price of US$132mn during the quarter. The company maintains a long-term revenue growth target of 6-8% CAGR, driven by webscale and cloud provider market growth.

- Market consensus

(Source: Bloomberg)

Trading Dashboard Update: Add Wee Hur Holdings Ltd (WHUR SP) at S$0.47.